Just when the dairy industry was getting used to back-to-back price rises at the Global Dairy Trade auctions, we have a negative result dropped in. Not large, at least at the weighted average price level with only a -0.7% change, but for WMP this extends to a -2.7% drop. A summary is below;

- WMP down -2.7% (US$2,971)

- SMP up +2.3% (US$2,724)

- Butter down -1.6% (US$4,890)

- Cheddar up +4.5% (US$4,042)

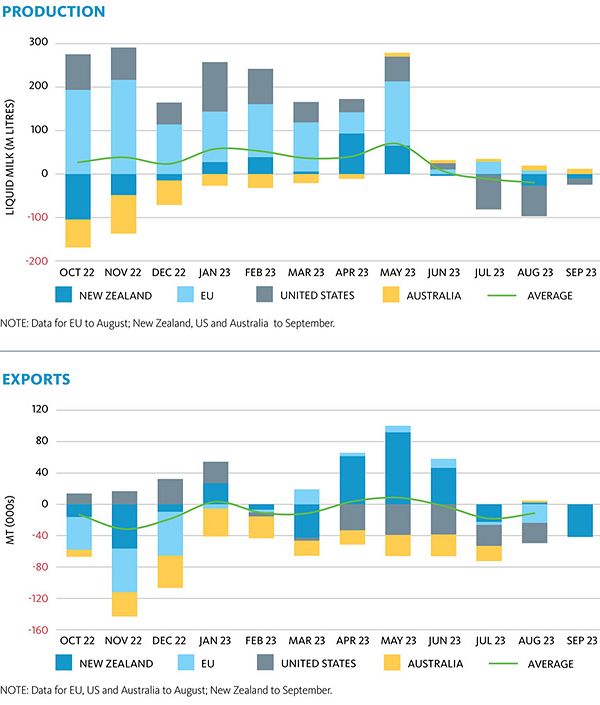

Even though both cheddar and SMP were up the overall negative result shows the impact the heavily weighted WMP component has on the average price and is the major driver to the farm gate price. While all expect the usual ups and downs through the season and this one is not a major cause for concern except it comes at a time when milk production world wide is lower than the previous year and exports are down (from Fonterra). (see graphs below).

Source: Fonterra

On top of the lower production the predicted onset of El Nino weather is expected to bring more production challenges for New Zealand and likely also Australia. Just as an aside on EL Nino, this year was predicted to be very similar to the 1982-83 season. So far, fortunately it has been anything else but similar. That year was challenging right from the early spring onwards (the drought it became broke April 16th, our wedding day so remember it well). This year keeps supplying regular rainfall although we do expect them to stop.

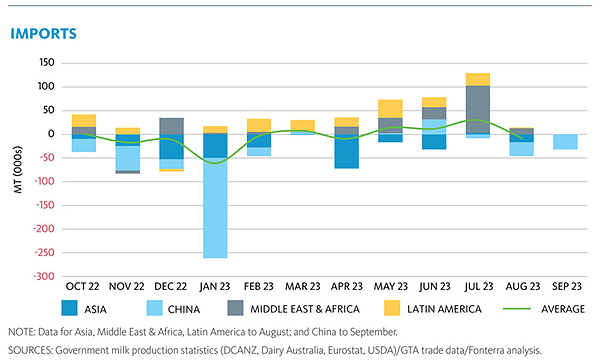

Back to milk returns, the problem (as can be seen below) is still obviously the lack of demand from China.

The reports coming out of China are that the resurgence is (still) occurring and an increase in GDP of +5.4% is expected this year (IMF report) reducing to +4.6% for 2024. The other continued relevance piece is that Rabobank have reported that “China is poised to become the third largest dairy producer globally”. Perhaps the influences on China’s domestic market as reported back in August are already making their impact.

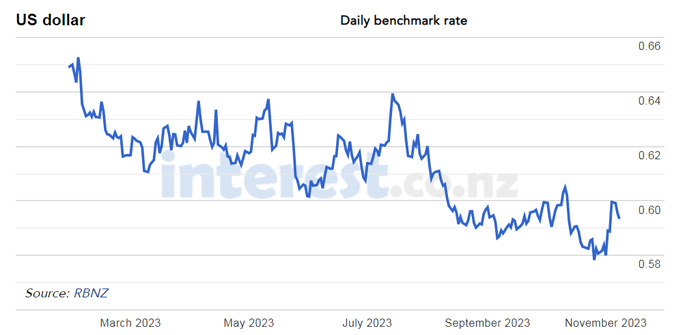

While banks have still been on the positive side in their forecasts, the best thing to date regarding bank forecasting is that they have been out over forecasting the NZ$ vs the US$ for the current period. Earlier on this year the general consensus was for a US$0.62 vs the NZ$ for the latter part of 2023. The recent rate has been around 59 US cents. The low dollar for farmers in general is doing more to support farmer returns than anything else in exports.

Sheep meat has not had any great news for quite a while and there is nothing in the outlook that would change this.

MIA reported that exports for the year to 30 September were $10.2 billion, down 11% on the same period last year and down 18% for the month of September. There is a double compounding reason for this.

One is that China has reduced both imports and what it is prepared to pay and Australia in sending far more sheep meat into the USA is effectively pushing New Zealand out of what it would have been hoping to be a substitute market to replace China. To be fair to the Aussies they have been supplying the USA with lamb longer than New Zealand largely due to their larger carcass weights being more accepted there. This year the Australian sheep meat exports are up to the USA due in part to the threat of El Nino and farmers pre-empting a potential drought, as well as the reduced returns from China.

Unfortunately for sheep farmers the local supply and demand conditions will also likely reduce farmgate returns as the processors can reduce what they need to pay to attract livestock as pressures to unload on farms here also begin to be felt.

This characteristic of the meat companies, even when operating as co-ops is the major difference between them and Fonterra. Co-op meat companies do pay a top-up component at the end of the season when the dust settles but it never seems to compensate for the large reductions in schedules farmers face from now through to April.

Hopefully the delay to the worst attributes of El Nino will provide at least some positives for farmers in the meantime although with Northern Hawkes Bay and Tairawhiti getting yet another deluge, a good drought may sound quite attractive at the moment.

1 Comments

Waiting for China to return as a major buyer could be a long slow painful death for our dairy industry .

Their aging and falling population, the collapse of one of their economy's biggest drivers - construction, their increasing internal production amongst other reasons..

Time to move on. Just worry how much of Fonterra's stainless steel is only good for WMP and nothing else.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.