By Keith Woodford*

For some time there has been a view developing within New Zealand that we have too many eggs in the dairy basket. There is also a view that we are over-exposed to China.

I do not share those perspectives, at least when they are expressed in such over-arching and simplistic terms. In contrast, I note that dairy is one of the things we are good at, and that our pastoral dairy resources are not easily put to alternative profitable use.

Yes, we could go back to sheep production, but I do not know where we would profitably sell the increased meat volumes. For beef, there are markets, but most of our beef is a by-product of dairy. It is hard to make money from beef cows.

I also note that China and the Western Pacific Rim are clearly where New Zealand’s economic future lies. With few exceptions, the rest of the world does not need us or want us.

Of course it would be nice to have a more diversified economy, and surely we must strive to achieve this. But there are also some specific realities that we do have to accept, and then work within.

Despite all of the above, I am increasingly concerned about one specific egg within the dairy basket, and that is whole milk powder (WMP). Currently, well over half of our dairy production goes to this one commodity product. In terms of global WMP trade, New Zealand is by far the dominant exporter, followed by the total European Union (EU) at less than one quarter of the New Zealand volume. And China is by far the dominant importer – even in the current problematic year it imports nearly four times as much as Algeria, the next most important country.

There was a time when our WMP exports were more diverse. It is less than ten years since Venezuela was our number one destination for this product. But with oil revenues much reduced, they and other oil-producing countries have stepped back.

In teasing out the WMP story below, for statistical data I have drawn exclusively on the USDA agriculture database as reported at www.indexmundi.com. That data is based on ‘market years’ not calendar years, and these market years vary between countries. Although not perfect, these data are the best that we have. In terms of the big picture it will be reliable. That picture is more than a little worrying.

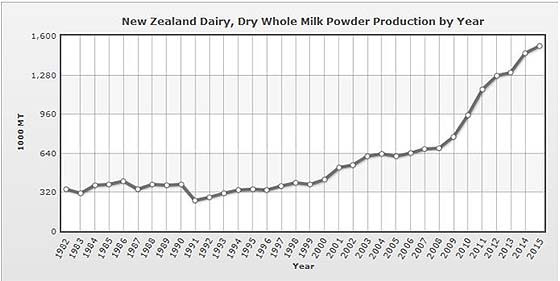

Over the last fifteen years, New Zealand has not only increased dairy production, it has increasingly focused on WMP. There have been huge WMP processing plants constructed at Clandeboye (near Timaru), Darfield, Edendale, Hawera and Pahiatua. These are the most efficient WMP dryers in the world.

In contrast, New Zealand’s focus on cheese, butter, skim milk powders and other dairy products has decreased in proportional terms.

The USDA estimates New Zealand milk powder production for 2015 at at a little over 1.5 million tonnes per annum. This compares to only 420,000 tonnes in 2000 and 680,000 tonnes in 2008.

In fact, so-called ‘New Zealand milk powder’ is not ‘100% Pure New Zealand’. This is because it contains up to 100,000 tonnes of imported lactose. By international standards, New Zealand milk is low in lactose relative to the natural protein and fat. Rather than removing some protein and fat and using these components in other ways, the New Zealand companies bulk it up with cheap imported lactose.

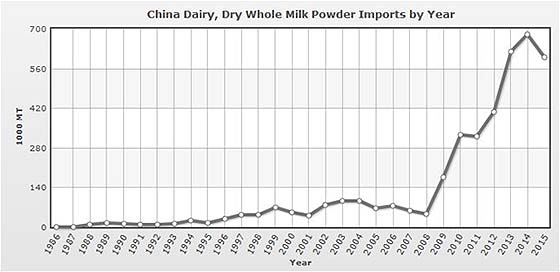

The other big producer of WMP is China, with estimated production for 2015 at 1.35 million tonnes. However, this year China will also import 600,000 tonnes, up from only 49,000 tonnes back in 2008.

Other big producers are Brazil at about 600,000 tonnes, nearly all of it used internally, and the EU at 800,000 tonnes, of which about 450,000 tonnes are exported.

So the overall global picture of WMP is that it is a minor product in the dairy world. Of total global dairy production, less than five percent is converted to WMP.

Essentially, the global WMP story is about China and New Zealand as the big producers, about China as the big consumer, about China as the big importer, and about New Zealand as the big exporter. Quite simply, there is no future for the current WMP industry without China.

So that begs the question as to how reliable is that Chinese market? And why do the Chinese consume so much milk powder relative to everyone else in the world? Over time will they want more or less WMP?

So far, the answer is that Chinese are consuming more and more WMP. Since 2008, consumption has doubled and is still rising at about six percent per year. But there are reasons to suggest that in the long term Chinese will change their buying habits, like every other country, and change to other forms of dairy.

And if that does happen where will New Zealand be?

Working out how the Chinese actually use all of that WMP is not easy. My estimate is that about 500,000 tonnes goes into infant and follow-on formulas. But that is just a rough estimate. A similar amount may get used in other formats including consumer packs, yoghurt and food service.

Almost certainly, the other big use is in reconstituted UHT milk. But for a very simple reason, there are no reliable statistics on this.

The simple reason is that the consumer regulations say that reconstituted milk should be labelled as such. However, my Chinese sources say that in practice this labelling does not happen. Indeed I have never seen it shown on Chinese milk packaging. So what would happen if the Chinese Government enforced this regulation?

The reason why Chinese milk processors like to use imported milk powder for reconstituted UHT milk is that it is cheaper than using locally produced fresh milk.

As long as Chinese manufacturers keep the provenance hidden, or as long as Chinese consumers accept reconstituted product, then our future is secure. But should the situation change, then we are on the back foot.

The conclusions that I draw from this are that long term basing of an industry on WMP is a high risk strategy. It is one of those strategies that might continue to succeed brilliantly as it has for the last 15 years. Or it may prove to be yesterday’s strategy that no longer works.

There are, of course, other strategies that New Zealand could follow. And to be fair to our major dairy processor Fonterra, there are some other eggs, albeit rather small, that are somewhere there in the basket. One example is the new mozzarella cheese factory near Timaru. This cheese will end up on millions of Chinese pizzas.

Another example is liquid milk, be that fresh pasteurised, UHT or the new ESL (extended shelf life) product. Chinese imports of liquid milk (mainly from Europe) have risen 100 fold in the last seven years from 4 million to 400 million litres. Where will they be in another seven years?

Like almost all value-add dairy, these new products require non-seasonal dairy production to be economic and this means new dairy farming systems. I have previously written about those systems, which we need to be researching and adapting for New Zealand conditions.

In writing this article, my aim has been to stimulate debate, not so much about the overall merits of dairy, as about the specifics of WMP. In conducting that debate, we need to remember that WMP can indeed be very profitable, but that it is no more than a basic commodity. It fits brilliantly with our traditional model of seasonal milk production that follows the seasonal pasture production curve. And it fits brilliantly with the Fonterra skill-set as a super-efficient processor. But in the long term, it may well be taking us down a different path to the course that global consumers are taking. For the long term, it sure seems dangerous to have that one big egg dominating the basket.

Keith Woodford is Honorary Professor of Agri-Food Systems at Lincoln University. He combines this with project and consulting work in agri-food systems. This a regular column here. His archived writings are available at http://keithwoodford.wordpress.com.

19 Comments

Interesting that Danone the second biggest Dairy Company in the world behind Nestle,has been operating in NZ for a season,turnover circa 4 to 6 times bigger than Fonterra,operate in 145 countries don't make one ton of WMP or commodity product.

Fonterra is poorly manage governed and about to unravel over the next year.

So now that Danone have purchased the Guardian milk powder plant at Clydevale last year, what will they make there - jelly beans? Danone and Nestle don't have the requirement that a cooperative has of processing and selling all milk produced. They have no loyalty to suppliers, just to shareholders.

The only difference to what is happening now verses the dip in prices 12 years ago is that the market price is very transparent and updated every 2 weeks, whereas this was never the case back then. I Find it interesting every one lays into Fonterra now, but never said a word when there was a $8 plus payout.

The year before Fonterra was formed we got a fantastic payout of $5/kg, the first year of Fonterra it was $5.30/kgMS. The second year it was down to $3.65/kg. The conclusion is that market supply and demand fundamentals always trump marketing/ownership structure.

Essentially, the global WMP story is about China and New Zealand as the big producers, about China as the big consumer, about China as the big importer, and about New Zealand as the big exporter. Quite simply, there is no future for the current WMP industry without China.

I don't agree with Keith on this. September 2013 to February 2014 China took more than 60% of our WMP exports. For the last month statistics are available (July 2015) China took less than 15%.

In July Algeria imported 23,400 tonnes of WMP from NZ compared to China's 14,500 tonnes.

Venezuela: 8,600 tonnes

UAE: 7,700 tonnes

Malaysia, Singapore and Sri Lanka 5,000-6,000 tonnes

Vietnam, Thailand, Taiwan, Saudi Arabia, Nigeria, Libya, Indonesia and Bangladesh 1,000-5,000 tonnes

Algeria will take volume but at a discount. Venezuela pays premiums. Singapore pays less than even Algeria. China pays close to average export prices.

The NZ dairy industry has an issue with over production of milk, and the lower payouts resulting from that.

The WMP story flows from a need to do something with that excess production.

Jeepers Colin, you cannot go around saying these things, they are meant to stay unspoken. You know, the things we know we don't know and the things we don't know we don't know, and the things we think we know that just ain't so.

It ain't what you don't know that gets you into trouble. It's what you know for sure that just ain't so.

Mark Twain

http://www.stuff.co.nz/business/farming/dairy/71862458/fonterras-230-mi…?

The doubling the value of our agricultural exports by 2025 strategy hasn't gone away.

It must though be getting harder to find anyone willing to advocate the strategy.

Colin, I do not argue with your July figures. But what they illustrate is that without China in the market, there is a fundamental oversupply except at very soft prices. No-one else will take up the slack except at very low prices. As for the differences in prices between countries, I think these are largely explained by specification differences. No-one willingly pays a premium relative to other countries and the auction system regulates this. However, WMP from NZ is currently selling at a discount to WMP from other countries; the reasons for that need teasing out. Also, WMP is currently less profitable than cheese, but Fonterra (and some other NZ companies) are locked into WMP by processing constraints. Of course, it is only 18 months ago that WMP was the most profitable of the dairy commodities.

The reason why Chinese milk processors like to use imported milk powder for reconstituted UHT milk is that it is cheaper than using locally produced fresh milk.

until at the stroke of a pen...

http://www.moa.gov.cn/zwllm/zwdt/201501/t20150108_4327632.htm

or http://www.microsofttranslator.com/BV.aspx?ref=IE8Activity&a=http%3A%2F…

On January 7, 2015 China's Ministry of Agriculture issued an emergency notice urging local authorities to adopt measures to ensure that farmers are able to sell their milk. Local officials are ordering dairy companies to keep buying milk from farmers to prevent them from quitting the industry or killing off cows.

looking back at 2014

estimates that [of] the 1.8-million-metric-tons of dairy imports--mostly milk powder--during 2014 constituted one-third of China's milk supply when converted to fluid milk-equivalent. At average output of 6,000 kg per cow, that imports [were] equivalent to 2.3 million lactating dairy cows. [And] that nearly all dairy products, yogurt, baked goods, and confections in China use imported milk powder for at least part of their raw material.

http://dimsums.blogspot.com.au/2015/05/chinese-dairy-balance-or-wipe-ou…

Henry, that is a very good link and should be compulsory viewing for Fonterra, DairyNZ, MPI and Cabinet:

http://dimsums.blogspot.com.au/2015/05/chinese-dairy-balance-or-wipe-ou…

While Chinese and NZ officials may have different perspectives of the world, both cultures appear remarkably similar:

This nuanced view of the dairy industry's future contrasts with the monochrome thinking of Chinese officials who seem unable to comprehend the complexities of the world. Chinese officials cling to a groupthink that views agricultural commodities as uniform, generic products produced by 200 million identical farmers. They generally fail to recognize that there are substitutes for commodities.

who knows what intelligence is going into board and/or policy committee papers... but gee you'd hope its on their reading list, even as background to question the strategy & corp./govt. affairs operatives...

and then take this

https://doc.research-and-analytics.csfb.com/docView?language=ENG&source…

and add from that blog this

http://dimsums.blogspot.com.au/2015_08_01_archive.html

So we see the some of those D20 firms have their own WMP plants, each at different points of the compass. How's that for luck...

Then the other shoe is Australian assets/operations, supermarket lost branded products earnings value, making CER work....

they are big shoes.

a view of the other shoe

http://www.asx.com.au/asxpdf/20150831/pdf/430zmmrjr7wtlg.pdf

see page 4.

and

page 13, note 11 point a.

Dairy's future: agribusiness.

$25 million net asset value, $2 million net loss, $800,000 administration costs and a $250,000 interest free loan from Fonterra Australia.

example dairy analysis ex RBNZ

http://www.reservebank.govt.nz/research_and_publications/official_infor…

A view from within China - released 26/8/2015

MARKET REVIEW

During the first half of 2015, the dairy industry in China has recorded a slower growth rate and the industry growth has been primarily driven by the increase of volume and improvement in product mix.

Amongst the wide variety of dairy products, liquid milk has remained the main product consumed in the Chinese market with milk formula being second.

Amongst liquid milk products, UHT milk was still the most consumed product despite recording a slower growth.

On the other hand, there was still compelling demand for quality healthy products by consumers, while there was a strong boost in product sub–categories such as high–end UHT milk, UHT yogurt, chilled yogurt and lactobacillus drinks.

Currently, the difference in consumption patterns of dairy products in urban and rural areas in China is highly significant. The dairy product consumption of the rural population, which represents 45% of the nation, accounts for less than half of that of urban population, leaving huge room for growth for the

dairy industry in rural areas.

At present, the Chinese dairy industry has achieved great progress in all aspects ranging from upstream raw milk suppliers to downstream dairy enterprises. With joint efforts by the government and enterprises, consumer confidence is gradually recovering. As globalization advances, interaction between the Chinese and overseas dairy product markets is increasing, Chinese dairy enterprises have expedited their efforts to “go global” and have actively commenced strategic cooperation with overseas outstanding dairy enterprises and have forged a strategic network for global milk sources. In the first half of 2015, the growth rate of liquid milk imports has declined. Imported liquid milk only had a marginal impact on the Chinese liquid milk.

During the period, the industry still faced the challenge of an excess supply of raw milk in China. Raw milk prices peaked in February 2014 and dropped continuously until now. The declining cost of raw milk and change in market demand together resulted in intensified market competition. Under these conditions, an optimized product mix can help brand enterprises lift their profit margin.

As for milk formula, the industry is still experiencing fast channel transformation. The maternal and child channel and the e–commerce channel are becoming increasingly important, which is an opportunity as well as a challenge to domestic milk formula enterprises

http://www.mengniuir.com/attachment/2015082623020100002299391_en.pdf

see page 18 and onward

Another view from China (21/08/2015) - highlighting the policy note of 07/01/2015 that seems to have trumped the FTA.

Market Review

For the first half of 2015, China’s milk industry encountered severe challenges — the volume of

imported milk powder kept increasing; certain domestic dairy enterprises have resorted to overseas dairy farms for future cooperation through, for instance, mergers and acquisition with such overseas dairy farms.

All these had led to the shift in raw milk procurement demand to overseas dairy market.

The imbalance between supply and demand in the domestic raw milk market became more acute,

leading to the further decrease in the price of domestic raw milk.

Considering the above and in order to stabilize the market and promote the long-run development of the industry, the Ministry of Agriculture of the PRC promulgated ‘‘ An Urgent Circular on Coordinating and Handling Difficulty in Selling Milk to Stabilize the Production of Dairy Industry’’ («關於協調處理賣奶難穩定奶業生產的緊急通知»)on7 January 2015, indicating PRC government’s awareness in the matter.

On the other hand, as numerous small-scale farms and individual dairy farmers left the market, the entire industry has transformed, under a stricter regulatory environment, from open-range rearing to standardized and brand-oriented intensive rearing, thus benefiting the existing sizable dairy farms. The importance of scientific feeding for milk cows, scientific layout of dairy farms, construction of environmental facilities as well as healthy development of cattle has attracted the industry’s attention.

http://www.ystdfarm.com/uploads/soft/collection/en/LTN20150821456.pdf

and in the minds of others...

one mans export trade life blood, is another mans "bad money drives out good" and market disruptive...

tell us what your really think...

from Modern Dairy.

INDUSTRY OVERVIEW

In general, 2014 is a challenging year for the PRC dairy product industry. In this year, as milk prices in the overseas market declined significantly, and imported bulk milk powder and imported liquid milk products flooded into the PRC market, a large amount of imported milk powder was reconstituted into reconstituted milk, resulting in the phenomenon that “bad money drives out good”, which disrupted the PRC dairy market.

In addition, the domestic dairy enterprises went abroad to acquire or cooperated with overseas ranches, and substantial procurement demands were shifted to the overseas, which intensified the mismatch between supply and demand of domestic dairy products. Within only one year, milk supply shortage was transformed into oversupply, triggering an enormous drop in pricing of the local raw milk in the PRC. Under the plight of continuous drop in milk price, a large number of dairy farmers withdrew from the market and dairy farmers dumped milk and killed cows in some regions.

To address the issue which farmers dumped milk and killed cows due to significant decline in raw milk prices, the Ministry of Agriculture of the PRC issued “An Urgent Circular on Coordinating and Handling Difficulty in Selling Milk to Stabilize the Production of Dairy Industry” (《關於協調處理賣奶難穩定奶業生產 的緊急通知》) on 7 January 2015, pursuant to which all levels of agro-pastoral departments under the leadership of local government shall in best effort manner take immediate action to adopt effective measures in facilitating and dealing with difficulties in selling milk to stabilize dairy production in order to protect the interests of dairy farmers and the long-term development of the industry.

On the other hand, scale farms showed greater advantages due to its stability and security in the supply of raw milk. According to industry statistics, the breeding ratio of current scale farm has exceeded 40%.

In the second half of 2014, the transformation and upgrading pressures faced by the domestic dairy industry increased sharply. Scale farms have become the focus of public attentions. We believe that scale farms are a scientific model and will be the trend in the future...........

http://www.hkexnews.hk/listedco/listconews/SEHK/2015/0323/LTN2015032376…

So, knock, knock: FTA, non-tariff trade barrier who?

FTA's maybe redundant, yesterday's utopia.

A sharp drop in global trade growth this year is underscoring a disturbing legacy of the financial crisis: Exports and imports of goods are lagging far behind the pace during past expansions, threatening future productivity and living standards. Read more

Is it about validity of investment or mal investment

Who is right?:

The private equity and stock market equity investors funding high cost year round China production, or

The Australian banks debt/credit funding of NZ seasonal production

Trade wise: does

the Ministry of Agriculture of the PRC issued “An Urgent Circular on Coordinating and Handling Difficulty in Selling Milk to Stabilize the Production of Dairy Industry” (《關於協調處理賣奶難穩定奶業生產 的緊急通知》) on 7 January 2015

lend itself to examination via:

Article 11 Non-Tariff Measures

1. A Party shall not adopt or maintain any non-tariff measures on the importation of any good of the other Party or on the exportation of any good destined for the territory of the other Party except in accordance with its WTO rights and obligations or in accordance with other provisions of this Agreement.

2. Each Party shall ensure its non-tariff measures permitted in paragraph 1 are not prepared, adopted or applied with a view to, or with the effect of, creating unnecessary obstacles to trade between the Parties.

http://www.chinafta.govt.nz/1-The-agreement/2-Text-of-the-agreement/ind…

Russian dairy production up 26% in year after food embargo – Putin Read more

Relying on growth in Asia might be wishful thinking.

In Vietnam, a group of Israeli companies led by systems developer Afimilk is building a $200 million dairy farm, one of the largest projects of its kind in the world. It will eventually supply half the milk in Vietnam.

http://www.reuters.com/article/2015/05/19/israel-dairy-idUSL5N0Y44V8201…

http://www.thenational.ae/business/economy/spoilt-produce-blights-india…

If India ever gets it's supply chain mgmt fixed - watch out.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.