By Keith Woodford*

In working out the long term positioning for the New Zealand dairy industry, we have to ask ourselves four big questions:

- What will happen in China?

- What will happen to oil prices?

- What will happen in America?

- What will happen in Europe?

In this article I will focus on Europe.

The need to shed some myths

To understand the fundamental changes that are occurring in European dairy, we need to first shed some myths. Dominant among these myths is that the European industry only survives because of subsidies.

The reality is that Europe has been competing on world markets, free of export subsidies, for the best part of ten years. The reason that everyone signed-off on elimination of export subsidies at the WTO in December 2015, which both Fonterra and DCANZ (Dairy Companies of Australia and New Zealand) got excited about in their press releases, was that the agreement was simply ratifying existing behaviours.

The counter perspective is that European agriculture still has large internal subsidies. It is true that some European countries, particularly the poorer ones, do still have subsidies that are linked to production. For dairy, these subsidies total about 0.8 billion euro, which sounds a lot. But it only averages out at about NZ 11c per kg milksolids. In the greater scheme of things it’s trivial. In any case, these subsidies do not apply in the major European exporting countries with the exception of France.

In addition, Europe does still protect its internal markets with tariff protection, but that is not going to change. Quite simply, as a matter of food security and regional security, the EU will never allow itself to become dependent on outside countries for basic foods. And we in New Zealand have zero influence to change that.

Our industry leaders can hammer away as long as we like at the Europeans, but in reality it is grandstanding for our own New Zealand audience.

Alignment with international prices

Despite the tariff protections, European farm gate dairy prices are now becoming aligned to international prices. In the new Europe, with no production quotas, and with the industry having to itself market surplus production, it is inevitable that this alignment occurs.

The major caveat on European prices being aligned to international prices is that there are lags in the system, which we are seeing right now. It takes a while for current international prices to work their way through to the farm gate, and the same lags can happen when international prices rebound. Also, the so-called international prices as measured by the GDT auctions are only for basic commodities.

The European producers, just like New Zealand’s Tatua Dairy Co-operative, have protection from some of the wild GDT swings. This is through their reliance on value-add products. Also, apart from Ireland, all European dairy systems are 12-month-a-year production systems. These 12 month production systems can lead to higher production costs, but they also lead to lower processing costs through better utilisation of processing infrastructure. This then feeds back into higher farm-gate prices.

The straitjacket of quotas

Until April of 2015, the European dairy industry was in a straitjacket as a consequence of production quotas. The legislation behind those quotas goes back to the 1980s. In those days, the European system administered through the Common Agricultural program (CAP) provided large production subsidies for domestic reasons. But this led to over-production. It also led to the so-called butter mountains, which could only be sold through export subsidies.

That European subsidy system was gradually whittled away during the 1990s and the early years of the 20th century for the simple reason that it was too expensive for the EU budget to maintain. During this time, the EU was getting ready for the eventual elimination of quotas.

Ironically, the last three months of production quotas through to April 2015 actually saw a reduction in production as producers, having got themselves organised for the new world, had to put the brakes on to stay within their old annual quotas. But then in April the lid came off.

Unleashing the entrepreneurship

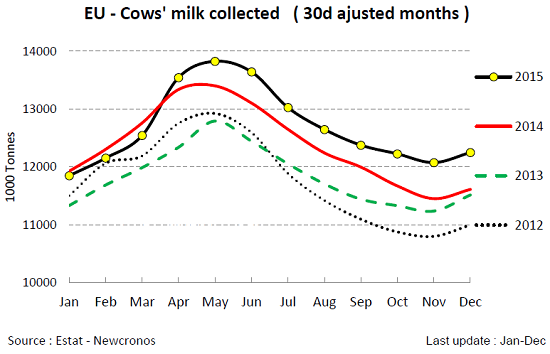

For much of 2015, our New Zealand industry leaders effectively under-reported what was occurring in Europe. The reason was that they chose to report whole-year to whole-year increases, rather than focusing on the specific month comparisons since the quotas were released.

To illustrate this point, if calendar 2015 is compared to calendar 2014 then European production only increased by 2.5%. But in the months from April to December, European production increased by 4% relative to the preceding year. And in December 2015, European production was 6% above December the previous year.

As long as January to March 2015 figures were included, then the message as to where the story was heading was misleading.

There is no doubt that many European farmers are going to experience huge pain. They already are. This is what happens when entrepreneurial forces are unleashed after being held back so long. Those of us with long memories know something about that in New Zealand.

Expanding markets

Currently, the Europeans are producing as much cheese, butter, infant formula and cream as they can, with cheese being more important than liquid milk. The Europeans are also selling increasing quantities of UHT and infant formula to China. With both products, they are out-marketing New Zealand.

Chinese infant formula statistics for 2015 show European countries with 78% market share of imported product, compared to New Zealand at 8%. Holland is Number 1 (at 34% market share and rapidly increasing), Ireland is Number 2 (at 15% and also rapidly increasing), whereas New Zealand’s market share keeps drifting down with each new set of statistics.

The Europeans would like to decrease their production skim milk powder (SMP), but with butter and cream being profitable, they keep producing the SMP as a by-product. However, the European production of whole milk powder (WMP) has been drifting down in response to low prices.

Amongst the general gloom, and given the ban on European cheese imports by the Russians, it is remarkable how well cheese prices have held up until recently.The Europeans have had good success with exports to the USA and Japan as replacements markets, and overall their cheese exports are almost unchanged from 2014. But in recent weeks the international price of cheese has been going pear-shaped. Ouch! The European pain is about to get worse.

Intervention stocks

The Europeans have been putting limited quantities of SMP into what are called intervention stocks. This is a form of temporary price support and is somewhat like Fonterra’s actions during the 2008/9 price crash. At the end of January 2016, there were about 50,000 tonnes of SMP in public intervention store, but it looks as if stocks have been climbing rapidly since then. The intervention quantities could reach a new limit of 218,000 tonnes over coming months. The main benefit of the SMP intervention is a smoothing of commodity prices.

These intervention stocks, by buttressing international prices, reduce the short-term pain for New Zealand farmers as well as the Europeans. But eventually, the SMP has to be sold, and that will slow the SMP price recovery.

What will happen now?

My current thinking is that the European production surge relative to last year is about to peak right now on a same-month to same-month comparison. From April, growth on a same-month to same-month basis may even stop. However, feed prices are low and so there are no guarantees.

Regardless of what happens in the short term, there is a good chance that in the longer term European production will further increase, as some farms grow and others get out of dairy completely.

For this longer term, the Europeans, with the possible exception of Ireland, are not going to try and compete with New Zealand with WMP. Europeans regard WMP as an outlet for product with no other immediate use. And they know that, in low-priced volatile commodity markets for long-life products, they lack competitive advantage relative to New Zealand.

One good example is the Arla Co-operative which now has more than 10,000 farmers in seven countries. Their aim is to increase production by 20% in the next four years, with all of this going into consumer products, and much of this heading to Asia.

I also note that Danone, whose brands include Karicare in New Zealand, has ambitions to process more European milk, and is currently building an infant formula plant in Holland at a cost of about 240 million euros. No doubt that product will be aimed at China and other Asian markets.

A remaining puzzle is whether Poland will step up to the mark. There is no doubt that Poland could become a major milk producer. Latest statistics show that milk production there is up 3.6% since quotas came off, but it could be some time before they really get their act together.

Implications for New Zealand

The full implications for New Zealand is a story for another day, and has to be tied in to what is happening with China, USA, and oil. But the big picture is that Europe has commenced a journey of radical reform. In future, there will be less European dairy farms but they will be bigger. And Europe is here to stay as a major exporter of consumer dairy products onto global markets.

Keith Woodford is Honorary Professor of Agri-Food Systems at Lincoln University. He combines this with project and consulting work in agri-food systems. His archived writings are available at http://keithwoodford.wordpress.com

21 Comments

Surely there is little doubt now that we have seen a structural change in dairy prices.

I think it is likely that this is about the new normal because Europe has so much potential to increase milk supply if demand increases.

Futures prices are pointing down again, good chance of the GDT following again because of European milk flows being in full swing.

Who will break the bad news to the ever optimistic Theo Spierings though?

Thanks Keith, interesting article. Do you mind explaining how you equate your €0.8bn European diary subsidy with the current CAP budget of ~€59bn?

Calaverite

My reading of the stats is that direct support to agriculture that is coupled to production is about 4 billion euros. (It used to be a great deal more.) Of this, 0.8 billion goes to dairy. Note that this is the coupled support. There are, of course, lots of decoupled support structures relating to the environment. But farmers get those supports regardless of how much milk they produce. Indeed they can get those decoupled support payments even if they totally stop milking cows, as long as they look after the land as per EU regulations. I mentioned those decoupled support structures in a previous article but did not go into them here. Perhaps I should have done so.

Keith

So is there $55b of subsidies that are not production related?? Seems an awful lot of subsidies and while not linked to production I think this might make it a lot easier to operate than a NZ farmer.... Seems a bit odd to exclude this in your article?? Why would you say this isn't having an impact or am I not getting it???

Great informative article thanks Keith, what happens to all the Fonterra capacity when stock numbers drop and herds dried off?

No helmet,

Fonterra's capacity traditionally runs over any 12-month period at about 50% utilisation, or a little under, because of the seasonality of production.

In contrast, Fonterra's Northern Hemisphere competitors ( with the exception of Ireland which is a seasonal producer like NZ) operate at about 90% capacity (on average) with some operating even higher.

Fonterra's capacity utilisation will now be dropping further as a consequence of increased investment in dryers but decreasing production. This drop will be occurring to a small extent this year but the trend will accelerate next year.

I have looked at some of these issues here: https://keithwoodford.wordpress.com/2016/02/25/a-fonterra-thought-exper… , and more generally, in a range of articles about Fonterra in the 'Fonterra' category at http://keithwoodford.wordpress.com)

Keith W

Thanks Keith, I lease to 2 dairy farmers, 1 going to Open Country, the other having compliance issues

, certainly alot of movement on the station.....

read that 330,000 budget dairy cows sent to works in last year above and beyond that of normal culling? this equates to the 5% of national herd and production. Not good for the supplement feed companies who would have been supporting these extra cows. Maize Silage now even questionable as a supplement as too much growing and harvesting cost.

Yes Donker, those extra cows eat a good amount of bought-in or farm-grown feed and farmers are seriously questioning the cost effectiveness of all inputs these days. It may be time for farmers to do a Fonterra themselves. Some of the input costs are well in excess of profitability and could take a real tumble. They've been creeping up for years. Time there was a "re-alignment". For example, maize seed is expensive. Grass seed is expensive. These costs need to rationalize somewhat.

What our global dairy system at present suggests is that it is more than capable of supplying increasing demand even at 2% growth per year. What this suggests is an average milk price around $5 per kg MS moving forward. What this means for NZ is dairy farm prices realigning with this new average. Dairy farm prices were largely inflated based on the assumptions that the world was short of milk going forward in to the future. What we are now seeing is the reality of this assumptons.

Land is worth no more than the early 2000's when you look at long term trends. The only thing that changed was banks willing to lend money and hype of a supply/demand expectation. This is now proving unsustainable

In short the payout at $5is sustainable, the bank lending is not.

Was there any word or hint from Fonterra on how the $ was affecting things?

I hear whispers that secret talks are on (cross party, as Labour has dirty hands here too) to repeal the DRA provisions obliging fontera to give and take milk to and from newcomers, in return for the monopoly splitting out the consumer ready products business ( telecom/spark style - with voting rights this time ) for NZX listing. The townie vultures are circling.

Can you get the NBR? give this link a try looks unlocked

http://www.nbr.co.nz/opinion/heartland-fonterra-needs-circuit-breaker-r…?

Investment analyst Brian Gaynor appears to have reached the same conclusion. In February he calculated Fonterra’s debt at $7.56 billion and net finance costs at $518 million.

This implies an overall interest rate of 6.85%. That being the case, any suggestions that farmers should take an interest free loan from Fonterra overlooks the fact that Fonterra is paying a higher interest rate than farmers can achieve themselves.

1 by Cam Henderson 1 hour ago

Looking at the half year results Fonterra's 19 billion in assets is only backed by 7 billion equity. Thats a an equity backing of 36% not approx 50% as they report. Fonterra is in a much worse capital position than is being reported

http://www.nbr.co.nz/article/fonterra-chairman-wants-two-changes-govern…

Rod Oram: Fonterra's fearsome task

http://www.stuff.co.nz/business/opinion-analysis/78217416/rod-oram-font…?

Yes AJ, that 36% will be the fontera debt+debt:equity ratio habit that Prof Woodford has reported on afore.

Of course the amendments to the DRA won't fix it (only a taxpayer rescue one day will do that) but the amendments will perfect the monopoly and set the townies up to fleece the cockies. Free enterprise is all just too hard for these Moderns nowadays, better just to get Pollies to do the dirty work for you - dress it up as the National interest and share the spoils with Banksters.

Looks almost a given (DIRA changes) , it will be the ability to add on bits that will be the worry. For instance will they be able to cap production from farms in marginal pickup area.

The analysis in Andrews links makes poor reading, it fits with my and many other amateur analysis and is at odds with Theo and Johns spin.

Still stick with my prediction that 5 years fromTAF it will be broken up, no matter how well or poorFonterra is doing.

Have a read from newsletter out of the States, whats with all the PKE? Not going to help you to keep your breakfast down.

http://www.milkproducerscouncil.org/updates/032516.pdf

than have a look at USA GDT analyses.

http://www.attenbabler.com/global-dairy-trade-biannual-chart-focus-upda…

PKE. I recently heard of two farmers whom I always looked up to as successful, organised sorts. Ones who I thought would budget well ahead and keep things under control. I was really surprised to discover that the last two seasons they've just plowed on ahead feeding the same supplements they fed at $8, one still planning on a herd sale to finance a new farm purchase at the same cow price as 2 years ago. In short there have been some just not reading the signs and believing Fonterra spin. They have literally only woken up to reality in the last month and maybe that is repeated for a fair percentage of the 12,000 or so.

Around here the dairy boys have pulled the pin on Fert and spray costs, love to be around the table when they discuss costs and who's for the chop next, bet the options are not pretty, without an asset sale or two.

An old guy told me that inStates 2005, the biggest difference in his life farming was today you have to sell assets to pay off farm debt, incomes no longer cut it in the debt repayment game.

Lower interest rates will only go so far.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.