By Keith Woodford*

As expected, Fonterra has announced a greatly enhanced six-month profit for the period ending 31 January 2016. The profit of $409 million (NPAT; i.e. net profit after finance costs and tax) is up 123% from the same period in the previous year.

The expected full year profit of 45-55c per share implies an annual profit of about $800 million compared to $506 million for the full year 2014/15.

These figures are all very much in line with expectations. The reason for this is that when milk prices to farmers are low, then Fonterra has low input costs. Accordingly, there is more scope for corporate profit.

Of course, given that Fonterra is a co-operative, its farmers do benefit from these profits. Fonterra plans to pay a 20c dividend in April which is at the upper end of expectations.

Fonterra also plans to pay subsequent dividends of 10c in each of May and August. Normally any subsequent dividends would not be paid until the October final dividend.

This planned early payment of subsequent dividends is aimed at supporting farm cash flows. By doing it in this way, Fonterra will avoid criticism from corporate and non-farmer investors in the Fonterra Shareholders Fund, as they too will get early payment. Indeed it is a very clever way to keep everyone onside.

The one group who do not benefit are the sharemilkers given that they only get a share of the milk price. There are several thousand of these sharemilkers, but their voices are seldom heard. They are too busy in the milking shed and out in the paddocks managing the cows to be doing media interviews. Sharemilkers are meant to be the next generation of farm owners, but their immediate focus is business survival.

I have previously written about how it would be necessary to scratch well below the surface to interpret the real economic meaning of these Fonterra results. And that is not an easy task.

Component segments of the profit are recorded on an EBIT basis (i.e. before interest and tax). That is the obvious way to do it, but it does mean that these numbers should all be strongly positive, if unallocated fixed costs plus finance costs are to be met.

The big increase in EBIT is from ingredients, with this figure up 77% to $665 million. Much of this is a direct consequence of milk powder prices, which dominate in the formula used to calculate the farmgate milk price. It is worth reinforcing: low milk powder prices typically lead to higher profits for Fonterra’s ingredients, food service and consumer products.

However, there is also another factor at play, and that is the unusually high margins this year between commodity cheese and commodity milk powders. The so-called profits from cheese relative to milk powders go to corporate profit rather than to milk price. So this further augments the profit figure.

This year, Fonterra has been producing as much cheese as possible – about 17% more in this six-month period compared to the same period of the previous year. But this relative profitability of cheese is unlikely to last, with international cheese prices heading pear-shaped in recent weeks.

In the article referred to earlier I wrote that key underlying issues would include whether there was evidence that Fonterra had turned around the red ink from Australian operations and its China farms. In fact, the red ink has continued, showing that more work has still to be done.

In Australia, Fonterra has made a $9 million EBIT for ingredients compared to $12 million the previous year. So that has gone backwards from an already weak position.

Australian food service and consumer products are bundled in with New Zealand, to give a combined Oceania total of $33 million compared to $10 million the previous year. But the New Zealand operations should surely be very profitable given the lack of internal competition. So it seems that Australian food service and consumer goods is still in lots of difficulty. Indeed the Chair and CEO in their joint report state that Australian results “are still not satisfactory”.

For China Farms, the six month EBIT has slipped further from negative $27 million to negative $29 million. Precise comparisons are not possible, and are confounded by a 54% increase in milk volumes, but it is clear that a drop of about 16c per litre has overtaken the volume benefits and operational savings that they have achieved.

Fonterra does not tell us the price they get for their milk produced in China, but my estimate is that they are still getting a farm gate price of at least $9 per kg milksolids. I think it may be more. So clearly they still have a very high cost operation over there.

One of the good news stories is that profit from food service and consumer goods has increased from $116 million to $241 million. However, I am unable currently to judge how much of this improvement is due to the lower cost of milk and how much is due to better performance in the market. I think it is mainly the former.

One of the “useful facts” Fonterra provides is that the amount of milk processed this year for food service and consumer goods has increased by 235 million litres (measured using an international standard of ‘liquid milk equivalents’) compared to the same period last year. This is an increase of 10% over the previous year, but the six-monthly increase would seem to only represent about 1% of Fonterra’s New Zealand milk supply. So progress is being made, but it is a long journey.

Even more notable than any of the above is that the EBIT for ingredients is $617 million but the overall company EBIT is only $665 million. So without ingredients (read commodities) Fonterra would be running a very small EBIT of only $48 million and hence a very large negative NPAT (i.e. after the profit after finance costs and tax). That could indeed take some explaining in terms of Fonterra’s strengths (undoubtedly commodities) and weaknesses (almost everything else).

The decrease in gearing ratio by about 2% needs to be taken with a grain of salt. It will have been influenced by the specific way that Fonterra calculates this ratio (only interest bearing debt is included) and the non-inclusion of all of those invoices from suppliers that now sit in the ‘to do’ pile for up to 91 days.

As I write this article some two hours after release of the results, I note that units in the Fonterra Shareholder Fund have risen one cent to $5.94. That would seem to imply that the market has seen no major surprises in the overall results. And that tells us that the market consensus is saying that New Zealand’s overall dairy situation remains unchanged.

Keith Woodford is Honorary Professor of Agri-Food Systems at Lincoln University. He combines this with project and consulting work in agri-food systems. His archived writings are available at http://keithwoodford.wordpress.com

12 Comments

Just watched Fonterra's Spierlings on John Campbell RNZ. Unbelievable level of BS. When asked why it doesn't pay it's contractors on time he said "We do pay on time"

But eventually Campbell worked out that what this meant was that they intended to pay at 90 days and did so. Meaning on time - well according to him. As for 30 days ?????

I don't think this forked tongue individual is of good enough character to run any significant New Zealand enterprise.

Slow paying of invoices has a deflationary effect. Not only that but they have money to pay dividends but not contractors. There may be grounds to claim that they are operating while insolvent.

Fonterra better hope that a creditor doesn't take action for involuntary wind up and claw the dividends back from farmers.

I don't think Fonterra are the only business doing this sort of late payments of the bills.

Yup

http://www.stuff.co.nz/business/78107481/christchurch-painter-says-buil…

AND food parcels needs have skyrocketed, people 'hot bedding' for accommodation etc.

It's amazing peoples 'elasticity' (what they are willing to put up with) and the ability of people to soak up (ie pay for) the economic crap caused by others.

Christchurch is very unstable in more ways than one.......I feel sorry for the painters as they are pretty much the last tradie involved in any job and the money seems to have dried up by the end of a job.

Economic crap caused by others starts from the top down.....all that tax theft has to be constantly soaked up then there is the plethora of fees, licenses etc.......always somebody with an outstretched hand in a bureaucracy somewhere........and at the end of the day we find we have to privately donate to charities to hopefully ensure people have access to the basics of some food etc ....screwed up world this socialist system is!!

I wonder if Theo tells his lawn mowing man that he'll pay him in 90 days time ? If not, why not...., does he need a cashflow to keep his family and business going ?

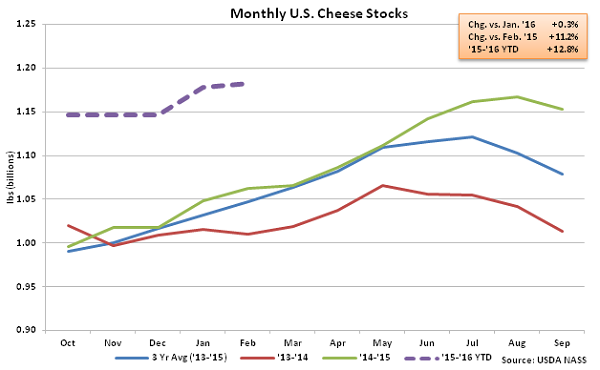

Feb ’16 U.S. cheese stocks of 1.18 billion pounds finished up 0.3% MOM and 11.2% YOY to a new 31 year high. The monthly YOY increase in cheese stocks was the 16th experienced in a row. Cheese stocks have remained higher YOY in recent months as milk production has strengthened in Midwestern cheese producing states while weakness in cheese export markets has continued. Strong cheese production has been partially offset by continued strong domestic demand, however cheese exports remained lower YOY for the 16th consecutive month during Jan ’16.https://secure.attenbabler.com/wordpress/wp-content/uploads/2016/03/Mon…

{kind=link}

Interesting, cause reading between the lines the cheese price and sales has been the mainstay of the dividend.

www.grassfed.com

Add this to A2

redcows, don't let me ruin your day but it's going to get even more, 'interesting'.

https://secure.attenbabler.com/wordpress/wp-content/uploads/2016/03/Mon…

{kind=link}

http://www.attenbabler.com/chinese-dairy-imports-update-mar-16/

http://www.attenbabler.com/eu-28-milk-production-update-mar-16/

Yea thanks Andrew needed that ;).

Re. China farms. The only line that is referred to as a challenge is milk price and cost of production but I would suggest the lions share of that loss is none cash adjustment to the value of livestock out there. The DCF methodology to work out value is so heavily weighted to milk price that there is a huge hit sitting there.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.