This is the release posted on the NZX this morning.

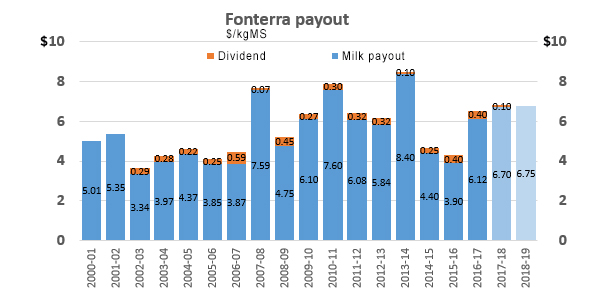

Fonterra Co-operative Group Limited today revised its 2018/19 forecast Farmgate Milk Price from $7.00 per kgMSto $6.75 per kgMS.

Fonterra Chairman, John Monaghan, said the change was in response to stronger milk supply signals coming from some of the world’s key dairy producing regions.

“Over the past quarter, we have seen increased milk supply out of markets including Europe, the US and Argentina. These regions have a big influence on the supply and demand balance and therefore global prices. For example, the one per cent increase in US milk production represents just under 100 million litres of extra milk.

“At the same time, demand for whole milk powder and dairy fats is showing signs of slowing in some parts of Asia, Africa and the Middle East,” added Monaghan.

Fonterra CEO, Miles Hurrell, said the weakening NZD/USD exchange rate had only partially offset the decline in global dairy prices, and it was important to give farmers a realistic assessment of the market.

“It’s still very early in the season and a lot can change over the coming months. A drop in the new season Milk Price forecast will be frustrating to our farmers, but it’s important we give them the facts so they can make informed decisions in their farming businesses,” said Hurrell.

The timing of today’s update is in line with DIRA requirements for Fonterra to review the Milk Price every three months. The Co-operative last considered the Milk Price in May.

The full payout history, including payout detail from other dairy companies, is here.

24 Comments

Look, I've been very critical of Orr, he succeeded in lowering the NZD, in part to help dairy farmers - the NZD has come back a little since then so the Farmgate milk price is obviously going to be lower ..

If farmers are upset about this, I totally understand and plead for them to look across the ditch to their Australian counterparts for some perspective.

That is NOT to say Fonterra is managing things well, but this will change. Farmers are going through a tough time at the moment - remember, farmers are NOT a protected species, though Labour is being quite good about things. Things/issues they inherited from the National government.

So, let us have some reasoned reporting, which gives credit where credit is due. Lack of business confidence might be advantageous for farmers (lower NZD) - a tarnished silver-lining for sure, but a silver-lining nonetheless.

Zach how low should the NZD go. Take a look at the chart. USD/NZD .Orr's job is not to help a few farmers.New Zealand's skewed focus on farming is simply misguided.

Like I said, I've been very critical of Orr, his recent statements were reckless (in my opinion) and I've wished him removed from his post more than once.

New Zealand is one of the few countries which PUBLICLY celebrates when our currency declines. You're right Cowpat, it's not his job and I'd point out his comments (probably to his disappointment) had little effect on the TWI.

It is what it is my friend, I agree with you.

A lower dollar helps the entire tradeables sector, which can only be a good thing if the economy is ever going to transition away from property speculation and population increase as core business.

Doris , weak currencies do not exist in isolation .

so we all get a hit on the value of our $, we find it doesn't go as far, we get payed in a dollar thats worth less, we then pay our farmers in those devalued dollars and we are better off?

NZ has a balance of trade deficit that averages about 2-3% of GDP over long term so a dropping NZD is net bad for us with the higher non-NZD denominated overseas payments that we have to make.

Devaluing our currency isn't enough in itself to kickstart the tradeable and non-speculative sectors. We need a business policy overhaul to shift investments from real estate into high-value R&D-driven ventures.

A lower currency rate may provide a brief impetus to the export sector of a country but the long-term effects on trade are not as one would expect, something economists have found time and again. Also, there were no significant increases in export volumes from the last time our dollar fell to mid-60 US cents towards the end of 2015.

https://www.wsj.com/articles/why-weak-currencies-have-a-smaller-effect-…

A higher dollar forces us to add value and increase productivity. A lower dollar is a race to the bottom effectively just a pay cut in purchasing power.

seems at odd with the news of lower production out of the EU,USA and Australia due to drought.

$6.75 is still nicely above the average FWE of $4.81 for the last decade:see P 28.

Operating expenses per kilogram milksolids averaged $4.81 over the last decade, encompassing a range of payouts along with the global financial crisis and various seasonal weather conditions. Operating expenses exceeded $5.00 per kilogram milksolids in 2012-13 and 2013-14.

However, the $4.60 operating expenses recorded in 2016-17 was only up slightly after farmers corrected their expenditure sharply in response to low milk prices in 2015-16.

Sky falling averted....

Old man yells at cloud

I'm assuming FWE doesn't include the costs of servicing debt? only costs directly to do with operating the farm?

Which would mean debt free farmers are doing quite alright and those armpit deep in debt not so hot?

Correct. The standard accounting formula: net sales minus operating expenses is EBIT (Earnings before Interest and Taxes). So the interest portion of the debt servicing costs is not included in operating expenses, while repayments only hit balance sheet items (cash and loan), not P&L.

Previous sector commentary from Rabobank suggests the majority of debt in this sector is owned by a few NZ dairy. So a majority of the market players are doing alright.

A peek at the Time series in the above link provides an average answer (Owner-operators, table 7.6...) The average term liability is of the order of $4m or $25/KgMS assuming 160K KgMS production. So debt servicing even at overdraft rates of high-6, low-7% is around $1.75/KgMS at 7%.

MPI's M.Bovis herd culls, their destruction of decades of genetics in the process, and the usual Gubmint lag in settling compensation, are likely bigger worries than a small wobbular movement in milk prices.

But, as in all averages, ymmv....

We now have well over 5000 properties with a forward contact mbovis animal. MPI are lauding the fact they have found another positive in Northland yet exploding ahead of them are movements of cattle to more farms. Apparently we have 90000 Nait users. According to MPI we now have more than 5% of Nait registered properties with a forward contact animal. Wtf.

MPI have put out a new format for their numbers. This now does not include the total number of forward contact farm properties.

Over 5000 New Zealand properties have a forward contact mbovis animal.

24/8/18 this was 5137

21/8/18 this was 4940

It grew by nearly 200 in three days.

This figure is mindblowing

I do not see any media picking this figure up

But I do see MPI have not published an updated figure in their late night friday update.

Why are we carrying on with eradication when according to MPIs own figures more than 5 percent of NZ farm properties have a forward contact mbovis animal.

Can anybody out there explain to me why 5000 NZ farms with an mbovis contact animal isnt a problem? I really want to know why I am under a NOTICE OF DIRECTION while nearly 5000 other farms arent?

Why? I personally know several farms who bought animals from the same place I did, same age group, who are not under a NOD and free to move and sell their cattle.

What the HELL is going on?

https://m.facebook.com/photo.php?fbid=1106956916124528&id=9442572990611…

Flick to photo 2/18 this format which gives all the current figures has been changed. They seem to have done away with the scary stuff.

waymad - it would be interesting to know how many farmers were/are on DairyBase - the basis for the stats produced. We were at the start but have pulled out as they didn't have enough farmers in the lower South Island that we could compare ourselves with. As we paid for the privilege of being on the database, we pulled the plug on it. Not sure where the numbers sit now.

Have not dug that far, and it does seem biassed toward the mom-and-pop family farm: 400 coos, 160K kgMS production. I'm more familiar with a few of the bigger shows - the difference is 10-100 times - so that's a whole different ball-game ops-wise.

Plus, Fonterra is only one of the players if the major one: Tatua, Oceania, Synlait, Westland and others - there's a lot of space left in the market gaps the Big F leaves....

FYI Waymad and Cas - while Dairybase is used for this stats, they are also “moderated” to make them accurate from a whole lot of big data sets. For instance the dairy debt from RBNZ reconciles to farm debt. So they are very accurate, and farmers have an average $25 per kg but it costs more like $1.30 to service. The operating exp figure above doesnt include the average 50c/kg drawings - which is really a wage cost and is the one figure that is most likely understated. Combine Bovis, environmental constraints, that Fonterra has likely still overstated the commodity milk price, and that Fonterra will be overcapitalised if supply declines and there is a bit for farmers to think about still.

Good points, gratefully received.

The other point about averages is that they are - er - averages. As a case in point, I'm aware of a smaller outfit on the West Coast with FWE in the low 3's: built-in irrigation thanks to Gaia, low debt and canny owners. So a 25c swerve in the price won't amount to much in that situation. Averages - always half are below 'em....

I agree - the range is wide and there are plenty of farmers who have never done better. It’s often the older generation who struggling to adapt, and may need to get out

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.