Fonterra has reviewed its milk payout price and has reduced it in this December update by -25 cents per kgMS.

Updated comparisons are here.

Here is Fonterra's announcement:

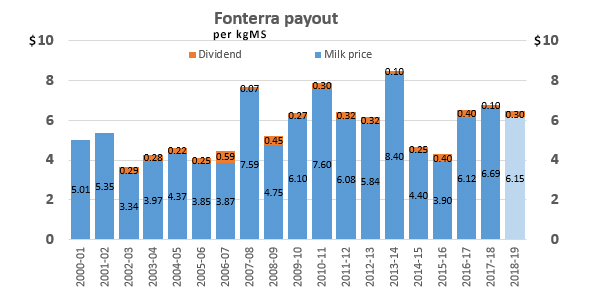

Fonterra Co-operative Group Limited today revised its 2018/19 forecast Farmgate Milk Price range from $6.25-$6.50 per kgMS to $6.00-$6.30 per kgMS and shared an update on its first quarter business performance.

Fonterra Chairman John Monaghan says the revision in the forecast Farmgate Milk Price range is due to the global milk supply remaining stronger relative to demand, which has driven a downward trend on the GlobalDairyTrade (GDT) index since May.

“Since our October milk price update, production from Europe has flattened off the back of dry weather and rising feed costs. US milk volumes are still forecast to be up one per cent for the year,” says Mr Monaghan. “Here in New Zealand, we are maintaining our forecast collections at 1,550 million kgMS. NIWA is saying its likely we will see an abnormal El Nino weather pattern over summer and this could impact our farmers’ milk production.

“Demand from China and Asia remains strong. However, we are seeing geopolitical disruption impacting demand from countries that traditionally buy a lot of fat products from us.

“Today’s forecast range assumes dairy prices will firm across the balance of the season. This is consistent with the views of other market commentators.

“There are still a number of unknowns in the global demand and supply picture and we recommend farmers budget with ongoing caution. Fonterra’s Advance Rate has been set off a milk price of $6.15 per kgMS.”

First quarter business update

Fonterra’s first quarter gross margin of $646 million is down $14 million compared to the same period last year and up slightly on a percentage basis from 16.6 per cent to 17 per cent.

Revenue of $3.8 billion, is down four per cent and sales volumes were down six per cent to 3.6 billion liquid milk equivalent (LME).

The Co-op’s Ingredients business, despite lower sales volumes, performed solidly during Q1 with a gross margin of $273 million, up $28 million on last year.

The Consumer business also performed well with a gross margin of $310 million, up $10 million on last year, and volumes were up five per cent.

Chief Executive Miles Hurrell says the Co-op generally makes a smaller proportion of its total annual sales in the first quarter due to the seasonal nature of our milk supply. “This means the results from Q1 do not give much insight into the Co-op’s expected earnings performance for the full year. It does, however, put the spotlight on where we have challenges that we need to address,” says Mr Hurrell.

“In particular, we are seeing challenges in our Australian Ingredients, Greater China Foodservice and Asia Foodservice businesses. I want to be clear with our farmers and unit holders about how we are tackling these issues.

“In our Australian Ingredients business, we have lower milk collections as a result of drought conditions and increased competition for milk supply. We are responding by focusing on the performance levers in our control – the main one being reducing our operating expenses to reflect lower milk collections.

“The lower gross margins and sales volumes in Greater China Foodservice and Asia Foodservice in Q1 are mainly due to the high sales volumes of butter and cream cheese at the end of Q4 2018, a slightly slower start to sales of UHT culinary cream and more sales of UHT milk which has a lower margin relative to our other products. We are expecting our sales to lift as we are seeing strong sales from our distributors off the back of demand in China for New Zealand made products, particularly our UHT culinary creams. We are also prioritising value and moving away from lower margin contracts.”

Portfolio review

Commenting on the Board led portfolio review Mr Monaghan says there is a lot of action and progress but it will take time to flow through into financial results.

“We have reached an agreement in principle with Beingmate that will see us return to full ownership of the Darnum plant by 31 December 2018 and enter into a multi-year agreement for Beingmate to purchase ingredients from us.

“We are also looking at our ongoing ownership of Tip Top and have appointed FNZC as our external advisor to work with us as we consider a range of options. We want to see Tip Top remain a New Zealand based business and this is being factored into our options.

“While performing well, Tip Top is our only ice cream business and has reached maturity as an investment for us. To take it to its next phase successfully will require a level of investment beyond what we are willing to make.

“We are still some months off from completing the full portfolio review of assets, investments and partnerships. We are moving quickly to meet our commitment to reducing our debt levels by $800 million by the end of the financial year. This requires both improved performance from last year and the divestment of assets.”

Lifting performance

In respect to the three-point plan to lift the Co-op’s performance, Mr Hurrell says progress is being made on fixing the businesses that are not performing. “Fonterra Brands New Zealand is one of the businesses that is starting to turn around. It’s early days but overall our Consumer and Foodservice business in Oceania delivered higher sales volumes and margins for Q1 compared the same period last year. A significant contributor of this is the improved operational performance in New Zealand.

“We have set our capital expenditure (CAPEX) limit at $650 million. While we are ahead on the same time last year, this was planned as we completed the final stages of projects from last year. Once these assets are delivered, our focus will turn to ensuring they hit their Return on Capital targets.

“We remain committed to returning our operating expenses (OPEX) to FY17 levels – however, they were up three per cent for the first quarter compared to the same period last year. The majority of these costs were committed to before we agreed our new OPEX target. They relate to higher advertising and promotion and storage costs in our Consumer and Foodservice business, additional costs since taking the management of Anmum back from Beingmate and higher storage and distribution costs for Ingredients as we collected and moved more milk than we budgeted for.”

Outlook for 2019

Mr Hurrell says the Co-op is maintaining its forecast earnings per share range of 25-35 cents.

“Q1 gross margin percentage was up on last year and we have identified the challenges that need addressing. Our earnings forecast for the remainder of the year is based on a milk price within the $6.00-$6.30 per kgMS range and, on this basis, we are confident in our earnings guidance.”

16 Comments

TIp Top up for sale, being fonterra they will most likely get it for a song if there track record is anything to go by.

this is one company that knows how to squander wealth creation on behalf of its shareholders

Tip top is tip bottom. They've been watering down their junk products for years. I'd be surprised if there is more dairy than gelatin. If it's tip top then tip it out. Whitaker's made a huge mistake going with these guys.

Like any business cash flow is king and what Fonterra VERY lightly touch on is the impact on dairy farmer cash flows. Fonterra are looking to take back 15c of the $4.15 advance made season to date. Merry Xmas dairy farmers - about $100m just got taken out of circulation that we have already spent running our farms.

Being well removed from dairying, looking at the graph it shows $6 or there about's is still above the long term average. Is that still a crap result regardless?

Averageman - on face value $6 seems okay. However it is still just an estimate the same as the $7 was just an estimate 6 months ago. This month in actual money - Fonterra will put $4.00 per kg in my bank account less .15c per kg they "overpaid" me for earlier months. This is about $1.50 below my operating costs so up goes my overdraft. If only I could work out how to buy eggs for 3c and sell them for 2c and make a profit. .

I'm hearing there's a few struggling dairy farmers due to having to share up. Time to roll out MyMilk nationwide?

Dairy farm auction, nth pahiatua, top family unit, only problem no one at last week's auction.

Yes. Costs keep going up. Sliding back to $6.00 is a kick in the teeth. I had a conversation with a farm advisor for a large corporate dairy a few years ago, he said they needed $6.50 to break even. Personally feeling it myself as I watch the jitters in the beef schedule.

Ok... so $6.50 is profit/loss point for the sector so that answers that question. Has opex costs gone up much in the last five years, and if yes whats the biggest item?

Comment heard frequently - "as soon as Fonterra said $7 at beginning of season, all contractors, service providers, suppliers etc put their prices up". Ask any farmer - once those prices go up, they don't come down if payout drops.

Break-even costs for dairy farmers nationwide for 2018/19 is forecast around $5.40-5.50 per kgMS, which means most farmers will have the ability to reduce debt or invest back into the farm. https://www.dairynz.co.nz/news/latest-news/forecast-milk-price-provides…

edit: for Fonterra farmers who need to share up partially or fully add in share price - currently $4.78share/kg

Is dairy farming really that marginal a proposition, or is it really just a property play? What about the dairy tech and productivity gains?

Te Kooti - From a personal perspective the payout volatility between seasons and within seasons makes life difficult. You borrow millions from the bank with no certainty of income. In the last six months gross income will have dropped about $150,000 to $180,000 for the average size farmer. Input prices haven,t moved, some have gone up. Our family don't buy for capital gains which does mean we have to sit out the market on occasion as cash flows don't justify asking prices. Prices seem to come back into line if you are patient.Productivity gains are now limited, quite rightly, by environmental concerns. Dairy farming is a good business if you are patient and persistent despite Fonterra's efforts lately to make it more hard work to make a dollar than it needs to be.

It is a mongrel to share up in this environment,falling payout advances, very low dividend return on those shares- there was a time when dividend return was higher than the borrwing cost to purchase

Dairy farmers have you noticed on today’s dispatch’s from Fonterra they are calling back cash from farmers to balance the books next month ?

Slight of hand I think

Yes I did notice. As my above comment - there goes $100m across rural NZ that we already spent on farm. If I was a conspiracy theorist I would say it's one way to push rural lending growth after bank lending having stagnated. Fonterra's books must be bloody tight to have to do a stunt like this especially after apologising profusely for taking money back from last season's end of year payout. Second time in 6 months Not a good look..

Competition is critical to successful businesses, we might not like but it's the reality. Previous Governments have been happy to leave these monopolies adding some claytons competition that were always too small to make a difference.

We still need businesses that can cope with competition in a globalised world. We need dairy farmers prepared to step up sell their shares and take a risk by buying TipTop. WE don't need Westland bailed out by the government. We should have multiple specialised companies, but thats the old, could have should've would've again.

These corporate farmers drunk on debt should have gone to the wall years ago. They have been allowed to have cheap immigrant labour, get councils turning the other check again and again and special banking treatment. They should be allowed to fail and the sooner the better.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.