Against the backdrop of pressure on its deposit margins, ASB CEO Vittoria Shortt is cautioning savers to be wary of chasing better returns by taking on risky investments.

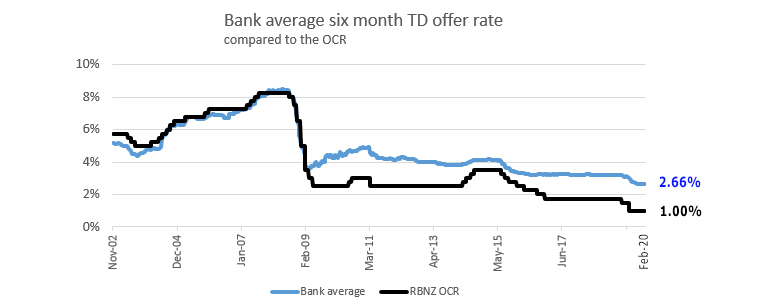

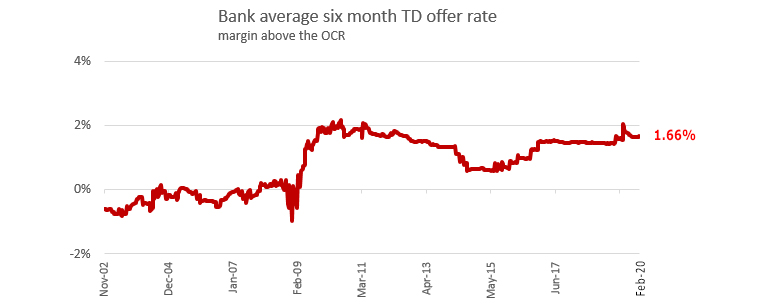

ASB's interim results, released on Wednesday, showed its December half-year net interest margin down 10 basis points year-on-year to 2.13%. The bank attributes the decline to lower interest rates reducing its margins in a competitive deposit market.

The bank's latest general disclosure statement (GDS), also out Wednesday, shows its term deposit book shrank $205 million, or 0.6%, to $33.829 billion over the six months from June 30 to December 31 last year. Total deposits and other borrowings increased $2.501 billion, or 3.8%, to $68.726 billion. Meanwhile Reserve Bank data out earlier this month showed system-wide annual household deposit growth falling to its lowest level in more than nine years.

Shortt told interest.co.nz that New Zealand's record low interest rate environment does put pressure on margins. ASB was seeing a "shift" from customers in deposits, she said.

"We are certainly seeing a shift in deposits that's true. In some cases that might be entirely appropriate if people are removing savings to invest in homes, for example. What would really worry me though is if people are trying to chase better returns by taking on risky investments," Shortt said.

Shortt said there were no particular type of investments she would caution savers and investors about.

"[But] we've seen over time that dynamic. If you look back to previous cycles the last time it happened was finance companies and I think that's fairly well documented. As a general note of caution people need to be really careful about where they're putting their money and what returns are available and the risk profile attached to it."

Although ASB can't fundamentally change the low interest rate environment, Shortt said ASB staff are "actively engaging with our customers." Things ASB's highlighting include its financial wellbeing toolkit, and contacting customers the bank's staff believe are in the wrong products to "help them try to change out into a better product that might suit their needs."

"We're also scanning the market and scanning overseas to see if there are any products that have been successful in overseas markets that might be useful here," Shortt said, adding the bank hasn't found any yet.

Despite the pressure on deposits Shortt said ASB remains "broadly comfortable where the levels are set" in terms of the Reserve Bank's core funding ratio being at 75%.

"So [changing] that's not on my agenda."

The Reserve Bank introduced the the core funding ratio in 2010. It requires banks to meet a minimum share of their funding from retail deposits, long-term wholesale funding and/or capital. The minimum core funding ratio for each bank - on a daily basis - is currently 75%. ASB chief financial officer Jon Raby said ASB is consistently above 85%.

In terms of debt issues, Shortt said ASB was "slightly terming out."

"What we're seeing through that is our wholesale funding costs are broadly flat to stable," Shortt said.

Asked whether the deposit pressure could feed through to lending Shortt said; "We're well funded. I don't have any concerns about being able to lend."

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

55 Comments

Invest in homes. It's entirely risk free.

Until the business/sector you work for runs out of credit (and you as well).

It is only risk-free if you own a home with 100% equity and with adequate insurance.

As homes are the largest investment one can make, other investments are generally less risky as they are smaller in comparison to your net worth.

Well I'm looking to buy a second house in Chch (for lifestyle ... close to restaurants, etc) which I wouldn't be doing if I could even get 3% on term deposits. I'm earning negative returns after tax and inflation, so I may as well live in the money for a few months each year. Noting one important reason, other than growing my girth and seeing my old mum more, is to punish the bank: they lose term deposits and they don't pick up a mortgage over that house.

Another example of how RBNZ stimulunacy is the end of free market capitalism as has by this stage distorted every market and rational decision so much.

Addendum: houses are not risk free though: first they cost to hold (that's why every man and his dog is Airbnbing everything in Chch, or so it seems), plus when the sharemarkets do correct, and I still expect to see S&P correct by up to 67%, which will take our over-valued markets go with it, thus the wealth effect disappears, and everything, including housing, takes a hit (just slower and not as violent as sharemarkets will be).

Would it be fair to assume that if the S&P 500 falls by 67%, our housing market would do the same?

And in terms of actual loss, based on the majority of adult NZ'ers who own homes, and given the median house price in NZ is now approx $630,000, that would be each typical, home owning NZ'er, losing a paper amount of value of around $400,000? And given our economy appear to only be stimulated by the wealth effect of home owning Kiwis, the future as we know it would be a very deep and dark depression?

Would this not, therefore, encourage people to diversify much more and not to buy more houses?

If I thought the S&P was going to fall by 67% I'd be buying gold (which I have..), not another house.

No, I reckon Chch values are flatlining - and for some time now - not a lot off build cost frankly: it's nothing like the sharemarket bubble. Also, if S&P corrects by 67% (Hussman, but the way), the NZX will certainly take a nosebleed, but nothing to that extent. It's US shares that are in Harry Potter land given Fed stimulunancy: they're the most expensive they've been in history.

Yeah, gold, but it has no yield and shouldn't be more than 10% of your savings: plus you can't eat it. I live in Sounds, so a house in inner Chch near the restaurants, for 'me', is a much better idea (plus my mum has dementia, could live for years, we have to make the trip a lot with a dog, so for convenience, it makes sense to buy a property and control out own destiny - finding accommodation is a nightmare with a dog. I don't even care about the 5 year brightline, overly, as I'm mainly in, obviously, cash and fixed income (plus other assets, but that is the main component), all of which are 100% taxed on income and capital gain,indeed, outside my own home, I'm in the lowest yielding assets that get taxed the most viciously because politicians are arseholes, our tax system is far too complex and hence, nonsensical in the main part, but it has to finance a state that is far too big, so I'm no worse off if I sell within 5 years and hopefully have to pay tax (as I will have made a gain) - albeit I don't know if it will hold it's value, it just won't lose half it's value over a couple of weeks.

You obviously know what can happen - using cases such as Ireland and Japan as examples?

Hell, older I get I realise I know nothing, other than patterns and hubristic central command economies (central banks), just like the Soviets, are ultimately always taken out by market reality - that is, price discovery (which has currently been killed, almost totally).

So I don't know what's going to happen anymore than I can time a market, thus other than a lowly correlated to equities Long/Short fund I barely own a single share (and have paid for that over last three years - but preservation of capital is all I care about at this stage of my life).

Sorry, detour. Ireland/Japan ... do you mean property markets or sharemarkets?

There is nothing new under the sun. These stimulunatic markets do correct and the effects will be misery on a huge scale, and impossible to avoid no matter how careful you are (there must be at that stage a reckoning for this utter recklessness of central banks). But the correction will be fast and vicious in shares, the sharp end of the valuation bubble; slow and more negotiable for property, commercial and residential (and at least you can squat in your house while you watch your shares evaporate into nothing :)

Good points Mark - agree with your line of thinking. Just pointing out that if you don't know what is going happen, history suggests its better to be diversified than all the eggs in one basket (which talking to many of NZ older generation, appears to be the case which is a little scary).

Right now, cash is king :)

Not according to Ray Dalio - quite the opposite

Yes, I've read Dalio.

Correction: for 'me' cash is king right now ... I use cash to mean cash and near cash (ie, short term deposits where we're getting better rates than in US).

I got 2.85% the other day for 6 months and rates are on the way up.

Waiting for opportunities to buy 2nd property. I wouldn't go anywhere near an investment less than 6-7% with all the risk out there currently. So cash is king. Looked at a few development sites, the price is build into do ups etc , everyone wants to make money without actually doing anything ..because they ca, ..its insane but its a bubble ..

I've been looking hard for something at a good price that we can add value. I've also got my doubts about development sites, pitfalls for newbies, I wish there were an independent (govt) body which could give advice to newish developers.

Ppl say it doubles every 7-10 years

Depends on the availability of credit.

The trick is to grow debt faster than income for decades to force a massive deleveraging.

Default rates on mortgages are still sitting around 2.5%, which is too high for record low interest rates. If interest rates move up by a small amount our whole economy will be in trouble.

I believe deleveraging will happen through deflation. Money is exiting the system so it becomes more scarce and therefore debt increases in value/weight. Interest rates are not that important.

But aren’t we encouraging young people to take on a lot of debt to get onto the property ladder?

If we would really care about our youth we would point them to the fact that the bottom just fell out of the rental market.

This is where I get confused as the young get labelled as lazy and self centered, while our economy appears to be rigged for the benefit of those who aren't young, who don't want to work, and want to use debt fueled speculation on assets to become wealthy while paying no taxes. And they appear to vote very strongly with self interest in mind, not a utilitarian approach.

Out of curiosity, what do you mean money is exiting the system? Isn't money supply increasing with interest rate cuts?

When debt gets paid off (or written off) the credit (money) disappears. Deflation is literally that, money disappearing from the system thus increasing in value. It will be more expensive for those who choose to hold on to debt plus they will find it harder to move their debt around.

That's why we really need to be focusing on productivity right now, not increasing money supply.

well smart contracts (deposits) with crypto getting just over 7 % - if you know about crypto you probably will also know about defi (decentralized financed) - no banks involved, that's per annum though, which is crypto chump change.... for example a token i follow has been slowly gaining interest is up 50% in a day.... wont happen every day but better than 0% at the bank with 0% guarantee of funds being returned.

Cash deposit with a bank = unsecured lender, plus helps them generate more instacash. please learn about how money is created to lend by banks, if they have a fraction of that amount held as cash deposits. Fractional Reserve Banking or a crypto??? PS: that token up 50% in a day was tixl - not financial advice...

I am nervous about crypto lending, despite the huge gains. That said, I am interested in potentially looking at staking ETH 2.0. Estimates are based on current usage and likely staking percentage, of a return of about 7.0% per annum, with no counter party risk (and Eth is up 115% this year alone).

As for Tixl, I see that gain but it is on a DEX with limited volume. Looks like it hit a low of 1.1 BNB and now is back at 1.62 BNB. It was 8 or so BNB at one point. I exited my position some time ago but am still watching it. Join the telegram groups for Tixl if you want to chat more about that one.

PS - here is an Alt for you, WAX. Was up 120% at one point yesterday, they are suggesting a gaming partnership with Disney

Sounds like you're sourcing from Nuggets News as Alex has been talking the same book. Guy was even bullish on XRP, which was a surprise as he's talked it down.

Asked whether the deposit pressure could feed through to lending Shortt said; "We're well funded. I don't have any concerns about being able to lend."

They certainly are:

We start with the idea of credit creation, specifically a swap of IOUs between a bank and myself involving a bank loan that is my IOU and a bank deposit that is the bank’s IOU. Nothing could be simpler, and yet the mind rebels, especially the well-trained economist’s mind, because this simple operation increases my purchasing power without decreasing anyone else’s. It seems like alchemy, or anyway a violation of some deep conservation law. Real productive resources are the same as they were before, and the swap doesn’t change that, does it? Spending of the new purchasing power adds another layer of perplexity.

If spending increases but real resources do not, then it seems logical that the increased spending must exhaust itself in higher prices—that is the intuitive appeal of the quantity theory of money. My purchasing power may increase, but everyone else’s decreases because their money balances buy less. From this point of view, the alchemy of banking seems like a kind of theft, something to be deplored in the name of economic science and if possible outlawed in the name of the general good.

A simple concrete example may help to fix ideas. Let us suppose that the swap of IOUs is a mortgage loan, and that I use my new purchasing power to buy your existing house. At the instant of sale, I swap one asset for another, and you swap the other way around, presumably because each of us prefers the asset held by the other. For present purposes, the important point to appreciate is that the alchemy of banking has made this sale possible, by creating new means of payment that you are willing to accept. After the sale, the bank’s new IOU is owed to you instead of to me. In fact, by accepting the bank’s IOU as payment, you are funding the bank’s loan to me, at least temporarily.

But that’s not the end of the story. You were willing to accept new purchasing power as means of payment for your house, and in doing so you wound up funding the bank’s mortgage loan in the first instance. But by no means does that mean that you are willing to fund the loan for its entire term. Indeed, what matters after the moment of payment is not so much your own portfolio preferences as the preferences of the rest of the world to whom you pass along the new purchasing power as you spend it. The question is, when you are no longer funding the loan, who is and in what form? Read more

The whole purpose of low interest rates is to get people investing in riskier assets. In the case of these emergency level interest rates it is to invest in return free risk such as bonds. Deliberate mispricing of financial instruments from central planning organisations such as the Reserve Bank (who should not be allowing misallocation of capital). In the current environment it's everyone's retirement funds that are at risk, more so in the US where their pension and retirement systems are caving in due to the demographic issue of the boomers retiring.

Pretty sure my grandparents managed to live comfortably throughout their retirement on the interest from their savings (80’s/90’s). Low risk, comfortable return.

Boomers may have a lot of wealth in property, but from those I’ve talked to, wouldn’t be able to do the same now (live off savings interest alone). The perceived wealth they have is simply that in my opinion - my grandparents likely had far less (relative price of home) but because of interest in savings, appeared to be far more comfortable/content in retirement than the boomers.

The whole purpose of low interest rates is to get people investing in riskier assets.

Not necessarily:

This is what Milton Friedman called the interest rate fallacy, and it indeed refuses to die. We can tell what monetary conditions are in the real economy, as opposed to financial liquidity, though the two can be linked, by the general level of interest rates. When money is plentiful, interest rates will be high not low; and when money is restricted, interest rates will be low not high. The reason is as Wicksell described more than a century ago:

"[The natural rate] is never high or low in itself, but only in relation to the profit which people can make with the money in their hands, and this, of course, varies. In good times, when trade is brisk, the rate of profit is high, and, what is of great consequence, is generally expected to remain high; in periods of depression it is low, and expected to remain low.

When nominal profits are expected to be robust, holders of money must be compensated for lending it out by higher interest rates. Thus, the same holds for inflationary circumstances, where nominal profits follow the rate of consumer prices. During the Great Inflation, interest rates weren’t low at all, they were through the roof well into double digits and higher by 1980. At the opposite end in the Great Depression, interest rates were low and stayed there because, as Wicksell wrote, the rate of profit was low and was expected to be low well into the future. High quality borrowers were given as much money as they could want while the rest of the economy was deprived of funds; liquidity and safety being the only preferences in what sounds entirely familiar. Link

{kind=link}

Not necessarily. Quite so. The low interest rates encourage people to spend, and the banks play a covert part in that. Remember the unsolicited mark up of the limit on your credit card. The dulcet tones, now you can afford that new lounge suite, upgrade the car, take a vacation. As IO relates to his grandparents, it needs to be remembered than up to the mid 1980’s there was scarcely any ability to incur personal debt. Borrowing was done on the tick, HP, lay by not by credit cards which have made borrowing both non specific and open ended, so much so that I believe far too many of the following generation(s) fail to distinguish the difference between money in their pocket that has been earned and money borrowed. I would wager that the average fifty something parent today would have one heck of lot more personal debt than the counterpart of 1985.

As my quote noted:

High quality borrowers were given as much money as they could want while the rest of the economy was deprived of funds; liquidity and safety being the only preferences in what sounds entirely familiar.

Banks extend 60% of their lending to one third of NZ households to buy leveraged residential property assets (~$460,000 for each household on ave.) - this class of collaterallsed bank asset is significant and represents undue concentration risk, unlike that which you refer to.

I think in the current environment, where we have such low interest rates used to try and maintain the 2% inflation target, much much higher LVR should have been enforced. Simply because people can service debt at such low rates, coupled with a FOMO mentality, means we have created asset bubbles that didn't need to be formed. Instead of making productivity the incentive, its result is FOMO speculation.

This is where I don't get the 2% inflation rate target we use - the available money is being leveraged into debt via fractional reserve banking, and technology appears to be pushing down many basket items measured in CPI, so all we appear to be doing is blowing asset bubbles, instead of sound monetary management/market stability. If anything, the reserve banks of the world are creating the instability, not preventing it.

In my opinion, if we want to operate in this low interest rate environment, LVR settings should have been much much more restrictive to prevent the situation we've found ourselves in.

Audaxes,

"Not necessarily:" Consider the following quotes;Former PM Theresa May-"Monetary policy-in the form of super-low interest rates and QE-has helped those on the property ladder at the expense of those who can't afford to own their own home".

Anthony Randazzo of the Reason Foundation; :QE is fundamentally a regressive redistributive program that has been booting wealth for those already engaged in the financial sector, or those who already own houses, but passing little along to the rest of the economy".

In 2012, A BOE report showed that its QE policies had benefitted mainly the the wealthy and that 40% of the gains went to the richest 5% of British households". In May 2013, Richard Fisher, President of the Federal Reserve Bank of Dallas said that cheap money had made rich people richer but had not done quite so much for working Americans.

The problem is that these so call 'emergency low ' interest rates are now seen as the new normal.Obviously ASB are seem people move money out of the bank into housing, because many people see that as low risk, and if the financial markets crash, people still have their house as is a physical asset. While people are not able to insure the money they haven't he bank, and the governments deposit guarantee scheme will only be fora tiny $50k per bank, so it appears for many,one of the only places to protect your money is put it into a house.. There are a huge number of FOMO house buyers out there at the moment, probably overpaying for a limited supply of houses

If said financial market crash happens, people will lose jobs right? And without jobs it is hard to make mortgage repayments. So to buy a house for security is fine, but you'd want to be sure that you don't have too much debt associated with it - as if the recession comes, and you lose your job, good luck convincing the bank that the house which you can't make repayments on is a good place to protect your money.

So to buy a house for security is fine, but you'd want to be sure that you don't have too much debt associated with it - as if the recession comes, and you lose your job, good luck convincing the bank that the house which you can't make repayments on is a good place to protect your money.

Part of the problem with housing is that many purchase decisions have been made on the asummptions A.) It provides shelter (consumption good); and B). It'a a de facto savings instrument in that 'the house also makes me money.'

Now re B, the problem is that 1.) Most people have no idea how much the house as an asset will appreciate by; and 2.) If the house price appreciation doesn't meet expectations (usually this is measured by rather suspect constructs), this can actually influence consumption behavior (think of it like a negative wealth effect, even if house prices haven't been exposed to a market crash).

A recent study in oz showed those who were house-owners have drastically higher savings and assets compared those who did not buy a home and continue to rent. Strange that. Actually no it's not strange its reality. They should have also asked which group is happiest.

Funny odd though, as the past days or so, the ASB & ANZ (our fave lender).. mentioned the opposite of drastically higher savings.. here on this beloved interest.co.nz - But like you said, may be? the NZ deposit savings, slowly moved to OZ buying cheaper/quality housing as compare to NZ, enjoying lower grocery bills, alas.. the deposit rates is lower than NZ but hey, they got 250K govt guarantee as oppose to NZ (this April?) of just 30-50K guarantee - So, like other sentimental findings, seems the OZ enjoying the funds flight movement from the flightless bird here.

Well how about you offer a higher level of interest for saving? Or how about we remove RWT from deposit account to encourage savings?

Or are we afraid our economy is false, in that it’s only based on increasing debt by lowering interest rates - instead of saving and productivity?

Go one better than removing RWT on interest. Exempt the first $5000 in interest from Bank deposits from tax altogether. That would give comfort to elders living on interest.

Tax system is warped.....young people attempting to save for first home are paying RWT and by the time you adjust for inflation, the money they are saving isn't increasing in purchasing power at current rates. Those that own property have no CGT and using a market of fractional reserve banking....its like a casino but the house (excuse the pun) is rigging the game - but doesn't realise that by winning in the short term, it will lose in the long term.

do they offer information on the maturities of their TDs,how much is longer term?they might also be getting nervous about the majority of the money moving to shorter maturities because of the flat yield curve.filling out the tax form this year could be a wake-up for some when they see the pitiful return on their savings compared to past years.

Kiwiwealth managed funds.

Yes, I agree "people should be really careful about where they put their money". That's why I have diversified a large portion of my term deposits away from the ASB; I have split those among the ANZ and the BNZ. Remember both ASB and BNZ both had to be sold to big Australian banks when they got into trouble in the late 1900's.

I also have a share portfolio with "Z Energy"( which is about the only stock currently rated a "buy" by Morningstar), "Fletcher Building" ( should be ok if Labour can carry out all the planned infrastructure over the next 5 or 10 years) and "Trustpower" which Infratil (its majority shareholder) absolutely refused to sell when it was looking to acquire Vodafone...it is the jewel in their crown. I admit that up until this point Fletchers has been NZs worst run company ever and they even now keep shooting themselves in the foot but surely.......?

And Z Energy and Trustpower are both subject to kneejerk regulation by government, as "Telecom (Spark)"and "Chorus" were under the last National government albeit for only a short time.

A while ago, they removed ability to deduct for depreciation (reason given was, its just "deferred" taxation anyway to stop people speculating in property. This sledge hammer was used to smash long term buy and hold investors together with speculators, resulting in massive shortage of houses. Did removing ability to deduct for depreciation bring down asset prices? BIG no. Will playing with market forces ever achieve the pronounced affect. Never. therefore, let the market play it out. Stop scarying people by saying money in your bank at pittance deposit rate is the most solid and houses are most risky. Invesments, any investments with calculated risks and reasonable gearing ALWAYS works.

"resulting in massive shortage of houses" there is no shortage of houses in NZ never has been.

we have a lot of government policies that distort their usage and treatment.

why can not a FHB deduct interest payments but an investor can ? why are new builds not treated more favourably than existing houses for investors ? (if you want to increase supply) why is buying new builds rather than existing houses treated differently by the government and banks

why do banks treat investors better than OO.

i have a friends that has 300K on TD with ASB (mortgage free) after the ASB CS told them that was the safest place to put their money, as usual they have not heard of the OBR or they are classed as investors in ASB by the RB

they were looking at a investment property but with all the new rules found to hard ( they were looking at buying an existing property)

so they are nibbling away at managed funds to see how that works, and having a look into commercial property (not schemes)

maybe they should just buy a house and leave it empty and pay off the mortgage, they will still get the CG without the pain ( a lot are doing it )

Agreed, there is not a shortage of houses in NZ!

There is a shortage of affordable homes in Auckland, that are affordable for many people.

The main reason houses have increased so much is due to overseas born buyers.

Speculators have jumped on the bandwagon just like the speculators did in the share market prior to the collapse in 1987.

Crazy leaving houses empty rather than renting them out when the returns on investment are so good compared to other rates of return and safety.

The Man, Auckland has a drought .. of affordable homes. Please send some chch affordable homes to Auckland.

Streetwise,

Based on that post, Streetwise isn't the term I would immediately think of. Do you remember when diversification meant having several finance company holdings? Your approach is somewhat similar. Why no Rabobank say? or TSB? Now, when Deposit Insurance comes in, then up to $50,000 in any bank will be ok.

Your 'portfolio' is even less impressive. Fletchers? Really? Then you have both Infratil and Trustpower in a very limited portfolio-only 4 stocks-that makes little sense. You really prefer Z Energy to F&P Healthcare, or Mainfreight or several others I can think of? I think you should seriously consider an Index fund.

ASB is feeling the pinch because they are offering rates that are at the rock bottom of the current market. Yet the bank has had record profits in recent years Add to that the situation where their staff don't have the level of knowledge required to respond to quite basic queries from the public, and it becomes clear that the days when the ASB was a great bank to deal with have long gone.

Why not.. ? try to shift all your idle funds into govt. guaranteed, stable, productive economies of ASEAN countries.. they average return is about 4-5% - OZ & NZ are s..t holes from the point of productivity return. They'd liked to sit idle hoping that the promise of gold deposits underneath it's land/RE speculation will forever bring up/maintain these countries GDP index. YR... says Tui ads.

Nice article from a CEO trying to scare people into putting money in their bank for a return that wont even keep up with inflation. People are not that stupid. The return on a 5 year deposit would be ludicrous at 2.5%. You'd be losing money after taxes and inflation.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.