The RBNZ has published this Statement.

New Zealand’s financial system remains sound, with strong capital and liquidity buffers.

Assistant Governor Christian Hawkesby said the Reserve Bank is actively involved in financial markets to ensure smooth market functioning despite the global uncertainty from COVID-19. Regular market operations continue to ensure there is ample liquidity in the financial system.

“The measures we are implementing today provide additional support to domestic financial markets. We will ensure our operations make financial markets operate smoothly,” Mr Hawkesby said.

"We are working in tandem with the banks, the wider financial market community, and the Government."

The provision of term funding

The Term Auction Facility (TAF) is a program that will alleviate pressures in funding markets. The TAF gives banks the ability to access term funding, with collateralised loans available out to a term of 12 months.

Banks currently have robust liquidity and funding positions and can manage short-term disruptions to offshore funding markets. The opening of the TAF will provide confidence that the Reserve Bank stands ready to support the market if needed. Further operation details on the TAF are available in a Domestic Markets media release.

Providing funding in FX swap markets

The Reserve Bank is providing liquidity in the FX swap market, to ensure this form of funding can be accessed at rates near the Official Cash Rate (OCR). This activity will increase in the weeks ahead to support funding markets.

Re-establishment of a USD swap line

The Reserve Bank has re-established a temporary USD swap line with the US Federal Reserve. This will support the provision of USD liquidity to the New Zealand market, in an amount up to USD 30 billion. This is a facility that is being offered to many other central banks globally.

Supporting liquidity in the New Zealand government bond market

The Reserve Bank has been providing liquidity to the New Zealand government bond market to support market functioning.

Ensuring a robust monetary policy implementation framework

To support the implementation of monetary policy, the Reserve Bank is removing the allocated credit tiers for Exchange Settlement Account System (ESAS) account holders. This change means that all ESAS credit balances will now be remunerated at the OCR. Under the previous framework, banks were charged a penalty rate on deposits of cash balances above their allocated credit tiers.

The removal of credit tiers for ESAS account holders will provide additional flexibility for the Reserve Bank in its market operations, by keeping short-term interest rates anchored near the OCR regardless of the level of settlement cash in the system. This framework for monetary policy implementation (i.e. a floor system) is common among other central banks overseas.

The Reserve Bank will continue to monitor the use of our liquidity facilities and ESAS settlement accounts. We anticipate that liquidity will continue to be distributed efficiently throughout the banking system. If not, we will review our framework for monetary policy implementation as needed.

A commitment to market functioning

The Reserve Bank has a number of tools to provide additional liquidity and the ability to increase the size of operations where needed. We are committed to using these to support smooth market functioning.

In addition to the tools listed above, the Bank has an established role to provide liquidity in the New Zealand dollar foreign exchange market in periods of illiquidity or dysfunction, and is operationally ready to undertake this role if required.

Mr Hawkesby reiterated that the Reserve Bank continues to monitor developments, and remains ready to act further to ensure markets and the financial system operate in a stable and efficient manner.

More information:

- Domestic Markets media release: Reserve Bank announces new facility and removal of credit tiers

- Federal Reserve announces the establishment of temporary U.S. dollar liquidity arrangements with other central banks

Below are comments from Westpac NZ chief economist Dominick Stephens on the RBNZ's action.

The Reserve Bank has announced a range of measures to support stressed financial markets. These measures were necessary, and we applaud the RBNZ’s proactivity. These actions will help keep short-term interest rates low. However, the RBNZ needs to do more to prevent long-term interest rates from rising unhelpfully.

- A Term Auction Facility. The RBNZ will lend to banks for up to 12 months, taking Government bonds, residential mortgage-backed securities, and other bonds as collateral. This basically ensures banks will be well-funded for the foreseeable future. This will prevent an increase in the cost of bank funding, which in turn will help ensure that short-term interest rates for businesses and households remain low.

- FX swap market funding. Banks sometimes borrow money from offshore and swap the debt back to New Zealand dollars. In recent days the cost of performing this swap has exploded. Left unchecked, this could have caused an increase in the cost of funding New Zealand banks, which in turn could have led to higher interest rates in New Zealand. The RBNZ has essentially offered to facilitate some of those swap arrangements, which will keep the cost of overseas funding contained.

- The US Federal Reserve and the Reserve Bank of New Zealand have established a $30bn US dollar swap line. This will enable the Reserve Bank of New Zealand to borrow US dollars if it needs.

- Providing liquidity in NZ Government bond markets. As we noted yesterday, the interest rate on New Zealand Government bonds has shot higher because bond market liquidity has dried up. Yesterday the NZ Government borrowed at 2.6% for 17 years, whereas last week the interest rate would have been 1.3%. The RBNZ is now actively buying NZ Government Bonds on the open market, in an effort to provide liquidity. However, the amount of liquidity provided seems tiny so far, and has had little effect on longer-term Government bond rates.

- The RBNZ is now paying the OCR on all cash balances banks hold at the RBNZ (previously, banks were paid a lower rate if they held large balances). This will give the RBNZ greater control over short-term interest rates, keeping them closer to the OCR.

Yesterday we predicted that the RBNZ would have to take actions similar to these to calm stressed financial markets and reduce the cost of bank funding. The ultimate aim of these actions is to prevent New Zealand interest rates from rising in an unintended way, because higher interest rates would worsen the economic downturn.

Today’s actions are likely to be effective at keeping short-term interest rates down, and will allow banks to continue lending smoothly.

However, so far the RBNZ has announced little that will effectively reduce long-term interest rates. In the wake of the RBNZ’s announcement, long-term Government bond rates have fallen only 10 basis points or so.

We suspect the RBNZ is going to have to begin a Quantitative Easing program very soon, similar to the Reserve Bank of Australia’s move yesterday. This would involve buying large quantities of Government bonds, which would reduce long-term Government bond rates.

The other way to keep longer-term Government bond markets calm is for the New Zealand Government to ensure that any future stimulus measures are temporary. Markets need to be assured that the Government has a plausible path to repaying the large debt it is going to incur as it cushions the economy through the Covid-19 recession.

25 Comments

This is more like: Reserve bank is the lapdog of retail banks and will do anything to ensure the status quo remains (high house prices, high asset prices, no productivity etc etc)

Throw likely increasing unemployment, slumping consumer demand and dire business confidence and we can all see where this is going.

Hear this morning the tourism association is talking about 100k job losses in the next 3 weeks.

Helicopter money incoming! Then most likely inflation... then I expect the RB to ignore inflation rate targeting in an attempt to inflate away debt...

The evolution of the RBNZ mandate. Started with CPI inflation targeting, added employment, then get rid of inflation targeting. China had inflation of 5% before this blew up and they started printing like crazy. .

I'm glad somebody else can see the writing on the wall.

The RBNZ will do its best. But nothing can prevent a 30% to 50% slump in house prices. The fool's paradise of fake wealth based on parasitic housing speculation is coming to an end.

Looks to me like the GFC liquidity crisis playbook reenacted.

Fed to the rescue of globalisation again.

Wonder what kind of impact this will have on USD this time around?

Except this time it's a pandemic so there is no moral hazard rescuing any institution. We are going to witness unprecedented stimulus, whatever it takes as Lagarde said.

Ever since the Fed announced, and conducted, its “massive” $500 billion “repo” operations, there’s been very light demand for them from the money dealers at the center of this monetary storm. Given these market fire sale conditions, obvious signs of gross systemic illiquidity, the Fed’s auctions should be bid full up to the limit each and every one. The demand for liquidity, any spare liquidity, is through the roof curiously everywhere except here.

The answer can only be collateral. In order to bid for the Fed’s bank reserves in any of these FRBNY operations, you have to post some of eligible MBS, agency debt, or UST’s. And when you do, whatever collateral you put up becomes encumbered (which means no repledging).

Dealers are obviously not doing so, and encumbrance is as likely a culprit as is the lack of spare collateral. If this is all new to you, I urge you to read my overview of this relatively unexplored yet central piece of the global monetary function, which includes explaining the utility of negative yielding instruments like T-bills. The intro is here, the diagramming here. To sum those up:

If only you had enough pristine collateral sitting idle on your balance sheet where you could substitute that unassailable security in repo and therefore maintain the funding you need in order to bury that illiquid monster somewhere on the balance sheet until the storm passes – and its value goes back to up to reflect a more reasonable and fundamental level. That substitution ability buys you the most valuable thing in a crisis – time.

The “illiquid monster” of GFC2, the bottleneck I’ve been writing about for years, is that class of risk corporate credits in CLO’s, leveraged loans, and other forms of junk (including and especially those issued in Eurobonds). Like the “toxic waste” of GFC1, subprime and other varieties of mortgage securities, corporate junk has become increasingly illiquid putting enormous strain on collateral chains – the very bottleneck dealers have been increasingly afraid of and hedging against as the lie of globally synchronized and too many Treasuries transformed into the reality of globally synchronized downturn and so obviously not enough collateral.

What are collateral chains? I urge you to read about repledging and collateral multiplication here. To sum this up:

Starting in 2016, however, things collateral-wise began to pick up for the first time. According to updated estimates from Manmohan Singh, the total volume of pledged collateral grew modestly from $5.8 trillion in 2015 to $6.1 trillion. But with the 2017 introduction of the slogan “globally synchronized growth” and consistent official emphasis on it, the aggregate exploded to $7.5 trillion – an increase of 23% for this money market that hadn’t really seen any kind of growth in nearly a decade.

The most worrisome part was this:

More importantly, I believe, the sourcing of collateral. The vast majority of it came from the “securities lending” side of things, $400 billion more in 2016 and 2017 compared to $200 billion due to hedge funds.

And those are estimates drawn only from visible sources (footnotes). Who knows what the real figure might be for the totality of global US$ shadow money, this eurodollar system. An enormous amount of pledged, repledged, and, at times, rehypothecated securities all predicated on the introduction of the worst kind of junk credits. Link

We are going to witness unprecedented stimulus, whatever it takes as Lagarde said.

Heard that before from Draghi - I guess it will be just more of the same then?

Stagnation Never Looked So Good: A Peak Ahead

Forward-looking data is starting to trickle in. Germany has been a main area of interest for us right from the beginning, and by beginning I mean Euro$ #4 rather than just COVID-19. What has happened to the German economy has ended up happening everywhere else, a true bellwether especially manufacturing and industry.

The latest sentiment figures from ZEW as well as IFO are sobering. Taking the former first, it had been quite buoyant last year on the false promises, I believe, of last year’s ECB QE introduction. The sentiment index had jumped positive though frustratingly in the same way it had falsely or prematurely done so in the past. Survey respondents seem to love their “stimulus” even after watching it fail to stimulate anything twice before.

The ZEW sentiment index was already on its way back down by the time the pandemic broke out of China. Last month, the number was just +8.6. The latest estimate is -49.5, the lowest since Europe’s 2011-12 recession.

PIGS spreads tightened significantly following Draghi's comments. Greece went from mid 20's to 2%, and they fell 130bp last night after Lagardes comments. Only the ignorant wouldn't understand the magnitude of those moves.

Are you suggesting their economic fortunes are better than Germany's because their respective yield spreads to bunds narrowed, since bankers saw a buying opportunity to deliver securities to the relevant authority for a quick turn?

No, that's not what I'm saying. In Greeces case, the ECB prevented it from becoming an Argentina and that's a very good thing.

A slow motion train wreck is still a train wreck

Someone suggested WWC, but maybe WWR is better - World Weimar Republic?

Wonder what kind of impact this will have on USD this time around?

Onwards and upwards so far.

The temporary USD swap line, and the countries offered support, is the clearest indication that any country which has aligned itself or continues to align itself with China will be at the mercy of the markets in the coming weeks.

Yeah, interesting geopolitics. I wonder whether Brazil had a window opened to them with the Fed during the GFC?

Why didnt the RBNZ do this yesterday?

They say they are listening to banks.. well NZ's biggest bank told them the NZ Govt bond market was broken and they needed to intervene. What was the response:

Orr: we are watching and nothing is unanticipated

Hawkesby: remember to wash your hands

NZD was extremely volatile overnight as the market grappled with the inaction of the RBNZ relative to the Fed, ECB and RBA.

In this market, having confidence in the ability and commitment of the central bank is paramount... and the RBNZ did themselves no favours yesterday.

I'm perplexed as to why Aud/NZD is nearly at parity given the respective performances of the RBNZ and RBA. Lowe looks dynamic, polished and in control while Orr appears totally disengaged and almost irritated.

- FX swap market funding. Banks sometimes borrow money from offshore and swap the debt back to New Zealand dollars. In recent days the cost of performing this swap has exploded. Left unchecked, this could have caused an increase in the cost of funding New Zealand banks, which in turn could have led to higher interest rates in New Zealand. The RBNZ has essentially offered to facilitate some of those swap arrangements, which will keep the cost of overseas funding contained.

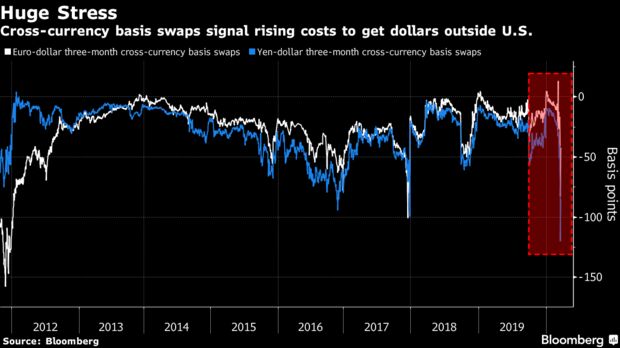

Big basis point cost increases:

3y NZDUSD xCCY is trading at ~NZD BKBM+36/USD LIBOR

5y NZDUSD xCCY is trading at ~NZD BKBM+40/USD LIBOR

Are you suggesting the RBNZ is going to intervene in the basis market? That's not my understanding.

Not at all. Just pointing out the reality of the liquidity premium being demanded from NZ bank counterparties if they were to enter into these swap agreements, at these prices. But I guess the NZD lender (supranational?) who is in receipt of the USD basis points wants the discount to USD Libor financing to facilitate the trade. What the RBNZ intends to do other than subsidise the arrangement is hard to know.

What I do know is that NZ depositors deserve a higher risk adjusted return for basically underwriting the NZ banking system. Foreign lenders are not worth the tribute they demand.

NZ isn't alone, all the basis spreads have blown against the US$. Clearly there is a $ funding squeeze,but it will dissipate

Clearly there is a $ funding squeeze,but it will dissipate

Exactly - that's why most have gone to a negative basis, not more positive - hence the US dollar lender is in receipt of the basis - view graphic evidence. Our local NZ banks are USD swap lenders, but are subject to a NZD leg liquidity premium, hence they pay the positive basis.

{kind=link}

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.