The mortgage deferral pile is shrinking rapidly.

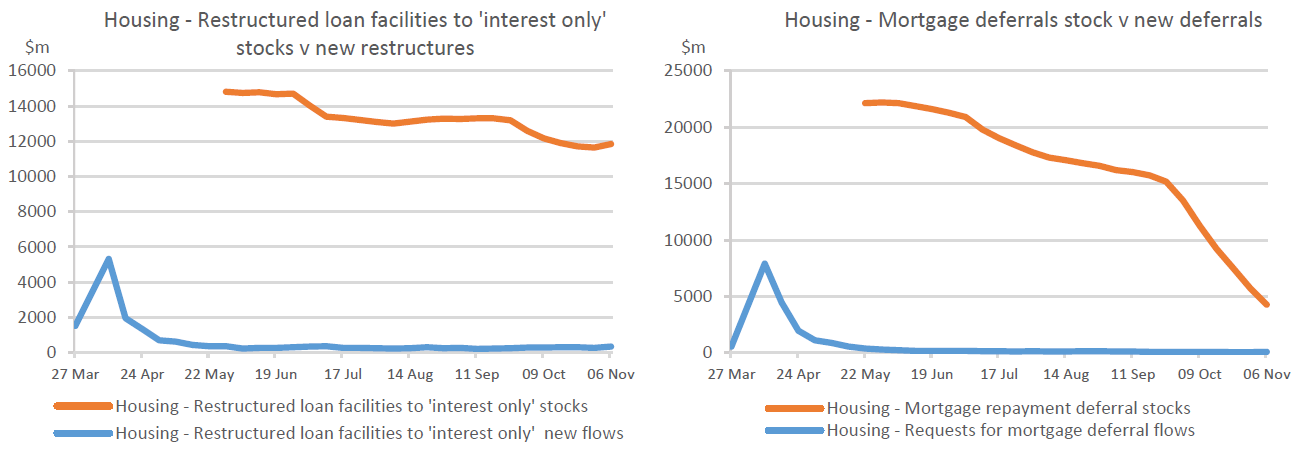

New figures released by the Reserve Bank on Monday show that as of the first week in November just $4.262 billion worth of mortgages were still on full deferral - IE no payments being made.

This contrasts with the more than $22 billion (about 7% of total mortgage stock) that was on full deferral at the end of May.

The mortgage deferral scheme was first announced by the RBNZ on March 24 at the height of the Covid crisis, as the RBNZ sought to ease the load for the public ahead of an expected torrent of job losses.

At peak more than 60,000 mortgage holders took advantage of the scheme, which was initially slated for six months.

The RBNZ then extended the scheme towards the end of August.

It now runs to the end of March 2021.

But with job losses being lighter than expected and, crucially, with the housing market having taken off, there appears to have not been much take up of the extension.

The RBNZ's figures show that as at the end of August there was about $16.5 billion of mortgage stock on a full payment deferral. This dropped to $15.6 billion by the end of September.

And then there was a massive drop during October to just $5.7 billion by the end of that month.

This sharp rate of fall has continued into November.

Also falling, though not as drastically, is the amount of mortgage money on which payments have been rescheduled to interest only.

Nearly $15 billion worth of mortgages had their payments rescheduled this way by the end of May, but by the beginning of November this total was down to under $12 billion.

11 Comments

I wonder how many are now paying interest only or extended their loan terms?

Great to hear. The NZ situation is looking far better than initially predicted. The Global economy isn't out of this storm yet though.

Isn't the economic situation in NZ supposed to get worse next year, and won't job losses pick up? I am wondering why so many first home buyers seem to want to get into such huge debt to buy a house now post lockdown, after seeing teh stress that mortgage holders got put under when teh first lockdown occurred. Also often being younger, FHBs some could the the ones who are at higher risk of losing their jobs. We just need undetected community spread to occur, and Auckland or NZ could go up levels, and cause more business closures. So far we have been lucky and also done well, but things can easily change. Especially if we try to open tourism too quickly, and the virus gets a foothold again leading to another nationwide lockdown.

I don't think they saw mortgage holders as being under stress so much as making tens of thousands each month. With no work.

Certainly that occurred afterward. But I do wonder if things in the market would have bee very different if we had done as badly as the UK or Europe. with the rona. Although I guess the cheap money is fueling asset bubbles all over the world now.

Goosing prices is a great way of preventing equity problems for those already in homes. Not so great for getting FHB in

The problem is, that's not the RBNZ's mandate.

Really ? It’s the only part of the economy that is “performing” entirely due to the RB settings.

they realised it wasn't really a holiday

There seems to be one stat that is missing on RBNZ's website under Lending and Money stats and that is non-performing loans and defaults resulting in re-possession

Absolute numbers do not give a feel for the extent of the problem. Is there sufficient bank capital adequacy to avoid an OBR if all those on interest only were to default? This is an extreme case but one can always reverse engineer the numbers by saying what proportion of the deferred mortgages can the bank capital support if the deferred mortgages were to default. Of course in default not all is lost as the bank can sell off the defaulted asset minimising their loss.

So there are thousands of households who do not have sufficient income to make any mortgage payments. These are the ones who are in real trouble due to lost jobs and failed businesses. Not those who just took the holiday at the start of Covid lockdown as it was no questions asked. What is the breakdown by region? What is the average mortgage amount? The banks should be encouraging them to sell now while the market is good.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.