New Zealand banks produced record quarterly profit in the March quarter, according to KPMG’s latest quarterly Financial Institutions Performance Survey (FIPS).

March quarter net profit after tax surged 21% to $1.643 billion, up from $1.361 billion in the December 2020 quarter. The main drivers were increased housing lending, higher margins, increased non-interest income, and the reversal of loan provisions booked at the onset of COVID-19.

However, the fact that bank profits have bounced back strongly won't be news to regular interest.co.nz readers. Thus we've delved into five other topical issues aired in the March quarter FIPS. These are detailed below.

1) Do we need more cyber security regulation?

Cyber security is becoming an even bigger focus, if that's possible. The FIPS highlights the summer cyber attack on the Reserve Bank, and suggests cyber security could be seen as under-regulated.

"New Zealand has minimal regulation with regards to cyber security, which no doubt contributes to a relatively low level of maturity for many of New Zealand's organisations."

"A number of recent high-profile cyber attacks or data breaches have highlighted the need for many organisations to increase their cyber security. This is particularly applicable to our banks which hold significant data both in nature and amount," KPMG says.

"The Reserve Bank has already issued draft guidance on what regulated entities should consider when managing cyber security risk in October 2020. Rather than waiting for regulation to be finalised or for another incident, banks should be evaluating the effectiveness of their existing controls."

The Reserve Bank issued guidelines for the financial sector on cyber resilience in April. This guidance, the Reserve Bank says, is a framework for the governance and management of cyber risk, which entities can tailor to their own specific needs and technologies, rather than a detailed or technical set of instructions.

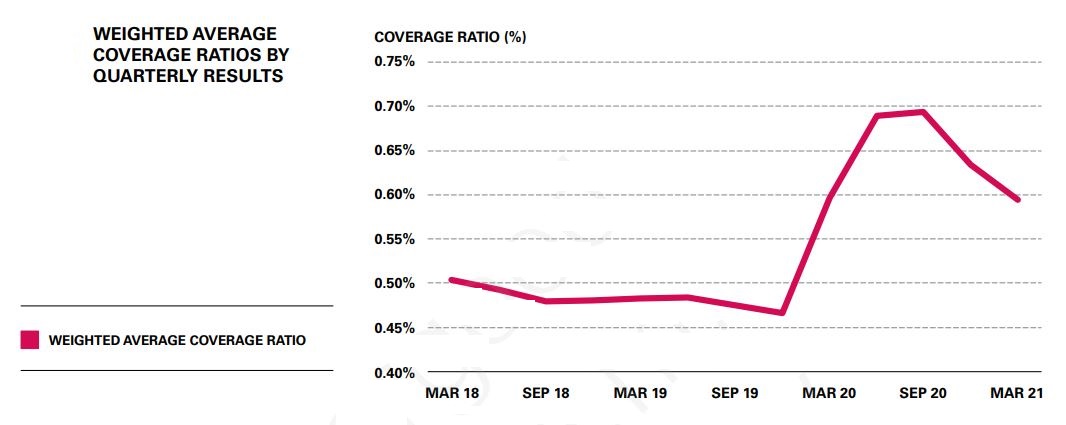

2) Loan provision releases rack up, but some are held in reserve.

At the onset of COVID-19 last year banks ramped up their loan loss provisions. But when the world didn't end they started releasing some of them, bolstering profits. Over the December 2020 and March 2021 quarters, New Zealand financial institutions made a combined net release of $202.6 million impairment expenses, KPMG says.

However as the chart below demonstrates, there's still some way to go to get back to pre-COVID levels.

"It would seem from the pace of the release, that most financial institutions' senior management might be taking a balanced approach with the releases as there are still some uncertainties with respect to the future economic outlook," KPMG says.

3) COVID-19 challenges banks' forward looking loss provisioning models.

KPMG also notes the predictive models supporting loan loss provisioning were built to meet point-in-time forward-looking expected credit loss estimates. But over the course of about a year, economic indicators moved from one extreme to the other. That means the loan loss models have been dealing with a high level of volatility and uncertainty.

"These models have never been trained to read across sudden contraction and expansion of the economy as most financial instructions' historical data used for the modelling exercise comes from a benign period. In addition, these predictive models were not designed to consider the effects of active government intervention."

"As such, management have become more cautious when analysing the outputs of the forward looking provision models as it may in some cases not align with their expectation. In theory NZ IFRS [International Financial Reporting Standard] 9 is expected to result in volatility in the level of provisions as economic indicators change," KPMG says.

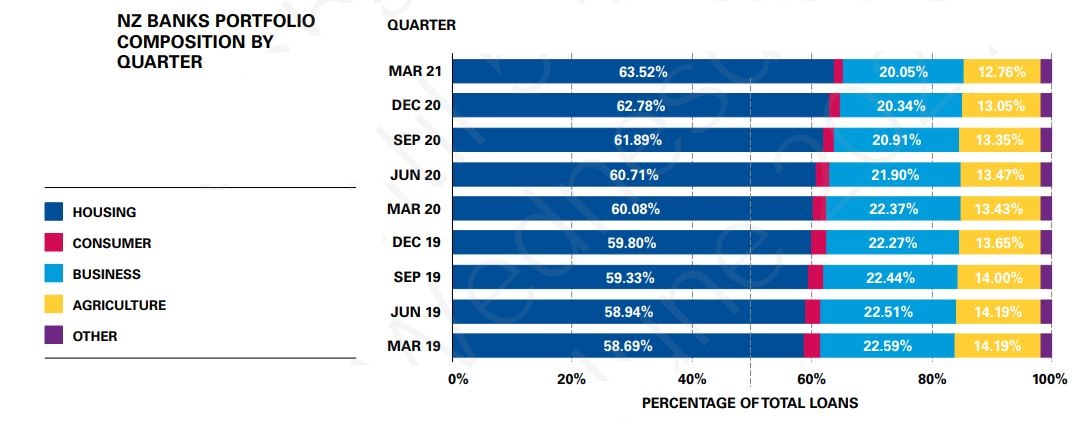

4) Housing lending growing as a share of total bank lending.

Regular interest.co.nz readers will be well aware that the housing market has been going ballistic, with record volumes of home loans being written by the banks. They'll also be aware that this surging mortgage growth, and slowing business and agriculture lending, means housing loans are growing as a percentage of banks' total home loan books. In May I asked ANZ NZ CEO Antonia Watson about housing lending rising to 69% of total ANZ NZ lending.

The FIPS chart below nicely encapsulates this move across the industry.

5) Climate-related accounting standards near.

With the Financial Sector (Climate-related Disclosure and Other Matters) Amendment Bill before Parliament, banks, insurers and others face being required to make climate-related disclosures in line with climate standards issued by the External Reporting Board (XRB).

The XRB is a Crown Entity responsible for NZ accounting, plus auditing and assurance standards. The XRB is expected to release its draft climate reporting standards from July 22. Annual climate statements will be required for financial years from 2022 once the Bill passes. Thus first mandatory disclosures are likely in 2023.

"The XRB's standards are intended to inject clarity and consistency into the field of climate reporting in New Zealand. The hope is to significantly increase not just the quality, but also scale of climate related reporting by New Zealand businesses. This will, in theory, see the financial sector improve the quality of its own climate-reporting - leading to a more efficient allocation of capital that steers us to a more sustainable future," KPMG says.

There will be some interesting considerations for banks.

"Banks with agriculture-heavy portfolios, for example, will need to investigate exposure to credit risks as the industry adapts to market changes. Insurers, on the other hand, may concentrate more on environmental climate risks from weather and natural disasters."

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

1 Comments

So, mortgage lending has risen over the 2 years rose by some 8%, while business and agricutural lending fell. Thus, risk concentration increases while house prices continue their dizzying rise and inflationary pressures seem likely to force interest rates higher sooner rather than later.

Meanwhile, financial stability is part of the RB's mandate, so what happens now when an irresistible force(rising mortgage rates) meets an immovable object(financial stability)?

Please send your answers to Mr. Orr.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.