Kiwibank's annual profit rose to a record high as income surged and the bank grew lending faster than system, or market-wide, growth.

Kiwibank says June year net profit after tax rose $5 million, or 4%, to $131 million from $126 million in the year to June 2021. The bank's previous record annual profit was $127 million in 2015.

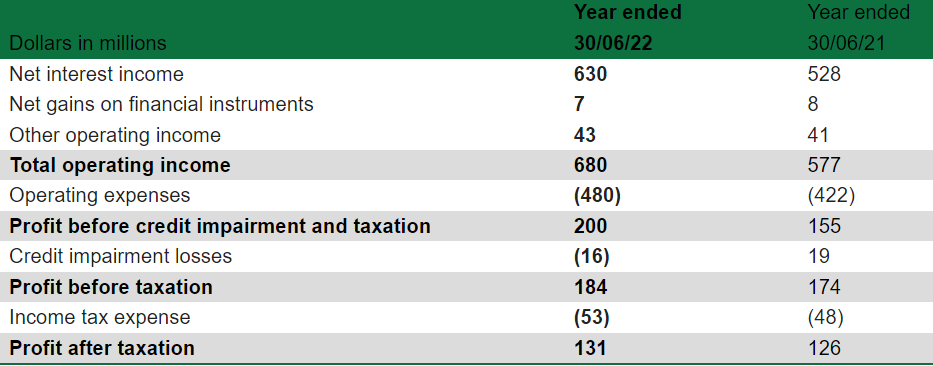

Profit rose as Kiwibank's total operating income jumped $103 million, or 18%, to $680 million. This was driven by a $102 million, or 19%, rise in net interest income to $630 million.

Net interest income reflects the difference between the revenue generated from a bank's interest-bearing assets such as loans, and the expenses associated with paying its interest-bearing liabilities such as deposits.

Kiwibank's operating expenses rose $58 million, or 14%, to $480 million. Annual credit impairment losses came in at $16 million versus a write-back of $19 million the previous year.

CEO Steve Jurkovich says Kiwibank grew home lending at the equivalent of 1.2 times system, or market wide growth, and grew business lending at three times system growth.

"Home lending growth of $1.8 billion [ to $23.152 billion] was driven by a strong first half of the year which slowed in the second half due to the consequences of changes to consumer lending laws (Credit Contracts and Consumer Finance Act), loan-to-value ratio (LVR) restrictions, a cooling housing market, and rising interest rates," Jurkovich says.

“Potential buyers are being a lot more circumspect – whether that’s first home buyers holding off, existing owners looking to upsize, or property investors taking a wait and see approach."

“History shows that different cycles occur, and the market will recover. At the same time, we continue to make great progress supporting our customers to achieve their home ownership goals," says Jurkovich.

Kiwibank's business banking grew $0.7 billion to almost $3.8 billion. Total gross lending rose $2.5 billion, or 10%, to $27.8 billion. Deposits from customers increased $1.8 billion, or 8%, to $24.216 billion.

'The models have just got no impairments to respond to'

Jurkovich told interest.co.nz that Kiwibank hasn't really seen an increase in borrower stress despite the sharp rise in mortgage rates over the past year, and highest inflation in 32-years pushing up the price of things such as food and petrol.

"The models have just got no impairments to respond to. We've seen credit card outstandings get paid down, we're seeing people being able to maintain their payments. I do think at the moment they are flexing on the areas that that they can. I know in our own experience I'm sure there are team members who are choosing not to drive into work, not to pay for parking, not to buy lunch in the city because those are some of the costs they can keep a handle on and it might give back $150 a week or something like that," Jurkovich says.

"So we are seeing people make different choices, but no, no stress at the moment. We did a desktop review of people that we have financed into homes in the last 18 months just to see if there was truth to this negative equity conversation. Out of all those thousands and thousands of loans we could find 70 that might possibly be in that situation."

Jurkovich says, however, that Kiwibank's serviceability test rate, the interest rate it uses to stress test mortgage applicants' ability to service their loans, will be reviewed next week. It's currently at 7.25%, and may be increased, potentially to 7.45%.

Kiwibank is owned by NZ Post, the NZ Superannuation Fund and Accident Compensation Corporation through Kiwi Group Holdings, which has recently sold sister businesses Kiwi Insurance and Kiwi Wealth. Kiwibank paid annual dividends of $17 million, up from $6 million in its June 2021 year, and in line with what it paid in the June 2020 year.

The bank's common equity tier one capital ratio, as a percentage of risk weighted exposures, was 10.5% at June 30 down from 10.9% a year earlier. The current Reserve Bank mandated minimum is 7%.

Loans at least 90 days past due rose $1 million to $17 million in the June year, with impaired loans also up $1 million, to $2 million. Kiwibank's credit impairment provisions increased $13 million to $67 million, but Jurkovich says in terms of asset quality, all that was discussed with auditors PwC was economic overlays and management overlays.

Income statement for the year ended 30 June 2022

39 Comments

Bank with a local bank if you can.

Yes, it makes sense to keep profits within NZ. Can people who bank with the foreign owned banks explain themselves..

100% agree with you in regards to keeping it local. But the government bank with Aussie owned banks. Go figure.

Kiwibank doesn't offer the level of services required for the government to bank with them. Although, that said, given that it now exists, and appears to be profitable (who ever thought that would happen!) then a bit of capital injection to get it up to scratch might actually be money well spent.

Ha! Even our money is printed in Canada (and before this is was printed in Australia).

We used to print it at a mint in whangarei.

Remember this next time you buy a car, fuel, computer, iphone or even a T shirt

We don't make any of those anymore. It's just as important to get the full life out of all of those things so I really admire those people that can repair items instead of sending them to landfill.

Yes, way too many items are made to be unrepairable. I'm looking at you Apple, Ariston and F&P lately. Repairs either not possible or parts so expensive it is not worth it.

The worst was the Ariston front loader washing machine. Needed a new water seal and bearing. However they laser seal the drum halves together so non repairable. New drum over $900.00 +GST. Bearing and seal $50.00. Never again!

I borrow from whichever bank offers the lowest rate and the best cashback.

I queried this with KB - they have conveyancers so the legal costs of switching banks are free. I asked TSB if they did the same - they said that was the point of the cashback. I've stopped looking at cashbacks now, unless they have free legal conveyancing AND cash of course. Do you know of any banks that do both?

No, but when I was looking to switch banks last time KB offered legal costs of conveyance and Westpac offered $10k. Legal Costs were $3k so $7k profit with Westpac. The offered rates from KB and Westpac were the same. No brainer for me.

Sure. In 2014 I looked at moving my business from ANZ. The GFC had taken its toll on my finances but I was recovering at that point, although I didn't have much to offer as a customer, just a mortgage and minimal savings.

TSB treated me as if I should be honoured that they would allow me to bank with them. They decided I didn't make the grade, and the person serving me made me feel worthless. It was humiliating, I was shaking as I left.

Westpac were happy to help, and they were 20 minutes from winning my business after I'd given ANZ an ultimatum on the interest rate they were offering, and ANZ caved. BNZ were also willing to take me on but weren't so competitive on rates.

I know many people in IT who work/worked for Kiwibank. Their impression of their systems has dissuaded me from exploring that option further. Maybe one day.

By 2019 my financial position was significantly improved. I was mortgage-free and "asset-rich" with a good income, but had big plans that required significant lending. ASB welcomed me with open arms, offering a very generous on-boarding cash gift, as well as a lending rate that beat every other bank. They have annoyed me a bit since then, and once my 5 year rate is up in 2026 I will shop around again. TSB may feature, but they're going to have to grovel. They showed little interest again in 2019.

I currently maintain savings accounts at ANZ, ASB, BNZ, TSB and Westpac, to spread risk in the event of a bank default. TSB's internet banking is the worst, although Westpac isn't much better.

Yeah I'm bitter.

I think that your Banking experiences would be pretty general thru out NZ

I used to bank with a the co-op, they were great. But when i wanted to release equity for a reno, they wanted a complex staged house build mortgage with all sort of requirements on the building contract, insepections etc. The Aussie banks were happy to just give me the cash, now i'm stuck there on 2.99% for 5 years.

I hear this a lot… but I get no benefit from kiwi bank profit. It’s not like it gets distributed to us. Now, with ASX listed banks at least I can buy shares and keep some of that profit in nz

I get no benefit from kiwi bank profit.

You don't think you'll ever pay an ACC premium or make a claim? You don't plan to collect superannuation in NZ?

True, but That’s what my ACC levies and taxes are for. Show me whether the return in capital surpasses other investments the super fund invest into and I will decide whether it’s worth it.

the return via dividends on investing in other banks is more immediate and tangible

Profits taken out of the country by a foreign owner reduces the value of the NZD. So you pay more for everything you buy.

While there is a cost of living crisis... the funnel of money from the lower class to the top continues

One of the issues with Kiwibank is that it is home loan focused.

So another banking operation - owned by the Crown - that supports the housing ponzi instead of NZ business further muddying Govt. actions and messaging

Trebles all round!!!

This is perverse. In times where most people struggle to paying their bills, there will always be someone making huge profits. In this case again as in previous cases: the banks. If they lose money, we (the tax payers) bail them out. So now Kiwibank have announced huge profits and raise floating interest rates at the same time, what should one say?

People get hung up on the dollar profit figure … but isn’t the more important measure how that relates to the capital invested? Ie is it excessive based on the investment?

otherwise it’s like saying returns on an investment should be capped in dollar terms .. whether someone invests 100, 1000, 100000 or 1000000000 …. But surely the amount invested matters?

One should say, why am I getting hung up about a $131 million profit from an entity owned by Government entities (i.e. owned by us, just moving money from one pocket to another), and not focusing on the ~$5,000 million profit made by the big 4 Aussie banks, largely owned by Australian shareholders?

KB's profit is a rounding error in our banking system.

By the people. For the people.

We need more publicly owned banks.

Every single council should found a small bank which offers mortgages to people within the district. If you take your mortgage with the council owned bank, you don't have to pay rates on that property while mortgaged since the interest on the property will easily exceed the yield on rates. It would lower people's costs, increase the funding of the councils and cut the australian banks out. Rates would only be paid by freeholders or people not using that publicly owned bank. Similar to the Savings and Loan banks circa 1933 till the savings and loans crisis.

Sure, we need council dipping their fingers in another pie… because as we know they’re excellent at efficient use of capital.

where does the capital for their lending come from in your scenario?

The RBNZ. Why give free money to privately owned banks and not public institutions?

Banks tend to benefit from rising interest rates, their margins grow fat.

Savers earnt almost no money on their savings in the last few years, yet banks make massive record profits.

From a reliable source ASBs profit was only 1% net profit so considering the business is worth approx 120b

its certainly not excessive.

I can't imagine what a banks net worth is made up of. Buildings sure, but what else. They are such strange businesses, holding everyone's cash and mortgages.

The only thing on their asset register is probably loans. Everything else (buildings, vehicles, IT hardware) etc are probably all leased.

I thought most Banks leased their Premises now so where is the Bricks and mortar part of their assets

You can see their profit on the RBNZ dashboard. But that's 1.2% net profit against assets on 13.8% of their own capital.

1.2% divided by 0.138 = 8.69% return on capital. Still 8.69% is a fairly low profit margin for a large institution in my opinion.

But what does it produce that is productive from that 1%. It is almost like a middleman clipping the ticket, when people could just go to the source.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.