Westpac New Zealand's annual profit has pushed past $1 billion for the first time, helped by a one-off $126 million gain from the sale of life insurer Westpac Life.

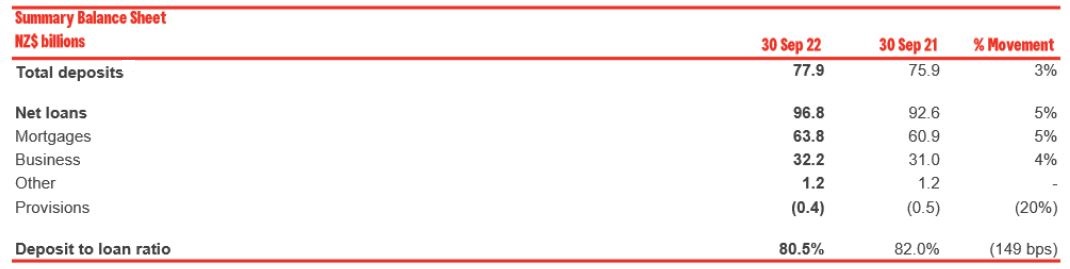

Westpac NZ's September year net profit after tax rose $116 million, or 12%, to $1.047 billion from $931 million in the September 2021 year.

Net operating income increased 10% to $2.709 billion, with net interest income up 8% to $2.278 billion and non-interest income rising 25% to $431 million.

Operating expenses rose 2% to $1.158 billion.

Westpac NZ recorded an impairment benefit, or write-back, of $27 million, down from write-backs of $84 million the previous year. Westpac NZ says its net interest margin was unchanged year-on-year at 2%.

'Not seeing any warning signs'

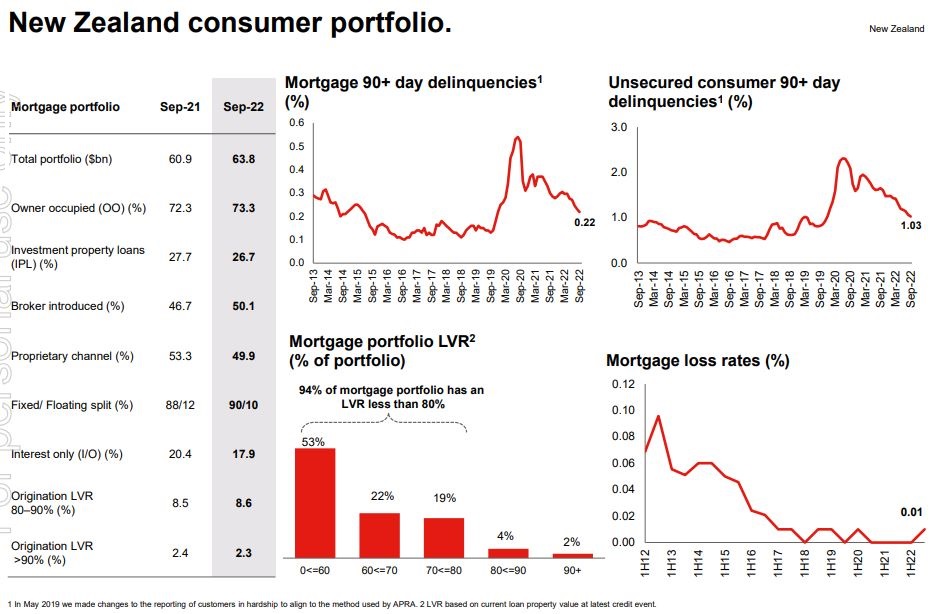

Home lending grew 5%, business lending rose 4% and deposits increased 3%, the bank says. CEO Catherine McGrath says Westpac NZ grew home and business lending market share in the second-half if its financial year, taking "strong momentum" into the September 2023 financial year.

"While the rise in interest rates has coincided with a retreat in house prices, recent home buyers who have bought for the long term shouldn't be worried about the current value of their property," McGrath says in Westpac NZ's press release.

"Inflation remains a concern, however our economists think that the rate of increase has peaked, and the accumulated effect of higher interest rates will gradually bring it down over the next couple of years," adds McGrath.

McGrath told interest.co.nz Westpac NZ hasn't yet seen any particular signs of borrower stress emerging. The bank's mortgage serviceability test for new borrowers is adding 2.5% to its interest rates at the time a loan is taken out. So far McGrath says "very few" borrowers are at a rate above that.

"For most customers fixing [loans] in 2021 that test rate would've been higher in terms of what they're experiencing in rollover at the moment," says McGrath. "We are not seeing any warning signs in the [mortgage] book so far."

Parent Westpac Banking Corporation posted a 1% drop in annual cash earnings to A$5.276 billion. Its net interest margin fell 17 basis points to 1.87%, its common equity tier one capital ratio fell 130 basis points to 11.3%, and its annual dividends rose 6% to A$1.25 per share, equivalent to 83% of cash earnings. Return on equity fell 46 basis points to 9.8%.

Westpac NZ's press release is here.

The Westpac Group press release is here.

72 Comments

It's not the value of the property that is the issue, it's the value of the mortgage.

If you don't need to sell the value is irrelevant, if you can't pay the mortgage, the value becomes very important very quickly.

Yup, the sad reality is that the debt itself gains value when the asset is declining.

The debt is a bank asset and will be written down if the collateral value falls below a certain point, determined by the RBNZ, and depositors will endure an equal haircut.

If enough households can afford the mortgage but only after making deep cuts in their discretionary spending, the "overvalued" property market becomes relevant to the entire economy.

Household consumption contributed to 2/3rds of NZ's GDP pre-pandemic. How deep a cut in household budgets is required to send economic activity into a downward spiral?

*provided you bought a house suitable for the long term, and taken on huge amounts of debt from us to do it.

**provided you don't lose your job in the inevitable downturn RBNZ is insisting we need to head off inflation.

***provided you can keep up with inflation in all your other living costs.

****provided you can service a mortgage at above the stress test rates you were tested against.

*****provided you don't need to drop down to one income for health/pregnancy/other reasons.

Am I missing anything here?

******provided you can afford the increased council rates and insurance premiums that will likely double then triple

*******provided you can afford the property maintenance and repairs

Heard first hand from an asset rich Boomer who spoke of their struggle under the weight of a 4% (fixed) State Advances loan. "We struggled too"

Pure ignorance.

you are aptly named

******** provided you or your partner don’t need to sell up to shift town for job or family reasons.

For a while there FOMO was going gangbusters. Who out there was thinking long term when all that was in focus was those delicious short term gains that would never disappear. Once got, considered banked! Now that narrative has sprung a nasty leak.

Just been reading a little around Nassim Talebs turkey problem. That things are so good for the turkey, and everyday this is reinforced by the good very results ( the farmers constant care and attention). So much so that it is not possible for the turkey to predict that Thanksgiving/Christmas is happening in just a few days.

The market gives such positive reinforcement that near the top everyone has such inflated confidence and gets involved, even those that understand the markets little. Have been around a number of times to see this. 1987 stock market were family members told my young sister over Christmas dinner to put all her savings into Brierly shares as “ you can’t loose” …… she did, and she did - loose that is, all of it. Property boom in the early mid 2000s were a large number ordinary joe blogs, who didn’t understand the property market or the subdivision process, got involved in medium scale subdivisions in the Bay of Plenty saying “you can’t loose” ….. they did and they took subcontractors with them …. I think a bank or two got caught badly in some of it too.

Last year again, they said it “you can’t loose”, this time it was RE agents and the folks jampacking the open homes, also in the workplace and other meeting venues, my son said that “appreciating property portfolios” along with “ you can’t loose” were regular morning coffee discussions with his young professional workmates. Again people with little knowledge, I was constantly horrified at people taking price ( to pay) advice from the RE agent selling the property.

“You can’t loose” is a warning cry and we heard it enough last year to delay buying/building a home. Let’s see how long we will have to wait to reconsider purchasing.

Lose not loose, for future reference.

Lose the hounds!

Oops on my iPhone on a train. I will do better next time :)

Turkeys, Black Swans and Cooked goose. Some people are going to be well and truly plucked.

If you listen to the DGM (above and below) you’ll never own a home…..

But you’ll be exposed, forever, to rising rents and egregious landlords - including through your retirement years.

Property ownership remains the best bet for the vast majority of progressive Kiwis.

TTP

"If you listen to the DGM (above and below) you’ll never own a home…..

But you’ll be exposed, forever, to rising rents and egregious landlords - including through your retirement years.

Property ownership remains the best bet for the vast majority of progressive Kiwis.

TTP"

From Tim Morduant, the head of property brokers, who also claims to be a 'poor renter' so he can spruik house prices on an online forum, even though he's been previously found guilty of deceptive behaviours by the Commerce Commission. Does the tiger change its stripes - it appears not.

Tim's predictions are all over the place. Look at this one from Feb 2017!: by tothepoint - d… | 24th Feb 17, 10:00am - "A fall of a mere 12% over the next 3-4 years would be a soft-landing, given the spectacular gains of the recent past. So, hardly a forecast to get too uptight about. But the fall could be more pronounced than that - shouldn't rule that out. Auckland property prices are in decline now. Unless there's a compelling personal reason, why would one buy a house in Auckland at this juncture? Better to "buy low and sell high" than the other way around - every Joe & Jill Bloggs knows that. And that's exactly the reason buyer confidence is fragile - as indicated by the falling numbers attending open homes"

Oh the déjà vu Tim must be feeling. Now we all know what advice has Tim (two face) been dishing out to FHB's this time around....

Remember, most of the people who come here whinging and moaning each day don’t own a home……

They missed the boat in their lives and ended up a bunch of sore losers - envious of those who are independent and have prospered.

They come here, en masse, to vent their disaffection. You’re best to ignore them and all their negativity. Don’t let yourself become contaminated.

TTP

Tim, you've let yourself become contaminated🤡

RP (AKA-Crash Crusader)

The Napier Property Brokers Ahuriri office has been shut down altogether. This is NOT a demotion or relocation to a smaller office like the Havelock North situation . Very sad indeed.

And yet Kevin Wagg from Property Brokers has been telling the public these exact words regarding property prices "We Bottomed Out In May And Have Been Increasing Month On Month".

Kevin Wagg had a sustained radio campaign promoting price increases.

Property Brokers have a new radio advertisement recruiting agents to join their winning team.

The Napier Property Brokers Branch near clive square has recently been relocated to an abandoned old jetts gym. This is a big step down for the agents I have been told.

So Havelock North Branch was the biggest but now is the smallest, some thought it was gone altogether.

Napier Ahuriri Branch actually is gone altogether.

Napier Branch at 19 Clive Square West has been closed down and relocated to 2 Thackeray Street Napier.

Is it possible TTP is misleading us ?

https://gilbutton.propertybrokers.co.nz/property/NC107026/unit-205-1-lever-street-ahuriri/

https://www.propertybrokers.co.nz/listing/nc76733

In normal conditions I would agree. However, things are far from normal.

The last ten years a central bank driven price stupidity is far from normal. Price has ballooned into ridiculous levels, boosted by the lowest of rates, capital gain seeking speculators, debt stacked rent seeking parasites, and agency transaction greed. Is now really the best time to go long on debt, last years buyers now being marketed as now in negative equity would suggest a bit more patience.

Look at the facts. Make your own mind up. Good luck.

Taleb's Turkey, Personified.

TTP.

So is she really saying that house prices falling at a time when interest rates are ramping up is just a coincidence... ?

In a debate in 2011, during the height of the eurozone crisis, Juncker responded to a conference-goer's suggestion to increase the openness of the strategy discussions in the eurogroup, by stating: "When it becomes serious you have to lie".

As banks in NZ are only required to put $1 in every $62 of mortgage lending, "What could possibly go wrong?"

As for this rubbish that ONLY 2% of lenders are in Negitive equity... well yes but that 2% is totally concentrated in the 5-10% who took out low equity loans near the top.... Banks will never have an issue recovering funds from a 20-50% equity situation especially borrowed 2010-2015, but if we see any serious % of Negitive equity borrowers going to the wall, there is going to be Balance sheet carnage at the big four. Think about it, if they loose 100k on a deal, it wipes out their capital for that loan and about another 6.2mil of lending....... if across all the banks say 20 bil is in low equity at risk lending... If say 50% of these loans failed think how much recapitalisation would be required in the middle of a recession It could..

"Become Serious"

Why is he tryting to justify their profit.....is it guilt

No, he is saying don't worry about the value of your house, just keep paying the mortgage, so we can make higher profits next year.

Sort of seems like New Zealand needs non-recourse mortgages.

Catherine McGrath = she

Safer to go with "they".

Thats Harsh Catherine is a breath of fresh air IMHO

"They" is a commonly used pronoun to avoid she/he even in times gone by. For example, "why did they do that?"

I remember occasionally my mother saying "She is the cat's mother."

Are these values sustainable if as a family we want to have a house, a decent life and also support our kids to have good education and not just be dependent on the dole support system of the government?

We have made a system where cash has no value and only way to make more is to keep buying more and more. How much more? We live in a world of finite resources. Did we forget that?

The system of more and more profits every quarter can't go for ever. It results in clashes and that's what we are witnessing world wide right now.

We are a small nation and we can bring a big change if there is a policy which will really be for everyone. But but but system is so corrupt and biased that nothing will change as even to win an election we need money and donations only come from someone who has a selfish reason to support that politician.

We don't teach contentment in our education but we teach greed in the name of growth.

We are past the point where new lending is required to make interest payments on previous lend would wide, We are out of cheap energy to keep the ponzi going, as powerdownkiwi suggests, now we have to change, but the traditional central bankers and economists have missed the crucial linkage between energy cost and economic expansion. The US used to understand this, hence the wars over gas and oil to feed the machine, Russia understands it, China has no natural energy supplies to support themselves, they will need them eventually to displace the US

When all the folk in charge have investment property portfolios it's hard for them to think beyond the status quo.

Banks always win.

"While the rise in interest rates has coincided with a retreat in house prices, recent home buyers who have bought for the long term shouldn't be worried about the current value of their property," McGrath says.

Matthews says we should want banks to be turning a profit, because otherwise they're losing money.

"If they're losing money, it's the customers who potentially are at risk in terms of losing the funds that they've got on deposit."

"Because it's been so long since banks haven't done well, we've kind of forgotten that that can happen." Link

Lose-lose for under rewarded, unsecured depositors.

"unsecured depositors."

If only more people understood these two words.

Westpac are one of the big four vampire squids wrapped around the face of kiwi humanity.

They are more than happy to feed "for the long term".

recent home buyers who have bought for the long term shouldn't be worried about the current value of their property

That's not going to go down well with the Interest commenters, most want to see blood on the street

Well, he's right.

If you only ever aspired to live in that formerly million dollar two bedroom slum-box for the next thirty years, then the valuation is of little concern.

The cost of servicing the money being rented from the bank however...

Someone is itching to spill blood on this forum....🩸🩸🩸

If we're experiencing a crash then its because of the unrelenting greed of the short sighted amongst us. Who should be held to account here? Who should shoulder the loss?

(Rhetorical question)

I will give an answer to your rhetorical question, YES, I think it’s unrelenting greed. And it was around in ‘87 and the early 2000s. It’s holding on too with greedy vendors trying to achieve last years hugely inflated prices despite this years borrowing environment.

Bummer, someone ruined it for me, I had a perfect "0" thumbs up !

Gee I wonder who that could be ?

There is something intensely dishonest about this Baghdad Bob approach to managing the emerging housing price pain for thousands of people. The banks need to manage the fall to avoid negative equity and bankruptcy for thousands of homeowners, with dropping standards of living for thousands of people despite full employment and a "strong" economy.

The refusal to acknowledge what has happened is going to result in an enormous backlash against the banks, far worse than after the GFC given the banks are posting billions in profit at the same time as the vast majority of people are faced with austerity. The banks are laying the seeds of their own destruction.

Here's a little song I wrote

You might want to sing it note for note

Don't worry, be happy

In every life we have some trouble

But don't worry when mortgage payments double

Don't worry, be happy

Don't worry, be happy

Your house used to increase by more than you earn

but now you must remember you're 'in it for the long term'

Don't worry, be happy

Don't worry, be happy

But negative equity might be there for 6% of Westpac borrowers:

https://www.stuff.co.nz/business/property/130275018/how-much-will-your-…

So this is the first official statement indicating that flippers are now an endangered species!

Nothing like telling people not to worry to spark panic.

Nikki Conners says property will double in 10 years ... always has , always ... ooooh , hang on ... a knock at the door ... the IRD & a team of liquidators !!!!

... Ms Conners will be delayed ... 10 years , maybe ...

Does this mean flippers finally got pwned?

Assurances from the bank about the future value of housing. That is more than the government is willing or able to do. - Shows who is really running the country.

Confirms that for young FHB that they have no hope of ever owning a home here and their only hope is to leave NZ. No point hanging round here getting paid peanuts, wishing and hoping, enriching landlords and getting bitter and twisted.

Voting for National will only make matters a whole lot worse. What is one of John Keys main jobs now?

You will have to compete with a flood of immigrants for jobs, housing and any public service or infrastructure.

Shows who is really running the country.

Those blessed with an abundance of entitlement mentality and a deficit of morals.

Give some possible dire circumstances i.e. declining property values, can an individual re-negotiate the loan outstanding? i.e. if they had borrowed $500k initially, but now with the decrease in value, agree to paying say $400k? Would lawyers be able to assist in this?

Mortgage = death pledge.

So not sure if your comment is sarcasm or innocence - but the bank would laugh you out the front door or off the call centre phone line.

You've made an agreement with them to pay them $500K over the next 30 years - and if you decide not to do that, you've defaulted on your side of the pledge. Good luck getting funding from any bank in the future if you want this type of credit history! (i.e. i just walk away from an agreed contract when I feel like it).

I remember people asking this question as well in the US back in 2008 and 2009 when house prices went into negative equity. Sure there was jingle mail - but it doesn't do your credit history any favours and good luck finding a bank who may want to lend to you in the future if you ever wanted to buy a house again.

Interesting though that people are thinking this way in NZ now. Might be another sign that the tide is turning.

I've seen it happen. People who otherwise had no assets than the place they were renting out seeing it rendered worthless overnight by leasehold increases on top of weather-tightness issues. It had to be a pretty hopeless situation where the costs of selling would have been more than what would have been recovered.

The offer was generally: "You can spend a bunch of time to make me bankrupt but the outcome is still going to be the same, or you can accept this full and final settlement and we can both walk away with something" but that's probably much easier to pull when the banks are raking it in from all directions.

From memory this debt remission was specifically taxable as a form of income as well. But it's been a while since I last saw it, and I'm not sure what sort of consequences would follow you around even if you managed to pull it off.

You are joking Bob???

You sign up for a Debt - its all yours and you owe every cent back + the higher and higher prevailing interest rates.

500K will be a total payback of 800 to 1.5m.......as mortgage rates will vary wildiy, at much higher levels in the coming years.

Pay more if you need mortgage holidays, Interest only and/or delay any payments.

Yip imagine holding more than $500K of debt now with the possibility of 10% interest rates in the future (which would have appeared impossible over the last 5 years (or more)). The amount of interest paid on that loan is going to be massive.

All the while as prices are reset by the math of yield. High yield....low value.

Wow. Even if your house becomes worth just $10 the bank would still want to to remain enslaved paying the $500,000 back, and will legally chase you to get it. They can even request that you put in more equity, or sell and then pay of the shortfall. Remember, the bank actually owns the house until you discharge the mortgage. You are just the risk proxy.

That's kind of a problem, the Reserve Bank of New Zealand needs people to worry and manage their spending back to curtail inflation. If people just keep spending as they have been the Reserve Bank won't have the desired impact on demand.

Propeller Properties in liquidation.

https://www.stuff.co.nz/business/130398591/two-of-queen-of-propertys-bu…

Speaks volumes!

If its only a little bit of tax....pay it. Hopefully that's the end of her adds as well. That the scale of her adds, including TV, went into overdrive as couple of months back was also telling. The sucker pipeline clearly had dried up.

Essentially another Doug Somers-Edgar type, but wearing that large cross to portray Christian honesty & values.

Great news let the ponzi crash and burn.

I would hear Property Brokers Advertisements immediately after she finished speaking on the radio. Tim Mordaunt would be all over her spruiking.

Strange how they have both gone extra hard out with talking the market up before her situation.

And as we know, the Property Brokers Havelock North Branch has been reduced to a shoe box.

Napier Ahuriri Property Brokers Branch is now closed down altogether.

It's such a DGM name 'Property Brokers' - bound to fail, like I have said before Property Fixers would better much more apt ...

It says a lot about how Property Brokers sees the state of the property market for the foreseeable future. They seem to be heading for the hills. Much like Tim's posts here on interest.co, the adverts are nothing more than self gratifying.

Not sure I buy the claim she had no knowledge that her company stopped paying the tax arrangement with the IRD. Would be negligent leadership of the company if that were the case.

Access to capital and equity to pay the debt off - but apparently not cash.

What kind of capital and equity - property, perhaps? Kind of hard to leverage that if a) no one wants to buy it, and b) the sale won't cover the finance!

I see homes.co.nz still has a vastly over optimistic price for my house about 12 - 15% over what I would believe it would sell for. One roof and my banks valuation seem to be about right . Why is that? With homes.co.nz I see that agents can alter the estimate of properties they are marketing, maybe placing the estimates too high? So would this then affect the estimates of the surrounding properties and push them up to unrealistic levels in the homes.co.nz algorithm?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.