By David Cunningham*

I’m sure I don’t need to remind anyone that our country is deep in a cost-of-living crisis.

Those with mortgages are struggling. Collectively we’re all having to tighten our belts.

And in the lead up to election day, our politicians are scrambling to come up with policies to support everyday Kiwis who are being stretched to their absolute financial limit.

And yet amidst all of this, New Zealand banks are thriving – bringing in record profits.

Banks margins have grown massively since the cost-of-living crisis began, by just over 15%. And every other week it seems, they’re pushing home loan interest rates still higher and higher.

People have rightly questioned how the banks can justify these ongoing increases, when wholesale interest rates have remained stable since the Official Cash Rate was raised to 5.50% on 24 May.

It’s why there’s a market study into competition in personal banking underway.

Taking a step back for a moment – let’s look at the facts...

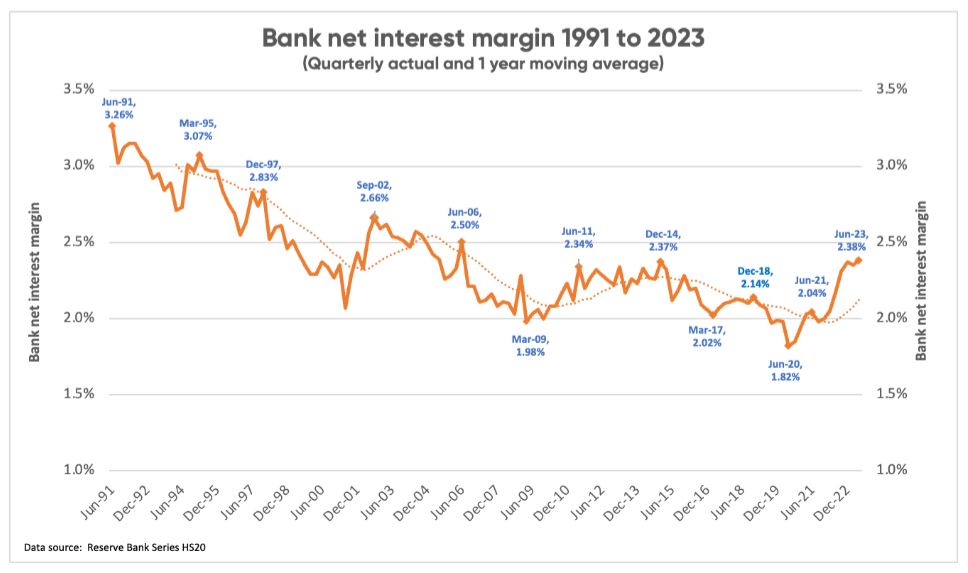

Eighty per cent of New Zealand banks’ revenue is generated via what’s known as their interest margin.

That’s the difference between the interest they pay households and businesses on their savings, (or on what they borrow from the wholesale markets, including the Reserve Bank); and the interest they charge when they lend money out to homeowners and businesses.

The below graph tracks the banks’ interest margin over the last 32 years:

You’ll note that after trending downwards for decades, over the last two years – just as New Zealand’s cost-of-living crisis has emerged – that interest margin has grown rapidly.

Collectively, the banks have managed to expand their interest margin from 2.04% to 2.38%, which has equated to a roughly 17% lift in their overall profit margin on their lending. In just two years!

And on the $660 billion of interest-earning loans the banks collectively manage, it’s a whopping $2.24 billion of extra revenue they’re bringing in every year.

Or $43 million every week

$6 million every day

$0.25 million every hour

$4,269 every minute

Or $71 each and every second

So, what’s the driver behind what the banks are doing with home loan rates?

It’s actually not a what, but a who.

His name is Matt Comyn – and he’s the Chief Executive of the Commonwealth Bank of Australia, which owns ASB here in New Zealand.

In mid-August, he came out bemoaning the “unsustainable” returns the banks are having to put up with on loans within New Zealand’s housing market. Here’s the exact quote:

"The mortgage market in New Zealand is even more challenged [than Australia], where pricing conduct is difficult to reconcile. We've pulled back on volume growth in New Zealand given the unsustainable returns.”

Really? Cast your mind back to that graph we looked at earlier. The interest margins the banks are earning hardly look unsustainable to me.

Prior to joining Squirrel, I spent 30 years in banking, including four as Chief Executive of The Co-operative Bank, so I know a thing or two about how the banking system works.

When the banks set interest rates for deposits and loans, they’re not thinking about those rates in isolation – they’re thinking about what it means for their interest margin overall. That’s just Banking 101.

What happening here is a practice called price signalling

It’s extremely common in oligopolies, like the banking sector, where there are a few large players and extremely high barriers to entry.

Comyn’s comments were targeted at the major bank CEOs in Australia, and therefore indirectly at the four big Aussie-owned banks here in New Zealand.

The signal he was sending? “Our prices need to be higher”.

Then it just takes one competitor to lead the charge – in this case, it was ASB – so everyone else can follow suit.

And that’s exactly what’s happened in the weeks since.

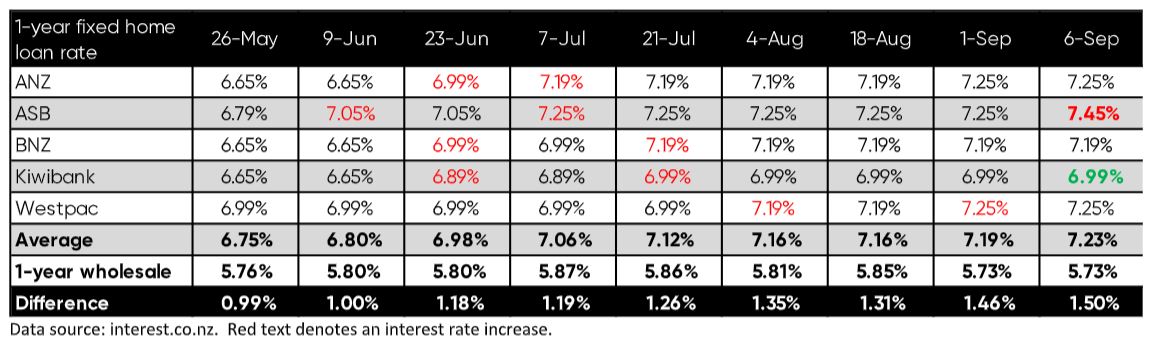

Here’s how it’s played out with the popular one-year fixed home loan interest rate:

Using the wholesale one-year rate as the benchmark, the margin has lifted from about 1.0% after the last Official Cash Rate change on 24 May, to 1.5% now, on average across the big banks.

And we can also calculate the bank’s individual margins… At one end of the spectrum, we’ve got ASB earning 1.72%, and at the other we’ve got Kiwibank earning 1.26%.

I’d welcome a move by our Australian-owned banks to take a leaf out of Kiwibank’s book – and give New Zealanders a bit of a break.

Our banks have a social responsibility to do what’s right by New Zealanders – and right now, everyday homeowners are suffering, to bank shareholders’ benefit. At Squirrel, we see it day in and day out.

The average mortgage interest rate Kiwis are paying on our home loans has risen from 2.8% in 2021, to 5.3% now – on a $500,000 mortgage, that means $12,500 more in interest payments each year.

And with mortgage rates as they are now, that average still has further to climb to over 7%, and that would mean a further $8,500 in interest payments each year.

All without factoring in any further moves by the banks to expand their interest margin.

My challenge to our four big Aussie-owned banks is this: put your home loan rates back down.

A rate of 6.99% for the one-year fixed home loan term would be a good start. It’s time for our big banks to do right by Kiwis.

*David Cunningham is CEO of Squirrel, a mortgage broker that also offers peer-to-peer lending and savings and investment products and services.

98 Comments

Where were you when TD were too low?

People don't loose their home when Term Deposits are low.... this is the exact kind of information that needs be published so people can understand who to direct their anger at and maybe get some change.

Wrong. For retirees once the saving are gone because you are living on your capital instead of interest then the house has to go.

I can't see the point in very low interest rates because you will all borrow to the max to compete with each other. Fox those who increased their mortgage to pay for a flash car or holiday then you are getting what you deserve.

Why do retirees have a right to live on interest and not have to spend some of their capital during times of low return to sustain their lifestyles?

Check the 4% rule, they should not be aiming to make it last forever and impoverishing themselves when returns are low. The goal should be to make it last over the time required...

W-w-w-w-welllll there B-b-b-b-billy. They've worked and paid taxes all their lives and built this great society we have today all with love and charity. They shouldn't have to spend a dime of their savings, hell it's an outrage they're treated like second class citizens by only allowing Gold Card free public transport outside of peak hours. Disgraceful...

And the universal non-means tested pension should at least be doubled, along with the winter energy payment. And why aren't council rates rebates higher?

Hibernating

Are you defending the banks by attacking the messenger?

Or just missing the point entirely?

If the banks dropped their margin to zero is it going to make that much difference. You all want 2% loans. Those days are gone.

Greed knows no bounds. Why would banks cater to the insatiable desires of those driven by avarice among the Kiwi population?

The surge in real estate prices to unjustifiable heights can be attributed to individuals relentlessly speculating on future profits, often outbidding their fellow Kiwis.

It's no surprise that banks have no remorse for these individuals today.

Are you saying my bank is charging me outrages rates out of spite because it despises be for my greedy audacity of wanting my own home?

Nah, Im pretty sure the greed sits with the banks bro.

Agree. The banks dropped their long term test rates to 5.5%, before hurriedly raising them back up to 9% within the space of 12 months.

People claim personal responsibility...okay sure, let's remove the Consumer Guarantees Act. Personal responsibility suggests a cheap fridge might not last, so why should the retailer be on the hook? Does personal responsibility apply to a homeowner whose sparky uses the wrong gauge of wire and their house burns down? The homeowner should have known.

People should have known interest rates couldn't stay low forever it's claimed. Well the banks have demonstrated they didn't know.

Non-recourse mortgages might be a good addition too.

Along with liberalising zoning to allow more building, not handing out money to banks in hard times, and not subsidising demand while constricting supply.

Too sensible Rick.

100%

Good pick up on the oligopoly signalling antics. Why isn't the ComCom all over this?

Yes! "Release the mighty Com Com" <sounds of war drums>.

Your mean whistling in the dark.

I would be very surprised if they could muster a whistle lol ;).

I mentioned price fixing in a comment here the day the ASB guy said that. If his comment is illegal the ComCom should be all over it. The potential fine should be absolutely massive considering the amount it could have costed NZers. But I imagine it maxes out at 100k or something stupid.

As much as I loath the FIRE industries parasitic profits, bank margins as presented in this article make sense to me.

Lower interest rates will have lower absolute margins but higher volumes. Higher interest rates will see absolute margins improve but with lower volumes.

While it looks low, I could be wrong, but isn't that net interest margin before you extrapolate against their capital?

ANZ/BNZ/ASB have a 15% capital ratio.

2.38% NIM @ 15% capital = 16% return on capital.

windfall tax on banks please.

That will push rates up

I don't care. It sends an all-important message to the C-level officers and shareholders.

One could equally argue this just indicates the OCR is too low. Which the CPI indicates also.

But this guy sells mortgages (is squirrel a second-tier lender?), and his raw sales figures must be dropping like crazy atm, so he's getting desperate.

He's trying to find nuts amongst the hay..

Good luck..but rates will be higher for longer

Rates will be higher for longer, but how long is longer?

Banks are trading on the lowest volume of new mortgages since 2012. Margins have been dropping for the last 30 years. No doubt in my mind, the OCR is not high enough, and deposit rates are too low. Banks can see what's coming, the cost of money around the world is still increasing, and its the end of a 30 year debt cycle. Banks are simply pricing the risk of their loans in the current environment, where asset prices are far too high (both residential and commercial), but their commercial exposure is what will be what is worrying them.

Residential mortgage NIM is at a histroical low - totally contradicting the article.

"guest" needs to google why banks make more money in rising interest rate environment (cost of funds).

-SMG.

Rocket and feather pricing.

And they're amply assisted by the RBNZ that telegraphs what will happen months in advance.

Two things the government can do to unwind the cost of living crisis and improve the economy longterm.

- reduce the expected dividend the kiwibank SOE pays to zero. If private Australian banks want to compete in the NZ market they will have to reduce their interest margin.

- merge the NZX with the Australian stock exchange. Businesses will have a viable alternative to raising capital than asking banks. Australian banks will need to reduce their interest margins if they want to compete.

It's funny to see how people here quickly came to defend the banks with something like "banks are not evil and they are helping people to get their home" when the interest rates are low. Now when banks need to put up rates to cover the costs and risks, they start calling banks are greedy and are not doing the right thing. Interest rates won't stay low forever, banks here are doing business, they are not charity organizations. Understand this and deal with your investments accordingly. Here, houses are not just home for living purposely only anymore. It's one type of the investments that we are obsessed with.

The banks could have helped people get into their homes without cooking the market. Why did the test rates need to follow interest rates down? Surely all being equal the market would have carried along while everybody, including investors, were being tested at 8-9% interest rates instead of 5.5% and enjoyed a small period of 2.5% mortgage rates. This is what defines the banks as greedy, temporarily expanding their loan book size by pushing the envelope on their own stress test methods.

How many young people who bought off the plans in 2021 will be screwed because the bank effectively bait and switched their pre-approvals? Seeing an uptick on the FHB Facebook page of these. Deposit paid, bank revaluing at $150k less. Developer not budging.

That's why I kept saying that banks are not your friends, they are not there to help you, they are in for business. I said this when the rates were low, and I also say this now the rates are high. Understand this and you will make better investments decisions. Younger generations really need to learn some basics about how money and investments work instead of just blindly making decisions to follow property ponzi scheme. Making financial literacy compulsory in schools will be a good start.

Was money/investments taught in schools 40 - 50 years ago? Or were banks a little more prudent back then, when you had to wear a suit and tie to sit down with the bank manager before taking out a mortgage 1 - 2 x your annual income? Didn't stop young people back then taking out 2nd mortgages and vendor finance to make it all work, so blindly making decisions is not reserved to today's young.

Would the basics of how money and investments work prepare someone in their mid 20's for interest rates hikes in magnitudes never seen in this country?

Back then houses did not cost 15 x average income in many places young couples just can afford to buy at these pumped up price’s even with the 20% crash we are a long off affordability form scratch. My pick is prices will continue to crash.

I still like my idea (although you had it first as it turns out), which is that the test rate used when the loan is taken out also becomes a ceiling for the term of the loan.

Yes I am a big fan of that too. Although people suggest that it might result in banks applying a % risk adder to all their loans, reducing the amount people can borrow. That is a problem how exactly?

That is a problem how exactly?

Someone else better answer - I think less debt and lower house prices would be a plus!

First off as a property investor/ developer I deal with 2nd tier banks rather than retail banks but when 2nd tier floating rates are near if not better than retail banks and are easier to deal with that shows me retail banks are creaming it. So why not a interest rate for the person who just wants their own home and that's it nothing more and a higher rate for a person with 2 or more easy to clarify it and IF (big if) NACT do bring back the tax deductions that on interest that would lower it back down. Actually if the banks had a moral code (cough cough) they would have a interest rate for the home owner at percentage eqvilant to the tax deduction off what an investor pays. But hey we have to realize this is Aussie owned they love screwing NZers

So why not a interest rate for the person who just wants their own home and that's it nothing more and a higher rate for a person with 2 or more

That may have been the case in the early 90's - a higher rate for investment properties.

I'm not sure on the above, perhaps someone older could verify what I vaguely remember being told that as a student by a bank.

You'll also probably find in the early 90's things called "interest only" mortgages were classed as non-performing loans, and used only when a borrower was in genuine financial distress.

These days it's used by investors to keep the ponzi going.

We're a SME Auckland based business and just renegotiated our loan ( through our broker) at Westpac for a one year term at 6.99 %. Interesting that behind the scenes banks seem more willing to negotiate other than their advertised rates to keep clients.

I am not a banker, so I would suggest that there is a little bit of information missing here. But first of all this is a great article we need more of them. But for those like me who do not really understand the finer detail can a few questions be answered?

What makes up a bank's cost of capital (I think the answer is obvious, but there might be something I'm missing)?

Do bank's operate on a fractional basis today or lend out at 1:1 on capital?

- if yes can we know the ratio? That will speak volumes on just how much money they make on capital including depositors funds.

- If the minimum required interest rate on on-call deposit accounts was the OCR, how would that impact banks? (The OCR is supposedly the risk free interest rate, and clearly any bank is not risk free)

Banks don't lend out their capital or their reserves as these are held to cover any losses, they create new deposits when they lend. They have to hold capital at 10% of lending but there is no reserve level that they must hold. https://www.hks.harvard.edu/sites/default/files/centers/mrcbg/programs/…

Not what I was asking.

I do understand they do not lend out their capital/reserves. But this article is commenting on the CEO of the CBA complaining that the bank's margins are too low. I think we depositors are being ripped off by the banks, as is also suggested by this article. But what does the actual 1.72 - 1.26% returns really mean? Their profits suggest something entirely different, to the degree that the CEO actually looks like a con man when he spouts off like he has.

The banks are required to maintain a level of capital as a percentage of their total loan portfolio as a hedge against their risks. You indicate it is 10%. That means and let's just for a minute suggest that their total capital reserves are made of depositors funds, that their fractional ratio is 10:1. This suggests that for every dollar they hold they effectively have loaned out 10 at a current interest rate of say 5%, which results for the bank an effective return of 50% ignoring their costs. Depositors interest rates forms a part of their cost of capital but at 1 - 2% that is nothing at all for even an on-call account, considering the bank is getting 50%. Is this accurate or not?

Customer deposits are not their capital, capital is shareholder funds and retained profits. Every dollar that a banks lends creates a dollar of new deposits and which the bank must pay interest on or it will loose its reserves to the other banks through the interbank payment system.

Customer deposits do form a part of their capital. That is borne out by how the OBR works and the fact that legally depositors are seen as unsecured creditors.

"Every dollar that a banks lends creates a dollar of new deposits and which the bank must pay interest on" This is the crux of it. Who is the owner of those deposits? They lend to a borrower who pays interest on the loan, common sense suggests that the interest they pay is significantly more than the cost of capital. But as we know, banks are only required to hold 10% of their loan portfolio value as capital, so where does the funds they lend out come from? Past discussions have indicated they have 'created' (to all intents "printed") the money. So it really doesn't cost them at all, but they do charge interest for it from the borrower. When the loan is paid back, to all intents the money is cancelled. Or is there some form of invisible cost that is not apparent? Yes those funds loaned out create a deposit, but that deposit is in the borrowers name, and the borrower pays interest there. That is not a cost to the bank. As I indicated in my question, depositors are getting shafted.

If bank margins are so enormous, why isnt Squirrel doing mortgages? Surely as the CEO of a competitor you would be welcoming big bank price gouging because that opens up the entire market for you? Go out there and compete instead of whining about it.

A lot has changed in the new [old] world where there is no more free money. Every company now has to allocate what has become scarce capital to the places where it gets the highest return. Its not really relevant if NIMs are going up in NZ if the banks can get even higher returns by investing that capital in Australia, or redirecting it to business lending, or simply leaving it on deposit with the central bank.

I looked at starting a bank a few years ago (they are just a business, after all). It requires a hefty amount of capital (from memory, $120M). And compliance costs were astronomical.

Why don't Interest and the readership start a bank?

One of the reasons why Australia is more competitive for mortgages is because of the entry of Macquarie. However, even Macquarie has now thrown in the towel and is toeing the line. Why? Because no one can afford to give money away to gain market share any more. Now its about preserving capital and providing returns to bond/shareholders so the prices of their shares and bonds dont tank (which makes it even harder to obtain capital).

If you haven't seen it, you'd probably like the movie "Bank of Dave", there's also a documentary series and book of the same name.

>why isnt Squirrel doing mortgages

They do.

Then why on earth are they complaining that their competition aren't being very competitive?

The same way electric kiwi are complaining about the gentailers. Squirrel stand to make more money from:

1./ Revealing the rort for what it is

2./ All the PR in the process bolstering their business

Great article. Well done.

All sounds fine. But a couple of questions. Firstly, why put mortgage rates down? How about putting deposit interest rates up? Secondly, with house prices falling, and a good few people coming off low rates into higher rates, impairments should be up, and will go up even further. This will be followed by actual defaults and mortgagee sales at cash losses. Are you suggesting that banks just suck those up? Or maybe they are allowed to prepare for the worst?

I agree. This is just a populist, self-serving article with very little relevance.

So you're saying you're completely okay with monopolistic businesses charging whatever they like and funneling your money into the hands of already seriously rich people?

Seriously?

I can only conclude you must be one of the seriously rich people.

How about home owners' enormous debt being eroded by inflation so they're essentially getting a home for free. THAT is what would happen if home owners were allowed interest rates well below inflation. Feel like you wouldn't have much to say about that.

How about home owners incomes being eroded by inflation and tax bracket creep so they are making even less each year to serve their mortgages that are costing them more and more each year?

I understand that inflation erodes the cost of debt in real terms, but this assumes your after tax income can keep up. That is why it works best for governments who can just print their own currency and steal the wealth of its citizen base.

Heres an experiment. Look at your 2020 Total annual income. then put it in the tax calculator to see what your take home is.

Now to got the reserve bank inflation calculator and put that value in to see how much you need today to get the same amount of goods.

Now go back to the tax calculator and increase the before tax amount until the take home is equal to the inflation adjusted amount.

EG Q1 2020 Gross $70,000 less tax and kiwisaver is $52,809. https://www.paye.net.nz/calculator/

The inflation calculator states you need: $61,140 to maintain the same purchasing power. https://www.rbnz.govt.nz/monetary-policy/about-monetary-policy/inflatio…

Going back to the tax calculator, adjust the Gross until the Net amount is $61,140. This means you need to now earn $83,300 to have the same purchasing power.

So your pay has had to increase by ~19% just to stay flat. That is a 6.33% payrise each year.

Or what about lowering business rates. Support the productive economy ?

How about tiered rates of taxes for businesses like we have with PAYE?

I have little doubt that the vast majority of businesses would like that far better than gifting huge payouts to the myriad of oligopolies that exist in NZ's economy.

"Squirrel", mortgage broker, would say this wouldn't they. In my day, not so long ago, there was no such animal as a mortgage broker clipping the ticket. Where did mortgage brokers come from anyway....we seem to have managed very well in the past without them. They add to the cost of a mortgage.

All our problems around housing stem from there being too many immigrants chasing too few houses. For instance, the town-house owner next to me owns to two town-houses, one in the grammar zone and one next to mine outside the grammar zone. He is from China and works as an IT professional in Australia where he earns more money and his son went to medical school there. This type of immigrant adds to the price of houses.

These aren't the theoretical ramblings of ticket clippers.....they are the facts.

Mortgage brokers are simply doing the job that bank lending managers and back office staff used to do. By eliminating these roles, banks make more profit.

Say what?

"In my day, not so long ago, there was no such animal as a mortgage broker..."

Mortgage brokers have been around for 150 years or more. They might have been known by other names in NZ, e.g. "solicitor", but exist they have. It used to a side hustle by most insurance brokers too. Nothing new at all.

They served a valuable purpose in forcing banks to get sharp with their pricing.

Far too many people are simply working direct with their banks at re-fix times and are getting right royally screwed. Never think that a bank's carded rates are the best on offer. Nor at re-fix time assume that you've got a 'good deal' because the rate on offer is better than the carded rate.

If a mortgage broker is complaining that banks are involved in collective pricing (aka price fixing) - the broker are likely to be correct.

Say what !!!!

"All our problems around housing stem from there being too many immigrants chasing too few houses"

Only half right.

It has little to do with immigrants they are a tiny part of the whole.

It has everything to do with supply. And the major factors limiting supply are the NIMBY policies used by our City, Reginal and Territorial Councils.

It has everything to do with supply. And the major factors limiting supply are the NIMBY policies used by our City, Reginal and Territorial Councils.

partially correct again but as economics is tied to human behaviour, i’d argue attitude from opportunity in the 1990’s plays a large part in out predicament. Consider a world where there was no crash late 80’s and houses prices stayed stable with marginal gains at best over the last 30 years. The incentive to accumulate houses as assets would be next to nil and other means of wealth accumulation for retirement would be more spread due to the range in gains. Now consider this would have had a more diverse cultural impact on children of baby boomers, and their children, and we would have a VERY different NZ than today.

My challenge to our four big Aussie-owned banks is this: put your home loan rates back down

A rate of 6.99% for the one-year fixed home loan term would be a good start. It’s time for our big banks to do right by Kiwis.

The Squirrel business is not feasible without the Ponzi. The biggest takeaway here is that the the cost of debt servicing is not eliciting the right behaviors. Whether that is good for NZ or not in terms of socio-economic health is not in question here.

The squirrel business is far more viable than the banks if the Ponzi scheme collapses or stagnates.

The squirrel business is far more viable than the banks if the Ponzi scheme collapses or stagnates.

Why? Essentially it's just another layer of ticket clipping.

If someone borrows a million dollars from a bank of course it’s the banks job to make money from it they are only around 2% over OCR what is the point of doing it for nothing. If someone ask you to borrow a million would you do it for nothing knowing that if you invested it it would pay you back with interest. These people paid way to much for property now the market is crashing they have to stand by this discussion or sell and recoup what they can. Nobody made them buy that house get on with life you made a financial mistake.

Seriously, what are recent home buyers rationale behind paying so much for a property, besides ‘everyone else was doing it’ or ‘they told me to’ or ‘I had no choice’

how about we recognise that we are signing legal documents stating we owe hundreds of thousands to a bank, and listen to our survival instinct saying ‘ no don’t do that’

The sad thing is when rates were at emergency low rates the FOMO just push up house prices to a place where everyone was stretching their finances now price’s are crashing and rates have return to normal the ones who were outbid and could not afford to purchase at silly prices are relived. By my experience it will be around ten years before price’s hit old highs from end of 2021,and if world financial problems hit harder it will be way longer but the way NZD is tanking inflation could change everything.

If someone borrows a million dollars from a bank of course it’s the banks job to make money from it they are only around 2% over OCR what is the point of doing it for nothing.

The problem more lies in the Reserve Bank and a bunch of MPs with property portfolios running policy for the benefit of their portfolios and the banks, rather than the benefit of multiple generations of New Zealanders.

Let's get real here.

Retail banking is a utility. But bankers like to pretend it is very complex and a dark art. It's nothing of the sort.

Since banks started user computer systems the costs have fallen.

Then along came the internet and not only did costs fall even further but the ability to hand greater volumes increased dramatically.

And yet banks cling to the nonsense that what they do is complex and therefore it's going to cost to use their services?

Enough of this total b.s.

The RBNZ and Government MUST act to get new entrants into the market.

Where are the big US and UK banks? Where are emerging Indian and Chinese banks? Isn't it about time the RBNZ and Government addressed the role they play in their absence?

But further - and this goes to root of the problem - where are online-only banks? I haven't been to a bank branch for 15+ years! A new entrant bank could be up and running virtually overnight doing online only services. Sure, the older generation may never become their customers but let's get real again, they're dying out!

Time for a public enquiry into what role RBNZ and Government 'regulation' plays in why there is so little competition? Methinks so!

How about a new 'branchless' residential mortgage bank where getting a mortgage only requires salaries and wages to be paid direct to them but can immediately be routed out to any other bank (that has ATMs, branches, etc.) so long as a minimum balance remains that covers the next mortgage repayment? Extremely low overheads would mean the best interest rates by a long, long way.

(BTW - That bank could be a government department ... See the big stick I carry? But I'm still talking softly.)

State Advances Corporation loans at 3% p.a. fixed for loan term borrowed directly from the RBNZ?

Criteria: First Home Buyer. Salary/wages into Kiwibank account.

Nah, young people these days shouldn't be so entitled to expect that sort of welfare.

I'm not trying to disagree but

Most bank (were) offer a cash back bonus on your mortgage if you direct your main salary to them (for the entire loan period I assume). It was like $400 (one time) so I guess that's how highly they value the utility of having that happen. It's just not that valuable.

We have at least China construction bank in NZ, It wouldn't surprise me if other banks are just not interested, our rates are scraping the barrel compared to global rates and probably arn't going to pay that many bonuses, especially when you factor in the exchange rates.

We already have both Kiwibank SOE and NZHL.

The Government MUST. Seriously? No the Government must not. This Government has interfered repeatedly trying to make things "bedder", and has failed risibly at every single turn, since they had no idea about flow on effects of their daft policies. How about this: Average weekly rent in 2017: $400, in 2023 up 53% to $610. Labours Healthy Homes regulations, massive inflation affecting mortgages & removing interest deductibility have pushed rent prices up record amounts while reducing properties for rent by 19% year ended June, while demand is up 35% (against reduced supply, pushing rents up even further). Who the hell could have figured out that would happen? Other than someone who is not an intellectual pygmy.

and banks pays OCR to govt through rbnz, so who gets the most money from interest hike? GOVT

Sickening

Retail banks made 7.18 billion in 2022. The government got 2 billion in tax from that. Sure they could try and get effective competition. But

The government could make the $2 billion in the blink of an eye by a) implementing a CGT and b) setting up a specialist "residential mortgage only" bank.

In fact, a CGT may not even be needed as a government owned bank doing only residential mortgages would be retaining profits about $4 billion of profits in NZ and the multiplier effect would do the rest. (Shame about the existing banks though. They'd have to downsize real fast.)

Went to main branch of BNZ in one of NZ's larger city asked for $10,000 cash out of my account the manager was stunned, we don't hold that amount was reply, come back next Tuesday.They don't do any foreign cash.

Decreased staff dramatically over last ten years,cheaper to use brokers

Never had an issue with large cash withdrawals from BNZ Frank. Foreign currency is a different story. Depends entirely on the currency, but if you want decent amounts, it's usually 2 days. And has been for years and years.

Went to the bank the other day so that I could pay the balance of our new roof clad. It's over the $10k limit on my account (which I am happy with). I figured there's less risk of it going to the wrong account and better chance of recourse if the bank teller makes a mistake.

While waiting in queue I had 3 different people suggest I just go home, phone up and increase my internet banking transfer limit. Even the teller suggested the same. Is their bonus structure tied to how many people don't visit a branch?

That's an expensive but entertaining evening, right there.

When I was a kid I played a game called Monopoly. I lost so many times until one day, they let me become the banker. Bingo. That's how you win at that game. Become the banker.

Buy everything you land on was always my strategy and so prevent your opponents from building a set.

I always used my turns to move any houses/hotels to be within the most probable range of my opponents landing on them, and used mortgaging of non-set properties to initially pay for the houses. always traded for the lower value sets first, because the effect snowballs pretty quickly. fleeced my family every game.

So many people didn't fix for 5 years when interest rates were much lower than 4% and started to rise. Kinda makes them responsible for the predicament they are in now.

Can't blame the banks for people not having the foresight to fix for long when interest rates were at their lowest point in over 45 years.

It's amazing how much of a free pass people give the banks. The only business model where a bait and switch is acceptable and the customer is at fault. What you're effectively saying is when interest rates were lower than 4%, the general public should have had foresight to fix long because it was obvious rates were going up. Yet the banks were still writing big mortgages with low test rates until late 2021, so the banks most certainly should have known interest rates were going up. But it's the wild west of the lending market, every man for himself.

I'm guessing you are unaware of the obfusication and outright nonsense the banks used to reject just about all attempts by people to re-fix - or break and re-fix - or consolidate debt - at these low rates?

Or that they arm-twisted people into far shorter terms? Or that they pretended rates had even further to fall?

Just one example: They applied "test rates" at the beginning of a 5-year re-fix at 2.99% rather than at the end of the five years while ignoring the fact that the vast majority of people applying to re-fix would actually be paying less than they were at their current fixed rate!

That's not applying "commercial judgement" - the "get out of jail card" they use for any suspect behavior - it's usury (the action or practice of lending money at unreasonably high rates of interest), pure and simple.

The word went out to bank staff when rates got that low. Doubt me? Here's ASB's chief executive Vittoria Shortt:

"We've been preparing for higher interest rates ever since we had record low interest rates."

Source: https://www.goodreturns.co.nz/article/976522089/times-are-tough-for-bor…

And people wonder why banks in NZ are so profitable. Sheesh. The answer is friggin' obvious. We have an extraordinarily weak regulatory system that allows banks to engage in this sort of practice.

Interest.co.nz would do well to follow this. Lots and lots great column inches.

It is the reserve banks which sets the interest rates(ocr). and govt gets all the surplus profit. and head of reserve banks is appointed by finance minister. so just think who will decide interest rate in nz.

Only reason they say for collecting money is foreign direct investment.

if then people would like to know how much is the amount which came to the banks in the last one year for which rbnz pays interest for?

yes some money might have came but all will be there in the real estate, how many million came in outside of real estate.

To stop spending govt don't need to take peoples hard earned money but can pay the principal borrowing.

Bank employees are biggest price inflators with their salary. and they teach lessons to others to stop spending.

Wait, Squirrel run a brokerage - so earn commission (isnt it like 1%??) and of course everyone gets cash when they sign up for a loan, so doesnt that also come from NIM?? I think it is disingenuous to talk about margins and assume that is only home loans, when it is likely generated by transaction accounts at banks having zero percent interest. Given capital, it may well be that home loans are not covering that cost. After all Squirrel website says they charge around 10% interest for 1 year??

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.