By David Cunningham*

Most of the time, there’s not a lot of difference in what you get between New Zealand’s main banks.

Home loan rates are a good example. It doesn’t matter which bank you’re with – the rates you’ll get are the same, or near enough, across the board.

But actually, right now, that’s not the case.

Two of our big five banks have really stuck their necks out in the home loan market.

At one end, there’s ASB. After bumping its rates up twice in the last few weeks, ASB is now charging customers 7.45% on the popular one-year fixed term mortgage rate.

And meanwhile, at the other, there’s Kiwibank – charging 6.99% for the same term.

To put that range into context, the 0.46% difference between Kiwibank and ASB would cost you $2,300 more each year on a $500,000 mortgage. Not exactly chump change.

The rest of the pack (ANZ, BNZ and Westpac) are running somewhere in the middle, between 7.19% and 7.25%.

When ASB last hiked its home loan rates a couple of weeks ago, it took the unusual step of justifying the move.

It cited changes in the OCR, wholesale interest rates, customer term deposit rates and the cost of overseas funding – noting that all had increased significantly in the last two and a half years.

In reality, however, both the OCR and wholesale interest rates have remained flat since May, and the cost of overseas funding has actually fallen since the start of 2022. For example, the wholesale markets spread the Australian banks borrow at has fallen from about 0.60% during 2022 to 0.45% now (data sourced from Bloomberg), which is at odds with recent comments by some banks.

So why the difference in rates then? Well, in short, it all comes down to profit.

One bank is prepared to sacrifice market share to earn higher short-term profits. The other is prepared to forgo higher short-term profits to grow market share, and therefore ensure stronger profits in the longer term.

If anyone wanted proof of where ASB’s thinking is at, in my view you need look no further than recent comments made by Matt Comyn, CEO of Commonwealth Bank – ASB’s parent company in Australia. He caused a bit of a kerfuffle when he came out bemoaning the poor returns on mortgage lending in New Zealand right now.

To me, what’s so disingenuous about Comyn’s take on the issue is the fact that banks don’t just make their money on mortgages. Their profits are actually largely determined by the difference between the interest rate they pay to savers and the interest rate they charge borrowers.

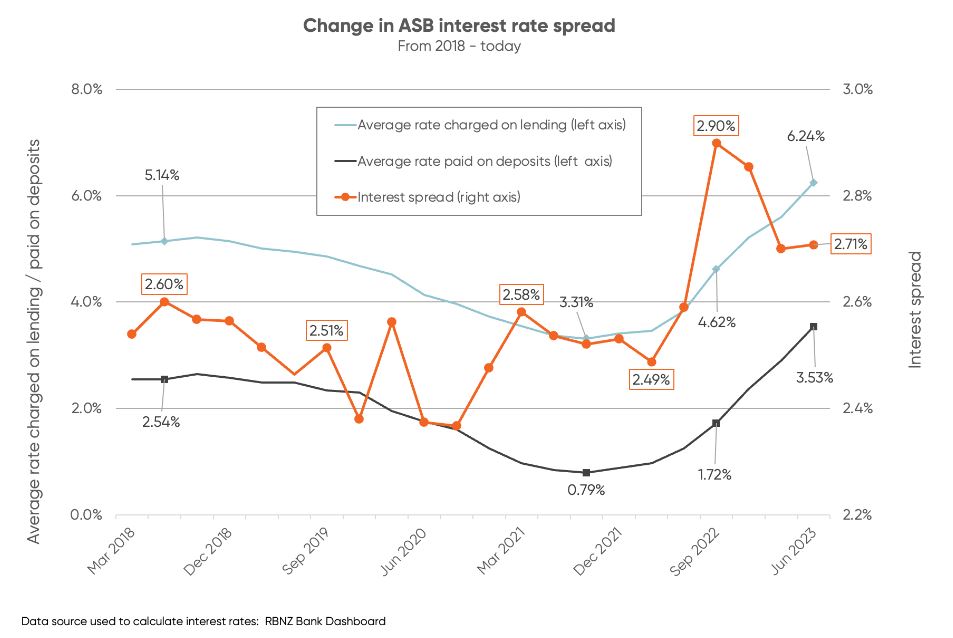

So, let’s zoom out for a second, and look at that bigger picture with ASB.

The below graph uses Reserve Bank data to track the average rates ASB has paid, and charged, over the last five years – and therefore gives us an idea of the interest spread it’s making (the line in orange).

Over the last 12 months, ASB’s margin has been higher than at any other time in the last five years. Not a bad place to be when the rest of the country is in a cost-of-living crisis.

Where to from here?

I’ve got a sneaking suspicion we could see ASB lower its home loan interest rates soon, at least to a level that’s back in line with the other Australian-owned banks. Its market share is being hit hard and the short-term profit from higher margins will be at the expense of longer-term profits.

For Kiwi who have a mortgage with ASB rolling over soon – or anyone considering a mortgage with ASB – it would be wise to shop around or ask them to match the best deal you can find.

Chances are good you could get a cheaper rate, and potentially a cashback of up to 1% if you change banks. Even on a $500,000 mortgage, that could leave you thousands better off.

*David Cunningham is CEO of Squirrel, a mortgage broker that also offers peer-to-peer lending and savings and investment products and services.

The opinions expressed in this article should not be taken as financial advice, or a recommendation of any financial product. Squirrel shall not be liable or responsible for any information, omissions, or errors present. Any commentary provided are the personal views of the author and are not necessarily representative of the views and opinions of Squirrel. Squirrel recommends seeking professional investment and/or mortgage advice before taking any action.

To view Squirrel's disclosure statements and other legal information, please visit its legal agreements page here.

35 Comments

or asb are keeping the rates high hoping to offload risky debt to competitors before it turns to custard?

they have double the impaired loans of anyone else except rabobank (who they have 60% more than). Though, looking at the 90 days but not impaired is going to make this quarter's update interesting reading.

ASB one step ahead.

I have returned most of my funds to ASB as I feel they are the safest bank i.e lending at higher rates to I hope premium customers. Anyone seen that ad at moment for Finance Now which seems to be owned by SBS that ad has set of alarm bells to me reagarding what type of lending they are targeting. Anyway I am being very careful moving forward as many loans in my view for next few years are going to default. What are some of the biggest borrowers/banks with exposure that we should keep an eye on ????

Yes Kiwibank and BNZ seem overly concerned about high interest rates, and have been trying to talk the market down for the last 9 months. Are they worried about their own book...........7% mortgages are only 1.5% above the OCR, not high at all. The international cost of funding has surged in the last 6 weeks, US 10 yr now 4.33%.

Becnz - why would premium customers choose to borrow at higher rates? Premium customers are the ones who can easily shop around for the lowest rates. More likely the borrowers left at ASB are the ones with low equity and/or income who are unable to refinance elsewhere.

I don't understand why KiwiBank can't grow quickly here. Any money lent returns a profit that stays onshore. The government would do well to simply fund a massive capital injection at wholesale rates and use the profits to fund something big and important like a new hospital.

I've heard from a broker, the turn around time at Kiwi Bank is around 15+ working days, so I would say they are being flooded with business.

But what is the quality of that business? 60% of FHB are the newly minted permanent residents buying with 5% deposits and the Govt guaranteed loan scheme. Not all business is good business.

https://www.oneroof.co.nz/news/first-home-loan-scheme-is-open-to-abuse-…

I’m not sure why the government should subsidise the housing market at all.

Obviously none of us will know, you would need to ask Kiwi bank themselves.

Noticed this ASB trend from a couple of years ago. They used to be one of the last to raise rates but are now firmly in first place. I’m a safe/quality customer $1M+, that they have driven away to greener pastures. I hope more leave tbh, and attitudes change.

Just to understand better, you had $1M+ debt to ASB and you decided to move it to another bank?

We (New Zealanders) chose to borrow like drunken sailors and collectively bid up the price of our properties far beyond any reasonable measure of underlying utility or value.

We shouldn't then be surprised that those on the outside eventually start treating us like the unhinged financial maniacs we are by demanding a larger risk premium.

We shouldn't then be surprised that those on the outside eventually start treating us like the unhinged financial maniacs we are by demanding a larger risk premium.

The 'risk premium' ultimately lies with 'the people'. We're on the hook if it all goes to seed. Not the banks. They know that.

I'm not really sure what risks our banks carry anyway. What are they?

A decrease in their mortgage portfolio would be the biggest risk as that decreases profits, shareholders who can vote with their feet will demand return for their money. If investors walk, banks must front up with additional capital, by making deposits and returns more attractive to their shareholders/customers.

Considering banks need to meet higher capital regulations, you can look at this the other way round, banks need to lower their lending relative to capital. For the same return, shareholders demand higher, and so banks need their loans to work harder.

The old capital regulation was 8%, I believe the new regulation is 12%. For the same capital, that’s a 33% reduction in lending. That lending needs to satisfy the shareholders so needs to work 1.5x as hard.

If you’re not thinking higher for longer, it can only be because you expect the economy to hit breaking point.

And maybe this is what ASB are doing, attracting capital while setting rates at a level that they can offload some risky loans, bring their loan book into balance and retain capital.

Yes yes. You express things well. When we consider 'existential' risk, the banks are like no other. And I think 2023 has been a good illustration of this, particularly in the U.S. banking system where many of the banks are arguably being propped up through manipulation of the money supply and central banking smoke and mirrors.

It's just unfortunate some of these New Zealanders are young and not clued up in macroeconomics, just caught out buying a house at the wrong time. They've believed that because the bank is taking ownership of the risk assessment (test rates) that they have taken into account interest rates cannot stay low forever, with their wealth of experience and data.

Golly. You're not suggesting the banks were looking to pocket these lenders deposits? I'm shocked!

What's Squirrel Bolton's mate looking to do here? Highlight how the customer is getting squeezed or indirectly pointing out how he cannot optimize the size of his ticket clip?

Love the sentiment, because that chap is a broker, he can't write an article that states ASB is bending over people who are experiencing a cost of living crisis.

To be fair, he also seems to be a bit disingenuous. He forgets to mention that out of that margin comes broker commission, which is chunky (and low new $ in market means a massive drop in broker commissions) ... and you never used to be able to get 1% cash back ... where does he think that is paid from?

He talks about flat swaps over the last bit, but if you zoom out a bit, the last time swaps were this high, like 2008, the interest rates were much higher (both HL and deposits), so they look to just be catching up. Depositors should be happy. Not every NZer is a borrower!

You highlight your lack of knowledge to everyone here with a statement like that, Interest rate offers are mandated to be the same via branch and broker, so with and without broker commission.

There is more to the picture than just swap rates, it might pay for you to read into how banks make their profits and what products/accounts have changed over that same time.

What mandate? While it might happen in practice, I've never seen regulators saying that. In fact, the fairer thing to do is for broker loans to be charged more to cover the extra cost. Why should other customers subsidize? The point still stands that commission is a large cost input. Let alone these crazy cash incentives.

Of course when Aussie tried to mandate that brokers should charge fees to customers for advice after royal commission, that got lobbied away. Wonder why.

You may also need to read up on the impact of rising capital requirements, and therefore rising capital costs. That has to drive up interest rates relative to where they had been to keep shareholder return on capital static. You may also wish to read up on CCCFA and the fact that cost justified credit fees legislation intentionally wants profit to be generated via interest rate margin instead of other fee margin. My point on swaps is simply to highlight there is recency bias here when people like Mr Cunningham talk about how rates have been flat.

Simple case in point - OCR has gone up by 5.25%, and neither fixed nor floating rates have actually increased by that delta?

Wait a moment there use to be a commentator on here saying the scrolls prophet said 10 percent guaranteed this year. If international borrowing interest rate has fallen the OCR hasn't gone up. The other 3 big banks are not raising their rates. Those scrolls might need to be left in a box beside the long drop

It was always my understanding that wholesale funding was a way to juice bank profits in Aussie - a kind of icing on the cake to please shareholders and a relatively small share of their total lending in terms of meeting reserve req'ments. CLSA used to run periodic scare campaigns that the Aussie banks were reliant on this wholesale funding and that the banks were potentially risky businesses. Not sure why CLSA used to say this as it seems that if you removed wholesale funding they would barely be impacted.

We borrow like we consume alcohol and the system will continue to support. They don’t want to kill you as long as you keep paying everybody is happy.

One of the problems with being one of the most expensive banks in the market is what happens to the overall quality of their book.

The good money that can be refinanced with other banks ... leaves - but the bad money that can't be refinanced with other banks ... stays. This can cause long term profitability issues - to say nothing of the bad press when the remaining staff - the good ones leave - try to filter the good from the bad and make the inevitable mistakes.

Not a strategy that shareholders should be happy with.

ASB may be offering special discounted rates to existing customers under the table, whilst publishing rates that puts off new more risky business.

Yes they are doing 6.99% for existing high equity customers.

Whoop-dee-doo. So are all the other major banks - if you ask and/or threaten them competitors offers.

Banks don’t want quality debt they want big debt. They would give a better rate to a dodgy $1 mil debt than a 100% safe 100k debt.

This squirrel David Cunningham is a top bloke looking out for us lenders !

ASB is doing RBNZ's work

If you goto ASB mortgage calculators etc, you need 20% deposit to get the best rates..... They do not look that hungry to win FHBers, I wonder what their internal modelling shows.

As a mortgage adviser this is great for business but man I feel sorry for their clients who are unable to refinance and are getting shafted for the sake of an aussie CEO's bonus package. The brand damage is massive with ASB generally not even considered for an application unless we absolutely have to go via them

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.