This week's fixed mortgage rate rise announcement from ANZ NZ suggests we are about to start another cycle of home loan rate increases.

The country's largest home loan lender has opened up space for their main rivals to rise into as well.

So it seems timely to assess the background drivers, and the pressures on bankers to hike rates at this time.

For a start, wholesale interest rate markets are pricing almost a full chance of a 25 basis points (bps) rise at the Reserve Bank's July 8 Official Cash Rate (OCR) review, and another full 25bps by October 28 (perhaps skipping a change on September 2).

But the OCR, currently at 2.25%, is only tangentially influential on fixed mortgage rates, mainly at the short end.

Most swap rates are influenced by the wholesale swap rates, and in turn they move based on a wide range of factors, local and increasingly international. After all, New Zealand is a debtor nation and we need to borrow some of what we need in offshore funding markets.

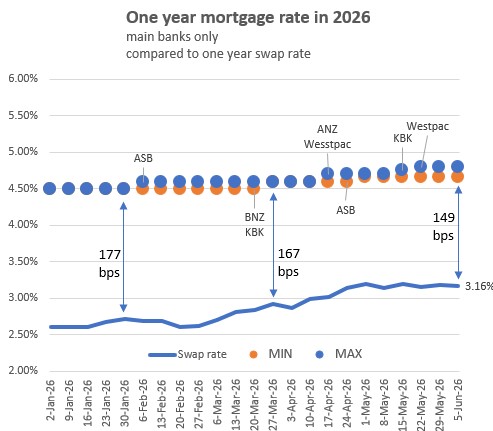

For the popular one year fixed home loan rates, here is how they have moved in the first half of 2026.

And for the equally popular two year rate, this is how they have moved.

It's clear that swap rates have not been rising recently, and don't seem to justify ANZ's recent hike.

But it is also clear that margins to swap are a little compressed, so there will be internal pressure from bank boards to restore these margins.

From our outside perspective, margin rebuilding seems to be the ANZ motivation. And that view is bolstered by ANZ not really increasing most of their term deposit rates when they made their across-the-board home loan rate changes.

Here is a snapshot of the lowest advertised fixed-term mortgage rates on offer from the key retail banks at the moment.

| Fixed, below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at June 4, 2026 | % | % | % | % | % | % | % |

| ANZ | 4.69 +0.20 |

4.79 +0.10 |

5.19 +0.20 |

5.49 +0.20 |

5.69 +0.20 |

6.39 +0.20 |

6.49 +0.20 |

| 4.49 | 4.65 | 4.95 | 5.25 | 5.49 | 5.69 | 5.89 | |

| 4.49 | 4.65 | 4.95 | 5.19 | 5.39 | 5.59 | 5.79 | |

| 4.49 | 4.75 | 5.29 | 5.55 | 5.89 | 5.99 | ||

| 4.69 | 4.79 | 5.09 | 5.19 | 5.49 | 5.59 | 5.79 | |

| Bank of China | 4.38 | 4.48 | 4.68 | 4.78 | 5.08 | 5.38 | 5.58 |

| China Construction Bank | 4.40 | 4.49 | 4.49 | 4.54 | 4.90 | 5.10 | 5.20 |

| Co-operative Bank | 4.59 | 4.65 | 4.99 | 5.29 | 5.49 | 5.75 | 5.89 |

| ICBC | 4.39 | 4.49 | 4.75 | 4.99 | 5.25 | 5.45 | 5.65 |

| |

4.49 | 4.69 | 4.95 | 5.19 | 5.39 | 5.55 | 5.69 |

| |

4.59 | 4.69 | 5.09 | 5.25 | 5.49 | 5.89 | 5.99 |

Fixed mortgage rates

Select chart tabs

Daily swap rates

Select chart tabs

6 Comments

Wouldn't it be nice if the other banks held their current rates, and ANZ were forced to back-track. Ha! I heard it. "Dream on" I hear you say :-)

What is good, is much higher deposit rates. Be good to get past 5% again soon, It is coming.

Already available. Check Interest saving pages 1 year and above.

Yes indeed, thanks, if you lockup for 5 years.

Be good to see it as floor for the shorter and then more up the longer dated.

How much, if any, of this can be explained by banks pricing in their perceptions of exposure risk in a falling market?

Most of the book is existing not new lending, I think this just margin protection. They will all follow and lift.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.