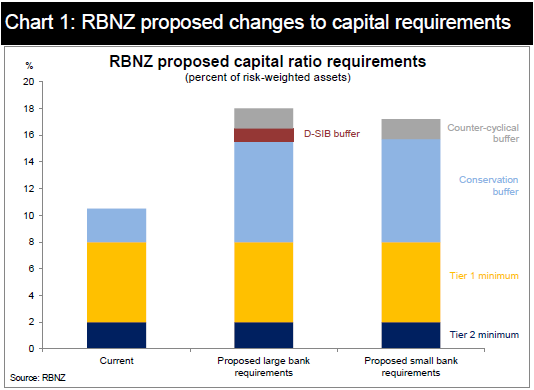

Last Friday, the RBNZ released a consultation paper proposing to increase the required Tier 1 capital ratio from 8.5% to 16% for the “Big 4” NZ banks (15% for smaller banks). Additionally, the RBNZ proposed to increase the “IRB scalar” applied to model-based risk-weighted assets (RWAs) from 1.06 to 1.2. This will also have the effect of further increasing large banks’ capital requirements.

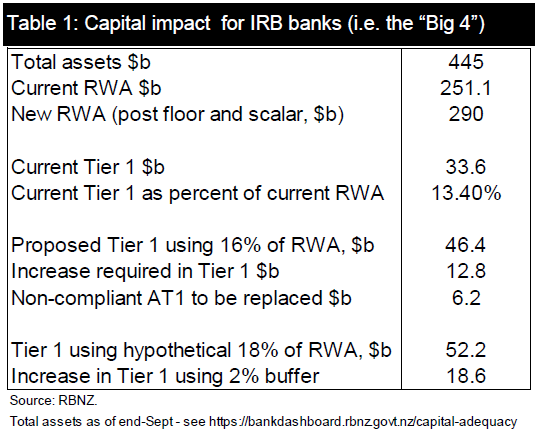

The Big 4 banks currently have a Tier 1 capital ratio of 13.4% compared to the current regulatory minimum of 8.5%. The RBNZ estimates that the Big 4 would need to raise $12.8b additional Tier 1 capital to meet the proposed 16% regulatory minimum (see Table 1, adapted from the RBNZ’s consultation paper).

Given banks tend to hold a voluntary buffer above the regulatory minimum, the required capital increase will likely be greater than this. Assuming banks held a hypothetical 2% buffer above the minimum (i.e. targeting an 18% Tier 1 ratio), this would imply the Big 4 banks needed to raise an extra $18.6b.

The Big 4 NZ banks are wholly owned by their Australian parents. The RBNZ estimates that the Big 4 would be able to achieve the 16% minimum target over a period of approximately 5 years using retained earnings (assuming 6% nominal credit growth and a stable return on interest-earning assets).

The consultation period ends on March 29th and the RBNZ will announce its decision by June 2019. The RBNZ has proposed a five year implementation period given the significant changes proposed.

Macro and rates implications

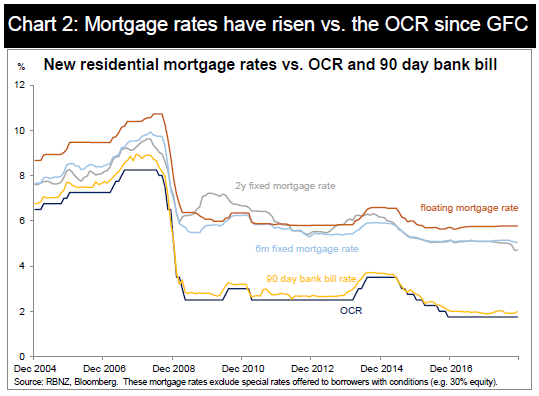

Since equity is the costliest form of funding (as it is the riskiest), the RBNZ’s proposal will likely mean average funding costs for banks will increase. The RBNZ’s survey of international studies suggests that a reasonable estimate is that a 1% increase in Tier 1 capital from current levels would increase the price of bank credit by 6bps. That would point to an approximately 25bp increase to large banks’ overall funding costs based on an increase from the current ratio to the proposed 16% minimum. Were banks to hold a hypothetical 2% buffer, for instance, that would point to an approximately 40bps increase in banks’ funding costs.

In turn, higher funding costs for banks might be passed on via higher lending rates or result in less supply of credit to the real economy. The RBNZ says it expects the impact on real economy lending rates to be “minimal”. This could be because the RBNZ expects banks to absorb the increase in cost via margins. However, it raises the prospect that the RBNZ might seek to offset any future increase in real economy lending rates with further delays to rate hikes, or even OCR cuts.

Directionally, the proposed changes would seem to be negative for growth and raise the hurdle for OCR hikes further. The RBNZ’s survey of international studies points to a relatively minor impact on growth (a 0.03% decrease to the steady-state level of GDP for each 1% increase in Tier 1 capital), although there is likely to be considerable uncertainty around those estimates. Either way, the changes will add to the growing market perception that the OCR will be lower-for-longer and help keep short-term interest rates relatively capped for now. It adds to the risk that the first OCR hike is later than our current November 2019 forecast (especially when combined with the recent falls in oil prices and rise in the NZD, which should weigh on headline inflation over the coming year).

To the extent that the proposed changes do transmit to real economy lending rates or result in credit rationing, the straightforward implication is that the neutral OCR will be lower. Were banks to increase lending rates by 40bps for instance, independent of the OCR, this would imply a lower neutral OCR by an equivalent amount. This would point in the direction of lower rates in the mid-to-long end of the NZ curve, which embed expectations of the terminal policy rate. The 5y5y forward swap rate is consistent with the market pricing a terminal OCR of around 3% currently.

The rates market implications are directionally bullish, especially for the mid-to-long end of the curve. But much depends on the final form of the capital requirements (expected mid-next year) and the reaction of the Australian parent banks. Additionally, the changes are planned to be phased in over a five year period, so it may take some time for the effects to be visible. Broader macroeconomic developments should remain the main driver of short-term NZ rates until there is more visibility on the likely consequences of the bank capital plans.

Supportive of bank debt

The RBNZ’s proposed increase to bank capital is supportive of senior bank debt given the significant increase in banks’ capitalisation. A 16%+ Tier 1 capital ratio will mean a much lower probability of default. We would expect senior spreads to grind tighter, even though the capital increase is planned to take place progressively over a five year period (meaning shorter-dated bonds will not benefit to the full extent from the increase in Tier 1 capital planned).

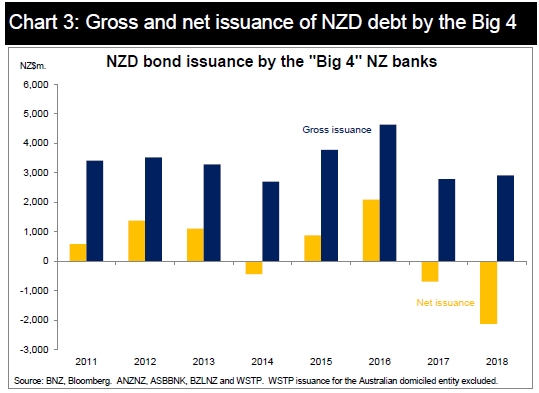

5 year senior NZ bank paper is currently trading around 100bps over swap. Net supply of bonds in the domestic market by NZ banks has been negative for the past two years, which is an additional supportive factor for spreads.

Bank debt issuance and the NZD cross currency basis

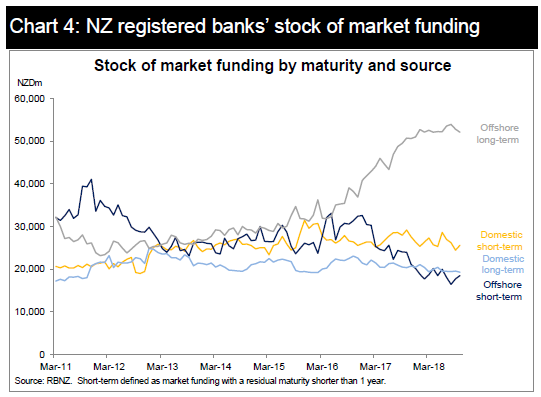

What happens to the future supply of bank debt will depend on credit and deposit growth. Over the past five years, deposits have grown just over $100b vs. domestic credit growth of $110b. The shortfall between deposit and credit growth was made up by long-term offshore market funding. In contrast, the stock of domestic market funding and short-term offshore funding fell (see Chart 4).

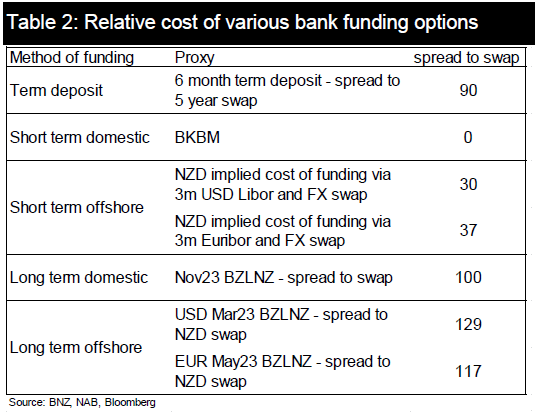

Looking ahead, there will likely be some downward pressure on term deposit rates, which should reduce deposit growth. The clear risk though is that wholesale debt issuance slows during the implementation of the new capital requirements, especially if credit growth is materially affected. Since offshore long-term funding is the most costly form of senior debt at present (see Table 2), it seems most at risk of being affected.

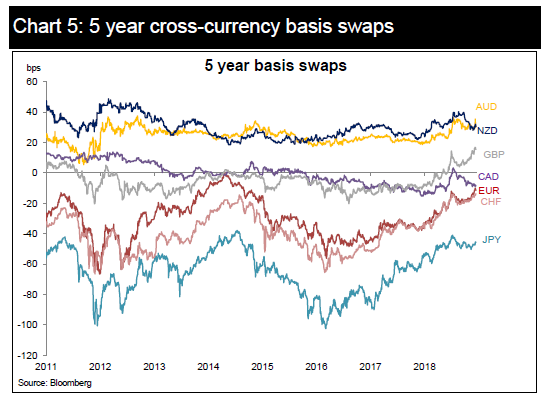

If NZ bank issuance offshore were to slow, then we would expect this to put downward pressure on the NZD cross-currency basis, all else equal. The NZD and AUD cross currency bases are positive, unlike most countries (see Chart 5), which we attribute primarily to NZ and Australian banks’ structural offshore funding programmes (the proceeds of which are swapped back to domestic currency to fund local balance sheets). In NZ’s case, this effect may be lessened if offshore issuance slows.

Potentially less growth in bank’s HQLA going forward

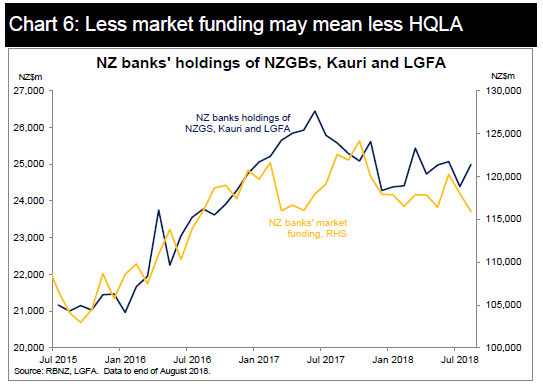

While the RBNZ proposal is primarily focused on the liability-side of bank balance sheets, there may be implications for the composition of banks’ liquid assets going forward as well. Banks hold NZGBs and other prudential liquid assets, in part to meet the RBNZ’s Mismatch Ratios (akin to the LCR).

If banks were to reduce wholesale funding for instance, over time there would be less need for banks to hold liquid assets to meet outflows. If banks’ wholesale funding grew at a slower pace than it has done over the past three years, it would also suggest that bank demand for NZGBs and other liquid assets would increase more slowly (see Chart 6).

In time, this might be expected to put some marginal upward pressure on NZGB yields relative to swaps, although we expect this should be second-order compared to the NZGB supply outlook and broader trends in investor demand.

10 Comments

Interest rates cuts, all the way, to the bottom.

Let’s face it - 5.95% is still a sky high floating rate in a ZIRP world.

Hummm more worries about the Ozzy banks according to Bloomberg

Article: Sydney's Property Plunge Will Be the Central Bank's Biggest Worry

https://www.bloomberg.com/news/articles/2018-12-18/sydney-s-property-pl…

The RBNZ will not want Auckland to catch the Sydney disease.

Maybe Orr expects them to raise rates and that's why hes keeping the OCR low. This sounds like a different way to prepare for a downturn / get through a downturn.

What downturn?

TTP

I'm reminded of that video of Comical Ali standing atop a building in Baghdad and saying to a reporter "The Americans are nowhere near here. The'yre miles away on the outskirts of the city" and the reporter looked over the balcony and smiled at the American troops down below....

This is a benchmark article for the one's expertise in our complicated banking / economic system :-)

I don't understand much of it - but would like to learn about many of the terminology they use here - spreads, domestic-offshore funding , swaps , bond , OCR etc :-P

Or they are just trying to confuse, because they can't convince !

Mate, Good on you to even read this one. I was going to encourage you, then saw the last sentence:)!!

I guess it's the reason why an in-depth-ish analysis like this one receives a lot less readership and even fewer comments, compared to the Gareth Vaughan article which not even scratched the surface and should bring shame to financial journalism.

Find any finance/economics student at/above year 2 at uni, and they can at least explain these terms. The analysis is pretty conceptual with not much number-crunching included (which would surely have happened behind the scene). These are matters all Kiwis should care about and try understand, as they will touch us all, and this time it is big. Just put aside the anti-bank, anti-establishment sentiment if any (as it doesn't really help does it), and try understand and have a rational debate about this topic.

Yes. PattyZ. Most of the DGMs and spruiker battle does not happen here.

And regarding the terminologies, may be year2 uni student would know about these terminology; but the actual impact and inter-relationship is hard to understand.

These numbers are ONLY used for a post-event analysis.. And if they make predictions, that is just to suit their needs !

Any downturn will be triggered by actions overseas. On a global scale, any levers the Govt can pull, are minor. Is everything all fluff unicorns overseas...based on overseas commentary I would suggest that its is not. The single biggest issue if the weight of over-inflated assets feeling the pressure of the weight of debt. Sound familiar?

Can the finance sector be responsible to control the weight of debt, or simply speculate to infinity to make their trading bonus - history clearly shows the answer to this. I guess the finance boffins can always package up the crap, give it a flash new name, and palm it off to some unsuspecting investor as some sort of derivative/collateralized debt obligations. Oh yeah they already tried that, people wouldn't be that stupid a second time.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.