The Reserve Bank (RBNZ) says quantitative easing and the use of term lending facilities will remain “mainstream” monetary policy tools that will continue to be used in the future.

The RBNZ started doing quantitative easing in March 2020 by buying mostly New Zealand Government Bonds via its Large-Scale Asset Purchase (LSAP) programme.

In December 2020, it also started providing banks with cheap funding to help them keep borrowing rates low via its Funding for Lending Programme (FLP).

Both programmes are mainly aimed at boosting inflation and employment. The RBNZ is due to stop making regular bond purchases via the LSAP in June 2022, and is due to stop making FLP funding available to banks in December 2022.

However, RBNZ Head of Financial Markets Vanessa Rayner said, in a speech delivered on Wednesday, these previously “unconventional” monetary policy tools will “likely remain mainstream for as long as global central bank policy rates remain at, or near record lows”.

Rayner noted that with the Official Cash Rate (OCR) already rock bottom, the RBNZ (like other central banks around the world) has “less space” to cut rates. There is also a “limit to how negative rates can go before causing adverse side effects”.

“This means that other tools that utilise the [RBNZ’s] balance sheet have become an important part of the ‘package’ of monetary policy instruments that global central banks have turned to.”

Rayner noted the RBNZ is one of only a few central banks in advanced economies that didn't have to deploy such tools until 2020.

She noted these tools can work in different ways, and don’t just reduce short-term interest rates like the OCR does. As the RBNZ understands these channels of transmission better, it will be able to “better calibrate an ‘optimal package’ of monetary policy tools in response to future shocks”.

Rayner also repeated what RBNZ Chief Economist Yuong Ha told interest.co.nz in an interview conducted on Monday afternoon (see above).

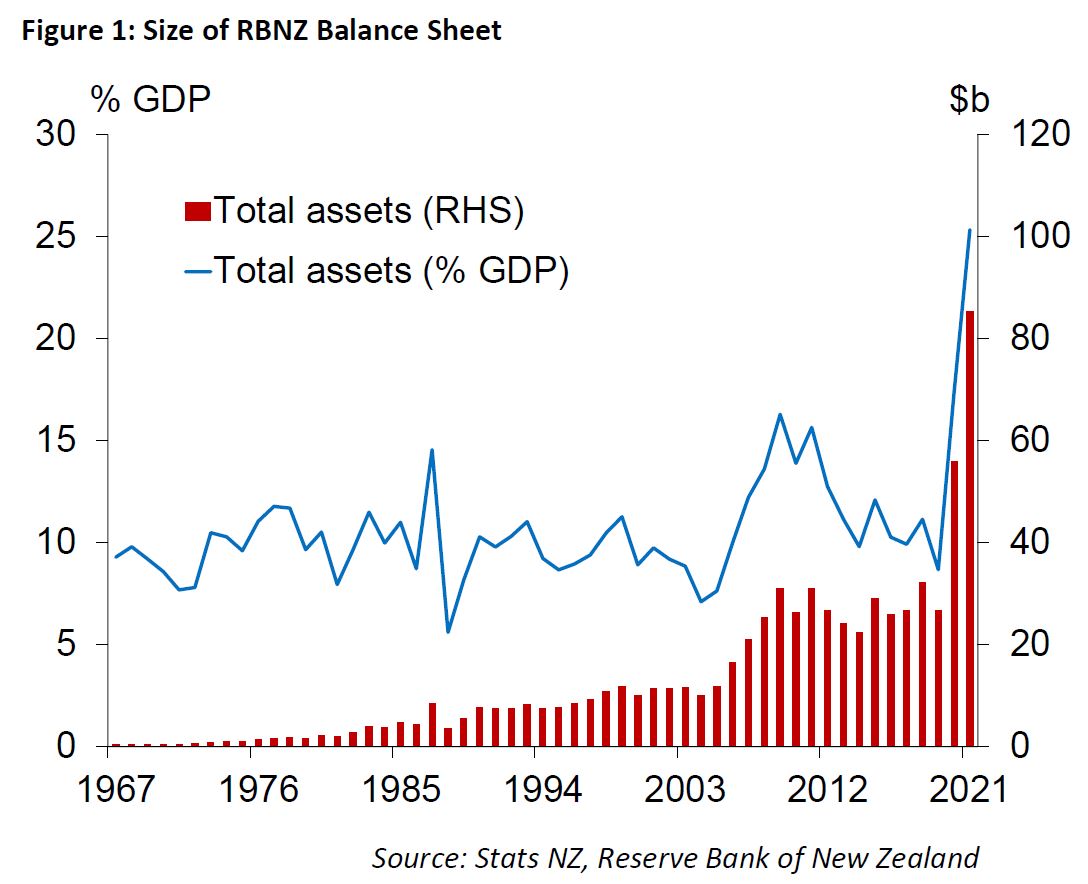

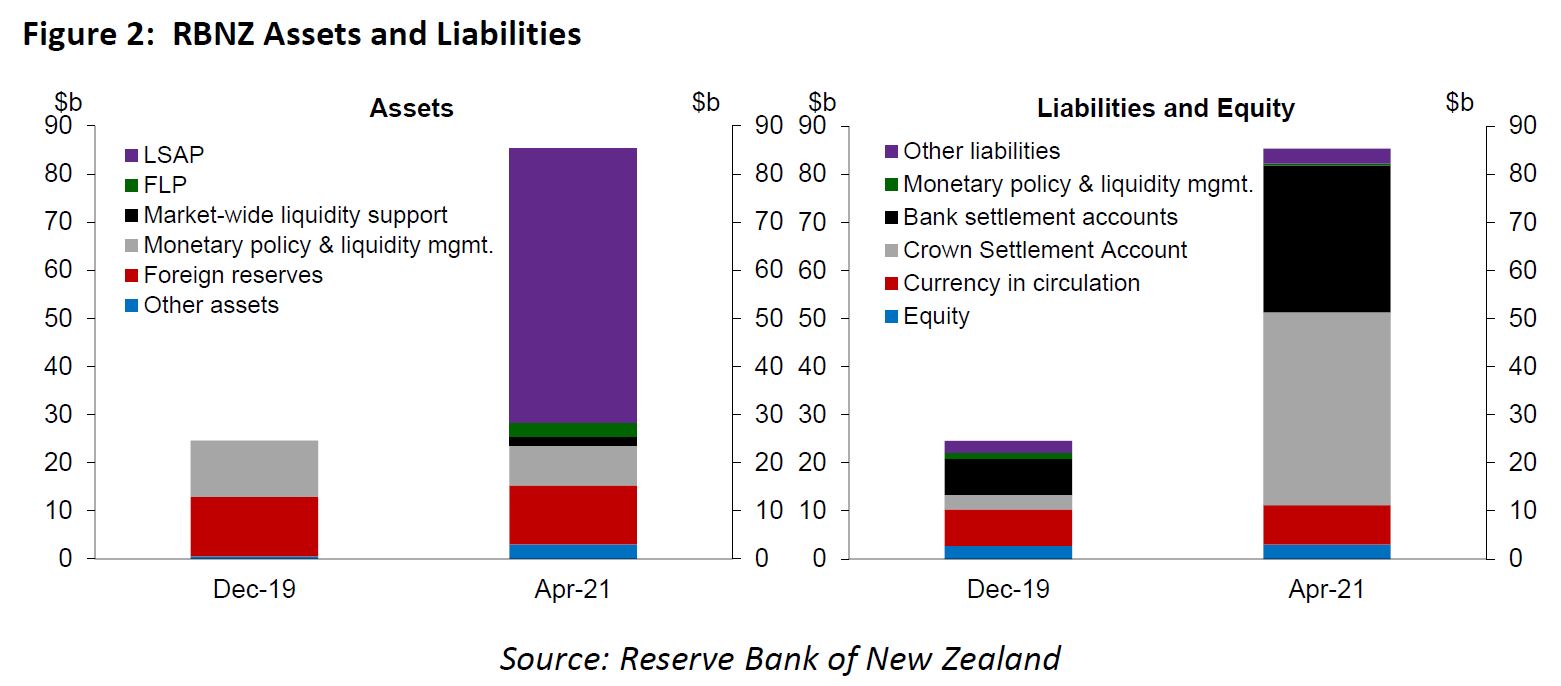

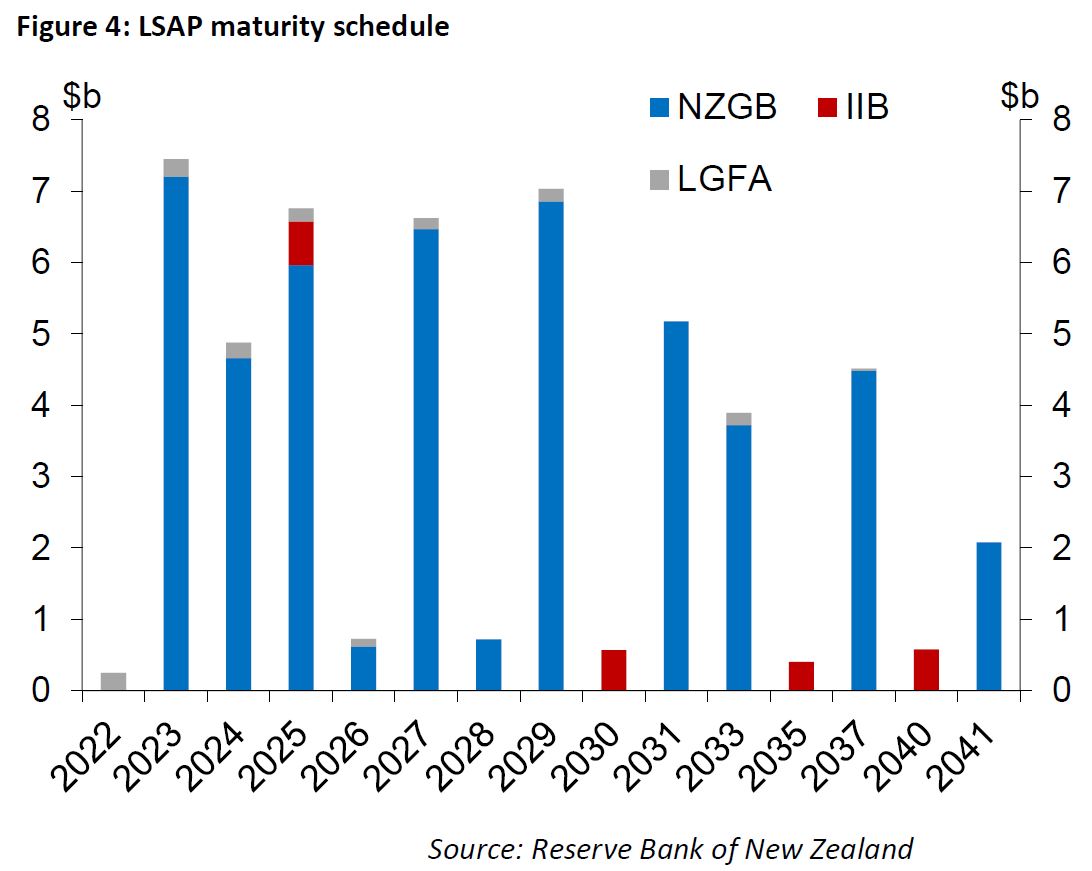

She noted all the bond buying the RBNZ has done via the LSAP programme has seen the RBNZ’s balance sheet balloon. For example, it now owns more than $50 billion of New Zealand Government Bonds.

But because some of these government bonds will only mature in 2041, they could end up sitting on the RBNZ’s balance sheet for decades to come.

And as Ha said earlier in the week, the RBNZ might not want its balance sheet to shrink at the pace at which the bonds it owns matures. So, it might decide to keep buying bonds to replace the ones that roll-off.

Rayner made the same point: “In many cases overseas, central bank balance sheets have remained large for a prolonged period.

“There have been some limited instances where the size of balance sheets have started to reduce when policymakers had sufficient confidence their policy objectives could be achieved with less support, like in the case of the Federal Reserve in 2018 and 2019.

“In the long run, the LSAP programme may be unwound and the size of the balance sheet may be lower than it is today. However, any decision to reduce the size of the balance sheet by not reinvesting maturing assets will depend on the level of monetary policy stimulus required in the future and will be decided by the Monetary Policy Committee, guided by staff advice.”

Financial stability

Rayner said the way the RBNZ does its job maintaining financial stability is also changing and some “further innovation” in its “balance sheet operations” may be required.

She noted the RBNZ has moved beyond being a “lender of last resort” to individual commercial banks that need liquidity to meet their short-run obligations, as it's started responding to “severe market dysfunction”.

“For example, last year we introduced a Bond Market Liquidity Support scheme to purchase small amounts of New Zealand Government and Local Government Funding Agency bonds at short notice when there were no other buyers in the market,” Rayner said.

“The subsequent LSAP programme also alleviated market-wide liquidity concerns, freeing up capacity on dealers’ balance sheets to return market liquidity to more normal levels.”

Rayner said the RBNZ would also change the amount of foreign currency it holds. It holds these assets in case it needs to intervene in the foreign exchange market to address market dysfunction or if the level of currency is unjustified relative to economic fundamentals.

Rayner noted changes being made to the Reserve Bank Act will require the RBNZ and Finance Minister to agree on a framework around the way the RBNZ manages and uses foreign reserves.

She said that unlike other central banks, the RBNZ hasn’t ramped up its foreign reserve holdings since the 2008 Global Financial Crisis.

Rayner indicated the RBNZ was viewing its monetary policy and financial stability roles through a climate lens.

Specifically, she said there is an “opportunity for central banks to take a step further to ensure their balance sheet operations actively support the transition to a low carbon economy and to ensure smooth monetary policy transmission over the long term”.

She said the RBNZ would consider “what adjustments we can make to our liquidity operations - including eligible collateral and pricing - to mitigate our own financial risks and to contribute to the development of the sustainable finance market over time”.

Risks

Bringing it altogether, Rayner recognised the RBNZ’s larger and more complex balance sheet creates risks.

The RBNZ has to think about how different monetary policy tools will flow through into the economy differently.

Using new tools also comes with “significant communication challenges”.

“It is generally more difficult to communicate the impact of balance sheet tools [other] than the OCR, as the current and future policy stance of these new tools cannot be accurately expressed using a single measure,” Rayner said.

“There is also greater uncertainty around the impact of balance sheet tools. This can lead to reputational risk and reduce policy effectiveness (e.g. the ‘expectations channel’ is weakened if policy actions and tools are not well understood).”

Finally, Rayner made the point the RBNZ faces additional risks by providing banks with longer-term funding and holding a lot of government bonds with long durations.

“In the past, the financial risks associated with traditional central bank functions such as monetary policy implementation and lender of last resort have been relatively low, given the collateralised nature of lending at typically a short duration,” she said.

“As we have expanded our operational tool set to include outright purchases of assets, longer-term lending and ‘market maker of last resort’, we are exposed to increased risks that need to be well understood and managed.

“Our priority is to not minimise risk, but rather maximise our ability to meet our policy objectives without undue risk - whether that be legal, financial, operational or reputational risk.”

31 Comments

"Rayner said the way the RBNZ does its job maintaining financial stability is also changing....."

"RBNZ"and "Financial stability" in the same sentence? Funny...

I would doubt the sanity of Orr and his team, unless the way they maintain their mental stability is also changing.

{kind=link}

Brilliant cartoon and great point in the cartoon of there not being enough 'stuff' to have the UK driving around in EVs let alone the whole world. Still amazes me every time we have the media running a story about how much we're meant to be cutting down on GHG emissions et al and then follow it up with a growth pedaling or population projection. When will the media start reporting not on the tailpipe emissions but what actually makes the engine run?

This won't help with the transport question - only new battery technologies will help with the environmental impacts of mining rare earths. But on the other hand, electricity production through a mixture of non-light water nuclear reactors and renewables is the way to go.

https://www.dhakatribune.com/opinion/op-ed/2020/06/22/op-ed-solving-cli…

In other words, welcome to MMT its here to stay. Take risk we will backstop any down side.

yip.... what a great society.

middle class unemployment insurance soon too ...government backed...and higher earners for sure too because that's only fair

marriage and mental health insurance cant be far away as products...$9.99 a week

Kiwis expect it!

Negative real interest rates are here to stay.

So everytime we have a recession in the future - the private sector takes no responsibility for this and central banks just continue to 'increase the size of their balance sheet'.

What kind of perverse incentive is this an what (bad) outcomes will occur?

I see that our media is praising interest only loans for saving some of our very wet farmers....

mana from heaven...how could we ban such an important option...

debt is our new jesus

Seems like a great use of interest only loans.

What kind of perverse incentive is this an what (bad) outcomes will occur?

I guess the brilliant plan in case of a crash is to print more to bailout both the lender and borrower. This should allow the Ponzi to run perpetually or at least till the place becomes absolutely unlivable.

Don't care what the apparatchiks and the boffins say, but the end result will be the destruction of the value of labor. You're going to need a skill set that enables you to dictate what you like or be able to milk the system accordingly. One of the best examples of this is court judges

Re value of labour, this is true if we ignore the mobility of labour. Once(if) borders re-open I am expecting the mother of all emigration waves, those that can see or are interested in their future will move to where the MMT experiment is not so advanced.

Re judges, having worked in the justice sector it was amazing and depressing to see just how random the process of court was. Each judge had their own way of managing the same case types, a fiefdom that was protected through the artifice of the three pillars.

Clown World.

I wonder what % of GDP the RBNZ need to have 'on their balance sheet' before we realise that we're running under a failing strategy?

Yuong Ha.... you have got no clue, for renters, losing their jobs and having a total reset in house prices would be MUCH better than having their whole future and their future offsprings lives forever ruined by being locked out of the ponzi and being charged insane rents plus paying taxes to fund housing topup grants to keep the ponzi going. You have done the wrong thing..... You have completely failed...... We can see what you have done......accept this fact and fix your mess or be tarnished forever like Orr!!!

No, it wouldn't. Losing their income and being forced to deplete whatever savings they have then ending up on the state housing waiting list, Then starting from nothing and trying to rebuild a deposit.. Sounds wonderful to you does it?

It would be temporary, not generationally eternal. Would a bear trapped in a cage with a needle harvesting its bile rather feel the initial harsh pain of removing the needle and be free of pain or sit still and accept the slow lingering dull pain of being tapped forever. If you were a renter you would understand. If you were a landlord you would also understand but just not care and try and convince the renter how fortunate they are.

Insane is the only word that some to mind. So much for telling people to save, when that value of their savings is losing value with real world inflation.

Inflation is not affecting everyone across the board to the same extent. FHB trying to save for a house are the worst affected in the country. Those that have the house already paid off and money in the bank are the least affected. There is simply no comparison from one end of the scale to the other.

Why wait and let time eat away your hard earned money?

Secure your financial future with a house today!

A house has been the only way to get ahead in this country and it shows. It was simple math for me, take out a 15 year mortgage and go hard to pay it off then be able to cruise and then give your typical NZ employer the middle finger. Local manufacturing and job opportunities in this country have suffered as a result of our housing obsession and we are still going backwards. Not sure when we will hit rock bottom but the next GFC should finish the job.

Pick one up for someone you love, its the gift that keeps on giving... RB guaranteed

Tis not going to end well...but end it will

Japan.

That is all.

There is no taper from here, no normalisation, just years of puzzling where the growth went.

The example they give of tapering -- USA in 2018/2019 -- is one where the central bank had to rapidly reverse their decision and embrace QE again!

Japan, the EU, and the Fed -- none of them have found a way to back out of the QE/low interest rate/foie gras liquidity swamp -- I'm sure it'll be a piece of cake for the RBNZ.

Inflation is our Obi Wan. "Even the darkest night will end and the sun will rise" - Victor Hugo

We're getting a good dose of inflation right now, but I suspect it will pass.

Even if it becomes a pressing problem, given the crippling debt burden we've (wisely, apparently) taken on, raising rates would be worse from a 'financial stability' perspective.

I think Minsky's ideas on the danger of systems that try to enforce too much stability might be the key here. Central banks are willing to do anything to prevent a moderate recession; yet their actions create so much moral hazard that the integrity of the whole edifice is undermined. They'll keep pushing the same approach until something breaks irrevocably and disastrously, until the point they are actually powerless.

So what happens when the bonds mature? Does the NZ government pay them back and then the RB has a load of cash sitting around? If so, what then? A "dividend payment" to the government?

Government issued currency will either be held in the form of bonds or as commercial bank reserves. Either way this money represents the private sectors and the foreign sectors savings and holdings of our Sovereign NZ Dollar Currency. Only taxation can cancel this currency.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.