ANZ economists have a view on what the Reserve Bank's best option might be if it decides to embark on 'unconventional' monetary policy - but they stress that any such policies carry risks.

In a recent speech, RBNZ Assistant Governor Christian Hawkesby re-raised the prospect of our central bank pursuing unconventional policies.

"Having effective unconventional policy options expands the toolbox of a central bank, which is naturally more relevant in a low interest rate environment. In this spirit, we published a Bulletin article last year on the practicalities of unconventional monetary tools in a New Zealand context, and we continue to learn from the lessons of our central banking cousins," Hawkesby said.

"It’s better to have a tool and not need it, than need one and not have it."

The question of the central bank applying different policies, such as for example quantitative easing, which was used overseas after the global financial crisis, comes about as people begin to wonder whether the RBNZ, with the OCR now down to 1.5%, is going to 'run out of ammunition' to help stimulate the economy.

ANZ economist Michael Callaghan and FX/Rates strategist Sandeep Parekh have had a detailed look and crunch of what the RBNZ's options might be for unconventional monetary policy in an ANZ New Zealand Insight publication.

"With the Official Cash Rate at just 1.5%, there is now a very real chance that monetary policy will run out of conventional ammunition in the next marked downturn (caused by, for example, a negative global shock, an extreme drought or an earthquake)," they say.

"Odds are rising that some kind of significant economic hit will occur before the OCR is back to anything approaching historical norms."

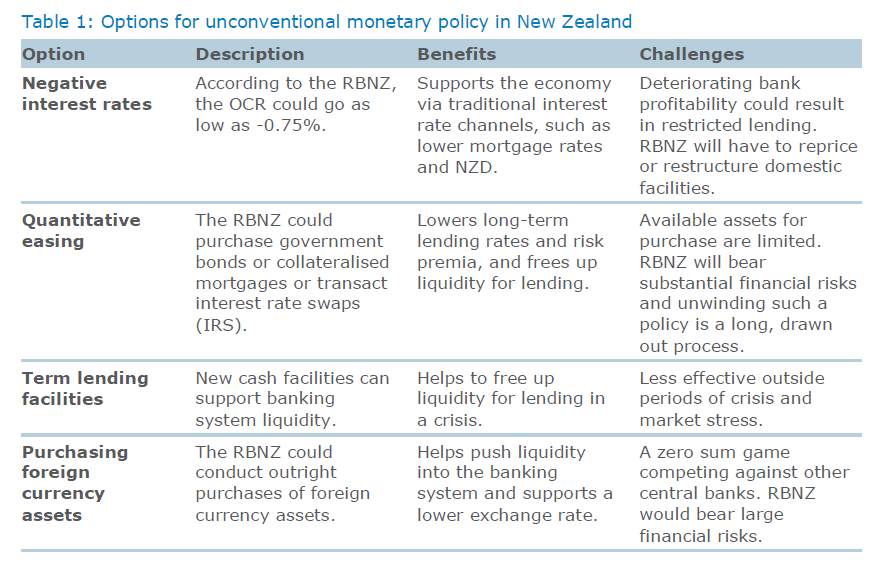

They have summarised the options the RBNZ has:

They say "it is certainly not a given" that taking New Zealand down the path of unconventional policy "would be necessary or wise".

"This paper does not address that complex question."

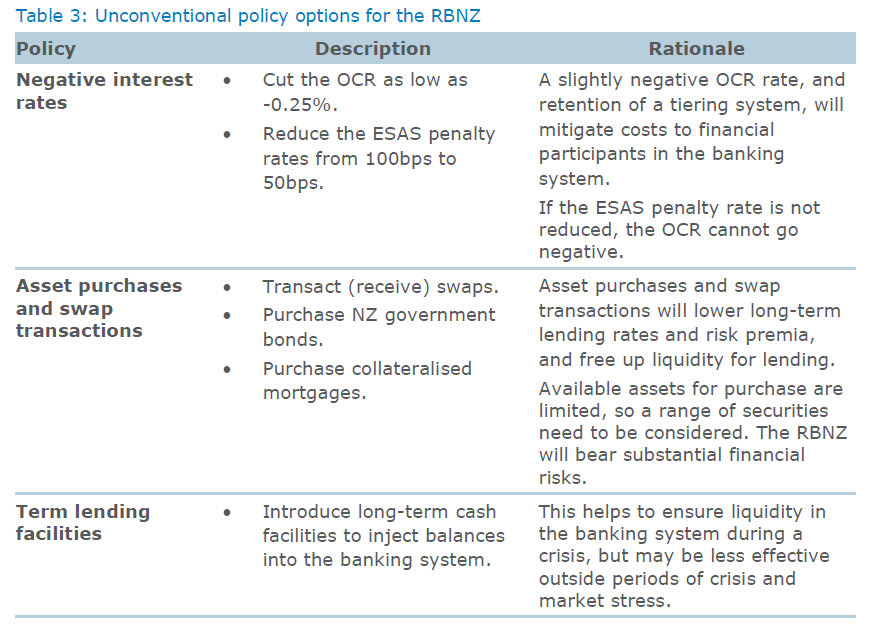

However, Callaghan and Parekh say that for the record, of the unconventional options available, they think that the best policy approach for the RBNZ would be to:

− reduce the OCR to -0.25% and provide strong forward guidance that rate hikes are a very distant prospect;

− reduce ESAS (settlement system) penalty rates from 100bps to 50bps;

− inject balances into the banking system (via a term auction facility); and

− transact swaps to reduce interest rate risk premia, and purchase NZ government bonds and collateralised mortgages.

"While we believe this would be the most effective policy approach, there would be numerous challenges, costs and risks associated with each part of it. Risks to the RBNZ’s balance sheet, market functioning, and bank profitability would be of particular concern."

They also say there would be several steps the RBNZ would need to take, and communicate to the market, to prepare for unconventional policy and retain market confidence.

This is the summary of Callaghan and Parekh's preferred option:

They say while they believe the options outlined above would be the best policy approach, there would be "numerous costs" associated with it as well as risks to the RBNZ’s balance sheet, while market functioning is likely to suffer.

And they say if pushed too far and for too long, unconventional monetary policy can lose effectiveness, given the negative implications for bank profitability and credit availability.

"Regardless of the policy options chosen, there are several issues that the RBNZ need to urgently consider and communicate to the market to ensure confidence in their ability to respond to a weaker economy. A plan for adjustments to the operations of the settlement system (penalty rates, tiers) and for fiscal and monetary policy coordination needs to be planned and communicated.

"At the end of the day, consideration must be given to whether unconventional monetary policy is a path we want to go down – the examples of those who have traversed this track before us certainly inspire a mix of hope and fear. But if unconventional monetary policy is a risky strategy, implementing it without prior preparation is undoubtedly a riskier one."

37 Comments

DGMs hate the fact that there are options beyond just interest rate cuts. So invested in a crash that they have an aversion to anything that could help with economic stimulus.

BLSH, don't read too much into an unconventional toolbox as a safety net. Its foolhardy to assume you'll always be insulated from the consequences of poor decisions. Yeah, I know, you'll next argue that under OBR, a small percentage of bank deposits are unsafe. The rhetorical question is, will you omit the part that in such dire times, property prices would have already crashed? If a housing recovery is on the cards for 2020/21 (according to you), why are you so invested in unconventional options beyond interest rate cuts? Being the first to post comment on this subject thread, it's easy to read the worry oozing from your comment.......

Remember this New Year forecast? "Auckland HPI: +1% - OCR: 1.75% all year? Are you still standing by it?

Not backing down from HPI +1% and median 0%. Also not backing down from 1.75% OCR all year as RBNZ was wrong to change it :)

BLSH, stop embarrassing yourself. Your comment (when read out) is so cringeworthy.

I sense a lot of anger and frustration from you. Cheer up coffin-dodger, life is too short to be miserable all the time.

"coffin-dodger" I love it:)

I think the main message is: WE WILL DO WHATEVER IT TAKES TO PREVENT A RECESSION

A Spruikers translation "I hope they print money cause I can see my losses only mounting. I do envy those flush with liquidity. In times of heightened anxiety, I even stoop so low as to label them lazy"

Yvil, in recent days you're honestly reading as a very anxious warrior. Just relax and take a chill pill. What will be will be.

'Yvil, in recent days you're honestly reading as a very anxious warrior'

RP have to say you come across as a ' angry old Narcissist' ! Envy of all those who made easy money off real estate and who will in the future.

Ha-ha-ha :) The cavalry has arrived! I'm truly flattered. "those who made easy money of real estate" Its a ditsy thing to say when it also includes me :) The difference is, my finances aren't leveraged on the foolish assumption of uninterrupted gains.

Keep humouring me Shoreman.

"WE WILL DO WHATEVER IT TAKES TO PREVENT A RECESSION"

That sounds like Mario Draghi. and look where it got him and the ECB.

I thought you believed in the free market.

Once the Fed hit around 0.25% that's when they switched to asset purchases. They had also bailed the banks out. So this isn't a matter of choice, when one option is exhausted then the next one is used. Asset purchases ended up being the last resort to prop up the market. They bought $4.5 trillion and are slowly unwinding the positions (which will take decades to finish if ever).

These unconventional policies lead to unusual market conditions and zombie companies end up being propped up, or financial engineering taking priority over running a profitable resilient business.

Why are we all so keen to avoid the consequences of our actions?

Indeed, whatever happened to standing on one's own two feet without state support?

Why not make the banks accountable, risk profile clear to investors with greater capital requirement.

If you FAIL you WON'T be bailed out so you better think about your ratio / profile correctly.

You want to stimulate, then give personal tax cuts and potential business tax cuts.

Agree my2c.

Government policy instead of reserve bank policy.

If people had more money in their hand, they will spend it back in to the economy.

Savers, spenders, retailers, familys will be happy.

So on a day that the CEO gets booted we get a publication from the same bank about unconventional (some would say unnatural) acts. We’re not even in recession yet and already we’re talking about asset purchases by the central banks and moves to near zero rates. Is anyone else concerned by this?

If you have a mortgage no. If you have your money in term deposits yes. The two tribes, Spruikers v DGMs.

HeavyG, your comment is understandably simplistic. It's actually short sighted (impatient) speculators vs visionary (patient) savers. In logical order there's greed, fear, panic then a world littered with opportunities. What's wrong with having vision? What matters most here is that when we reach the bottom, those financially liquid souls who have lost the least will then look to the sky ;-)

Money is losing value every day and your term deposits are tanking. You've mistaken laziness with enterprise. When you are left holding worthless paper you will see the real value of land and buildings.

Oh-okay, now HeavyG thinks he's still living in the 1970s, or is it Zimbabwe? No wonder you've been robbed of valuable insight. Remember, you can't eat a house when you are insolvent!

See who's laughing when your TD rates drop below inflation.

HeavyG,

I believe in keeping my finances as simple as possible. Most of my capital is in the share market,with some in a rental property. I have no debt. I also have 15% of my portfolio in cash(TDs). Why? partly because I would never want to be without some liquidity and partly because I have been taking advantage of the buoyant market to gradually take some profits to be prepared for a market fall-whenever that happens. The rate of interest on these TDs is not relevant. They are all short-term-from 3 months to 1 year.

Losing money's not relevant! And you're on here giving investment advice... SMH

Whether the Federal Reserve indicate a reduction in the funds rate this week,or in the near future the last time it starting an easing cycle, way back in September 2007. At that time both the RBNZ and the RBA in particular were continuing to raise rates. Albeit like all central banks they reversed course, but from a more advantageous starting point However .a decade later , after gorging on real estate ,we now, not only have lower current rates than the United States ,but also a lower exchange rate How our currency will be impacted in the coming months may be fraught with interest.

So...is this why house prices are tipped to rise 18% or so?

If interest rates keep falling, people will pile into housing again.

Hmm

So there will be 18% more funds being funnelled through housing. The interest payments on a $750k mortgage @ 4% are the same as a $3 million mortgage at 1%. The only thing holding them back will be capital ratios.

If you fail year after year, decade after decade, maybe the issue is not what tools you need for your toolkit, the problem is very likely you. Economics as it is today leaves Economists no way out, no way to check their most basic assumptions because they’ve been carved into Economic “law” by the Great “Moderation” even though the Great “Moderation” was built upon nothing more than “good luck.”

It is absolutely absurd. This is all astrology, or, as I called it three years ago, magic number theory. A puppet show.

In other words, this is no time to be timid because everything that he [Paul Krugman] and others like him promised didn’t work, which to them means that it didn’t work because it wasn’t big enough even though when they planned what didn’t work they said then that it was bigger and better than the time before that. There is apparently no economic ill that the “right” amount of policy can’t fix, even if that ill is policy. Unfortunately for the world, economists obviously aren’t permitted to know what the “right” amount of policy is until they actually see whether what they did do was it (I am not making this up). Why not just dispense with the façade of science and discipline and just throw darts? It’s as likely as what they are doing now to come up with the magic number answer.

If it takes you eleven, nearly twelve years to figure out after rounds of QE and the like that you now might need NIRP, then you don’t really need NIRP. You need to start over from the beginning.

None of those things "stimulate the economy" , all they do is pump up asset prices.

Sadly enough in the eyes of those who are in control, stimulating the economy and pumping up asset prices are the same thing.

And therein lies our problem. Most commentators on this forum would agree that it's a good thing too. So divorced are we from the natural inclination towards productive work, entrepreneurship and the conditions that are necessary to generate wealth through diligent work, we are now left to squabble over how best to satisfy a population of vultures and parasites who have a vested interest in asset price inflation (sorry, the financiers would call it 'the service economy'). The real economy is the farmer hanging in his shed. Banks are a moral hazard at this stage... for those who have morals.

Gee we really are in a race to the bottom. 'Interesting' times....

The ECB had this to say about NIRP

We show that negative policy rates affect the supply of bank credit in a novel way.

Banks are reluctant to pass on negative rates to depositors, which increases the funding

cost of high-deposit banks, and reduces their net worth, relative to low-deposit

banks. As a consequence, the introduction of negative policy rates by the European

Central Bank in mid-2014 leads to more risk taking and less lending by euro-area banks

with greater reliance on deposit funding. Our results suggest that negative rates are

less accommodative, and could pose a risk to financial stability, if lending is done by

high-deposit banks.

Audaxes, good post. Where does that leave NZ banks who are heavily reliant on domestic deposits (80%)? It's hard to imagine domestic depositors being prepared to pay banks to hold their money. It will be interesting to see what happens if/when RBNZ implements a negative OCR. Property prices would well and truly be plummeting along with employment and confidence to warrant it.

They won't go negative, or buy govt. Maybe corp if things kicked off.

Else IRS & FBB. Need to think about the problem they trying to solve.

OCR is independent of balance sheet exp

Before we consider “unconventional monetary policy” shouldn’t we look for examples anywhere in the world where these ideas have been implemented and actually improved things?

So much from learning from others mistakes.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.