Taxpayers will lend "viable" firms that employ 50 or fewer full-time staff loans of up to $100,000 under a new “Small Business Cashflow Loan Scheme”.

Legislation authorising the Inland Revenue to administer the scheme was passed on Thursday.

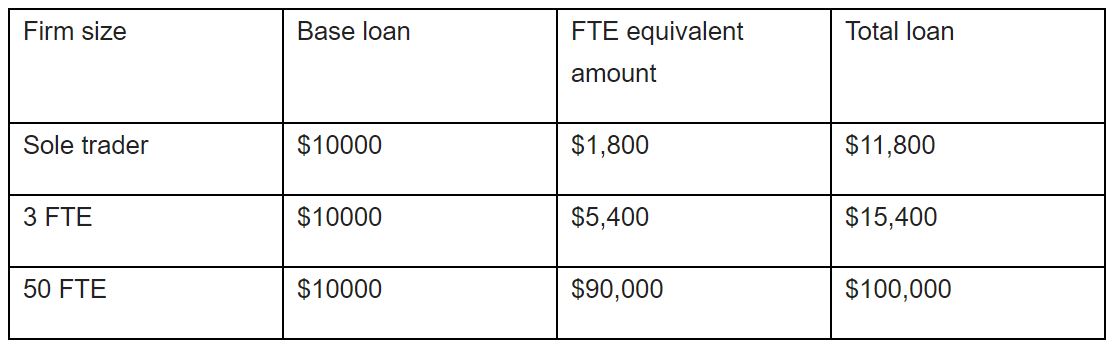

Providing more detail on Friday, the Government said it will loan firms $10,000 each. The size of these loans can be extended by $1800 for every full-time employee the firm has. Here’s an example of what this will look like:

The loans will be interest free if they are repaid within a year.

Thereafter an interest rate of 3% will be charged for a maximum term of five years. Repayments won’t be required for the first two years.

The Inland Revenue will start taking applications on May 12. At this stage, it will only take applications for a month. This window will be reviewed.

The loans can be used for core business operating costs (including, but not limited to, rent, insurance, utilities, supplier payments, or rates), and will be available to any ongoing business with the purpose of supporting it to remain a going concern.

The benefit of the loan cannot be passed through to the shareholders or owners of the business, for example, by a dividend or a loan to the shareholders or owner.

Businesses will have to declare they are "viable", use the money for core business operating costs and enter into a legally binding loan contract.

Asked by interest.co.nz how the Inland Revenue will assess credit risk, Finance Minister Grant Robertson noted that Inland Revenue already has a lot of information about businesses, making it well-placed to do these assessments.

He said borrowers will be audited and the Inland Revenue will be given more resource as it takes on this new task.

Robertson couldn't put a figure on the value of loans he expected businesses to take up.

This scheme is distinct from the Business Finance Guarantee Scheme, through which taxpayers are underwriting 80% of individual bank loans to eligible SMEs.

Robertson said it was necessary for the Government to write businesses loans directly, in addition to underwriting bank loans, as the latter isn't meeting businesses' needs nor the Government's expectations.

He is changing the rules around the Business Finance Guarantee Scheme so more businesses are eligible. Banks can now lend to agricultural businesses under the scheme and can provide unsecured loans. For more information, see this story.

Robertson said: “We are targeting this [Small Business Cashflow Loan] scheme to those who have a viable business but have been put in a position of not generating any revenue. These kinds of terms are not available anywhere else.

“We are committed to sharing the burden of the impacts of COVID 19. As a responsible Government we must ensure we are using taxpayer money carefully as we provide support for business."

151 Comments

This might help a bit, but only around the margins...

Better than nothing, though.

With the details released it now looks like a political headline rather than any genuine large loans to businesses.

As you allude to say with 50FTE, 100k might cover 6 weeks wages. It's not going to prevent anyone from going under, it may just postpone the inevitable for a short while.

It could prevent some going under. But agree not many

With the details released...... after the legislation was passed..

New Zealand's Parliament is famous for being able to pass laws quickly in a crisis.

But on Thursday it might have moved too quickly, after an error meant that the wrong piece of legislation was introduced to Parliament and then passed within hours, accidentally bringing into law a multi-billion dollar loan scheme.

https://i.stuff.co.nz/national/300002365/parliament-passes-the-wrong-la…

Draw your own conclusions.

How do you work out $100000 covering for 6 weeks wages @$1800 per employee for 50 Full Time Employee, after tax, acc, kiwi saver etc that would not cover 2 weeks, (it would work if you paid $7.50 gross per hour). A sole trader has a fighting chance to make the $11800 work. If they offered loans at an extra $10,000 per 5 employees that would put companies in a far stronger position.

Funding people who can't repay is not 'better than nothing'. It's just a terrible idea.

We as taxpayers are unaccustomed to getting a return on our investment, nor expecting to ever see our taxes again, so par for the course really. I hope it helps at least one business. Maybe the govt could reduce the tax burden on businesses to make them more profitable, say - no business tax for one year. But how shall the ever-compassionate clique of socialist overlords ever survive without the limelight upon them for an extended period of time showing us just how full of care and worry they are for us. No, rather tax us, to the point businesses become unprofitable, then use those taxes to bail us out because we are unprofitable. Brilliant scheme. Job security for bureaucrats. Hooray!

"tax us, to the point businesses become unprofitable" - I'm pretty sure the current economic downturn is due to this thing called COVID-19 (you may have heard of it), not taxes.

i think most tax payers work for companies with 50 FTE or less anyway and if it slows the inevitable of going down a % of those employees could and will end up on unemployment benefits anyway which the remaining tax payers will still have to pay for, even if it may just slow the domino effect, extending more time to a company the better chance it has to not continue a domino and turn things around.

So does the margin include say uber or google or any of the big overseas owned companies with hardly any employees in NZ? is there a turnover reqiurement as well?

“It has become clear that the support that is available to our small and medium businesses from banks is not meeting their needs nor our expectations..."

Banks typically have the very unreasonable expectation they get their investors money back. I know that's a difficult concept for a politician to grasp but I think your about to learn that shoddily lending money is a very easy way to squander billions like clicking your fingers. I've stated that this is not an appropriate activity for government and only hope they reach the same realisation rapidly.

"Banks typically have the very unreasonable expectation they get their investors money back."

Govt has no such restriction. The taxpayer is a bottomless money pit, no issues there if we squander a few $100k here or there.

Agreed, in fact early on the Government said they would shoulder 80% of the risk, and the banks still didn't step up.

You keep using the phrase "banks didn't step up". There are two problems with this line of thinking:

1. The bank work under a regulatory framework the government made.

Unlike a government, a bank cannot lend to just anybody, anything at anytime. A bank is accountable to both shareholders and regulators. So they do exactly what they are allowed to do and no more. A bank has annoying realities like loan and capital ratios.

2. The phrase is code for 'what I want them to do'.

Banks are not politicians. If your business is not likely to be able to repay a loan they won't lend to you. When a bank doesn't 'step up' your business is probably is dire straits. Governments, by contrast, can loan to bankrupt companies and are accountable to nobody.

This is a local repeat of the US government policies that led to the GFC and when it explodes in bad debts from companies who never had the ability to repay those loans the tax payer will wear the cost.

Have you ever applied for a business loan to a bank , that didn't involve property?

They don't just want ther money back , they want a cast iron guarantee and still sting you a higher interest rate. Most small business loans are backed up by the owners house, if you've got no property forget it .

Want to borrow money to buy propertry , well , how much , why not go for more? They are more likely to reject you for not been ambitious enough .

So, so true - my experience as a small business owner as well. Banks bend over backwards to service the rentier/property class - but the productive class, they are plain and simply miserable/awful/horrible to deal with.

Good on the government for being prepared to say that about the banks up front. This government is learning really quickly that banks have absolutely no concerns for the well-being of society whatsoever.

"bend over backwards to service the rentier/property class"

In truth it's ANY asset class that gives certainty the loan is likely to be repaid, although property certainly fits that bill and Kiwi's love there property so it's very popular.

NZ property is an incredibly obvious bubble, thanks to bank policies. It works great until it doesn't. There is no "certainty the loan is going to be repaid," they have just grossly mispriced the risk. There is a very low default rate *as long as house prices are rising.* In fact this dynamic ensures that over a long enough timeline, a point will come where much of the debt cannot possibly be repaid.

"banks have absolutely no concerns for the well-being of society whatsoever."

They act as if they are not the social welfare department. Although I believe they have similar levels of social responsibility performance as other businesses in NZ.

If you where lending your own money would you not do the exact same thing? Every dollar a bank has belongs to somebody be that an insurance company waiting for a large event, a pensioners retirement, a childs university fund or someones dream car.

To your first question, and in the interest of full disclosure, I worked in finance for many years.

I noticed you didn't include bank shareholders in your list.

According to the Reserve Bank, the new capital requirements mean banks will need to contribute $12 of their shareholders' money for every $100 of lending up from $8 now, with depositors and creditors providing the rest. Link

I worked in finance at one stage. Our job was to use our clients to benefit our shareholders. And to comply with government laws. Not recommendations and requests, but laws. Only people in dreamland would think it possible for a public company to be "socially responsible" in a manner that is going to cost the shareholders money, and only to comply with one of the above requests or recommendations. That's why we have laws. We know where we stand, and we know our competitors have to pay the same costs of operation as we do. If the government doesn't like what we do they make a law against it. Think LVR. No request, just law.

"I worked in finance at one stage. Our job was to use our clients to benefit our shareholders."

Just to put your comment in some context, what area in finance specifically?

Take a look at the banks accounts squishy. Unless the money is secured somehow with the bank, it belongs to the bank! Not a depositor, pension fund or some other entity. It is the bank's. They're just too short sighted. I agree that they needed to take some care, but with the Government saying they'll shoulder 80% of the risk, the banks then needed to step up. They didn't!

They did EXACTLY what the government regulations allowed them to do.

Loaning money to people who cannot repay it is not "stepping up".

Nor is lending to companies under the same premise really. When you've invested a lot of time and effort in something it's human inclination to hang on beyond all rational judgement. When a bank declines a loan they are doing so with knowledge and experience about the probability of the outcome of your business.

By extending lending outside those parameters we are also extending a false sense of hope to many and guaranteeing destruction. It is no different to Frédéric Bastiats parable about broken windows really, society destroys what it finds to be valueless. That's the sober reality of all of this, people could have started over but will instead cling onto false hope. Delaying "Creative destruction" as Ben Bernanke put it.

Which is yet another reason we need a tax system designed to penalise non productive assets "businesses" and grow productive business. We needed it 3 decades ago, better late than never?

No. You miss the point of taxation. It only exists to extract money to pay government costs. Nothing else. Not all income, or everyone's income needs to be taxed to pay these costs. Making taxation more and more complicated and silly means more opportunities for tax minimisation, avoidance and evasion.

I do "these loans" on the daily, and its generally not the business owner or the banks fault as much as the accountants.

How do I keep customers? Drive down taxable income at all costs!

The amount of times I've seen sneaky expenses or had to explain drawings isn't income is disgusting.

Yes, know exactly what you mean.

“It has become clear that the support that is available to our small and medium businesses from banks is not meeting their needs nor our expectations as a Government,” Finance Minister Grant Robertson said.

Well, for once i think the banks are being smart.

Now the government is issuing junk loans that the banks won't even touch, god help us. They are simply not a commercially-minded lender. This will be massive waste (encouraging everyone to just grab the money and punt), ending up as a liability for future taxpayers. I also expect the government will be far less rigorous in collecting debts than the private sector too.

"Well, for once i think the banks are being smart." So you think the banks are right to essentially drive and support a collapse of the economy through SME failure? Such an attitude is both short sighted and would, long term, shoot themselves in the foot.

Murray - the 'economy' was going to collapse, without the virus.

And both banks and Govt have the same problem in a powerdown world - less and less underwrite (physical, as in real) going forward. Only a fool would issue more debt at a time when the current crop of it was unrepayable. This is nonsense - extend and pretend nonsense.

Banks assess risk. The government regulation make them do it.

Why loan money to people who can't repay it?

Being responsible with other peoples money is not driving the collapse of anything.

Banks are f-ing terrible at assessing risk over the long run. See: GFC in rest of world, current bubbles in Aus/NZ.

Show them(Bank) the carrot (House) and see how they go out of their way as long as, have decent equity locked in the house.

Makes sense, easy to liquidate and people are very committed to retaining a roof over their heads.

Grant is talking like someone who knows a thing or two about getting other people's money, and not having a show of paying it back.

Another useless bit of PR rubbish . One sole trader could have had a business with a turn over of $300K p.a.but now at zero. What can he do with $11,800? Go to Antoines for a great one off meal with a top wine then starve the other 364 days in the year.

exactly...they are just trying to spread out the unemployment numbers across 5 months instead of 3. Meanwhile nothing meaningful has come out from the government to help create jobs or stimulate the economy to get some confidence back. Just cheap loans and welfare. Business need to create/maintain turnover Grant in order to pay debt...not load up on more debt to pay debt.

This government is not interested in HOW businesses operate to create profit and jobs. They are only interested in being seen to be doing something FOR businesses in a slightly patronising way which you can get away with when your salary is from the taxpayer and who you're lending to is at the mercy of real world conditions that drive business fluctuations. "Oh you poor businesses who don't have your snout to the spigot of taxpayer money which we extorted off the productive capacity of NZers, poor you, here have some of it, interest free, we're really benevolent up here." Good luck with that.

Haha, too right. Well, they way the wheels are coming off this economy, someone is going to have to get a handle on how profits are made quite quickly. I’m not sure they actually care !

Why does it not surprise me that a property leech doesn't know what a productive entrepreneurial type can achieve with $11,800.

Seems like a good idea. I mean why not - may as well if we're going to try and keep businesses and employment opportunities afloat with wage subsidies, do something like this as well. Not a big amount, but if it helps a few businesses survive I support this initiative.

Just so long as the government and tax-payer do not expect to see that money back.

If we didn't expect the money back it'd be called a "subsidy" and not a "loan". We should expect every penny to be repaid and keep a close eye on arrears, defaults etc.

It's a bad idea for a number of reasons.

1. It destroys the pricing of risk in the marketplace.

If it's 3% for any business regardless of its ability (or probability) to repay then risk management has left the building. This is what fuelled in the GFC.

2. The IRD doesn't have the skills, process, systems and staff to run a retail bank.

Without these the level of practical control must be extremely low until they are all created. That will take years.

3. If you can't get a loan from a bank you are probably a high risk, why should tax payer underwrite you?

This will socialise the losses to the tax payer, who could extremely angry when they pour in.

4. If the IRD doesn't have a banking license so there is zero governance or accountability.

This is a huge problem, creating a situation where vast amounts of tax payers funds are poured into a system without effective governance. If banks don't need such governance then why was it created?

5. Where are the cross checks to stop political pressure for loans to particular businesses?

If you remove risk analysis as the basis of who should qualify for a loan, and at what rate - what is left is 'who you know' and in combination with a zero governance model is a recipe for crony politics and corruption the like of which NZ has rarely seen.

If it weren't for your beloved banks being disgustingly incompetent at risk management and driving massive amounts of unproductive malinvestment, we wouldn't be in this mess.

I suspect this is really seen internally as semi-stimulus, they just don't want to call it that.

No, no and no

Election year. Money for jam.

Looking at it further, a small SME with 50 staff gets $2K per person.

Just enough for one cup of tea and two biscuits per employee per year.

Milk and sugar extra.

You completely misunderstand it. The loan is to meet cash flow commitments (fixed costs) during the period of disruption (i.e., lock down and/or transition from lock down). Fixed costs of concern to most small businesses being commercial rent, insurances, power connections, communications services, etc. They were quite content with the wage subsidy scheme for their employees. You'd have understood this had you listened to the five small business owners that were interviewed by the select committee on Monday this week.

This is perfect for them. If paid back in the first year - it's interest free - and they don't have to take a new or increased lien on their homes to make it happen. Once many are open again, they will easily be able to do repay inside a year, according to those interviewed in select committee.

Cynicism without understanding is pretty awful at this time, BD.

I agree Kate. I think some of the criticism is over the top.

As I said though, it's going to have limited benefit. But it will have some.

Finally, amidst of too embarrassment of keep propping up F.I.RE production by govt,banks & RBNZ? on their initial Covid19 responses (removed FHB deposit, LVR, reduce OCR, No TD guarantee, NO CAR, wages subsidy straight for landlords,banks etc) - something to prop another side of real job/business productivity. After week from this announcement?, soon will be back again to stabilise the RE by next memo;.. a guaranteed income for private/commercial landlords (despite 70-80% stellar return the past 10 years)..by more tax payers hand out. - C'mon Neoliberal is that all you knew?

Could be quite handy with the right business. Invest $100k in new high efficiency equipment or staff training? Imagine how useful this would have been in the months post gfc....could have saved a lot of businesses.

It could be quite handy for ANY business.

Who doesn't want cheap money without risk premium, especially people who might not be able to repay it. It's what created the GFC.

They are flying by the seat of their pants and making idiotic decisions, which seem to be getting sillier by the day and are starting to show signs of major panic. I'm guessing the smarter ones in govt (and I'm using the term "smart" with some abandon) are probably beginning to realise that unemployment will be >20% come election time and they need to engage in some serious central planning a la Soviet Union-style to try and save their careers... oops, I mean the economy. It won't work, as any rational business owner will be looking to cut overheads and get rid of debt, not increase it! However, as a mechanism to throw away tax payer money down the drain, then of course it will work a treat.

I would be inclined to agree except there is no announcements of any stimulation measures for household spending. Ultimately, without an increase in consumption and associated cashflow, debt will become a noose.

And all those businesses who could not get a loan from a bank, because there is an insufficient probability it can be paid back, can get cheap money from the tax payer with zero risk premium.

The destruction of risk management, all under written by the lucky tax payer.

It's like watching the GFC process all over again.

What do all you armchair Austrians do for a living? Seems like all you can do is repeat talking points that have no application to the specifics of what is happening right now.

So do I borrow 100k with my staff of 50 employees, try to recoup or maintain my T/O in a low confidence, or destroyed market (for at least 18 months), help pay my O/heads. Or do I tread water and go into cost cutting mode and shed 15 % of workforce and reduce my OHeads by 450k a year? it aint going to stop the flow of redundancies.

Its like putting a band aid on a cut artery.....

I agree FCM - I think they're just trying to prevent a spike in unemployment like they've got in the states. I looks like up to 50 million unemployed over there the last 4-5 weeks (like 20-30% of their labour force). Guess they're hoping to make it a more gentle ride towards hell.

Gee, they do seem to be regulating and targeting these initiatives where needed. Excellent governance.

Kate, lift it eh?

This isn't 'excellent governance'.

This is 'trying to restart unsustainability 101'.

After all this time, I'm not sure you get where we are. Physics trumps emotion, every time. And physics-wise, we were in terminal. near-term trouble BEFORE this. This was the opportunity fo a re-book, no a restart.

https://www.newsroom.co.nz/2020/05/01/1151416/six-new-approaches-in-a-w…

pdk, as I explained to Big Daddy above - I get my impression from having listened to the business owners brought in by the Select Committee on Monday this week;

https://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=12327901

These are small businesses servicing a lcoal/community marketplace. And you yourself have spoken about our need to re-focus on the local. These are not the Kmarts and McDonalds' and Progressive Enterprises.

Supporting them through this is all a part of that re-start. Destroy local commerce and all you have left are multi-nationals.

PS did you know my Dad was a physicist? I answered that point you always make on another thread recently.

Unless the IRD is made to apply for a banking license and abides by the same banking regulations as all other banks -- then they aren't regulating at all.

And if the IRD has no banking license then the government is creating a bank -- without effect governance.

It would be hard to do a worse job than the commercial banks have done with all this "effective governance."

Grant said in the presser. 400000 eligible businesses. Even at only 10k each. That is 4 billion !!! If only half of them claim for 2 employees minimum that is another 720 million!! Let's just call it 5 billion minimum. Is that the best way to spend 5 billion. Half of that will be written off. Why not feed it in from the bottom. A billion a month via payments to the people in the first 2 months of level 2. To spend into the economy and give it a kick start. The money finds its way to businesses that the people value and want to see survive.

That will happen too, but the businesses need to still be alive by the time Level 2 happens.

You and I are thinking alike. I'm guessing it will come with the budget.

I suspect we are amongst a handful on here who have direct real-time experience of what's happening in the small business community. Seems to be a lot of bulldogs on here who just come on looking for another reason to bark at Jacinda.

Hi, most, perhaps more than 95% of commenters here seem to not own a business that makes something. And as a tradesman with a factory that makes something out of timber, I always have to laugh when i read of banks, or insurance companies talking about their “products”... Just goes to show how far removed a large chunk of society has become from daily real life that involves physically making something useful. And that shows clearly in how far heads are in the clouds, or sometimes in the sand, lol.

So you dont think that blind and unthinking allegiance is also a problem

FM also stated that they understand many may not be able to pay in future so everyone should go for it as government is not expecting to be repaid.

Banks are not doing their job as expected...OBVIOUSLY...Banks are more interested in housing ponzi as more lucrative to them so.........

The aussie banks preference for housing over lending to productive enterprise/SMEs is the root cause of NZ and Australia's slow motion debt crash. We need to review their social licence to create credit with keystrokes. This is an important move by the govt - clearly opposed by the bank's spin machine. We need more interest free loans for nz business of a far greater scale.. Inflate the debt millstone away!

Indeed - Why the banks just want our houses

Agree - freedom to innovate.

It was in our elected representatives power at any time to readjust the lending window of banks into more productive sectors of the economy, but everyone was too interested in making capital gains on their property. In that alone, I hope it all tanks. And then, the productive entrepreneurs will be appreciated when they slowly build up wealth again.... under the loving whips of our Chinese masters.

Glad to see this later support is being delivered via the correct agency IR and not msd. IR have very good systems, data and records so at least there is some comfort the record keeping will be correct and these loans tracked (whereas any wage subsidy issues will just be dropped into the massive debt beneficiary debt bucket that is effectively unrecoverable)

What make you think the IRD have the staff, systems, processes and skills to run a retail bank?

....ummmmm maybe their track record. One of the most effective tax systems in the world operated right here by IR. Piece of cake for them to track this. And not a cent of gong to an Aussie mother bank.

That enough for Ye?

No.

Their record is in taxation when what is required is a retail banking. To suggest they are the same is hopelessly naive.

The chances any bank that loans money to people without regard to risk is going to make a profit is extremely low.

You’re overthinking it Ralphy. The loans will just sit on the taxpayer IR account like due tax does (or student loan, fam support etc) They may kick in the interest or they may (more likely) just right it off.

Quite within their competence.

There are only two choices here. Either the IRD will apply for a banking license and be subject to the same level of regulatory oversight as all banks or they won't.

If they are granted a banking license, then given the depth and breadth of the regulations, the chances they have the staff, skills, processes and systems in place are zero.

If they do not obtain a banking license the tax payer will a underwrite vast loan portfolio without effective governance (they could simply do something like what you suggest).

I suspect there will be no banking license, no effective governance and no risk management. The fruit of which will be a GFC style bad debt implosion somewhere in the future the tax payer will fund.

"The fruit of which will be a GFC style bad debt implosion somewhere in the future the tax payer will fund."

That is what we're already in for because your supposedly messianic banking sector risk management is anything but. This is the *response* to the mess YOU CREATED.

Sounds like you are in the employ of a bank financed organisation...? I have to tell you that my dealings with IR over the many years i have been in business has been one of surprising level of professionalism and trust in chartered accountants being generally pretty straight laced and obliging with the IR rules. The banks on the other hand are simply parasites in large part on the economy. The very small amount they lend based on security other than residential property, is laughable. [ Insult unnecessary. Don't do it. Stick to the issue. Ed ]

Terrible idea, loans that are too risky for banks are now being done by the government and guaranteed by Joe Worker.

Taxpayer dollars aren't real money. By the time those loans default the government will be into its next term. Still, we can tax the remaining businesses at twice the previous rate and recover the money lost I suppose.

Not real until your taxes really go up.

Because the loans are made without regard to risk numbers of them will never be repaid. Just like mortgages were defaulted on in the GFC.

What is the interest rate for these loans?

Pretty sure i heard 3%.

So if that's better than all other banks I guess tax payers will be very well abused.

3% but don't have to pay anything for the first two years.

Will the interest go up based on how likely a business is to be able to repay the loan or is it just a fixed number plucked out of 'no-risk' land?

interest free for the first year... its in the 'breaking news' banner at the top of the page

How about giving money (capital) to people wanting to START a business? Some will fail, some would become big drivers of the NZ economy.

Can't these fools see that old businesses aren't dynamic enough, too top heavy and are just tacking on an app here and there.

Entrepreneurs are chomping-at-the-bit to replace, erase, disgrace and displace them. Yet the capital investment taps have been wielded shut for years.

"Long Live our the Zombie companies !!" cry boardrooms throughout NZ.

"How about giving money (capital) to people wanting to START a business?" Nothing stopping you from becoming a VC if you have an eye for future success. Your money is at risk but the rewards are all yours.

If the government is propping up your competitor with tax payers money, you would have to be quite silly to compete wth that.

You could only get money at a price based on a an actual risk analysis. In contrast, your competitor gets 3% regardless of risk or probability to default.

Many of those would-be entrepreneurs are millenials with student debt and the massive drag of having to save a gigantic deposit or service a gigantic mortgage. I have plenty of friends who would make great entrepreneurs but the risk of failure is simply much too high. To have a thriving entrepreneurial culture you need to be able to try and fail without basically destroying your life. This entrepreneurial revolution can't and won't happen until the property speculator culture is dead and buried. There is a lot of creative potential there waiting to be unlocked, but there's a lot of pain to be swallowed before we get to that point.

Will the IRD have to apply for banking license?

Will they abide by the same banking regulations as all other banks?

Has anyone kept a running total of all the money the Govt has puked out over the economy? 12 week wage subsidy, up to $100k for 400,000 businesses, taxpayer guaranteed bank loans, doubling winter energy payments, have I missed anything? What is the butchers bill going to be when we add all this up?

It will never be repaid.

Even before, it was never going to be repaid.

The question therefore is: What will money be 'worth' post hock (sorry it wasn't a proper hoc :)

its being funded by QE, does not need repaying

https://www.rbnz.govt.nz/news/2020/03/rbnz-to-implement-30bn-large-scal…

What was the butchers bill going to be if they didn't do it? A dead economy and half the population on welfare? This loan idea seems completely daft, but the rest of it is somewhat understandable at least.

Is this the Jacinda Put?

Nothing like enough to promote growth - probably enough to keep a couple of marginal companies going, that probably really shouldn't survive.

But for my company that is looking to expand with new automation for low cost housing, we could do with the same but up to $500,000 - with some more restrictions, such as higher turnover, in business 10+ years, and very low existing borrowing.

Sounds like you might be best looking for an equity investor, as opposed to a loan?

A reasonable proportion of bank deposits come from "little old ladies term deposits..."

They want them back..... funny that banks have to be quite careful when lending margins are small with a low OCR. There is simply no point doing unsecured lending to small under-capitalised tourism businesses here..... if the business had no or low risk the owner would have no issues using their home as security!

Going into this crisis most small business where already heavily in debt due to the amazing Rock Star Economy and record tourist numbers.

In life no one owes you a loan....

Remember a loan from family tends to occur after the bank has said no.

Family don't want to have those difficult questions about "security".

People seem to have the idea banks say no to spite them.

But governance and accountability matter in the end, unless you want to create another GFC by destroying risk management.

The regulators have made it IMPOSSIBLE for banks to do non-responsible lending, including to businesses that are about to fall over in the middle of a Pandemic.....

You got what you asked for.....

Just thinking and just throwing some maths around to ponder.

For a short-term struggling company affected by Covid-19, the government options seem:

- Either, Interest free loan of $100,000 to a SME for a year with 50FTE and hopefully paid back.

- Or, the 50 FTE on unemployment benefits for a year, (married not counting kids 52weeks X $407.67pw) is $21,000 pp or $105,000 in total and definitely not paid back.

Me thinks there may be very good financial advantage - as well as lots and lots of social advantages - to offer the $1000,000 which at least some is hopefully going to be paid back.

"and hopefully paid back"

But the IRD doesn't have retail banking risk assessment processes, skills or systems to know whether it is likely to be paid back. They have your tax records I suppose, but that not the same thing is it.

And in the end, if the business was not viable it will be back for another loan later. If you don't grant that loan then your 50 FTE are unemployed anyway. Just a timing issue.

Ralph: "Businesses will have to declare they are viable". IRD have grounds to come back at owners if company proves not to be viable.

Personally I would rather see the 50FTE in employment for the year if possible - surely you have some empathy for them.

Given its illegal for a company to trade when insolvent then insisting on a business having to declare its viable is a bit meaningless.

Personally I like the jobkeeper scheme in Australia, pay the company to pay staff. Ultimately something similar in NZ would likely cost less than the losses from giving money to businesses the banks have already said are not viable.

no trading while insolvent rules have had a recent change..... less director responsibility now

Yes, the Australian business support has been much much better than the NZ.

Simpler, tax free and larger.

Finally you say something I can agree with. This money is getting injected one way or the other, whether as "loans" or as stimulus or as welfare, it's not going to not be injected. Everyone whining about this seems to have no real pulse of what is happening in the small business world and the true size of the hole.

One tiny detail, if a business goes broke the IRD always have first bite of the remaining asset sales......... and the IRD are looking after the scheme

Another good point, do the IRD even have a bankruptcy management department?

Ralph, Ralph . . . .

Where have you been hiding all your life???????

IRD are probably the leading instigators of bankruptcies in New Zealand - always have and likely always will be.

Probably or actually?

On what scale?

Or do they in fact relay on the accounting profession and have only narrow interest in the taxation side?

Actually. Without any doubt the IRD would feature in the vast majority of all bankruptcies. They are often the instigator of bankruptcy proceedings, and very commonly listed as an interested party in proceedings.

Instigator can mean little more than who called in the receiver.

That involves none of the leg work.

Ralph - you are making it clear you don't understand what nice chaps and lasses the IRD are.... in normal times...

Its normally over failure to pay GST.... once they start proceedings the law says they get paid first

and they will chase directors current account that are over drawn to hell and back.....

though often they are simply removing scum from the business pool, who never take drawings and

simply run up huge current acc drawings for which no tax has been paid

then shut things down - this happens more then you would think.

You may have heard that joke

"Researchers have recently started using lawyers instead of rats in their lab experiments.

You don’t get so attached to them, and there are some things a rat just won’t do."

If you have issues with the lawyers you can always use Liquidators..... there is NOTHING they will not do. The more you experience them, the less chance of any emotional attachment.

Yes, but none of that involves any of the skills of execution. They aren't the receiver.

I guess they can continue to outsource receiverships to the accounting industry. That is at least scalable.

But is that all a retail bank does?

Download a NZ based banks recent full year balance sheet / accounts and take a look at divisional earnings......

there is some complexity to these businesses....

Ralph

Are you serious?

IRD initiate more bankruptcies than anyone. Get behind in tax payments, horrific penalty interest rates, and then they will bankrupt you without hardly blinking.

They used to say “Its our job to be fair” - it should have been “feared”. Ask that guy Henderson (book and film about his experiences) - he tried to take them on but I think bankrupted him three times.

Naive to suggest that IRD have no experience in instigating bankruptcies.

And just to be clear they employ a large number of lawyers and accountants specializing in bankruptcies within their IRD team. Don't think "do they have a bankruptcy management department?. . . . rather "just how very huge is their bankruptcy management department?"

Why do you suppose receivers exist?

What do you think they do for a living?

Ralph

Receivers are appointed by the courts to carry out the job of winding up the company (including selling assets and distributing any monies) once bankruptcy has be declared.

Your 3.55pm comment shows you very confused regarding bankruptcies and receivers.

"Receivers are appointed by the courts to carry out the job of winding up the company"

Exactly. NOT the IRD.

yea.. was my first thought.. does this loan rank pari passu with other existing debt?

it will rank as IRD debt IMHO

the worst kind

ranks after secured debt with mortgage or lien on assets tho ie much bank debt 8)

it helps if you have been playing this game for hundreds of years.

the patsy always gets screwed

Thinking about it, I should apply. Who doesn't want $100,000 interest free for a year.

Perhaps I should buy bitcoin.

Oil is one of the most liquid markets... what could possibly go wrong?

Maybe just park it in USD as a risk hedge?

Oh sorry it's only for business people, not bank employees.

Draw down. Buy crypto. NZ dollar is fucked thanks to Adrian Orr. Hodl. Profit in 12 months.

If our dollar is going to plummet then any export or tourism business is going to boom over the next few years. Any debt any of us owe to an Aussie bank can be paid back in a few years with the new value dollars. We all did it in the eighties. Good times.

We are going to be poor, when buying anything from overseas. Say goodbye to cheaper electronics, and inflation could rise as a result. Also rising building cost for imported materials, cars, fuel the list goes on. It isn't good. Maybe we should merge economies with Australia, seeing some politicians and business folk are so keen to go into a bubble with Oz, and become an independent state?

I do believe Labour will get another term and I really hope they will. They have to clean up (yeah right) the mess they are creating now.

I really wonder what National would have done. If we had gone down the route of UK, we could be an a far far worse position than we are now, with risks of rolling lockdowns for over a year to 'flatten the curve', so the health system can cope, with 8+ waves of the virus. Based on how many tourists we have had come in earlier in the year, and all the expats returning, we are lucky that we didn't get more cases and getting it spreading more.

"money for nothing and the chicks for free" U2

Dire Straits.

Do not think they will make great effort to get our money back. A quiet writeoff to avoid politcal fuss is more likely. Look at student loan writeoffs.

Madness. We gave Labour Party the Government chequebook and they went berserk. How are we going to explain this to our grandchildren.

The "Beloved leader" Ardern has led us over a cliff, like lemmngs.

Taxpayers cannot and do not fund anything. The government creates our currency, taxes when returned to the government are deleted the money ceases to exist. We spend government money, it doesn't spend ours as counterfeiting money is illegal.

The majority of commentators seem to believe people in business have limited mental capacity to calculate the risk of taking on debt in a downturn and that this will be a mad dash to take on debt. I would hope naivety of our current financial situation is limited to the minority.

97% of our workforce is made up of business with less than 20 FTE, and they produce around 30% of GDP.

If we must take on some shared risk as taxpayers to keep our economy as we know it as functional as possible, then I’m ok with that. I’d rather viable (strong emphasis on viable) businesses risk repaying a tax-free loan to cover short term cash flow issues vs failing and seeing many tens of thousands in the dole queue with a very immediate and potentially higher long term cost to the working taxpayer.

Hopefully we don’t end up kicking the can down the road with both loan defaults and unemployment, but the onus is now on the IRD to make sensible decisions on who to loan to. I think we have to put some trust in them as we need immediate solutions in conjunction with the medium/longer term infrastructure type solutions for the proverbial "shovel" ready activities.

Source: https://www.mbie.govt.nz/assets/30e852cf56/small-business-factsheet-201…

In some cases this will be a life ring/raft saviour that will help support some small yet viable businesses through the coming storm, for others it will become an anchor which will eventually hold them back from sailing through the storm and drag them down resulting in termination of the business. Small business owners would be wise to assess whether they want to cut loose now or batten down the hatches for what looks like bigger weather looming on the distant event horizon. This reminds one of the DFC days in the late 1980's and early 1990's...

Just read the conditions , if you owe IRD money during the loan term, the interest free ends , and the rate becomes 3 % plus IRD's penalty rate , for the entire amount / term .

Just the thing a business in trouble needs.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.