Here are the key things you need to know before you leave work today.

MORTGAGE RATE CHANGES

ASB is the latest to raise fixed home loan rates. More here.

TERM DEPOSIT RATE CHANGES

BNZ and ASB raised term deposit rates today. We assess their 'fairness' here. Nelson Building Society also raised their TD rates.

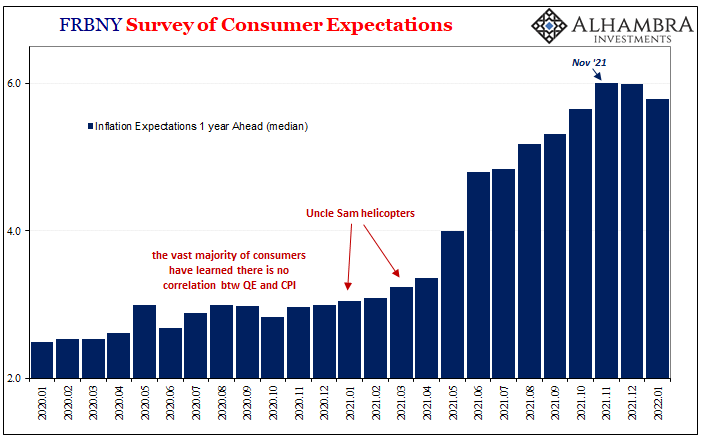

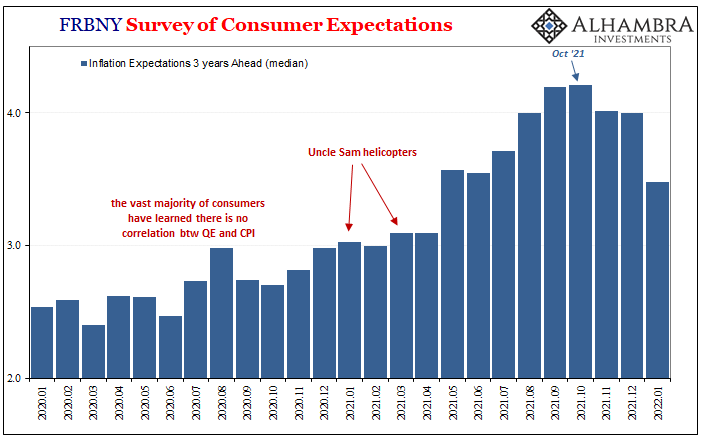

RISING INFLATION EXPECTATIONS

The RBNZ has revised its household expectations survey (M13) to bring it up to 'best practice' and match how other central banks are surveying this same data. It means most of the changes reported today have a different base to prior reports, although they advise the 1 year expectation is still comparable. Those surveyed say that current inflation is running at 3.7% (actually its 5.9%, so financial understanding is not flash). These same people say in one year it will rise to 4.5% and in five years it will rise to 5.6%. Expectations - even from this surveyed cohort of unknowledgeable people - is that we face rising inflation.

KEEPING SUPPLY CHAIN OPERATORS HONEST

An international task force ("working group") has been established to identify potential cartel conduct in global supply chains. This group includes our Commerce Commission, the Australian Competition and Consumer Commission, the Canadian Competition Bureau, the United Kingdom Competition and Markets Authority and the United States Department of Justice Antitrust Division. The group will share intelligence and use existing international cooperation tools to help detect and investigate potential cartel conduct arising from disruption in global supply chains, they say.

EXTRA MONEY ON THE MORTGAGE?

Westpac claims its data shows that a majority of Kiwi households with mortgages are financially better positioned than a year ago to cope with the twin strains of Omicron and rising interest rates. 68.1% of Westpac’s home loan customers were ahead on mortgage repayments by at least 3 months, at the end of 2021, a jump from 65.9% at the end of 2020. Those customers were ahead of their scheduled mortgage payments by a median amount of $11,022 or 10.5 months – up from $9,657 and 9.0 months at the same time in 2020.

COSTS RISE AT THEIR FASTEST RATE IN 20 YEARS

Producer prices moved up sharply in December, according to the data released today. Input costs were up more than +8% on a yea-on-year basis. Output prices were up +7.2% on the same basis, so firms aren't able to pass on all they are being hit with. But so far, there in no suggestion this is an intractable problem. However, the cost of new capital goods are rising very much faster, up +9.2% year-on-year and their fastest rise since this series was started in 2002.

BUSINESS OVERHEAD COSTS MIXED

Away from direct costs, business overhead costs are generally rising faster too. Commercial rents are up +6.5% from the same period a year ago. Gas is up an eye-watering +27%, road freight up +7.3%. There were some surprises in this data too - sea freight was up just +1.4% (you wonder what they are counting here), and electricity costs fell sharply after big rises earlier in the year.

FARM COSTS UP SHARPLY TOO

On the farm, input costs are all up, led by fertiliser which was up +47% in a year. All other costs increases averaged +7.2%, with dairy farm costs leading the way with a +7.9% rise, and the smallest was for horticulture but still up +5.8% in a year.

MEMORY PROBLEMS SPREAD

In other media, there has been considerable publicity about the rise of second tier lenders to finance property development. Many are raising funds from the public via special funding vehicles like syndications, capital ventures, and the like. All are targeting "wholesale investors" who are presumed to know what they are doing. Many of those seem to have very short memories, chasing yield, 'buying' the promoters marketing, and ignoring the liquidity risk. Memories are short because it was these same liquidity risks that came home to roost when most of the finance companies went belly-up. Many promoters went to jail. Investors lost most of their capital. That 2006-2012 finance company crisis was mostly about non-bank lenders sourcing public funding for property development. (This is one reason you won't see many ads for modern day capital raising for property development on interest.co.nz.)

CORPORATE BOND PRICED

The Investore (IPL, #37) bond raised the full $125 mln, and will pay an interest rate of 4.00%, the company has advised. It was at the upper end because the 5 year swap are is rising.

LOCAL PANDEMIC UPDATE

In NSW, there has been 9,243 new community cases reported yesterday, now with 109,524 active locally-acquired cases, and another 15 daily deaths. There are now 1,381 in hospital there and continuing to fall away. In Victoria they reported 6,935 more new infections yesterday. There are now 48,852 active cases in that state - but there were 14 deaths there. Queensland is reporting 5,795 new cases and 9 more deaths. In South Australia, new cases have fallen to 1440 yesterday and 3 more deaths. The ACT has 561 new cases and one death, and Tasmania 623 new cases and no deaths. Overall in Australia, more than 24,500 new cases have been reported so far although not all counts are in yet. In New Zealand, there were 18 cases stopped at the border, plus 1929 new cases reported in the community, another new record.

GOLD UP FURTHER

In early Asian trading, gold is now at US$1894 and up +US$24 from this time yesterday.

EQUITIES WEAKER

The S&P500 ended its day on Wall Street sharply lower, down -2.1% after a building selloff all session. Tokyo has opened today down -1.3% and heading for a -1.6% weekly fall after a volatile set of trading days. Hong Kong is down -0.5% at its open; Shanghai is down another -0.4% but at least they are heading for a weekly gain. The ASX200 is down -0.8% in early afternoon trade and may end their week unchanged. And the NZX50 is down -0.9% in late afternoon trade and almost certainly will end the week little changed by giving up earlier gains.

SWAPS RETREAT

We don't have today's closing swap rates yet. They are likely to have fallen back today as risk is off while the prospect of an invasion of Ukraine is imminent. The 90 day bank bill rate is unchanged at 1.23%. The Australian Govt ten year benchmark bond rate is down -2 bps from yesterday to 2.22%. The China Govt 10yr is little-changed at 2.80%. The New Zealand Govt 10 year bond rate is now at 2.77% (down -3 bps from this time yesterday) and now above the earlier RBNZ fix for that 10yr rate at 2.76% (down -8 bps). The US Govt ten year is now at 1.98%, and down -5 bps from this time yesterday.

NZ DOLLAR FIRMER

The Kiwi dollar is marginally firmer today at 67 USc. Against the Aussie we are up at 93.2 AUc. Against the euro we are higher at 58.9 euro cents. That means the TWI-5 is firmer at 71.4.

Appreciate this coverage? Support us and go ad-free. Find out how.

BITCOIN FALLS

Bitcoin is down sharply today to US$40,789 and -7.4% lower than this time yesterday. Volatility over the past 24 hours has been extreme at just on +/- 5.0%.

This soil moisture chart is animated here.

Keep ahead of upcoming events by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

62 Comments

My boys understand fuzzy logic and quantum mechanics, and they say that there is still room for upward valuation in residential property. Be quick.

There. Now we've got that out of the way, maybe we can talk about something more interesting.

Can I interest you in a debate about protestors?

Please no.

Please don't, I have just mastered bypassing any posts with those 4 capital letters on top, I will have to add you to the list now!

I have just mastered bypassing any posts with those 4 capital letters on top

Hey, come one now, VTHO seems like a lovely person. ;)

I didn't think I needed to be specific, ha!

Looks like the NZ50 is building momentum in losing steam real quick.

Next week's RBNZ's fireside chat may determine if 2022 will be another year of write off for NZ equities.

Kiwisavers. Sad.

NZ50 was one of best performing stock markets from GFC to Covid.

But the main point to consider is that the NZ housing stock value to GDP is close to 5x whereas equities cap is closer to 1. The NZ50 is not as sensitive to the OCR as to S&P500.

I know you're a property bubble cheerleader so I thought I would point that out.

The OCR is our version of the VIX index on NZ50.

As much as I want RBNZ to act aggressively next week to prove my point and earn me another 'I told you so' moment, I think it'll be a little too harsh on hardworking Kiwis to lose money in their Kiwisavers just to achieve that.

Yes, we all know you're a champion of the hardworking Kiwis.

For people chucking money into their kiwisaver every month waiting for retirement in a decade or 4, a downturn in the NZX isn't a big deal. Most would be diversified into other assets classes and geographies anyway which spreads the risk. Also no leverage involved.

It's those highly leveraged property investors that we need to be concerned about.

Your assumption is aspiring first home buyers don't need it and there aren't people retiring across the country at the moment.

If you're close to retirement or buying a house you should be in a conservative or first home buyer fund with less exposure to volatile instruments like shares. Maybe have your boys run you through some personal finance rules of thumb some time.

Exactly. Novice stuff.

Yes - my assumption is that most people have basic financial literacy, although the comments section does make me question my assumptions sometimes.

"If you're close to retirement . . . you should be in a conservative . . . fund with less exposure to volatile instruments like shares."

No - that is the "novice" comment.

In retirement you are most likely accessing your funds over a considerable period - likely 20 years or more

So if close to retirement, split your funds between conservative and growth funds and draw on your conservative fund in the short term and gradually move funds to top up your conservative fund when appropriate and to meet your needs. KiwiSaver providers allow you to nominate what fund you wish to make a withdrawal from.

Yes, balanced for retirees. Conservative for FHBs looking to buy in next 2-3 years.

CWBW ......your bias towards residential property really shows .....even to the point of "rubbing their noses in it" for Kiwisavers, who most working people are with....do I detect some malevolence towards anyone that is NOT a property investor ? ..... those current HPI figures not treating you well CWBW ??? .....I'm sitting in the sidelines with NZ property mate, its still expensive for what you get ...going to wait for those people who have indebted themselves up to the eyeballs and pick up a beach property (at least 10m above sea level !) when this crazy property market really comes to its senses.....

Timing the market are for superstars.

However, one thing is certain, there won't be superstars in the aspiring first home buyers market.

They need their Kiwisavers holding up for any hopes.

The only exceptions are those cash loaded or on shadow banking like bank of mums and dads, alternate lenders, etc.

In a "proper" economy, not based on residential property, people should NOT have to touch their Kiwisaver to buy a house.....NO exceptions.

So Singapore's economy is improper and based on property?

Your maxims seem extreme.

Singapore or Hong Kong’s economic model is largely about arbitraging the inefficiencies, or loopholes, in their larger neighbours. To some extent, money laundering is the core business. It doesn’t take a genius to come up with this economic model. Link

Nor should asset prices be supported for Political aims. Surprising how many apparent Capitalists are against the free market.

mfd,I am not sure how you work out that some capitalists are against the free market when capitalism is all about the free market. Politics can only tinker on the edges of any real market.

Capitalism is about seeking profits.

Free markets are about a lack of government intervention and open trade.

There's crossover, but a capitalist doesn't have to seek or endorse a free market. Often quite opposite, any good capitalist seeks some form of exclusivity.

I'm also sitting on the sidelines until prices come down. I was notified today that yet another property I had been watching failed to sell at auction (now being sold by deadline). Think I'll wait until I see it priced.

Didn't take much financial IQ to pick the slump in shares. I sold a whole lot about October last year.

Also doesn't take much financial IQ to pick the housing slump underway.

HM

Basic financial IQ actually says be very, very careful about trying to time the market - property or shares.

The majority of posters on this site were picking a housing slump in March 2020.

As an aside, a couple of comments I really love from March 2020 are:

- Buy a house now and be laughed at and pointed at by everyone you know, because you will officially be stoopid.

- Don't worries be -30% drop cone end April

- The property market and its many disciples enjoying their last supper (that one is Independent Observer)

Fair enough.

Let's see what my timing and predictions are like:

- bought house in late 2019

- Sold shares October 2021

- picked the OCR to be back near current levels within 18 months, and looking to fix mortgage again accordingly in 2023 (currently fixed at 2.3%)

- my central forecast for house prices to be down 5-10% by end of 2022

Let's see how I go, I am sure you will remind me if I am wrong, seems like you keep records :)

MortgageBelt, I note your comment yesterday, I should have been clearer, suggesting mortgage rates will not hold normalization at 4.5 to 6% and drop back to 3.0% only encourages addicted housing speculators with more sugar and would be a social disaster for NZ. We need normalized TD rates of 4 to 5% to happen to give conservative investors an alternative to housing. This would free up many houses and hopefully reduce the number of locked up empty houses of which there are many in Auckland at the moment. Lets hope for NZ we have seen the last of the 3% mortgage for balance sake.

Maybe you’re right.

Im not advocating the merits of low interest rates just have a sense that there are too many headwinds and potential black swan events ahead for the old normal of a full cycle of rate rises.

yes I accept that MBelt, but I think inflation, US rate rises, and exchange rate pressure on petrol will be un-stoppable here. We will know in 2 years !

Also I don’t think interest rates are necessarily the main reason for housing problems. Look at the UK, Germany, US - they have lower rates than NZ but kiwis put everything into property & home ownership. It’s something about the NZ psyche and lack of decent investment vehicles that aren’t taxed to death.

Coming to a bank account near you - New Zealand goes Caracas.

No more donations at this time, please and thank you for all the help you’ve given here. All my accounts have been frozen. @KiwibankNZ cannot give me a reason why. Still trying to sort. So @KiwibankNZ are trying to starve us out.

edit - well what do you know -

FUBAR nz@NzFubar·5hPeople power wins again ✊ sat in Kiwibank, word got around, people turned up to Kiwibank, a Wairua Tapu was given, we sat down in numbers and my accounts were unfrozen within two minutes. Still no reason given but accounts back up ✊❤️

According to ZB ChCh this morning, Brownlee of National & Woods of Labour both expressed deep interest, and mutually so, as to the identity of the financial supporter of the parliament protestors. While the government were too lax to contemplate & react to the warning offered by Ottawa of likely outcome of the protestors on arrival, perhaps though, Jacinda has been much quicker, in contacting her soulmate Justin, re his stroke of genius, freezing suspect bank accounts? Just kidding!

I hope not, it's a surefire way to create a currency crisis and a run on banknotes.

Unforeseen consequences, like towing vehicles.. I'VE GOT NEWS FOR YOU; Unvaccinated protesters can't catch a plane, so you'll be creating permanent protesters lol :) Then they'll send for people to pick them up, effectively creating more protesters.

Some maturity is needed. The government has case studies, the protesters have case studies.. yet as far as I'm concerned they can ALL spread Omicron, which itself is considered very mild.

Businesses throughout the country are crying out for customers, they say people are scared to go out - WELL NEWS FLASH: there are huge numbers of potential customers in Wellington CBD right now and they're not afraid .

I think fantasy land needs to be abounded for the reality mandates are past any useful use-by-date. Don't let the lines of communication break down - sort it out and get your backside to the Backbencher

If you're quick maybe later in the year we can all laugh about it.. "remember the time Trevor put the sprinklers on and cranked music?" "Yeah that was a d*&^ move, kind of funny with the Twitter music requests though!" "haha, true that.. what about how the protesters then posted memes about luring Jacinda out with bundles-of-hay?"

"Definitely a classic.. geez, it was looking pretty tense there for a while.." "Yeah, but as the anthem goes; Peace, not War, shall be our BOAST." "Yeah, thankfully they managed to come to their senses"

Be Quick

The PM is the expert on locking down cities and ruining businesses. So she wants the protesters to go home and stop locking Wellington so she can do it herself?

Nice scenario Zack.

It may be more difficult for the team of 5 million + 1 million to ever forget the hate speech (‘river of filth”) this week by a cabinet minister Woods under the protection of parliament privilege.

I accept that.

For a lot of people it will be wanting the mandates gone and for Labour to sit in the corner until the next election.

One thing interest.co.nz has taught me this week: DON'T let the sun set on your anger.. be quick to apologize and change direction when things aren't working.

Yep - division is our enemy.

Unfortunately some leaders divide & (try to) rule.

Divide & rule. Lord Minto (yes John that is not you, far from it) set Hindu against Muslim. Shockingly cruel & in-humanitarian. This government t has created, in hugely more modern times, and in four short years a society here, that has never been so divided.

Good stuff Zack. I see freezing of bank accounts as a stark warning as to why we don't want to go down the cashless, state digital currency route. I don't know @FUBAR from a bar of soap but if it can happen to him it can happen to anyone. Thankfully Kiwibank saw some sense.

Zack, thank you, “bundles of hay,” best one liner that I have heard for many a long time. Good to be able to go to sleep tonight with a quiet smile.

=)

As I said this morning, this rise in second tier finance is worrying. Really does bring back bad memories of those dark mezzanine finance days.

You get the feeling it’s going to unravel....

Oh for sure, a slow motion traincrash

And the rock solid security offered is….?!?

Current drawdowns from peak:

S&P 500 -9%

Shopify -61%

Facebook -46%

Square -63%

Tesla -29%

Paypal -66%

https://www.cnbc.com/2022/02/17/cathie-wood-says-her-innovation-stocks-…

Not to worry says Cathie.

Cathie Wood of Ark Invest said Thursday the technology companies in her innovation-focused portfolio are drastically undervalued, and she believes that her fund’s recent sell-off is short-lived.

“Our biggest concern is that our investors turn what we believe are temporary losses into permanent losses,” Wood said.

Be slow!!!

They seem drastically undervalued to her, because she bought them at all-time highs.

Truly, one of the greatest (and most predictable) flame-outs in investment history, and certainly not done yet.

She has come to define the new technology space – Michael Milken was another who was similar in stature some decades ago – the “junk bond” king – in the late 80’s he ruled supreme.

Ended badly for him, securities and tax violations (1990) – but later with a forgiveness (Trump) and redemption (founder of medical philanthropies).

Whether you like your analysis written in crayon or not The Tuttle Capital Short Innovation ETF (SARK) is up over 50% since inception last November. Betting against Cathy has been both profitable and amusing.

Those surveyed say that current inflation is running at 3.7% (actually its 5.9%, so financial understanding is not flash). These same people say in one year it will rise to 4.5% and in five years it will rise to 5.6%. Expectations - even from this surveyed cohort of unknowledgeable people - is that we face rising inflation.

That's for the Dec 21 quarter. The Mar 22 quarter shows one year mean at 5.8% and 2.1% for five year mean expected inflation.

Fed survey exhibits falling term inflation - graphic evidence here and here

{kind=link}

{kind=link}

Our Chris Joye over the ditch thinks house price falls will cap interest rate increases.

Since we released our forecast for a 15-25 per cent correction in house prices after the first 100 basis points of RBA hikes in Oct last year, banks have followed suit. Westpac is calling for a 14 per cent decline in prices in 2023 while CBA and NAB are fingering 10 per cent. And there are already clear signs of a welcome cooling in conditions with house prices in Sydney and Melbourne effectively flatlining since November 2021

https://www.afr.com/wealth/personal-finance/house-price-falls-will-cap-….

I rest my case.

That's what I have been saying for about 6 months and almost no one agrees with me!

I do!

But if I’m wrong then my floating choice will fail, thankfully small enough not to matter much.

Yeah, I am absolutely fine if I am wrong too!

It will just be a nice bonus if I am right!

Plus, it's fun being a contrarian.

Inflation will likely "cool" due to base effects anyway this year. Little comfort for consumers of course.

NZD is key if it keep low inflation will stay high, but going shopping for meat up around 15%-20 most meat is from NZ not sure why a sharp raise in price petrol obviously creating inflation and this looks like going higher so not sure if inflation is going to cool soon.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.