Unemployment has remained at 3.4%, while private sector ordinary hourly wage growth has risen to 8.2% from 8.1%, according to March quarter labour market figures released by Stats NZ.

The figures are stronger than those expected by the Reserve Bank (RBNZ), which had forecast 3.5% unemployment and just 7.6% private sector annual ordinary hourly wage growth.

Beyond those two 'headline' figures the data for the March quarter appears even stronger than at first glance.

The underutilisation rate – a broad measure of spare labour capacity that includes those unemployed, underemployed, and in the potential labour force – fell to 9%, from a revised 9.3% in the December quarter.

In the March 2023 quarter, the labour force participation rate increased to 72% and the employment rate increased to 69.5%. Both are the highest rates recorded since the particular data series - the Household Labour Force Survey began in 1986.

There were 22,000 more jobs added in the quarter, taking the total number of employed people up to 2,886,000. Employment growth in the quarter was 0.8%, well ahead of the 0.2% forecast by the RBNZ.

"Unemployment and underutilisation rates, as measured by the Household Labour Force Survey, have been sitting at or near record lows for more than a year," Stats NZ's work and wellbeing statistics senior manager Becky Collett said.

The employment rate for women increased to 65.2% in the March 2023 quarter– the highest rate since the series began in 1986.

The employment rate for men remained steady over the quarter at 73.9%, remaining the highest rate of male employment since 1987.

A cooling labour market is needed for the RBNZ as it battles to try to get inflation back towards its 1% to 3% target range. As of the March quarter the annual inflation rate as measured by the Consumers Price Index (CPI) still a long way from target at 6.7%, even if this was a reduction on the 7.2% rate as of the December quarter.

The unemployment rate has been in the low-3% range since the September 2021 and a shortage of available workers to fill jobs has helped to fuel inflationary pressure.

ASB senior economist Mark Smith said the latest figures "suggest that the NZ labour market has remained extraordinarily tight".

"What will the RBNZ do? Since late 2021, 500bps [basis points] of OCR [Official Cash Rate] tightening has been delivered, the most on record. At 5.25%, the OCR is well into restrictive territory according to our and RBNZ estimates.

"However, the starting point for the labour market and inflation remains miles away from where they will need to be to provide the best chance for achieving sustained growth in future. We expect a 25bp hike in May, and a 5.50% OCR peak this cycle.

"More downside risks are emerging, but the OCR will not be cut until the RBNZ is confident there is sufficient slack in the labour market that will see CPI inflation settle in the 1-3% target range. We expect OCR cuts to commence from mid-2024 and view current market pricing (which includes 25bps of cuts by year end and more than 150bps of cuts by late 2024), as being a tad premature."

Unemployment

Select chart tabs

97 Comments

Looks like 50 bps is back on the menu..

Not in one shot, probably. I think it quite likely that we will see two 25bps raises by end of the year, with a peak at 5.75%.

I reckon 50 if not more. Banks are dropping rates, unemployment isnt growing. The RBNZ wont want to drag this out forever as it is now. the frogs are boiling too slowly and the long term damage will be worse.

Good news! Keep up the hard work team. And make sure you get your 8% raise.

Lets just celebrate this data for one second before we turn eyes to what the RBNZ will do. Are we to dare to dream to get a goldilocks scenario?

Indeed. All predictions around the tight labour market easing and wage inflation coming down are proving to be incorrect. Neither the economy is cooling nor are skills flowing into the country where genuinely required.

I am seeing a lot of businesses in my broader field starting to bring forward their plans on investing in capital expansion and/or labour-saving technologies, particularly manufacturing. Interesting times ahead!

"private sector ordinary hourly wage growth rose to 8.2% "

So an OCR of 8.5% isn't far-fetched after all....

According to spruikers, a 4% OCR was impossible 'because the housing market is the golden goose that cannot and will not be allowed to fall in price - because Jacinda Adern said so'.

And yet here we are with an OCR >5% and unemployment near record lows.

The world works in mysterious ways.

No just the figures get manipulated in mysterious ways.

Which figures get manipulated Zwifter?

According to you also mr independent

It's almost as if there is a delay of around 18 months before OCR changes flow through into the real economy...

My observations are that the delays between OCR change and willingness to pay change has been 6 to 12 months for property, which may perhaps be the time to the average mortgage borrower's refixing event

"Public sector ordinary time hourly earnings increased by 4.9 percent"

Pretty savage for the stretched public sector workers

And yet our current account deficit widens, not unexpected in an inward looking economy that borrows to spend.Looks like we have a lot of job creation going on somewhere.

I think the party will really start when the current account deficit contracts suddenly. Which it will

Do you have access to data that suggests we can claw ourselves out of this massive current account hole? I heard one international expert saying even if we halve the deficit from its record high (cut the deficit by a whopping ~16b or 20% of our total exports), we'd still be at an unsustainable level.

The problem is it that it is not mathematically sustainable. Eventually it will cause a debt crisis (either govt or private) if it stays a this rate. Because we won't be able to increase exports to address this problem we will have to decrease imports. This will cause a significant fall in consumption and a serious recession.

Is it a recession if we just stop buying imports? Imports aren't part of our domestic economy which we measure recession against.

How do we stop imports? its nigh on impossible to put caps on things - the only way is to stem demand via the OCR or to raise import taxes (all sorts of issues). so its back to our good mate the OCR.

The problem we have is the value of goods we export is exceeding the value of goods we import. We then issue IOU's to make up the difference. In effect we borrow from abroad. This borrowing being reflected in our quickly deteriorating NIIP. How can we realistically do this? 2-3 years. Something has to give.

Print a few billion and hand it out to rich peeps... or lend it without interest or controles... to people that are locked up in NZ.. then watch queues of container ships arriving ... i am not sure we can be surprised.

lol.

This is interesting, it seems to point to the economy being 'alive' without tariffs and not producing quite so much domestically ie importing goods and mainly domestically consuming services?

Note that broadcasting equipment (2.5%) and computers (1.4%) form a sizeable amount in any recent year

https://oec.world/en/profile/country/nzl?yearlyTradeFlowSelector=flow1

2021 Cars 8% Crude 3.7% Delivery Trucks 3.1% Refined Petroleum 3.8%

2016 Cars 9% Crude 4.7% Delivery Trucks 3%Refined Petroleum 3.3%

I wonder what the effect of the govs recent changes on CO2 fees for car imports will be. Many cars that were eligible under recent changes for rebate are no longer, messing with the market upsets things.

That's incorrect. Imported goods and services are subtracted in GDP calculation but the economic activities around imports are still accounted for (logistics, warehousing and transporting, retail, banking, etc.) Not to mention the importer-driven activity. E.g., Warehouse Group mostly sells imports but has a large number of employees working in front and back office and buys local services when selling imports. All these activities exist because those items are being imported in large quantities from elsewhere.

Those goods don't just land directly from the offshore factories; local services are performed to bring them to consumers.

I agree. Soaring current account deficits also a result of a country's downward slide in the economy's export competitiveness/complexity.

True also in our case where consumption patterns have kept up with first world standards, but not our production. So, the gap in value continues to widen while the volume deficit also increases as we import more people to work in the domestic economy.

The significant fall in consumption will have to come at the expense of our first world living standards.

I mean that's the end game. Unless we adapt by increasing exports we will have to accept a lower quality of life.

We do, at the government level...a lot of people paid to shift paper around and input it into a computer.

Wage price spiral is now underway... RBNZ need to raise by 50 bps at the next meeting

Clearly the rises have been too slow and too low to get the desired effect. The OCR should already be at 6% plus but they just couldn't take it there because of housing. Its basic stuff the OCR needs to be HIGHER than the inflation rate to bring down inflation.

the longer they wait the higher it will need to go. should raise 75 and threaten another 75.

faffing around isnt getting us anywhere.

most people dont give a stuff if house prices crash further anyway - i really would love them to as it would sort tons of social issues asap - plus clearly the current drop in prices hasnt stopped much of the spend anyway (the fear is all to protect a few who are either overleveraged or desparate to keep making money from houses.... and honestly they made their own beds )

Raising the OCR 500bps (1900%) in 18 months is not faffing around.

It is when you consider most of that time was lost returning to neutral territory.

Inflation is heading down in most places around the world but very few have OCRs (or equivalents) above their inflation rates.

Might have dropped slightly but in europe its up and everywhere else its above targets. Noone has succeeded yet. We have to wait to see.

At my next salary review coming up i'll be seeking a salary increase that covers any increase to my mortgage costs. The more the RBNZ increases, the more i will be demanding and I will be likely to get it given staff shortages.

Clearly RBNZ's panicked moves are not working or maybe even causing their own wage spiral. Doing more of the same doesnt seem to be a good idea huh?

'Clearly RBNZ's panicked moves are not working or maybe even causing their own wage spiral. Doing more of the same doesnt seem to be a good idea huh?'

Chicken/egg situation.

You (and many others across society) ask for 10% wage increases to cover incresed mortgage costs, and it will show up as unacceptable wage inflation, and in response the RBNZ will raise the OCR/mortgage rates even higher. So you ask for an even bigger pay rise, and it shows up as even more wage inflation...and the RBNZ raise mortgage rates even higher again!

If you want to stop your mortgage rates going higher, you need to do the opposite of what you intend to do above and ask for a pay freeze.....and tell everyone else to do the same....but you won't, right?

So without realising it you are the problem that you are blaming the RBNZ for.

All they want is for you to be poorer and to accept that fate (not a tough ask right?) This is the cost of bailing everyone out in 2020 (there are no free lunches in an economy).

It is chicken / egg. But not my problem.

Wage rises are a response to inflation, not the cause of. People seeking decent wage rises did not kick off this inflation spiral. If anything wages have been driven down for a decade or more in real terms. Yet - where was the outrage then?

Households did not cause this, yet here we are being asked to carry the can. Whilst the RBNZ doesnt seem to have any problem with extreme profiteering going on. Just look at the Banks / Supermarkets / Electricity Companies and many, many others.

Also why should I as a homeowner in my late 30's be asked to 'take one for the team' when others - boomers, people who have small to no mortgages and other well off others get to bank the gains and contribute nothing to get inflation under control.

Sorry but this 1980's view of the causes and solution to inflation is no longer fit for purpose.

Good luck with this view - your indoctrination into the real world is approaching (whether you like it or not - the powers that be couldn't care about your personal circumstances and victim mentality).

https://clarityadvantage.com/claritycms/wp-content/uploads/2016/12/iSto…

{kind=link}

Thanks for not actually having any reasonable response to my point, which to me reads that you are probably someone who falls into one of the aforementioned groups and expect everyone else to do the hard yards to get inflation under control.

The good news is that the 'real world' is changing and not everyone is indoctrinated enough to think a 1980's solution can fix a 2023 problem.

My reasonable response to your point was in the original reply - but went completely over your head because it wasn't what you wanted to hear.

You will act in your own self interest and demand for wage increases - this will be viewed as more inflation by the central bank, and as a result they will keep raising OCR/mortgage rates. As a result, you will be no better off.

If you think you have a better strategy for monetary policy perhaps you should let us all know what your ideas are in this new 'real world'?

In the real world as it currently stands.....I don't expect that any particular group should have to be responsible for doing the hard yards to get inflation under control (in which you appear to think you are the victim - and do have a good case to argue) - but in the 'reality' of the current system, the only lever central banks have is to increase the cost of debt to remove demand. If you are holding a lot of debt right now (which is something I have warned against on here for many years), then perhaps you just find yourself in the wrong place at the wrong time. Unfortunate but a reality that you will find a way to work through.

If you don't want to deal with that reality - as I say good luck to you as you learn how the system currently works. And if you don't like it - good luck changing it - honestly I would help you change it to be fairer if there were the political will to do so and mechanisms that we could use to help share the pain more evenly. As it stands, it has worked out to favour older generations at the expense of people your age. What are you going to do about it?

You can complain to the wealthy oldies and say that we should have wealth taxes to remove money supply from the system (and reduce their ability to spend over their retirement) - but they will tell you to run for the hills - so they are happy that you slave away and pay lots of interest on your 8-10x wages loan on your expense house and have less to spend in the economy. And be thankful for the opportunity to do so! This is how the real world currently works - welcome to the 2020's.

If you want to stop your mortgage rates going higher, you need to do the opposite of what you intend to do above and ask for a pay freeze.....and tell everyone else to do the same....but you won't, right?

That obviously wouldn't work as no-one would do as requested.

Morhyoss is correct in his evaluation that the higher than usual wage rises are a response to inflation, not the cause of it.

Ok - I think we're looking at this from vastly different perspectives.

I'm explaining this to you how the RBNZ will view it (and what they will likely do as a result and how it will impact people in the coming years) and not what you personally think is right.

Hopefully this distinction can be comprehended.

And of course wage rises are a response to inflation! That is so obvious that it doesn't need to be mentioned. What does need to be mentioned and acknowledged is that central banks don't want those wage rises - they want you to be poorer. Their aim is to crush wage inflation and raise unemployment. But people don't seem to want to get that or accept that. That is 'the reality' we are facing - love it or hate it.

So the choice is accept getting poorer for the greater good, and suck it up! That’s crazy. I get that wage inflation will cause interest rate rises but only if everyone can get rises. If you are in a skilled profession it’s the time to play hardball. Make sure you do you homework and be prepared to walk if you don’t get the money you want (not necessarily right away). I would also add be prepared to leave NZ.

by HSL | 3rd May 23, 5:35pm

So the choice is accept getting poorer for the greater good, and suck it up! That’s crazy.

No it is not - the crazy part was what got us to this point.

If your net wealth (nominal or inflation adjusted) is the same this time next year, I'd say you will have done remarkably well. But I'd suggest the majority of the population will be poorer - the value of their assets will be less and the cost of the consumption items they need to buy will be higher.

And this is what central banks want to remove aggregate demand from the economy.

This has been predictable for ages. Everyone is aware of how reserve banks solve inflation (raising rates) and of the likely risk of a house price crash... which is now happening.

Thus why should I as a homeowner in my late 30's be asked to 'take one for the team' isnt a valid question. if you gamble (buy a house or other investment) its your responsibility to assess the risk and if the worst happens you should have a plan to deal with it.

Its not taking one for the team - many didnt choose to gamble, or managed their risk better.

Now - you have to assess your situation - do your research and work out how bad it can get, the losses you are willing to take etc and your exit strategies.

Its always been this way. no victims here.

Thus why should I as a homeowner in my late 30's be asked to 'take one for the team' isnt a valid question. if you gamble (buy a house or other investment) its your responsibility to assess the risk and if the worst happens you should have a plan to deal with it.

Yip - which is why I had been telling young people to be very cautious about loading up with too much debt in recent years as nobody cared about them - they were just going to be used as fall guys/girls for other parts/players within the economy...(property speculators encouraging people to buy, the central bank saying for banks to lend courageously etc).

FHB's in the past few years were essentially being thrown under the bus/being used a cannon fodder to prop up the wealth of those already holding assets - now they are loaded up with debt - they can't escape.

or what? you'll go find another job?

Wait till your employer calls your bluff.

Well yes, I am actually entertaining another opportunity at the moment, which is offering a significant bump on my current position.

The bigger your salary the more savings to your boss when it come to lay-of time. Be careful out there.

More power to you. Hopefully you've researched where you're going, because in a downturn, it's the last employed that's first to go..

That's not generally true. It's an opportunity to weed out the deadwood, some of which may have been there for years.

Research out from Bamboo last month is 65% of HR departments follow it. That's 2:1 in favour of generally true - though you're right, it's not the only way.

Ooooh scary!

Let’s stop the rates hikes immediately!

At some point the business revenue drops and there is no money to increase salaries. Thats the game and it will always work eventually.

That is exactly what is already happening out there.

Signs of an overstimulated economy. Unemployment at this level last seen just prior to the GFC.

Rock and hard place for central bank.

Keep rates high = asset price destruction and (very high probability of) nasty recession.

Drop rates = risk inflation going higher/becoming more entrenched/over stimulating economy even more.

Chickens coming home to roost for years (perhaps decades) of loose monetary policies - pumping asset bubbles and extending too much debt that the productive economy (wages) are going to struggle to service.

https://eurweb.com/wp-content/uploads/2022/09/Chickens-Have-Come-Home-t…

{kind=link}

I just wish all that debt was at least spent on something useful. What have we got to show for it? Barely any upgraded or new infrastructure, very few high-value businesses, a crumbling education system, and healthcare tearing apart at the seams.

What a waste

Yip and that is private debt. Imagine the public debt we created over covid to pay everyone's wages while they sat at home (and gambled with private debt on the housing market....) - it was billions of dollars and could have instead be spent on new infrastructure - e.g. hospitals/roads etc.

Now government trying to cut funding for things like the new Dunedin hospital.

As has been pointed out - everyone will need to accept that we are now poorer, but nothing to show for the money that has been spent. i.e. we are going to all collectively have to take a reduction in a quality of living to pay for that fact that the government paid us all to stay at home - while the pumped economies full of money - creating this inflationary mess we are now in.

'The employment rate for women increased to 65.2% in the March 2023 quarter– the highest rate since the series began in 1986.

The employment rate for men remained steady over the quarter at 73.9%, remaining the highest rate of male employment since 1987'

All so that we can be serfs/slaves to the retail banks who lent so much money to working age people in order to just buy a house.

I guess this is a by-product of our collapsing birth rate.

Lol - because people in their 20's and 30's have struggled to buy houses in order to feel settled/secure enough to raise children.

Chicken/egg stuff.

Create the secure environment (shelter/work/community) and young people will get married and raise children.

Do the opposite, and create FOMO/FOOP/stress/depression/anxiety via poor financial and social conditions with society and young people will put off getting married and having children.

Couldn't agree more. I wouldn't be feeling very secure in a house with a 6-800k+ rolling onto new interest rates this year that's for sure. FOMO was also fueled by people seeing prices skyrocket so darn quickly that they felt like they wouldn't be able to have children if they didn't get a house and start the next chapter of their lives, and were getting outbid at every opportunity by specuvestors. Now those who bought in the frenzy will hardly be able to afford to have kids with the mortgage in tow and as we know, biolgical clocks and the changes in the chance of conception has all the stats to confirm. All of this for the benefit of banks and those who already had multiple houses. A very sad state for the young of our country, who we should be doing all we can to keep, educate, train and retain.

Yes it is almost treasonous that politicians have used a housing bubble and its 'wealth effect' for political gain.

It is very popular in the short term, but with very little care/consideration/compassion toward the longer term impacts on people and society.

Hence my anger of the last 5+ years seeing people trying to promote ever higher house prices (for their own financial or political gain) as I can see the damage it is causing.

Its not really the people who pushed the ponzi that are to blame - Its the idiots who bought into it. Dont they teach Tulipmania anymore?. At some point it had to crash.

A big lesson in personal accountability.

It's a hard one though. If you are wanting to start a family you have a limited runway for that. And for a lot of people renting and having kids isn't a tenable situation with how little stability renters in NZ have. It is easy to say "wait" but what happens when you have already waited and house prices just kept going up? The biological clock keeps ticking and time starts to run out at some point you just have to jump in.

Not sure what the solution is but I can see why people aren't happy. If we could structure it so only investors get bitten and FHB's who were just wanting a home to live in and raise a family didn't get kicked as hard that would be great but not sure how that could be practically done.

Yeah but lifes not like that.

We built a capitalist society.. cant complain when it doesnt suit because some people made money and we lose money.

That is the problem though - we've created a system where nobody honestly believes that they can or should lose.

I want and deserve all of the return and none of the risk!

I'm not saying that you are wrong. You're speaking the harsh truths that need to be said.

But I am just saying that you can see why people made the choices they did and how the negative externalities have some wider social implications. Calling them idiots for doing what should be fairly normal and trying to start a family isn't overly helpful commentary. It's ignoring the other reasons for owning a house apart from the financial ones.

Although I guess even if they lose money though they still have a roof to live under, there are worse situations to be in.

I have far less sympathy for investors who were chasing capital gains and operating purely out of greed, they are the ones who made this situation as bad as it is.

And they wonder why property crime is rising when their economic policy has been to loot the following generations.

NZ's housing crisis is a moral problem, then a policy problem. People felt entitled to live beyond their means at the expense of following generations.

An economy built on speculation is destined to falter. When working hard is no longer correlated to higher incomes and a better life, the disassociation of effort and reward makes society as a whole more fragile.

And now we see the results, crimes up, health outcomes stagnating, and our most productive young workers leaving in droves.

Despite the tight labour market the number of children in benefit dependent households has increased by approx. 40,000 over the last 6 years.

So still not worth joining the labour force and these numbers do not show up in the unemployment statistics

Yeah, well, fewer workers and more retirees makes workers a prized resource: https://data.worldbank.org/share/widget?indicators=SP.POP.1564.TO.ZS&lo…

Demography is destiny and you my little workers are prized piggies.

BRICK TOP; You got to starve the pigs for a few days, then the sight of a chopped-up body will look like curry to a pisshead. You gotta shave the heads of your victims, and pull the teeth out for the sake of the piggies' digestion. You could do this afterwards, of course, but you don't want to go sievin' through pig shit, now do you? They will go through bone like butter. You need at least sixteen pigs to finish the job in one sitting, so be wary of any man who keeps a pig farm. They will go through a body that weighs 200 pounds in about eight minutes. That means that a single pig can consume two pounds of uncooked flesh every minute. Hence the expression, "as greedy as a pig".

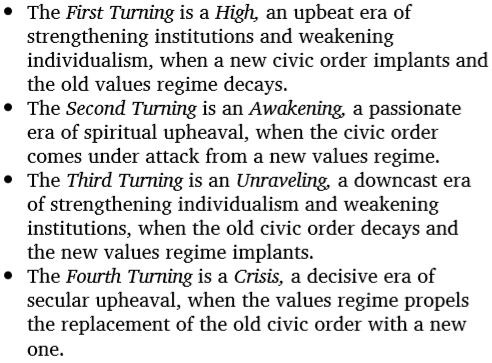

What is playing out is very close to what the authors of 'The 4th Turning' predicted. Strauss/Howe theory.

https://ebookscart.com/wp-content/uploads/2019/12/1-78.png

{kind=link}

A period of crisis through until the end of the 2020's - with financial chaos and the high possibility of some type of WW3 event.

Boomers born just at the right time during the high, but only to find things deteriorate throughout their lives. Millennials born to live their young adult lives (like their greatest generation grandparents) through economic crisis and wars...before the next high begins.

We appear to have finally seen an inflection point in the inflation environment. Millennials will probably live through an era of low or no asset price appreciation (for example home ownership will no longer a magic money tree) but increasing wages.

Why can't we get MoM data on CPI?

Old systems, manual process/compilation and lack of spend ........ there is some argument that the set could be noisey at monthly levels and longer periods act to smooth the data set.

Massey's GDP live has it tracking at 6.7%

As a business owner, we have seen a sales slow down since November last year, April fell off a cliff (circa 35% down on last April), and this month is looking similar. Retailers I have spoken too are definitely slow, other importers I know are feeling the same trend. I have no intention of cutting staff but Im an SME not a big corporate, rubber will hit the road on unemployment soon...

Sluggy,

Can you say what line of business you are in?

Swimming and spa pools. Luxury items basically. Admittedly the last couple of years have been halcyon daze, I never expected it to continue.

Undoubtedly a strong report, but if forced to pick out a couple of points of minor weakness they would be:

1) Decent uptick in the non seasonally adjusted unemployment rate (from 3.3 to 3.7%). Would normally dismiss this as noise/seasonality, but the covid related shocks to the labour market over the last couple of years have made the seasonal adjustment process tricker than usual. BLS have discussed this in the context of their own survey data.

2) A fall in average weekly hours across raw, seasonally adjusted and trend series. Is the first sign of slack a reduction in hours worked?

Neither of these are close to signalling a soft market on their own, but it will be interesting to see how they evolve over the next release or two.

Where do they get these pay rise increase percentages from ??? ......a mate of mine in the public sector was talking to one of the bosses and basically the answer, in a nice way PC way :) was "if you want a pay rise, best move on and get another job"......so for anyone in the public sector out there, what has been happening on the ground ?

Also, I would love to see the data base/surveys for salaries/wages, these Government agencies get their % figures from ...I would well imagine it would be like the unemployment data - manipulated to suit their modus operandi .....pathetic.

My wife used to work for the public service...flew in and out of Wellington, she often joked it was a waste of money as meeting may been an horu tops and took most of day get to the airports (but guess when tax payers money who cares) . When Jacinda said there was a pay freeze no pay rises etc over the lockdown period, my wife got a increase, as did many others. How they worded it was, it's not a pay review or a rasie, all we are doing is moving your pay within the pay bracket of your tier. Go fiqure.

The public sector wage freeze was a travesty - I saw right from the start that the incentive was to shift jobs instead of being loyal to an employer and that is exactly what happened - churn is huge. A lot of agencies had "pay adjustments" recently to help with inflation pressures, but for many it was essentially a 3-5% pay cut after tax depending on their salary, after adjusting for inflation.

The result of all this seniors are getting jobs as principals, not because they deserve it but because certain skills are in high demand and employers are willing to pay principal rates to secure senior skills. Rinse and repeat, and you have the churn the public sector is seeing.

The % rates from agencies would exclude contactor fees

The big rises are coming from the private sector, no surprise the public sector is losing staff:

"Public sector ordinary time hourly earnings increased by 4.9 percent"

My own pay has gone up by about 5% over the last 2.5 years, there are higher increases to low earners - policy is essentially to compress the wage scales. Lots of skilled health care workers looking overseas to greener pastures.

This tells me that the Reserve Bank hasn't made a lot of headway in reducing domestic inflation pressures. Maybe it is a matter of timing - and the softening will come - but it may also mean that we have a lot further to go yet before the tightening cycle peaks. That would be consistent with history, whereby monetary policy has to tighten much further than the snowflakes predict.

The bust is normally almost as deep as the boom was high... its natural. So there is a long long way to go yet.

People are still wearing their rose tinted glasses expecting a few more months of pain and back to the glory days. Reality is that we will be discussing the new norm of falling prices and higher unemployment for a few years yet

Previous lowest unemployment rate 3.4% in December 2007. It didn't get back to that level again until 2021.

It was nearly 7% in 2012.

Any what happened shortly after 2007.....The ponzi pump party may have trouble recalling after the hangover of a decade of bloat resulting from emergency rates.

Another 0.5 % OCR rise!

"This Labour market is way too hot!" said Goldilocks.

But its not a fairy tale.... the biggest credit bubble in NZs History will be no Happy Ever After ending.

Won't the RBNZ look silly if inflation falls away WITHOUT people losing their jobs and businesses going to the wall? ...

Perhaps that's the conclusion government has come too and is why they're opening the immigration gate ... [Just kidding. I give government virtually no chance of any such thinking.]

This is great news for the country and should be celebrated. The quality and remuneration of the individual jobs may vary but overall a positive stat for once. All this includes the increases in the minimum and living wages which seem to have been silently absorbed somewhere. On the other hand all these employed people being able to actually live on the wages with the exorbitantly priced everyday items at the supermarket and Briscoes I am not so sure about. The well reported world wide rort of companies increasing their profit margins off the back of ‘just being able to do so’ blaming supply chains issues/war/etc seems to be alive and well in NZ as well. What can the average customer do about it? Squat unfortunately. Just sit back and watch it play out in frustration.

I think we can all agree the cake size is the cake size. The only way we can balance things up where we can afford to support our people and at least maintain their current living standards is to reduce their tax burden and make that up with taxing the currently untaxed income of the rich at a rate that fairly reflects their ongoing obligations to operating, maintaining and developing our country and society. The cake size stays the same but the outcomes are quite different for the country and the people who live within it at the opposite end of the income dynamic.

We need numbers.

What is the:-

Total on the unemployment benefit

Total on sickness benefit

Total on jobseeker

And costs of it all.

Costs of all the listed above is around $3.3 Billion since thats all basically the one benefit. If you add up all the other benefits excluding Super we get to around $16 billion.

But even if we cut all of that spending the trade deficit will still be $30 Billion plus. And got to consider that most of that benefit money flows back into the economy since it's spent mostly on necessities so a lot of businesses would likely be hurt as well.

You can't tax your way into prosperity but you also can't budget your way out of poverty, our issues are far deeper than what can be solved by spending cuts.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.