Inflation pressures are continuing to rise, according to the results of the latest monthly ANZ Business Outlook Survey.

ANZ chief economist Sharon Zollner said the "upward trend" in inflation pressure had continued.

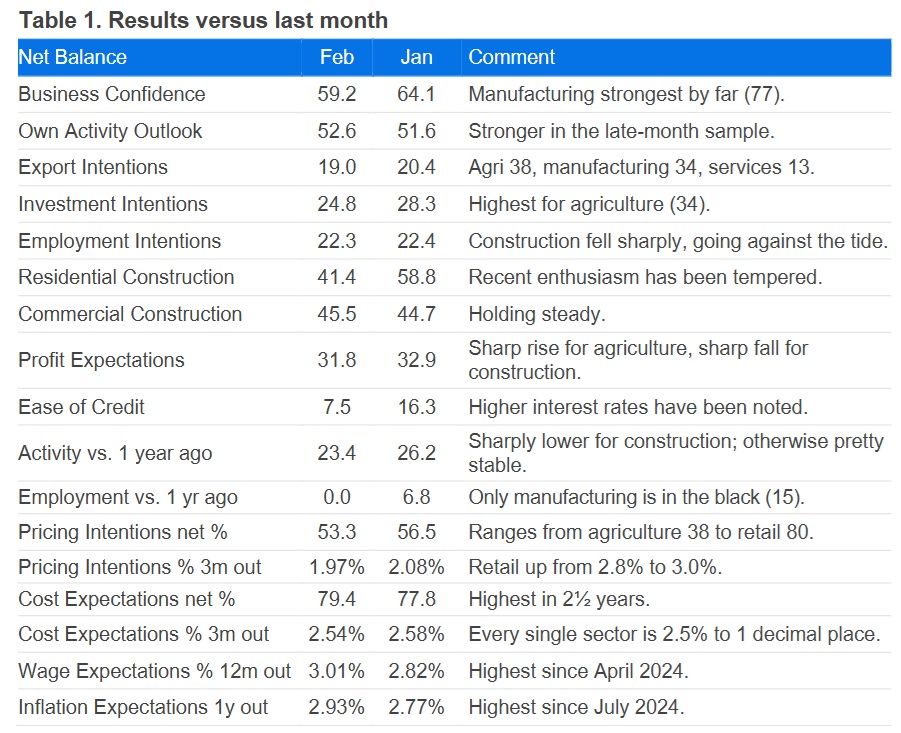

"The net percent of firms expecting to increase their prices eased very slightly but is still trending in the opposite direction to our and the RBNZ’s [Reserve Bank's] inflation forecasts," she said.

"The net percent of firms expecting higher costs also remains elevated."

Zollner said the increase in wage pressures seen looks very modest thus far, "but the level of pricing intentions is not consistent with widespread expectations that headline inflation will trend lower this year, nor are the expected wage measures currently particularly supportive of forecasts of flat or falling wage pressure".

She said that 'headline' Consumers Price Index (CPI) inflation looks set to drop back into the RBNZ's 1%-3% target range for the March quarter (the annual rate was 3.1% as of the December quarter) and the RBNZ noted multiple times in the recent Monetary Policy Statement that they are “confident” it is on its way back to 2%.

"But the fact is, the economy surprises forecasters all the time, and we’re keeping an open mind."

In terms of the overall survey results, Zollner said business confidence fell 5 points in February, but at 59 it is still very strong. "Overall, the activity indicators across the survey are solid."

The inflation indicators were mixed. The net percent of firms expecting to raise prices in the next three months fell 4 points to 53%, giving up about half of last month’s jump, while the amount by which firms expect to raise prices eased a touch from 2.1% to 2.0%.

Expected wage growth is rising, and the net percent of firms expecting cost increases (79%) is the highest since July 2023.

"Economic momentum continues. Reported past activity (the best indicator of GDP) remains high, though the volatile construction sector saw a sharp fall," Zollner said.

"Reported past employment was mixed, higher for manufacturing but lower elsewhere."

The sharp turn in interest rates seen from late-November until mid-February has had an impact on the Business Outlook survey – expected credit conditions and profitability have taken a hit, and past activity has also seen a bit of a wobble, Zollner said.

"But with the RBNZ having engineered an easing in monetary conditions last week, it will be interesting to see if these indicators stabilise next month."

9 Comments

Just got notice from Nova, our kwh will go from 23.416cents to 26.339 ex gst.

11.2% inflated price. CPI below 3% , yeah rite.

Our changes on 1st April with Meridian: (inc GST)

Daily charge - 155.04c to 172.29c.

c/kWh - 30.52 to 33.88.

Solar will be on the to do list once we get the house double glazed/re-lined.

Genesis

Daily $2.6749 to $2.3756 (!!)

$/kWh $0.2352 to $0.2539

Gas 45kg refill $152.17 to $147.83 (!!)

Ours lines charges are going up 15c per day form 1/4/2026. Irritating, but the solar buyback from summer should still help subsidize the winter bills hopefully. Either way, it just keeps reinforcing that the decision to get solar was a good decision and should be worth considering for others.

Morning mantra chant at RBNZ headquarters: 'inflations coming down, inflations coming down'

😅🇸🇪🥂

You make it sound vaguely like a cult.

Oh. Wait...

There is a real disconnect between the forcasters/economists rose tinted view of the world and the real world of working people, struggling to make ends meet. It's amusing when they say they are "surprised" when the hard data lands. In the real world, living costs across the board are rising unabated. Food prices are rising on average 2.5% per month. In this reporting season company profits are lauded. But this is not because of efficiencies or increased productivity, its because the companies have increased their prices well over inflation by multiples. A recent case in point example; Sky have announced a profit lift, but Skys big cash cow Sky Sport Now have increased their subscription prices 37% from April 2023 to April 2026. This fact is never mentioned when commentators talk about rising company profits, they then make the claim it is a strong sign of our economic recovery.!

Powershop (Meridian) has told me our bill will increase about 12% from 1 April. It breaks it down to half for the Transpower/local network costs and half theirs, generation, retail, meter etc. I believe that, I've followed the Transpower information about its impact, on its website.

Meanwhile the supposed 'large profits' of these companies are touted by the ignorant as a reason not to put prices up. My Genesis shares are down 30% from 5 years ago, driven by the 22% cut in the dividend a couple of years or so ago. In the past two years, annual dividend increases have averaged 2.5%, under inflation. So that's the position of the owners of these companies, supposedly delivering profits that would stop price increases. Some financial comprehension from journalists, Consumer NZ etc would be useful.

Increased revenue from price increases is going to the grid upgrades needed mostly for new solar inputs and to catch up with long delayed maintenance, as well as investment in new generation by the 'big four'. Their expenditures are in their annual reports and even the paper most days. Much of new investment is for adaptation to climate change - more electricity for everything - and it should be no surprise that this adaptation is not free. Climate change costs emerge in energy costs first, and mostly, and we should accept and deal with this, not deny it with pfaff about profits being big, which is incorrect and illusory in practical terms, as demonstrated.

Given the sheer volatility of the figures, how big is the sample?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.