Well, you might have expected it would be bad. And it's REALLY bad.

The latest ANZ Business Outlook Survey, which takes in the full month of the Middle East Crisis, has shown a marked deterioration in the confidence of New Zealand businesses, coupled with a surge in inflation expectations.

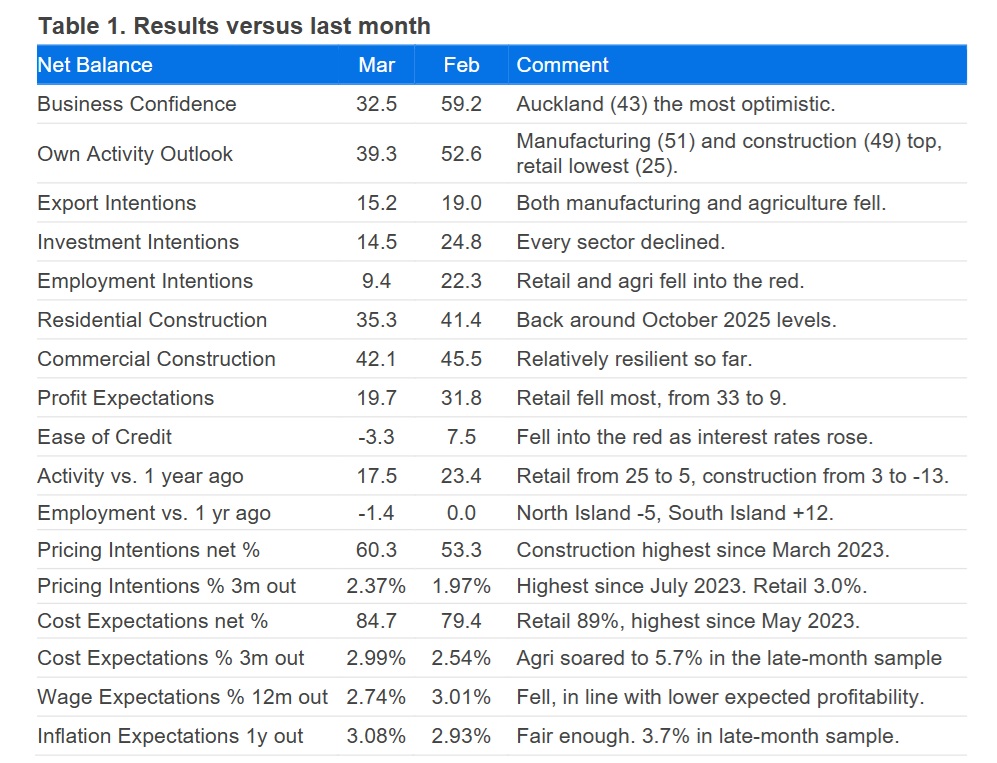

ANZ chief economist Sharon Zollner said the headline business confidence measure fell 26 points in March, down from 59 to 33.

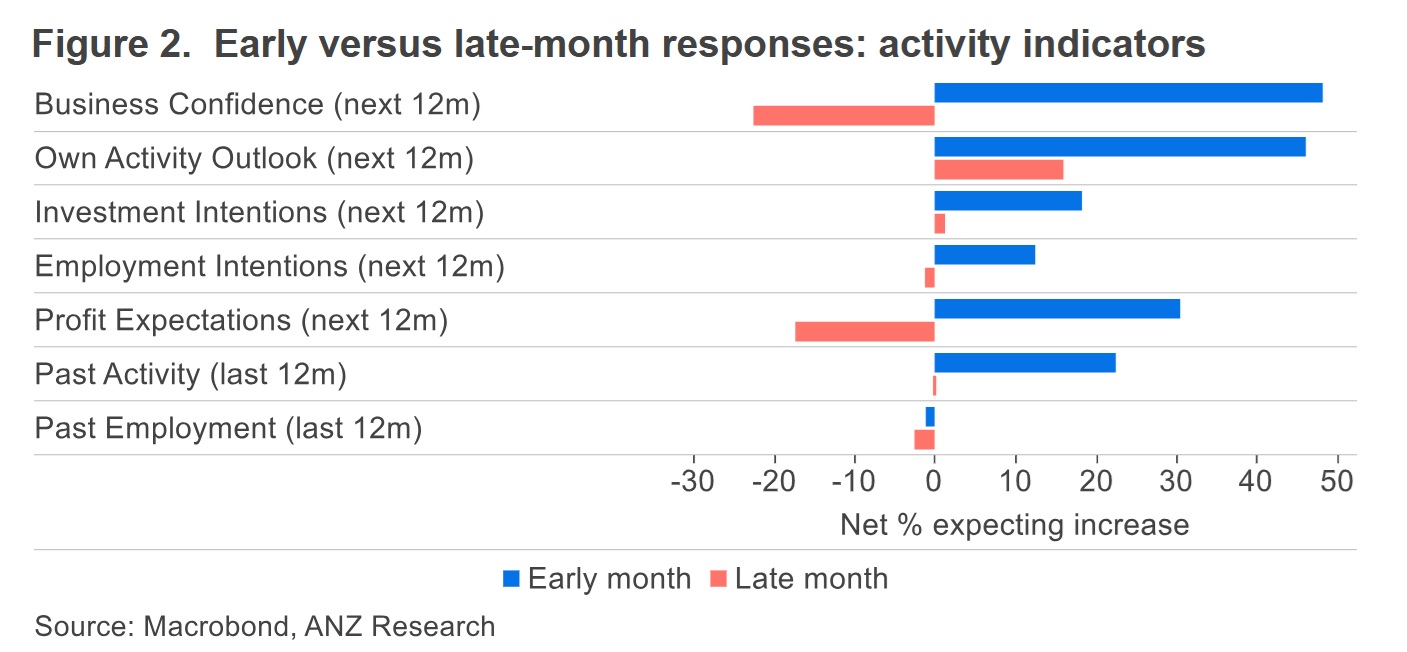

However, the late-month responses actually had an average score of minus-23 as businesses digested the potential implications of the Middle East shock - and realised that it was not likely to be short-run.

Zollner said the bulk of the latest survey responses were collected the day after the Middle East conflict began.

"However, around a third of responses came in following an email reminder on 23 March, enabling us to get an idea of how things evolved as the month went on (while noting that due to the smaller sample the late-month data is more volatile).

Forward-looking activity indicators dropped sharply as the month went on, while cost and price indicators rose.

"Nothing surprising there. Of the activity indicators, business confidence (which asks about “general business conditions”) took by far the largest hit over the three weeks in question, while profit expectations also went well negative.

"But arguably of most significance, the past own activity read was much weaker in the late-month sample, suggesting that some firms are already feeling the impacts. It was broad-based: every sector saw a sharp fall in this indicator. Retail and construction saw the biggest falls, but we would note the data is very volatile when split two ways, so we will stick to hand- wavy comments on that front," Zollner said.

She said in terms of impacts already being experienced, past activity fell from 23% to a net 18% of firms reporting stronger activity than a year ago, with a particularly sharp fall for retail (down 20 points to +5) and construction (down 16 points to -13).

"Late-month responses averaged 0, not boding well for next month," she said.

"Inflation indicators were higher, unsurprisingly. The net percent of firms expecting to raise prices in the next three months rose 7 points to 60% (67% in the late-month sample), while the average amount by which firms expect to raise their prices rose from 2.0% to 2.4% (3.3% in the late-month sample).

"The net percent of firms expecting cost increases (85%, up from 79%) is the highest since early 2023, while a monthly number equivalent to the late-month read (93%) hasn’t been since mid-2022."

Zollner said it was unsettling times for businesses.

"Just as the economic recovery was starting to feel real, dark clouds have gathered," she said.

"It’s not just anxiety about the future; many firms are already reporting that their activity has taken a hit as people defer their decision-making in the face of uncertainty."

The fall in the activity indicators as the month went on is understandable, as it has become increasingly clear that this is not a short-lived shock, but something more persistent, she said.

"Firms are understandably in a mood to reduce their risk-taking – but the unfortunate truth is that one firm’s risk (a purchase, an investment, a hire) is someone else’s opportunity."

22 Comments

All in an election year to boot. One can only wonder what interest rates will be by Nov 7. If nothing happens, NZ will be in a grip of inflation storm that can easily roll the govt back to the ones that printed and wasted 100b.

Don't lose your jobs and hope your tenants dont either.

🍿

Yeah was looking at this before and thinking 'well it wouldn't surprise me if mortgage rates are in the 7-10% band by the end of the year' - with the RBNZ scrambling to raise rates rapidly after refusing to do so in the first half of the year as they deny what is unfolding around them while simultaneously saying 'we've learned the lessons from 2021-2023'.

Yep I reckon a 0.25% rate raise now would set the right tone, a 0% wait and see is just adding kindling to the fire.

7% maybe...CPI getting into the 5's this year is probable, OCR going up 100bps over the rest of year (if the RBNZ are proactive) could happen...that would be around 5.5-6.0%(ish) one year retail rates?

Lets say they do what you're asking for...hiked high enough to give you that 10% retail rate (8%ish OCR?), it won't move the dial on what we pay at the pump so you'd have 10% mortgages alongside $3.50/$4.00 diesel/petrol...I'm interested to hear the roadmap to prosperity from that point...it seems like scorched earth demand destruction...people can't afford anything other than petrol...I guess that eventually shrinks the CPI 🤔😂

"Lets say they do what you're asking for"

To be clear, I'm not asking for anything. Just describing how the system works and possible outcomes given current context and potential developments.

RBNZ could keep OCR low, but wholesale rates could well just keep ignoring them and become completely detached. The more they do this, the more embedded inflation may become.

The last time the OCR and the 1&2 year swaps became this detached was in 2021 and we know how that turned out.

My apologies, it seemed like you were advocating for this so I made an assumption it was what you wanted.

I agree that the OCR should be raised, but I am talking about two or three 25bps rises over the next few meetings, its token but it does bring the OCR closer to swaps, sends a shot over the bow of those businesses who are seeing this an opportunity to try to price gauge, might strengthen the kiwi slightly...it wouldn't do much to retail rates so shouldn't take capacity out of the economy (as we discussed swaps are doing this anyway) but it would at least make the RBNZ look like they are actively trying...it risks further denting sentiment I guess and what damage to "the" recovery could that do?

An aggressive hiking cycle with the current state of the economy scares the sh*t out of me thinking about the destruction it could create...although with their track record the eventual following stimulus could be exciting! 🤦🏻♂️

The major concern with rates going that high is that this time around the economy isn't growing at 3-4% like it was during the last hiking cycle.

Apparently it is - 3% in North Island and >5% in South Island.

RBNZ: nothing to see here, inflation will go back to 2% in the medium term.

Yeah like 2028 after further destroying the value of peoples savings and incomes, thus further destroying living standards (which is exactly what inflation is, where the money you have, buys less of the things you want/need).

It is, but this is supply side inflation.

Monetary policy is way less effective against supply side inflation.

Was monetary policy effective at solving 3 decades of supply side deflation? (where the economy was flooded with cheap goods and services and our answer to solving this was to increase aggregate demand by increasing the money supply via private debt/house prices).

It deferred the rationalisation of our currency and labour market.

And over a supposed 3 decade span, not 3 months.

It started off as supply side last time didn't it (I remember paying $3.30 for 91), supposedly transitory.

Wasn't monetary policy invented after the oil shocks in the 70's?

Monetary Policy has been around for centuries.

Last time you had a perfect storm of supply and demand side inflation. Supply side due to COVID, and demand side due to COVID stimulus.

There isn't much a government can do to make your money worth more relative to something that's in short supply. It should only lose value.

You can make your currency worth more than other currencies by having higher interest rates. Probably not much more though.

Perfect. Imports are cheaper and houses will be as well. Go JJ.

The highest cash rates are held by Turkey, Argentina and Russia.

Do they prove or disprove this theory.

Neither really, as you’d need to know what their currencies would be worth with lower cash rates. Just because their currency is shit, doesn’t mean it couldn’t be shitter. I wonder how they got into that situation in the first place?

Poor leadership mostly.

Also based on risk of the sovereign state defaulting. Small default risk and high rates means in demand. High risk and high rates not so much.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.