ASB has posted a 7% rise in interim profit to a fresh record high, with income boosted by customers paying fees to break fixed-term mortgage contracts in a falling interest rate environment.

ASB's net profit after tax rose $30 million, or 7%, to $474 million in the six months to December 2015 from $444 million in the six months to December 31, 2014.

Parent Commonwealth Bank of Australia (CBA) said ASB's operating income growth of 7% was boosted by favourable other banking income (IE not interest income), and strong lending and deposit growth. Other banking income surged $42 million, or 23%, to $228 million.

This was boosted by stronger markets performance and what CBA describes as "higher fixed rate loan prepayment cost recoveries," or as ASB puts it; "a recovery of the cost of unwinding the swap and a loan condition that the customer agreed to when taking out the loan." For customers this effectively means paying fees to break fixed-term mortgage contracts, as reported by interest.co.nz in November.

'Not a fee'

CEO Barbara Chapman told interest.co.nz "a lot" of the bank's other income increase stemmed from "cost recovery" as customers broke fixed-term loans.

"I think if you took that out the increase in other banking income would be closer to the 7% mark. So a lot of it is due to that," said Chapman. "(But) it's not a fee. It's factually an unwind of the hedge associated with that fixed rate loan. At ASB we account for that differently to our competitors. So we put the recovery of the break cost from the customer in as 'other banking income' and unwind the hedge through our interest expense line. Whereas other banks net it off all in their interest expense line."

"So that impacts on our margins. The other banks will be putting the recovery they get from customers through as an 'interest off set' so their margins will naturally look higher than ours do. It's just a different accounting treatment," said Chapman.

ASB says the composition of its home lending book has remained reasonably stable at around 77% fixed versus floating.

Net interest margin falls

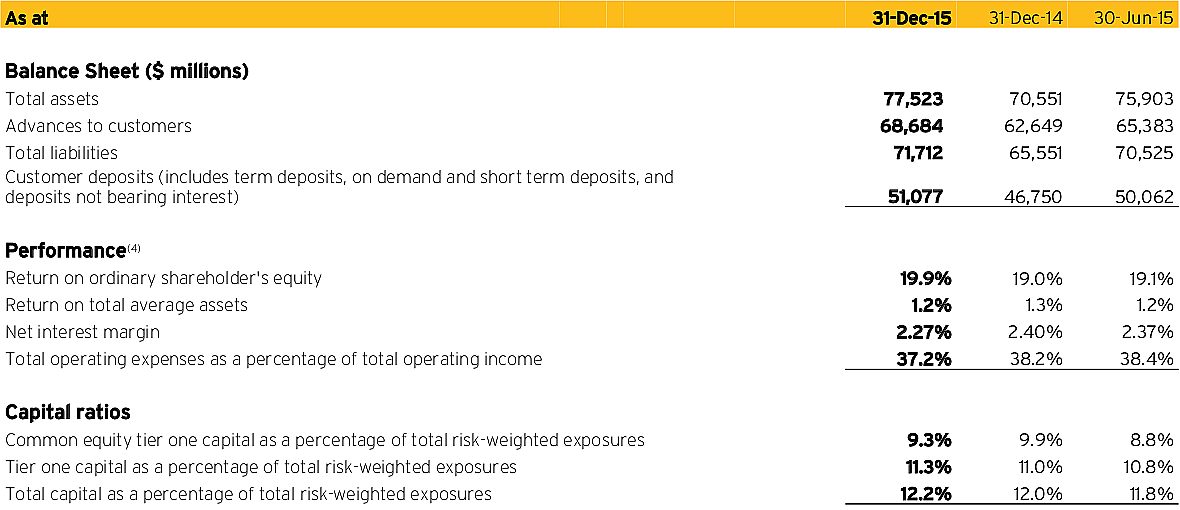

ASB said its net interest margin dropped 13 basis points in the six months to December 2015 from the same period a year earlier to 2.27%.

"The largest single contribution to the change in net interest margin is the trend of customers taking advantage of the current low interest rate environment," Chapman said.

"Against the background of a highly competitive market for both lending and deposit products, we have also seen a continued customer preference for lower margin fixed-rate mortgages."

The bank's expense to income ratio was down 100 basis points to 37.2%.

Home lending up 8%, business & rural lending up 14%

ASB grew home loans by 8%, which was in line with the market, to $45.662 billion, and business and rural lending by 14%, above the market, to $21.310 billion. ASB's loan impairment expense rose 11% to $41 million, largely due to an increase in rural lending provisioning in the dairy sector. Customer deposits rose 14% to $48.524 billion, and total assets and total liabilities were each up 10% to $77.474 billion and $70.030 billion, respectively.

Interim net interest income rose 3% to $844 million, with total operating income up 7% to $1.1 billion. Operating expenses rose 4% to $414 million with technology and frontline investment rising, plus inflation related salary increases given as the reasons.

Rural book 'sound'

Of ASB's dairy loans, Chapman said the rural book "remains sound, reflecting good credit management."

"Our priority has remained on looking beyond the current cycle and supporting our customers in the sector as they manage their farms and businesses through this challenging period. That said, we have increased our level of provisioning for the rural portfolio to reflect the challenges the sector is currently facing," Chapman added.

Funds management income rose 17% to $42 million, with funds under administration - on a "spot" basis - up 16% to $11.731 billion. Chapman said ASB's cross selling efforts were paying off with about 40% of customers now having ASB wealth and insurance products.

ASB

ASB/Sovereign market share

Dec 2015 June 2015 Dec 2014

Sovereign profit down, insurance income up

CBA said New Zealand insurer Sovereign's interim cash net profit fell 5% to $54 million due to lower investment returns and higher lapse rates. However, insurance income rose 15% to $123 million, boosted by annual inforce premium growth, positive claims experience, and reduced policy liability expense following the expiry of transitional tax relief.

Meanwhile, CBA itself posted a 4% rise in interim cash net profit after tax to A$4.804 billion. It's paying a fully franked interim dividend of A$1.98 per share, and CBA's return on equity came in at 17.2% versus ASB's 19.9%. CBA's net interest margin dropped five basis points to 2.06%.

ASB's interim cash net profit after tax rose $37 million, or 8%, to $475 million.

Here's parent Commonwealth Bank of Australia's announcement. And here's ASB's press release.

3 Comments

Meantime banks keep interest rates high despite slumping swap rates. Bank margins at record levels and widening rapidly as swap rates drop - why are we not seeing 3.75% published mortgage rates for 2 or 3 year terms?

because us shareholders want our profits and we come before borrowers

and don't forget banks aren't charities.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.