Standard and Poor’s (S&P) warns banks’ profits could be in for a hammering if dairy prices keep souring and Auckland house prices keep soaring.

While the threat is big, it says banks are strong enough to take the hit.

The ratings agency has drawn this conclusion in a report released today, ‘Will home and dairy prices sour the performance of New Zealand banks in 2016’.

Dairy debt a worry

It recognises dairy farms are struggling with losses amid depressed prices.

Dairy prices fell for the fourth time in a row at last week’s fortnightly GlobalDairyTrade auction.

While the price of Whole Milk Powder is 19% above the low it hit last August, at US$1,890, it’s still 62% below the level it was at in mid-February 2014.

S&P says: “After a prolonged slump in dairy prices, many dairy farmers have incurred operating losses.

“About 10% of New Zealand banks' lending is to the dairy sector, which accounts for two-thirds of agricultural loans.

“A further 10% of these farms accounted for about one-third of total dairy sector debt; these farms tend to have higher levels of debt relative to output, leaving their operating cash flows exposed to downturns in their sector.

“Should lower dairy prices persist, we believe banks would have to raise their provisioning, which would be detrimental to their profitability.”

S&P notes most forecasts suggest prices will in fact remain low this year, yet it says a cut into banks’ profitability will be “manageable within the current ratings”.

It says that as the global supply and demand imbalances eventually unwind, “dairy prices will revert to their long term trend and that New Zealand farmers are likely to benefit more strongly from their low costs of production.

“We also observe that the devaluation of the New Zealand dollar in 2015 has helped local dairy farmers cope with lower product prices and demand.”

Continued house price inflation an unlikely threat

As for the effect of rising house prices, S&P says New Zealand banks would be more vulnerable to a sharp correction in property prices, if prices spike.

REINZ figures show the national median house price hit a record high of $484,650 in September last year, while the median price in Auckland hit a high of $771,000.

Yet it believes signs of a slowdown are emerging in Auckland and prices will stabilise.

“We anecdotally observe that a recent decrease in demand from Chinese buyers occurred in part due to foreign buyers having to register with the New Zealand Inland Revenue Department and an increased scrutiny of capital outflows from China,” S&P says.

REINZ figures show the national median house price has dropped back to $448,000, while the Auckland price has fallen to $720,000.

S&P goes further to say it expects the other key property price drivers to remain unchanged from 2015.

It believes the high demand for residential mortgages will stay, as long as low interest rates remain. It also expects strong migration to keep fuelling demand for houses in Auckland.

“We do not foresee an immediate change in the central bank and regulatory response over the short to medium term.

“In our view, regulatory actions such as loan-to-value ratio “speed limits” and curtailments on investor lending did, to an extent, counter the rise in residential house prices. We are also of the view these tools have a lagged effect.

“We also believe that the curtailment of high loan-to-value lending will support the resilience of residential mortgages portfolios for the banking system in a downturn. That said, New Zealand household indebtedness remains elevated, evidenced by high private-sector debt levels.”

It says that even though the risk of further housing inflation remains low, “a further increase in credit pressures will not result in a revision of the anchor assessment for banks operating in the country but may have a bearing on the risk-adjusted capital ratios we calculate for individual banks”.

Banks profitable enough to weather any storms

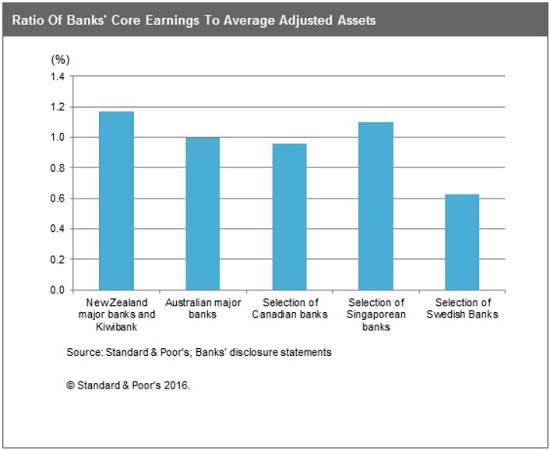

S&P says banks are profitable enough, relative to their international peers, to deal with these housing and dairy risks.

“Given the oligopolistic nature of the system and absence of overcapacity, we do not foresee that banks would be taking on undue risks even though some margin pressures may be looming on the horizon,” it says.

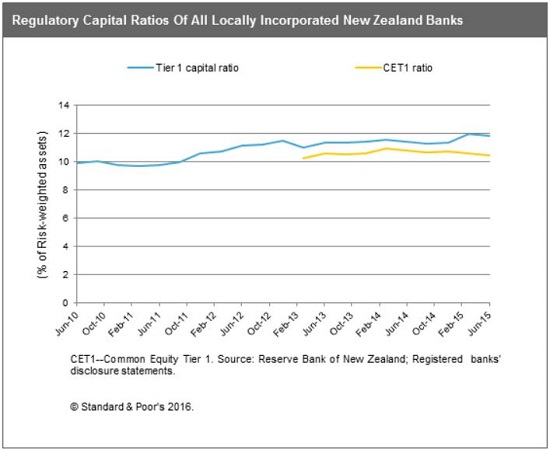

It maintains banks also have enough capital; their level of capitalisation being up for review by the Reserve Bank of New Zealand (RBNZ) again this year.

Furthermore, S&P notes the RBNZ has conducted “high-level stress tests” on banks’ dairy exposures.

“We also observe that the banks are being encouraged to work with dairy farmers that are under stress and that lending to these customers occurs on the basis of expected profitability should dairy prices recover, thus avoiding a kneejerk reaction that might put the industry into a tailspin.”

S&P notes that the rating of the New Zealand subsidiaries of the four major Australian banks, remain on par with each other.

Therefore any major pressure on the parent bank issuer credit ratings are likely to be mirrored in the New Zealand subsidiary.

In other words, S&P warns that any weakening in government support for Australia’s major banks may hurt the ratings of their subsidiaries here. However it says the chances of this happening are slim.

“In our view this is likely to occur if the Australian government develops and implements a more comprehensive bank-resolution regime, particularly if it confers wide bail-in powers for the regulator,” it says.

20 Comments

Anything from S&P is not worth a damn and that was well established after 2008 so .....I ask why the hell is this so-called credible website entertaining their garbage opinions on credit worthiness?

Seriously? Do you take us for idiots?

Well said.

Having said that though, their conclusion is one anyone could have reached anyway. The huge profits the banks are reaping out of NZ clearly puts them in a strong position. Combined with their willingness to loan money against exorbitant house prices and record milk solids pay outs, they are at least complicit in the current situation. They are effectively the driver behind the wheel of a speeding car. They were capable of applying a brake to reduce the speed, but have chosen not to.

The ultimate regulator is the RBNZ and they are more interested it seems in the ambulance at the bottom of the cliff (NZ depositors taking losses with OBR) rather than preventing by more prudent regulation.

In the meanwhile, the current huge profits (and more) are expatriated to Australia and retained earnings in NZ are reduced and provisions for bad debts are minimized. It's a one way street with NZ depositors propping up the banking system in both countries.

Do the regulators actually have the power to regulate depositors which is what they are actually doing?

The RBNZ issues all banking licenses in NZ and can regulate in virtually any way they want to insure stability of the banking system.

There are some regulations which would probably be avoided for political reasons - but not for legal reasons.

In the past few years they've prided themselves on 'light handed' regulation on the basis that it has worked so far.

But the overall result is a propping up of residential property investment and more recently dis-incentive for savers - and no security for NZ depositors. That is entirely under their control.

You missed my point Billsay....as you say yourself the RBNZ issues the banking licenses and what I'm saying is there is no contractual arrangement between depositors and the RBNZ. Is it possible that depositors are in the business of banking and should therefore be registered entities? Are depositors advancing money and therefore required to be registered as a bank? The RBNZ is regulating an activity that is carried out and that position and conduct has never been challenged in a court of law and if there is an OBR I'm guessing that there will be some kind of court challenge and will that challenge see great big gaping holes in the RBNZ?

The RBNZ Act states that it is the RBNZ who are to be lenders of last resort.

The primary function is to maintain stability in the general level of prices and promoting the maintenance of a sound and efficient financial system......An OBR would suggest they had failed in their duties as outlined under the purposes of the RBNZ Act. You have either maintained something or you have let it go, abandoned, neglected, squandered it. So again an OBR could see court challenges as the maintenance side could be deemed absent.

Exactly, as S&P will tell you in court, these are just their opinions, and opinions are not facts, but liable to change as new information comes to light.

As for your final question, the answer is yes, and they are mostly right. You don't need to look further then John Key to work that out.

Everyone is entitled to their views. But all the same, their ratings are still relevant in the real world. So that makes what they think relevant, and useful content here. We run views from a wide range of sources (and allow some pretty out-there views to run in the Comment stream). We are not about to withhold opinions just because some people don't like them.

Whatever you think of credit ratings agencies, their ratings still influence the cost of debt for the government, NZ banks & companies and therefore our mortgage rates as well...

Bank of America is partnering with Freddie Mac on yet another scheme that will allow borrowers to get home loans with as little as 3% down.

"Bank of America is rolling out a new-mortgage product that would allow borrowers to make down payments of as little as 3%, in a move that would represent an end run around a government agency that punished the bank for making errors on similar loans," WSJ reported, earlier today. "The new mortgage program, which the Charlotte, N.C.-based lender plans to unveil on Monday, will let borrowers avoid private mortgage insurance, a product to protect mortgage lenders and investors that is usually required for low-down-payment loans and that could make the new loans cheaper than those offered through the Federal Housing Administration." Read more

Freddie Mac is heading for more than just a credit downgrade, that will never happen.

Just proves that if the regulators don't do their job by putting a leash on the banks, then they will find a way to circumvent the rules. Bob Dylan said best - "When will they ever learn?"

Having said that this site is not evangelising.

They are simply reporting what S & P said.

We have all seen The BIg Short but I for one am grateful this site does not censor what what they report.

Reporting what a proven corrupt and utterly incorrect rating agency says only gives such organizations oxygen to continue with their quite criminal bs. That's the main issue I have. Why feed the weeds?

The imbalances continue....when are they going to correctly value the risk.......what about the derivatives or is that of no concern because we have bail in's called OBR? Around the 19 min mark this CEC report directly references NZ and the RBNZ's OBR.

Its all wallpaper on the toilet wall!!

People are lazy and crazy.

People still listen to the Pope.

People think Janet Yellen has a clue.

People think the United Nations means something.

Just add S@P et al to the mix.

Note that the vertical axis of the capital adequacy ratio graph says Risk - Weighted assets. Note the word weighted. The actual un-weighted figure may about 1%. This is the same method that was used to evaluate the debt instruments that went belly up in the GFC (1). As per last time, when it hits the fan, suddenly everything is in trouble and the so called risk weighting goes out the window. Do they ever learn? You would think S&P would know better. It is after all their business to asses risk properly.

Standard and Poors sees stabilization in the Auckland housing market but is concerned about New Zealands high household debt. Talk about obfuscation. Auckland has gone on debt binge , whilst for the most part since 2008 the remaining New Zealand households have deleveraged or at least not significantly altered their debt loads. I estimate Auckland currently accounts for 64 percent of New Zealands household debt equivalent to 145 Billion. When we talk about household debt to income , it is not New Zealands numbers that matter , it is Auckland. Again I estimate that household ownership in Auckland currently is around 56-57 percent, the lowest nationally, which ironically means that Aucklands average income is skewed on a national scale by rental income. Given that we still have no numbers on foreign (Chinese ) purchasers cash or otherwise, fewer Aucklanders have simply have taken on increasing debt loads to push average household debt /income well over 300 percent and for those Aucklanders who actually own property the numbers for this concentrated group are a time bomb. To enable the increase , Auckland has taken on interest only mortgages, this is the area the RBNZ should have focused on alongside mortgage/income ratios whist the government focused on offshore purchasers.. I used to love musical chairs at parties. How many chairs are left

Well has S and P decided yet if Deutsche Bank going to be the new Lehman? Or is it too close to the "melting core" of the Derivatives fiasco to approach...

"The silent bailout of the German banking system, which started before the Greek debt crisis blew up, has been underreported to say the least by financial media. None of these bailouts attracted the attention of regulators in Frankfurt and legislators in Brussels."

(Wolf Street comment stream)

Are the rating agencies still being paid by the banks ?

In my real world for any dairy price to be 164% below its peak means it must have reached zero and gone negative.

That is some achievement!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.