BNZ's annual profit has fallen 12% largely due to a drop in trading income from the bank's markets business, and losses on hedging derivatives from a stronger New Zealand dollar and interest rate movements.

BNZ's September year net profit after tax fell $125 million to $913 million from its record high of $1.038 billion last year.

Net interest income rose 1.3% to $1.757 billion. However, total operating income dropped $163 million, or 6.7%, to $2.269 billion driven by a $216 million, or 67.1%, fall in gains less losses on financial instruments to $106 million.

Operating expenses rose $24 million, or 2.8%, to $889 million, and impairment losses on loans fell $8 million, or 6.3%, to $120 million.

| BNZ performance measures | Sep 2016 | Sep 2015 | Annual change |

| Net profit on average assets | 1.01% | 1.27% | down 26 basis points |

| Net interest margin | 2.19% | 2.33% | down 14 basis points |

| Cost to income ratio | 39.2% | 35.6% | up 361 basis points |

BNZ attributed seven basis points of an 11 basis points net interest margin drop in the second-half of its financial year from the first-half to higher funding costs.

Lending grew $6.162 billion, or 9%, year-on-year, to $74.378 billion. Deposits from customers increased $4.752 billion, or 10.2%, to $51.481 billion. Total assets rose 6.6% to $92.541 billion, and total liabilities increased 7.3% to $85.536 billion.

Short-term effect predicted for new LVR restrictions

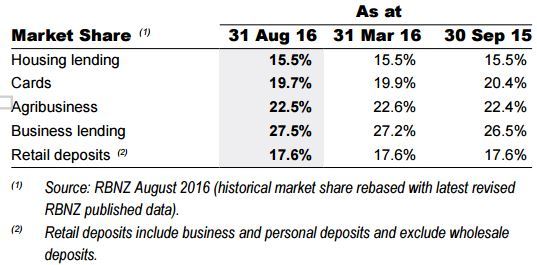

In the home loan market BNZ said it had retained its 15.5% marketshare, helped by $1.8 billion worth of residential mortgages written through brokers.

"Housing affordability continues to be an issue, and as long as migration and supply are key factors the recent [Reserve Bank] loan-to-value restrictions will only have a short term effect. Like all banks, we anticipate that there will be increased pressure on lending margins in the coming months which will influence interest rates," BNZ CEO Anthony Healy said.

Below are BNZ key marketshare figures.

Restructure a productivity push

Healy told interest.co.nz a restructure underway at the bank is taking place in BNZ's head office, and is part of an ongoing focus on productivity.

"Ultimately I think it's about 100 FTE [full-time equivalent staff] net saving so it's not dramatic in a scheme of 4,000 to 5,000 people [employees]. But there's no doubt that the sector is going to get leaner over time," said Healy.

"There's going to be a real focus on productivity because our customers, - what they're demanding of us, and some of the non-traditional competitors that are coming into our market at much lower cost bases, requires us to keep focusing on productivity and getting leaner and reshaping where we put our funding and money and FTE and investment."

Dairy outlook 'could be turning for the positive' as impaired assets top $1 bln

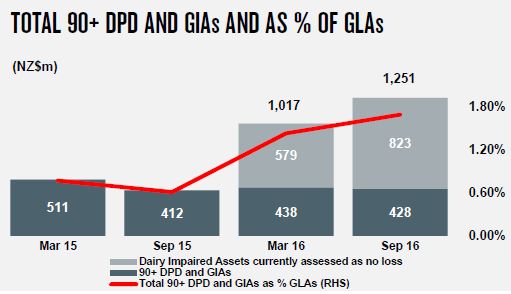

In terms of lending exposure to the dairy farming sector, BNZ said 57%, or $8.4 billion, of its $14.7 billion agribusiness exposure is to dairy. Of this, 56% is fully secured, 43% partially secured, and 3% unsecured. As of September 30, the bank had $1.078 billion worth of gross impaired assets, of which $823 million was dairy loans currently assessed as no loss based on collective provision and security held.

Over the year to September BNZ's loans more than 90 days past due plus gross impaired assets to gross loans and acceptances jumped by 108 basis points to 1.69%.

Healy said BNZ had taken a prudent approach to dairy lending, which he described as market leading, with provisioning decisions taken early.

"The outlook could be turning for the positive, but while there is still some uncertainty we will retain our prudent approach," said Healy.

In the year to September BNZ increased its specific provision for doubtful debts by $8 million to $100 million, and lifted its collective provision for doubtful debts by $67 million to $398 million. Thus total provision coverage to gross loans and acceptances increased by five basis points to 0.74%.

The chart below shows the dominance of impaired dairy loans among BNZ's bad debts.

*90+ DPD means loans more than 90 days past due.

*GIAs means gross impaired assets.

*GLAs means gross loans and acceptances.

Capital bolstered

BNZ's common equity tier one capital ratio stood at 10.21% at September 30. Down 49 basis points year-on-year, this was still comfortably higher than the Reserve Bank mandated 7% minimum. And Healy said BNZ strengthened its capital position this month by issuing $900 million worth of mandatorily convertible subordinated perpetual unsecured notes to parent National Australia Bank (NAB). This issue lifts BNZ's tier one and total capital ratios, at 10.54% and 12.04% at September 30, by another 1.48% each. The Reserve Bank mandated minimums are 8.5% and 10.5%.

BNZ's September year cash earnings rose $13 million, or 1.6%, to $836 million.

NAB posted a 4% rise in annual cash earnings to A$6.48 billion, with its fully franked, final dividend unchanged at A99 cents per share. NAB's net interest margin dropped two basis points to 1.88%.

Here's BNZ's press release. And here's NAB's press release, and this is NAB's investor presentation.

11 Comments

But wait... wait.. what? I thought banks were in this furious margin grab as per quite a few articles on this site. Net interest margin dropped 14 basis points.. suggesting NZ'ers (unsurprisingly) are getting a better deal. Yes its a big profit, but then its a big company employing thousands of people responsible for billions in assets. It's not perfect, and it would be great if more of this profit went to NZ'ers, but its not the massive issue some go on about

some of the profit does go to NZ through kiwisaver, most funds would have some exposure to the four big banks

Now come on Leverageup, that kind of reasoned thinking is not welcome on this site, banks and bankers are the bad guys remember. How dare you use facts and logic to point out that a bank making a profit is actually a good thing. Shame on you....(I will extract my tongue from my cheque now).

Poor Banks, making less profit, I'm almost feeling sorry for them. NOT

"In terms of lending exposure to the dairy farming sector, BNZ said 57%, or $8.4 billion, of its $14.7 billion agribusiness exposure is to dairy. Of this, 56% is fully secured, 43% partially secured, and 3% unsecured. As of September 30, the bank had $1.078 billion worth of gross impaired assets, of which $823 million was dairy loans currently assessed as no loss based on collective provision and security held. "

43% partially secured? That implies some high LVR lending. It would make sense for share millers, but I doubt very much that the BNZ has any more than a few percent worth of its dairy lending to SM's? How did the others get to be 'partially' secured? What is going on?

Now Which Expert or agency is correct BNZ or ANZ

BNZ (Tony Alexander) were mostly getting it right in recent years if I had to pick.

Take you pick :)

You are having a laugh right? Tony Alexmarketer has a terrible track record!

In regards to Real Estate.... He has been largely right for the last 6 yrs... (as far as I can remember)

Yes. Tony Alexander has been consistently accurate

On housing maybe, though let's reserve judgement till after the bubble bursts. And to be fair, it's not been a hard one to call.

How about currency, dairy prices, Brexit.... my problem with tony is he says what marketing want him to say, he's no more an economist than the Briscoes lady

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.