ASB's interim profit for the six months to December has risen by 6% to $507 million.

ASB chief executive Barbara Chapman said the result was the product of "strong momentum" across the business and, "in particular, reflects diversified balance sheet asset growth in key customer portfolios, with total lending up 11% compared to the prior comparative period".

ASB is a wholly-owned subsidiary of Commonwealth Bank of Australia (CBA), which also reported today. In New Zealand CBA also has the insurer Sovereign.

Chapman said despite some challenging market conditions, ASB continued to see robust nationwide volume growth in our business, rural and retail lending portfolios.

"It has been particularly pleasing to see our people and teams right around the country deliver such a strong performance, with sustained growth in markets outside of Auckland," she said.

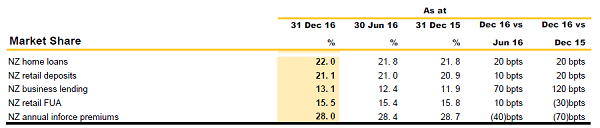

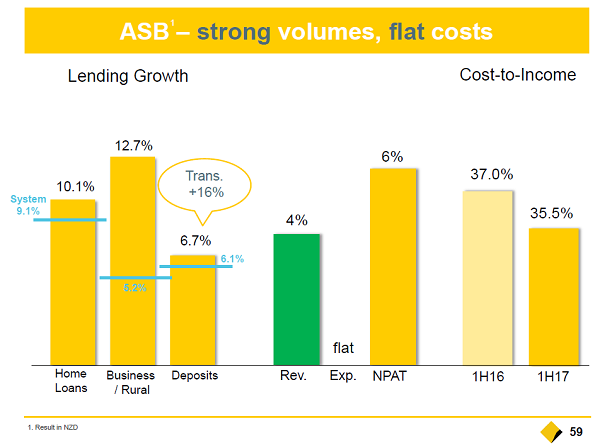

Home loans increased by 10% against the prior comparative period while business, commercial and rural lending grew by 13%. Customer deposits also continued to grow (5%), "despite increased competitor intensity and slowing market growth".

Key financial points

• Cash NPAT of $507 million, an increase of 6% over the prior comparative period

• Statutory NPAT of $525 million, an increase of 11%

• Cash net interest margin decreased by 17bps to 2.21%

• Advances to customers up 11% to $76 billion

• Loan impairment expense was $49 million, up 20%

• Sustained momentum in funds management with income growth of 12%

• Cost to income ratio for six months of 35.5%, an improvement of 150bps

• Costs held flat for the second consecutive half following strong productivity gains

Cash net interest margin (NIM) decreased 17 basis points to 2.21%, which ASB said predominantly reflected higher costs associated with wholesale funding and increased costs relating to customers breaking fixed rate loans.

“As customers take advantage of the current low interest rate environment we are seeing a continued preference for lower margin fixed rate loans,” Chapman said.

“At the same time, banks now are facing a changing dynamic around the increasing volume and cost of international funding needed to meet local lending requirements. With levels of local deposits failing to keep pace with the amount of lending banks are doing, the increased use of offshore funding has increased funding costs, reducing our net interest margin.”

ASB said its operating income growth (on a cash basis) of 4% combined with tight control of operating expenses resulted in a cost to income ratio for six months of 35.5%, an improvement of 150bps over the prior comparative period.

“We have continued to invest in building frontline capability in specialist areas,” Chapman said.

“At the same time we have maintained a strategic focus on leveraging technology to manage costs, improve productivity and simplify our business. With our customers’ preferences shifting to digital channels at an ever increasing rate, our focus has remained on providing them with exceptional experiences, in whichever way they choose to access and manage their finances.”

Loan Impairment Expense (LIE) grew 20% ($8m) from the prior comparative period following increased provisioning, "reflecting strong lending growth and lower home loan provision releases".

ASB said it had finished 2016 "with a number of significant external accolades".

"In December 2016, the bank received the MBIE Diversity Leadership Award at the Deloitte Top 200 Business Awards. The award acknowledged ASB’s clear vision and strategy around building a range of initiatives to embrace diversity of thought and background. In the same month, ASB was named 'New Zealand Bank of the Year' by international magazine 'The Banker' for the fourth consecutive year," ASB said.

In September 2016, ASB began distributing more than 50,000 ‘Clever Kash’ digital moneyboxes to customers who had joined the waiting list for the device. Clever Kash is designed to make saving fun for children and introduce good financial habits as society becomes increasingly cashless. Demand for the innovative device continues to grow.

Meanwhile, insurer Sovereign saw net profit fall to $44 million from $51 million at the same time a year ago.

The whole CBA group recorded a net after-tax profit of A$4,907 million, up 2% on the comparative period.

The CBA full release is here, while the ASB media release is here.

11 Comments

Profit up, interest rates up

Wow , a profit rise like this for a small player is astonishing , their non-performing loans written off ( impairments) are small at just $8 million so it shows a sound book

A small player Boatman? ASB has the second biggest mortgage book in the country.

But i.t.o. total assets ANZ is the biggest followed by BNZ and Westpac , then ASB

ANZ is almost twice the size of ASB .

That's $8m more than the corresponding six months last year, not just $8m.

Difficult to make any real observations on the soundness of their loan book without more information. Home lending will make up the larger number of potentially impaired loans, but the business book will typically be the higher value per item.

They seem to be going after business loans where the margins are better.

shareholders of CBA will be smiling this morning

I have found their service isn't has good as what it was. They also now appear to outsource their cashbox deposits, and I have just had a cheque I deposited into it go missing. Has been a hassle to find out what has happened and I still don't know..

A cheque?

It's probably at the museum.

Yeah probably !. Although it is an international one and the only affordable or easiest way for some companies to pay.

I've heard from people who work there that the culture has been declining...becoming more like a small division of CBA than a Kiwi culture. Perhaps this is having an effect on service too.

i agree - servicing is changing. I had one, good, account manager for 4 years, and since then have had a new, not so good, account manager every 6 months.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.