By Alex Ross*

Kiwi rides the speculative bubble

It was supposed to be a pretty quiet few weeks in markets, but as so often happens over the Christmas holiday period, thin liquidity can drive some exaggerated moves. The Kiwi added another 3.5% since we last wrote on December 21, before topping out at 33 month highs around the 0.73 handle mid last week. The sell Dollar buy anything trade we foreshadowed late last year just seems to keep trucking. Vaccine hopes continue to be the main market driver. Even new strains of COVID, or riots on Capitol Hill for that matter, were seemingly unable to shift the market buoyancy. Stock markets are making for fresh all time highs. Bitcoin hit 40,000 last week. Shares in Tesla are up tenfold from their March low. Are we really in the middle of a global pandemic?

One of the more striking (and incongruent) statistics reported in December was that US bankruptcies dropped to a 14 year low. This news came just as Coronavirus cases were experiencing another surge in the States. Without doubt the US Government’s response to the pandemic has forced the Federal Reserve to add significantly more weight to their dumbbell. The sheer size of the Fed’s balance sheet screams a weak Dollar on a reflation trade. Commodities, stocks and growth linked currencies like the Kiwi and Aussie are the major beneficiaries. But can this reflation trade survive 2021?

All eyes on the Chinese Yuan

Another factor aiding the rise of Asian-Pacific currencies has been the strength of the Chinese Yuan. Last week the Yuan marked its highest level since mid-2018 against the US Dollar. In fact, December marked seven straight monthly gains for the Yuan, its longest run since 2011.

But from Tuesday, the Yuan has begun to weaken as Chinese policy makers sent a string of signals that they may be starting to get uncomfortable with their currency’s continual rise. The People’s Bank of China (PBOC) has now made it easier for mainland companies to make more loans offshore, while they have also cured financial institution USD borrowing.

The PBOC certainly have a few other tools in their kit, such as increasing the QDII quota for overseas investments or loosening restrictions on the annual quota allowed for residents to buy foreign currencies (currently set at $50,000).

So, for now you may say they are merely tapping the brakes on Yuan appreciation. But if they decide to get serious on limiting Yuan strength this can certainly curb or at least cap Chinese appetite of our exports. The surprise moves from the PBOC helped the Kiwi top 4.70 against the offshore Yuan, a level last seen in both January 2018 and January 2019. We think more direct trade from NZD into CNH will grow through this decade.

When will reality bite?

As we cast an eye further ahead into 2021 we have to ask ourselves for how much longer do we think this speculative bubble in risk assets and currencies will last. By and large that sentiment continues to be vaccine driven.

Politically the likelihood of a US Democrat dual house majority can add further stimulus to the mix. We saw last year that in the initial stages this increased spend can be supportive of the risk carousel and therefore is likely to drag the Kiwi and Aussie in in its tow.

But eventually one thing or another must happen: successful vaccines and the sheer volume of stimulus generates inflation leading to central banks thinking twice about a normalisation of policy, or the vaccines are a flop and/or growth fails to pick up and we have an economic relapse. Either way both scenarios present a major risk to asset prices in the back half of 2021, and therefore to current NZD valuations. Granted we think the Kiwi is likely to drive higher in the near term, even if the latter half of January sees a corrective phase, but the current valuations of assets (Bitcoin at 40K, S&P at 3800, property values throughout NZ) just seem so over-hyped and out of touch with economic reality that in the FX world, we have to prepare for the fact the bubble may just burst this year.

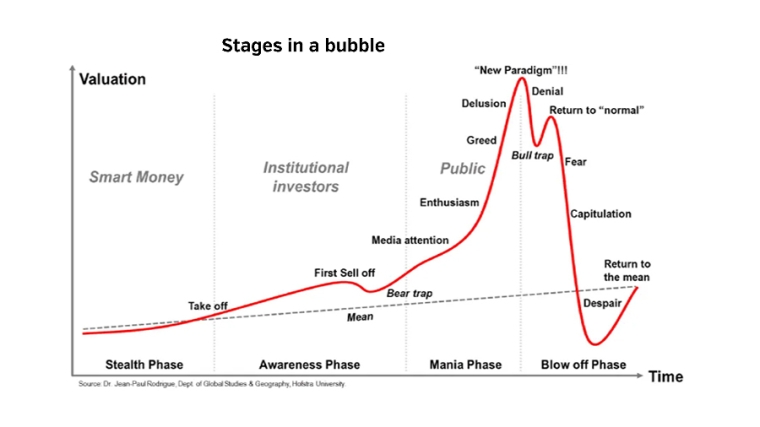

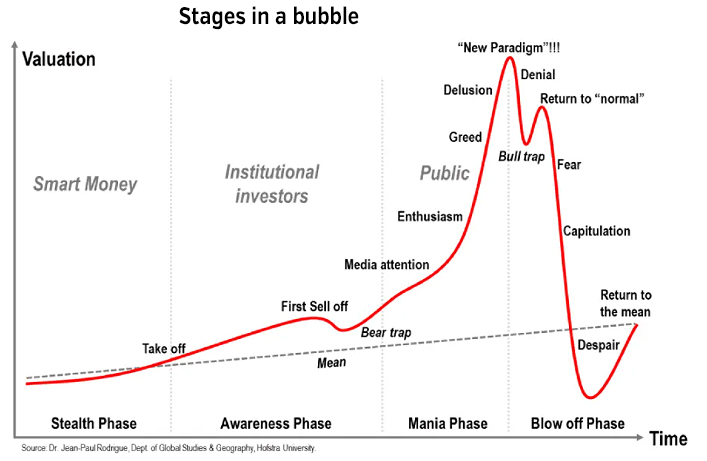

Taking Dr Jean-Paul Rodrigue’s famous model of economic bubbles we think we are nearing the state of delusion.

For us signs of that are evident in seemingly rational explanations being provided for why Tesla stocks have gone up from around $88 to $880 in the space of 9 months, or Bitcoin exploding from $4000 to $40000 over the same period.

While one might postulate that the demise of fiat money could explain some of the attraction of Bitcoin, is a 10-fold surge in any asset over 9 months ever simply rational? We think not, and see such explanations that we are now in a “new paradigm” as further evidence that we are nearing the final stages of a massive speculative bubble in 2021.

In many ways we hope we are wrong but for local importers and exporters we think you simply have to be prepared for anything in 2021, and by and large that means having a risk policy, taking protection against your budgeted rate, but maintaining an element of participation should we see more extreme moves (in both directions) this year.

Alex Ross is Client Manager, Western Union Business Solutions and is based in Auckland. You can contact him here.

30 Comments

Sigh - I now understand why farm prices haven't moved in decades. We don't have any 'smart money'.

I guess Catch 22 applies to NZ agriculture - Only the insane.....

I don't thin k the bubble was allowed to burst with farm land, it just wasn't an option for banking interests. So you just limp along.

Andrew most observers and/or owners know the emphasis went from Capital Gain (on land) to Profitability (on the enterprise). That rotation happened some years ago (at least 5-7 maybe more)

If you can't turn a profit (NPAT) then the enterprise isn't viable - just like any other business. Farms had the CG effect for decades that masked struggling operations

Won't happen to productive land Andrew, unless it's being funded in that devil cycle of irrational exuberance lending practices.

This time it's different!

It won't happen in NZ, because NZ is different.

The market can remain irrational longer than you can remain liquid...Think wit printer going Brrr its going to keep going for a while yet. look what happened after 08, stock market just kept going up.

Great saying and true. Although from 08 the rally has moved in step w/ easing monetary policy - hard to separate the line of lower interest rates w/ increased asset prices. Any predicted rally in equities from here implies further easing which past first half of this year seems hard to believe. The yield curve has steepened quite a bit over the last month and is now positive implying interest rates in the future will be higher (likely flat for a loooong time then higher). Point being the main driver in asset prices (lower interest rates) that was present post 08 is no longer there.

When a bubble is intentionally created by bad policy, more bad policy can be piled on to keep pumping it up.

Inflation will come with a vengeance sooner or later and the central bankers will simply look the other way.

It's already here, just not in consumer prices.

Yes. But consumer prices will follow.

And if interest rates rise even a fraction the great houses of cards will tumble.

Dr Jean-Paul Rodrigue’s famous model of economic bubbles describes the Bitcoin charts between each halving in perfect detail. If that also applies to this cycle we're currently at the Media Attention phase. Outside of the halvings bitcoin will likely follow the technology adoption life cycle in both adoption and price (until it hits peak saturation at which point it will stabilise). At just 2% global ownership BTC is not even out of the innovator phase yet.

The world is desperately hungry for an asset with governance that has immutable rules and that is Bitcoin, where the rules have been baked into the codebase since inception in 2009.

Yes. I'm not convinced BTC is in a bubble, despite it appearing to outperform most other bubbles. But it's all subjective anyway.

But why has it happened now for BTC? You could almost take the perfect storm argument (massive money printing, institutional adoption) alongside the price to time path as defined by the halving sequence.

If it is in a bubble, the big difference is that most owners of BTC should be psychologically prepared for the price to go to zero. That is quite unlike any other bubble. That is not to say the price will or can go to zero. This is the mentality adopted by those who understand asymmetry.

"The world is desperately hungry for an asset with governance that has immutable rules". The world is concerned with sufficient food to survive, and shelter to live in. A very small subset of the money obsessed is concerned with other things - which, for most citizens of the world, are unnecessary luxuries.

All of the money creation is being done by the banks and this indeed is causing inflation but only in house prices. The money from QE is not entering the economy as it is held as bank reserves which are not lent out.

The government could be using fiscal policy much more than it is to maintain jobs and productive output and as long as it is not competing with the private sector for resources then it would not be inflationary.

The Chinese govt issued vouchers for discounts for people to go out and spend (all issued via WeChat). Very successful and far more effective than anything the NZ Govt has done. All the NZ ruling elite knows is mon pol and their dumb house price bubble.

From what I have heard, didn't the US initially send out cheques to people. Many then put it into bitcoin and stocks. Then they decided to send out debit cards, to get people using the money in stores. IMO if NZ is printing money, they should give people a debit type prezzie card, to then spend in NZ. Much of the money the government handed out in the wage scheme apparently ended up in peoples savings, which is not going into housing and stocks.

You are correct - the US Govt sent out US$1200 cheques to everyone. They are now in the process of sending out a further US$600 to each individual. Mr Biden has indicated that he plans on sending out a 3rd stimulus payment (last $ figure was $2000 per person)

Time to take some cream off the table, folks, before it evaporates.

Now, If I can just figure out when to sell my Auckland home ($1m +) & then the next day after settlement the market will crash 50%, so I can buy two houses with my money!!

Not going to happen. Actual physical assets like a house that you can live in and make money at the same time are going to remain a solid investment. Somewhere warm and dry to live and sleep at night is top of the list of just about everyone's list.

Yea, that intrinsic value, peace of minds, to raise family thingies. Like you've said, unlikely to happen when the Financiers were strong behind it/Banks.

.. or is it? - just wonder why the promo of good result from stress test, and all lobbied against CAR, against neg OCR, TD guarantee kind of opposite to their OZ parents somehow. Hmn..

A tent and a sleeping bag will keep you warm and dry for about $600

Prices however could go sideways for a very lng time, which is effectively a drop when you take into account inflation. . House prices can also drop. Maybe not 50%, but if the prices have gone up 20% in one year, what is stopping them dropping 20%, especially if interest rates rise over time. It was baking experts that predicted 15% drop in 2020

Re Carlos67 - Tell that to all those people who were forced to sell their houses as prices tanked after the GFC eg Ireland and USA, including in NZ. I had neighbours forced to sell their houses into a depressed market - small business people who had secured business loans against their house, others who had lost their jobs, or their business income had dried up. A friend of mine told me her bank insisted she stump up cash to reduce her borrowings. She was forced to sell her house and her businesses. The delusion is to think it will never happen here, or “this time it’s different”

It's bizzare to me that the market narrative is "vaccine driven" when the virus is by far outgrowing the vaccine effort. Far more people will get Coronavirus than get the vaccine if you plot out both based on current trajectories.

Well, read again the article.. there's an insertion there with the word... delusional.

Actually the market isn't "vaccine" driven. It's well and truly shrugged off the effects of CV19. Total DR is about 2-3%, not a showstopper. Still 97-98% of consumers buying.

The current DR of 2%-3% is when people are being treated. What happens if hospitals become overwhelmed and have to turn people away? How many people will die from other injuries/illnesses that are usually not fatal when treated but will die because of an overwhelmed healthcare system? Your 2%-3% might rise quickly. The higher transmission rate from this new strains is a big big threat.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.