By Alex Ross*

Trouble in paradise

Let me be frank. Central banks are in trouble. After years of dormancy the inflation beast is finally awakening. As the former German economist Rudiger Dornbusch once said “in economics things take longer to happen than you think they will, and then they happen faster than you thought they could”.

For the last decade reserve banks the world over have been telling us they want consumer price inflation, but they’ve been lying. That’s because their solution to everything has been to lower the price of money, expand their balance sheets, pump up asset prices, and increase global debt.

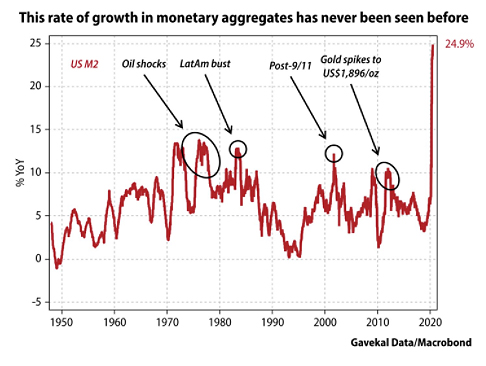

When Coronavirus hit this time last year things went parabolic. This rate of growth in monetary aggregates has never been seen before. Check out the rate of M2 money supply in the US below. The prospect (and impact) of higher inflation predicating higher interest rates is now daunting.

Beware the Cantillon Effect

In the 18th century Irish-French banker and philosopher Richard Cantillon laid out his theory of money supply. Cantillon suggested that an increase in hard money would first benefit those closest to the ruling powers. The wealthier you were the more financial assets you could purchase at relatively low prices and then see those prices inflate.

He suggested that it was only later that the effects would appear elsewhere, and that the further away from the ruling classes that you were the more you would eventually be harmed by higher food prices and lower relative wage increases. If you’ve taken a trip to the local supermarket in the last week you would know the Cantillon Effect is now in full swing.

Bond markets are pricing in inflation

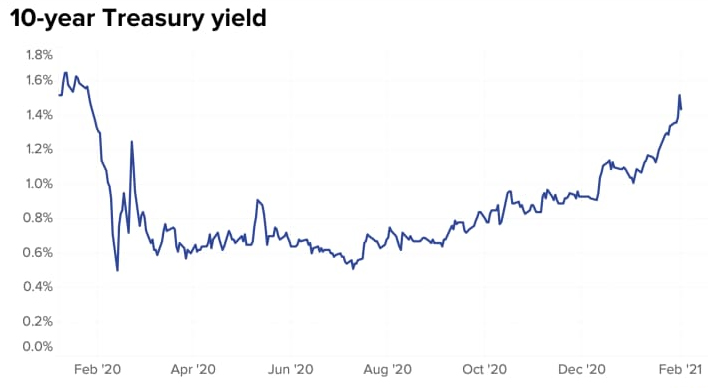

There’s an old saying that the bond market traders are the smartest guys in the room, and the past fortnight has seen some big interest rate moves. Much of the focus has been on the US 10-year Treasury yield. That’s a market that is clearly seeing inflation ahead.

The Biden Government just this weekend finally passed their US$1.9 tln COVID relief package, and there’s talk of another $3 tln to come. Add in an expectation that most Americans will be vaccinated by mid-year and you suddenly have growth differentials tilting in favour of the US.

Source: CNBC

And yet the Fed continue to see their extraordinarily loose policy as still appropriate.

During the peak of COVID they never once queried the rather questionable employment data, but suddenly last week several Fed officials suggested the real unemployment rate might be around 9%, despite official data suggesting it is at 6.2% on Friday night. Inflation expectations surveys are now also being heavily scrutinised. When these prints were anaemic last decade no one seemed to stop and question their legitimacy, but suddenly now that their prints are moving higher attitudes have changed.

The key takeaway from this is that central banks will only be dragged kicking and screaming towards monetary policy tightening.

And markets have now got a sniff of this.

In fact, bond markets are telling you that concerns are growing that the Fed may allow inflation expectations to anchor above 2%, and that the Fed will be forced to take swifter action later due to complacency in the near term. The pummeling of tech stocks in the last week is endemic of this – the longer dated expected cash flows of technology are suddenly more heavily discounted due to rising inflation expectations.

The impact in FX markets

For FX markets (and markets as a whole) the real concern is not the recent move in bond markets but the swiftness of its move.

In just six weeks the US 10-year has advanced from 1% to 1.5%. Where might it be in 6 months? As per our introduction rising yields are a major problem for central banks, not to mention sovereign governments. Higher bond yields simply raise government interest payments on their debt, making it harder and harder to get deficit spending under control.

In the near term we expect the Federal Reserve (and potentially even the RBNZ) to adopt yield curve control to try and suppress bond markets. Should we get that as close as the next Fed meeting (on March 17) then that could lead to another USD weakening phase, propping up risk assets and commodity currencies. At this stage though the Fed have shown no signs of changing tack, and so bond markets look like they may continue to poke the bear, leading to more AUD and NZD losses should US yields continue to rally. Through Asia the Korean Won and Taiwanese Dollar are also being hit hard by rising yields.

A game of chicken

In the end though, there will be no get out of jail card for central banks. As we wrote last week we believe higher inflation is here to stay.

Direct government spending into the economy has ballooned over the last year, interest rates are at all time lows, and supply chain problems persist.

But overall, we think the biggest change through COVID is businesses are no longer willing to operate on lean margins. Cognizant of the fact many were bailed out by government wage subsidies many now want to build up a rainy-day fund. Expansion is a nice to have but making more with less is the mantra. Harking back to Richard Cantillon, money printing has distributional consequences that operate through the price system, and just because those changes didn’t show up immediately doesn’t mean they aren’t coming.

And so, we are now left with a game of chicken. Markets have known for a long time what has been inevitably coming, and bond traders are ready to test central bank’s mettle. Whether they adapt yield curve control or not is rather irrelevant in the longer scheme of things – central banks are now playing game theory with markets thinking they can win, when ultimately markets will be ready to have that head on collision if needed.

In FX that can foster a weird dynamic – a continued reflation trade that is ultimately NZD supportive, punctuated by sharp and sudden sell offs when another bond market spike hits.

In the long-term heightened volatility and a resurgent US will eventually take its toll on the Kiwi, but for now importers and exporters should keep a sound rolling hedge strategy, and when a good rate presents don’t bother waiting for it to get better.

Alex Ross is Client Manager, Western Union Business Solutions and is based in Auckland. You can contact him here.

15 Comments

"At this stage though the Fed have shown no signs of changing tack"

At some stage it was always probable that The Fed, and the wider USA political class, would decide that defending the Reserve Currency, and all the perks that accompany that, would outweigh the cost of protecting asset prices.

That would see asset prices falls significantly, and the US$ soar. But those two things can be temporary.

Losing the hegemony of the US$ would not.

The Shock happened in 2008, The Wave is about to arrive.

It's not that there aren't inflationary dynamics in play; there are. The issue is that not all the dynamics in play are inflationary, and the deflationary dynamics have been building for the past two decades. Funny things happen when we substitute debt for earnings and speculation for productive investment...... interest and principal piles up, even at near-zero rates. Stagnating wages that buy fewer goods and services every year with ever-higher debt loads and monthly payments, and then add in higher taxes, and we end up with insolvent households and enterprises that must borrow more to stay afloat. If they can't borrow more, they default.

Those that can't borrow more can't spend, and that's a problem because the entire economy depends on everyone borrowing and spending more every year. i.e. "growth."

When loans are paid off or written off due to default, the money supply shrinks. That is deflationary.

(CH Smith)

The smart money always wins and virtually never works at the central banks. This is going to get wild.

Isn’t the real question here whether the rise in inflation expectations turn out to be temporary price push inflation due to the much anticipated supply chain blocks of reopening. Or whether a much longer structural swing higher eventuates.

Currency debasement didn’t seem to have a big effect on inflation after the gfc, but this last injection was a lot higher.

The counter argument is of course smart people always finding ways to go things faster and cheaper.

The economic cycle will reassert itself, ultimately assets will be priced according to market fundamentals. The central banks have built asset bubble sandcastles on the beach, and the tide is coming in. This was always going to be the problem: you artificially inflate asset prices....cool. But then you are stuck having to defend what I would term 'structural bubbles', asset bubbles protruding far above an otherwise flat to falling wider economy. This has become the ultimate nightmare during the COVID pandemic, and central bankers have had to throw the kitchen sink into keeping their structural bubbles inflated. Clearly they've created a perverse situation where asset prices have risen further even a the wider economy has been in turmoil.

"The economic cycle will reassert itself, ultimately assets will be priced according to market fundamentals".

Exactly right, and I have been saying this for quite some time. The biggest bubbles (like residential housing) will be the first to burst, and it is going to be an almighty one. All asset prices are currently inflated - bond prices are simply just first to feel the heat (and they will be first to realign to economic fundamentals), but housing is going to be next.

All the RBNZ can do is to keep the housing Ponzi up and running for a little longer, at best.

This is unfortunately the truth. You can't just "invent" money by lowering interest rates and pumping up lending. We don't eat money. You can't live in money. Money doesn't provide energy. It's a means of exchange, and it has to reflect the resources that underpin it.

Central banks may be able to game the system for another year, or 10 years. Who knows. But eventually the chickens will come home to roost.

It all comes back to 2008 GFC. Central banks found there was too much unsustainable debt in the system and it was at risk of collapsing the financial markets. They think the lesson from 1929 was that you can't sudden curtail lending or it will trigger a depression. Unfortunately the lesson they SHOULD have learnt was that a build up of unsustainable private debt, and the resulting asset bubble, made a depression inevitable when it popped. But instead we have central banks that have just doubled down on ramping up debt, and they will just make the inevitable collapse worse.

Our politicians have ultimate responsibility, they set the mandate that the reserve bank has to operates under. It is instructed to maintain inflation to between 1% and 3% and to try to maintain employment levels and Its only tool available is the control of interest rates. The government itself could have been more proactive with the use of fiscal policy to maintain levels of spending in the economy.

From that perspective, I think the issue is that 50% (or more) of the population think they are going to benefit from these policy settings - hence why the status quo has political popularity.

If or when we cross that threshold - which the divide appears to be growing wider - as the pie gets divided and bigger chunks given to the wealthy and less of the pie given to the poor (see the equality stats for the last 30 years) - then politically we need to watch that space. Poor people tolerate being treated badly for a while, then they don't and it can be quite sudden and dramatic.

It makes a huge difference however if its 1 year away compared to 10 years away. I have said it before, nobody will care if the correction is 10 years away. Even if we all know for sure the correction is 10 years away, very little will change right now. Everything these days has a short term focus, its the reason why we are in this mess in the first place. Excellent article, one of the few I have actually read on here.

Tom...well said. Adrian Cantillon Orr?

The chooks remind me of Orr and GR playing their dominant strategies

Governments don't need to issue bonds in the first place, they are only a subsidy for the finance industry. Economist Warren Mosler had this to say in the HuffPost.

Proposals for the Treasury

I would cease all issuance of Treasury securities. Instead any deficit spending would accumulate as excess reserve balances at the Fed. No public purpose is served by the issuance of Treasury securities with a non convertible currency and floating exchange rate policy. Issuing Treasury securities only serves to support the term structure of interest rates at higher levels than would be the case. And, as longer term rates are the realm of investment, higher term rates only serve to adversely distort the price structure of all goods and services.

I would not allow the Treasury to purchase financial assets. This should be done only by the Fed as has traditionally been the case. When the Treasury buys financial assets instead of the Fed all that changes is the reaction of the President, the Congress, the economists, and the media, as they misread the Treasury purchases of financial assets as federal ‘deficit spending’ that limits other fiscal options.

https://www.huffpost.com/entry/proposals-for-the-banking_b_432105

Very well written Alex. Hopefully this article clearly illustrates that the RBNZ does not have control of the direction we go in. They can take measures to slow down the speed we are moving, maybe even temporarily alter the direction in which we are moving but have little control on our destination.

Are you qualified to be inducted into the LOL betting odds hall of fame? Everyone, of course, has it! What should be done in this case? To begin, make sure you've gained some experience and found a site where you can bet on your favorite team. Also these two, however, are not a concern. To assist you in taking the first steps into the professional scene, we have created a dedicated tournament website.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.