Welcome to our first of these daily summaries in 2022. Here are the key things you need to know before you leave work today.

MORTGAGE RATE CHANGES

No changes to report today.

TERM DEPOSIT RATE CHANGES

None here either.

SOPHISTICATED NEW SCAM

Westpac NZ is warning New Zealanders about a sophisticated new scam that involves a fake Westpac investment prospectus. The prospectus is formatted to resemble a Westpac document and includes professional-looking imagery. This is what it looks like. Westpac said the scammers had put significant effort into making the prospectus look authentic. “Would-be investors are encountering this scam when they do internet searches for information about investments and term deposits. These people are asked to enter personal contact details on the websites which come up in the search results, some of which may purport to help people compare investments. The scammers then email or call the would-be investor using those contact details.” They noted written and verbal communications from the scammers used convincing language and appeared credible. “We have had a handful of reports about the scam so far. We want people to be vigilant and report any suspicious activity so our financial crime team can investigate.”

DECEMBER 'PROVES' THE HOUSING MARKET WILL BE DIFFERENT IN 2022

The housing market was considerably slower in December compared to a year earlier. According to the December REINZ data, there was a big decline in December sales and prices were weaker too. Infometrics says the market has turned a corner. Westpac sees the data showing higher mortgage rates and tighter lending restrictions are having an impact. ANZ says the data confirms the market is slowing. Kiwibank says the housing market looks to have finally cracked.

BUSINESS CONFIDENCE TURNS DOWN TOO

NZIER’s QSBO shows weaker demand and confidence. Just as inflation pressures accelerate, business confidence sinks. More than half of surveyed businesses are to raise prices in early 2022. ANZ says businesses are fretting about inflation and the pandemic. "Today’s data is more evidence showing that the labour market and inflation are probably even further beyond the RBNZ’s targets than they (or we) thought when the November MPS forecasts were published." Westpac says "The persistence of inflationary pressures was one of the reasons why we think that a series of OCR increases in rapid succession will occur this year."

RETIREMENT SECTOR STRUGGLES, LOSING INVESTOR INTEREST

Investors who piled into the retirement/rest-home sector expecting easy gains are probably feeling disappointed. Last week the listed companies in this sector lost -3.3% of capitalisation, getting on for nearly twice the overall market decline of -1.9%. Year-on-year these companies have lost -6.0% of capitalisation whereas the overall market has lost -2.3%. Despite only being 8% of the overall capitalisation, these companies have lost -21% of all the past year's pullback, some -$640 mln. The big loser last week was Summerset (SUM, #14) which fell -3.5% in those seven days. But everyone declined - the least was Arvida (ARV, #29) which shed 'only' -2.5% in the week.

FLP ACCESSED AGAIN

Late last week, another major bank dipped into the RBNZ's Funding for Lending facility, taking $500 mln. Bank treasurers are probably feeling the RBNZ could end this piggy-bank availability soon, so if they need the funding, now is the time - certainly before the February 24 MPS. The FLP has now disbursed $7.2 bln of the $28 blnb originally allocated. It costs banks OCR, so at the moment this is funding at 0.75%. Once allocated, they have this funding for three years

LOOKING FOR A FAST FINISH

There is another dairy auction early tomorrow morning, the 300th since this system was started. Since the last event, Fonterra has advised that New Zealand milk volumes will be about -1.6% lower this season than originally anticipated. The peak was well and truly passed now so there is little chance of making the shortfall up. The dairy futures market is suggesting that the WMP price could rise by as much as +9% and the SMP price rise by +3.5% tomorrow. Of course, anything like this will underpin a strong milk payout price.

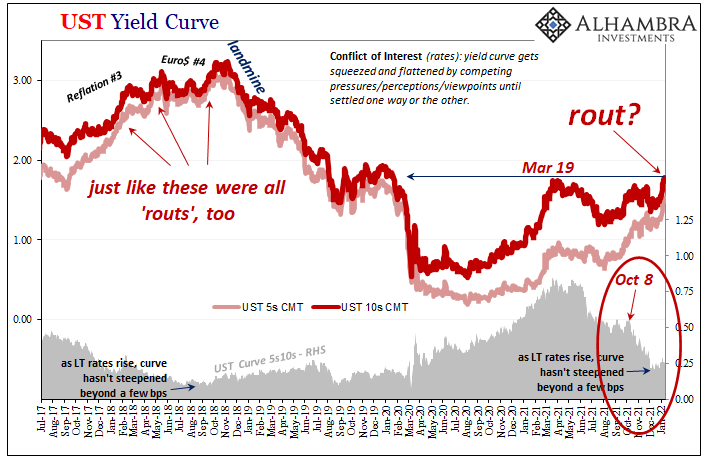

UST 10yr YIELD MARCHES UP

With the US financial markets closed, you might think global interest rates would stay little-changed. You would be wrong. The benchmark UST 10 year yield has risen today to 1.82% and a one year high. There is growing market conviction that the Fed will start raising rates in March, and possibly more aggressively than previously thought. But also see below.

LOCAL PANDEMIC UPDATE - AUSTRALIA'S DEADLIEST DAY

In NSW, there were 16,067 new community cases reported yesterday, a sharp fall, now with 326,356 active locally-acquired cases (and undoubtedly an undercount), and 33 more deaths. There are now 2,850 in hospital there. This is confirming the NSW Chief Health Officer's recent warning there will a high number of deaths in coming days. In Victoria they reported 20,180 more new infections yesterday, and little relief. There are now 235,035 active cases in that state - and there were 22 deaths. A "Code Brown" (mass casualty event expected) has been declared in most major Victorian hospitals. Queensland is reporting 15,962 new cases and 16 new deaths. In South Australia, new cases have risen to 4,685 yesterday with no more deaths. The ACT has 1601 new cases and 1 death and Tasmania 1310 new cases. Overall in Australia, 73,258 new cases have been reported so far although not all counts are in yet. In New Zealand, there were 30 cases stopped at the border, plus 14 new cases in the community.

GOLD FIRM

In early Asian trading, gold is at US$1821/oz and up US$6 from thsi tiem yesterday.

EQUITIES MOSTLY RISING, EXCEPT THE NZX50

The NZX50 is down -0.2% near the close of trading today. The ASX200 is up +0.3% in early afternoon trade. Tokyo has opened up +0.7% in late morning trade. But Hong Kong has opened up +0.6% and while Shanghai has opened up +0.2%. US markets are closed for a public holiday (MLKing Day).

SWAPS UNCERTAIN

We don't have today's closing swap rates yet. They are likely to be little-changed although a jump in the UST 10yr is an unexpected twist for the long end. The 90 day bank bill rate is up +1 bps at 1.05%. The Australian Govt ten year benchmark bond rate is unchanged at 1.91%. The China Govt 10yr is soft at 2.80%. The New Zealand Govt 10 year bond rate is now at 2.54% and up +1 bp but still below the earlier RBNZ fix for that 10yr rate at 2.58% (up +3 bps). The US Govt ten year is now at 1.82% and +3 bps even though Wall Street is closed.

NZ DOLLAR UNCHANGED

The Kiwi dollar is holding at 68 USc and unchanged. Against the Aussie we are also marginally softer at 94.2 AUc. Against the euro we are little-changed at 59.5 euro cents. That means the TWI-5 is still just over 72.2 and unchanged.

Appreciate this coverage? Support us and go ad-free. Find out how.

BITCOIN DOWN AGAIN

The bitcoin price has slipped to US$42,287 and lower by -1.4% from this time yesterday. Volatility over the past 24 hours has been modest at just over +/- 1.7%.

This soil moisture chart is animated here.

Keep ahead of upcoming events by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

84 Comments

https://www.macrobusiness.com.au/2022/01/ardern-looks-to-pump-faltering…

Saw this news article but unable to read as only for subscribers but does it mean that Jacinda with just one data suggesting that ponzi may stall is going all out to pump housing market by pumping mortage.

Comments welcome specially if anyone has access to above news.

If true, Is anyone surprised.

Pump it full of kindness... it's what kiwis expect.

That soil moisture map isn't looking good again, and that's with la nina...

Nothing more than a few showers in the 10 day forecast for Auckland.

Just need niwa to re-benchmark the colours so that it doesn't look so bad. If they are unsure how to manipulate it just ring Stats NZ and ask for the CPI desk.

Yep the old soil moisture deficit will hit again, I'm guessing. Trying to sell stock at the moment but I suppose so is everyone else. Typical hillcountry farming senario.

Late last week, another major bank dipped into the RBNZ's Funding for Lending facility, taking $500 mln. Bank treasurers are probably feeling the RBNZ could end this piggy-bank availability soon, so if they need the funding, now is the time - certainly before the February 24 MPS.

Hmmm....

FLP terms - Under the FLP, the Bank will offer 3-year funding to eligible institutions. The funding will be structured as floating rate Repurchase Transactions priced at the Official Cash Rate (OCR), each for a term of three years.

I thought a "Code Brown" at a hospital ment bring a spare pair of underpants.

Parents know full well what it means.

https://www.theguardian.com/business/2022/jan/17/china-warns-west-again…

Now China is screwed and instead of looking for solution is pursuing their policy of threat / warning.

More than a 10% increase in Wellington house listings today (based on TradeMe).

good bye greed, hello fear.

Number of listings has gone up 100 in just over an hour, on a Tuesday. Tomorrow might just be a record.

You'd have thought all the agents had been on holiday or something.

It's the 18th. No wonder productivity is so low here.

Poor fellas in denial, I just hope he got out when he had the chance.

New property listings have jumped, in what could be the first sign the property market is starting to turn in favour of buyers, the latest realestate.co.nz data shows.

From same time last year.

"And suddenly, out of nowhere and for reasons totally unrelated to falling house prices, the government decided that reopening the border to all and sundry was a 100% safe thing to do."

Property Investor Page located in Lower Hutt:

Hi everyone im looking for some advice if possible. I have a property that has been on the market coming up 3 months I brought it 9 months ago and did renovations and put it on the market can no longer sit back waiting with mortgage costs, rates, insurance for an empty house. Our own home is mortgage free and wondering what the best option would be. Only had one offer 30k below minimum asking i which we would be making no profit.

Interesting that they aren't renting it out. Indicates it was a do-up for capital gain, and rental numbers would not stack up.

Oopsie doopsie.

Turns out this is the property. Paid $780k in April 21. Wants over $900k.

https://www.trademe.co.nz/a/property/residential/sale/wellington/lower-…

I'm assuming the following from the property title is a typo and it should be a $1.2m (not $12m) priority amount (if it's the priority amount lodged on the title).

12118914.3 Mortgage to Kiwibank Limited - 18.5.2021 at 11:00 am

Poor old Tall Poppy. Another one bites the dust.

If he bought it April 21 why is the last sale dated Jul 2019?

Sale will be under brightline rules so profit is fully taxable.

Anyone with a guess on cost of renovations?

Doesn't appear to stack up if purchased for $780k.

According to homes.co.nz there's a sale 27 April 2021, and one before that was 15 July 2019.

Thanks.

For some reason the realestate.co.nz listing doesn't include the April 21 sale.

"Property Student" type groups might spot it and start them and their mates lowballing the seller to lower price expectations. I attended one such group's seminar once out of interest and they talked openly of doing this (before another group got told off for it).

So if they take minimum asking that is only a 30k profit? Assume then there is tax and some other things they won't have accounted for (don't seem the smartest) then that is f*** all profit really. I assume they took into account all the hours they themselves put into the house, weather it be DIY work or organising contractors etc. Seems like a huge piss around for like 20k after tax. And they might not even sell it for what they want, I can sense the desperation from here lol.

Assuming they didn't equity leverage to 100% from their OO property, let's say they borrowed a conservative $500k and put down $280k deposit, then interest only at 3% p.a. = $11k in interest costs over 9 months and probably $2 - $3k in rates.

https://www.realestate.co.nz/42048134/residential/sale/105b-kamahi-stre…

"...the new carpet and vinyl, modern led lighting, an upgraded kitchen, bathroom, new mains pressure hot water cylinder and more. You will simply love the open plan living and dining with fantastic indoor-outdoor flow to a brand-new sun deck perfect for outdoor entertaining with your family and friends."

Oops indeed.

Diddums.

Interesting anecdote thanks.

Is someone really ready to fork out 870k for this ???

Probably worth offering 800k?

Holy Moly its on!!!

U.S. 10 Year Treasury Note to the moon.

https://www.marketwatch.com/investing/bond/tmubmusd10y?countrycode=bx

At this rate your balls are going to be pretty blue by the time the market actually takes a dive.

What's the matter Pa1nter, not feeling too well?

Suns out, waves are decent size, thankful to have ridden out the last couple years in NZ, feel pretty good thanks.

How's it your end impatiently anticipating misery for other people?

It's called utilitarianism and most of those investors who are about to get burned deserve everything they get, especially the ones who put the rents up. Karma is a wonderful thing.

What if they were a family that decided to buy a house to live in?

How about the other 100 families who could not afford the inflated price that 1 family paid? At least that family will have a house to live in and when prices crash the other 100 families will be able to afford that luxury too. Everyone's a winner, except greedy unscrupulous investors.

You perspective is only sound if the other 99 houses are owned by investors. Moreover it's just a sad fact that in a market with a finite amount of housing not everyone can buy a house, because someone else can outcompete them, no matter what the prices are set at.

This issue is exacerbated further in larger population centres, especially ones which attract a lot of migrants.

The other 99 houses will be from investors, many will have been ghost homes just sitting empty waiting for more capital gains. Why does simply going back to 2019 levels panic investors so much?

Only a quarter (maybe less) of homes sold in the last year or so are to investors. Definitely not 99%.

Investors can probably stomach a return to 2019 better than private home owners.

Investors are so caring and compassionate towards less fortunate people its truly wonderful to behold.

Some will, some won't.

You hold an irrational level of contempt.

I also have contempt for people who harvest bile from bears, same type of mentality if you ask me, let the bear have just enough of a life to keep taking from it, but do not let the bear have any happiness, but that's just my opinion.

Yeah also not rational but that doesn't seem to be your jam.

Unfortunately they might get burned too depends on how much mortgage they carry and when did they get in the market. You wonder why banks are tightening up the lending rules now…I know people don’t want to listen to this. But sometime truth hurts.

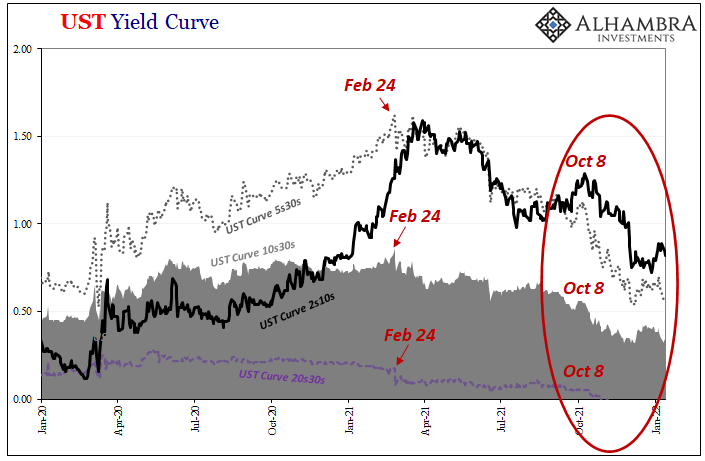

Check out the UST five year and the consequent bearish spreads here and here.

{kind=link}

{kind=link}

Can you explain what effect this has on the real world, for a smooth brain such as myself?

The 10-year yield is used as a proxy for mortgage rates in the USA. It's also seen as a sign of investor sentiment about the economy. Things look like they may be changing.

Just so you know, the most common mortgage interest fixed term in the USA is 30 years.

I know.

Yes..not available to the NZ ponzi mortgage market.

30 year loan would suggest a long term commitment to a home, not flipping every couple of years

BTC has followed the 10year bond pretty spot on for 1.5 years at least. Now there is a huge divergence with the bond up and btc down. People hoping for that btc pump to keep the correlation!

EQUITIES MOSTLY RISING, EXCEPT THE NZX50

The question isn’t whether one should adapt to unprecedented Fed policies, but instead, the form those adaptations should take. We are fully convinced that these historic valuation extremes have removed decades of investment returns from the future, and strongly suspect that the Fed has amplified future downside risk as well. I believe investors have placed themselves in a position that is likely to be rewarded by a very long, interesting trip to nowhere over the coming 10-20 years. At worst, they may discover the hard way that a retreat merely to historically run-of-the-mill valuations really does imply a two-thirds loss in the S&P 500. Link

Simplicity has bumped their floating mortgage rate to 3.15% from 2.25%: https://simplicity.kiwi/simplicity-first-home-loans/

less pork for fhb now

The benchmark UST 10 year yield has risen today to 1.82% and a one year high. There is growing market conviction that the Fed will start raising rates in March, and possibly more aggressively than previously thought.

It is depressingly circular isn't it? Traders guess that the Fed is going to increase rates, so yields rise in anticipation, Fed then responds to these 'market signals' and pushes rates up. Capital flows then shift to where they can find the best balance of risk / yield, and so it goes on. It is an inherently unstable system - and there is a multi-billion dollar parasitic financial industry that exists simply to profit from that instability.

I have just received a response to my OIA request of last year to Kainga Ora on the number of new builds in Auckland for the 2021 calendar year versus number of demolitions. We always hear spin about the amount of new housing built, but never about the net gain (new builds less demolitions).

The data in the response is staggering, and perhaps because of it there is a whole lot of unwelcome spin in it.

Drum roll please...

651 new dwellings tenanted, 576 dwellings demolished. A net gain of 75 dwellings in 2021....

Amazingly low, even much lower than a cynic like me was expecting.

Wow! That’s staggering. I hope they are doing better outside of Auckland

They do of course generally plan to put many more houses on each section. So this is transitory. But as you say it has not been reported.

Another example: There are maybe 40 ex-Navy (now Maori) houses in Devonport which were demolished. Only a few new ones built as yet.

I suspect that there will shortly be a large oversupply of houses because no account of house loss will have been used by the Council and Govt. All they see is the lack of housing right now.

This panic building will all come onto the market at once. many developers will go bust.

But they have been plannjng for many more houses on sections for years now.

I think these stats are staggering.

If they demo'd 500+ houses, I'm amazed they managed to build even 600 on the sites in 2021, pretty tough getting completions.

The figures are new tenanted houses, there were challenges with their data on completions etc.

Yeah, cause they will be behind. Auckland had how many weeks in 2021 with almost no construction?

I'm still involved in projects that started mid 2020 that should've been done and dusted early last year. So far, 2022 is looking even worse. The industry just can't cope with shortages and their flow on effects, job shuts down due to shortages or lockdowns, by the time it's back and running the subcontractors have moved on, more waiting while people can come back, etc.

From what I understand, they've accomplished almost more in Hamilton.

You are being generous on them. If they had a decent amount more underway in 2019/2020 as they should have then they could have completed a lot more in 2021.

Also, a lot of building was able to occur in lockdown. I know because the next stage of development where we live was occurring across from us.

Look, I will acknowledge 2021 was hard but that's still a pitifully low net gain social housing with 20,000+ on the waiting list.

When you have things like this happen

A total of 482 families and individuals were taken off the waitlist and moved into housing over April, but they were more than replaced by 1443 new entrants to the list.

Its a pretty tough battle.

All that shows is there's demand for housing that's capped at 25% of ones income. If you somehow moved all 1443 into housing overnight, then how many rental properties would be left empty? Understand some of these applicants are probably sleeping in garages, couches and bathtubs but many are probably in private rentals.

How many existing dwellings did they buy, in auctions, competing with FHBs

Of the 651 dwellings, 125 were bought from private developers.

Nice going.

A pretty humble increment: 75 new dwellings. Even if that is 7 people in each, plus another 4 in the garage, it's not a lot of extra dwellers compared to the wait list of 24000 households:

https://www.stuff.co.nz/national/politics/300363280/public-housing-wait…

They have exceeded my expectations.

Good research HW, puts new builds in to perspective. What are the stats in the private sector?

Interesting - the 'Rich Dad Poor Dad' author predicting a massive house price crash:

https://www.nzherald.co.nz/business/prepare-for-war-rich-dad-poor-dad-a…

Is he selling a book or advice on it?

Haha, probably.

He's a big gold bug also

Money doesn't seem to buy a good face job.

I don't really get Kiyosaki. He advocates borrowing as much as you can and investing in stuff that generates cashflow (the article says he's reported to own 8000 properties), so leverage off other people's money, and at the same time he's all "Govts are printing too much money and it will crash". I suppose he's been happy to get rich on a rigged game, and is getting ready to save what he can if it rolls over.

I'd have more respect for him if he used his resources to do something like visibly support his mate George Gammon and his "Ënd the Fed" campaign.

I agree with most of things he says be there is something i find fishy about the guy

Self promotion is his game.

He is a marine, you know

Oh yeah he loves the rigged game.

Some of his other comments from the article.

Kiyosaki, who was reported to own more than 8000 properties, said the next financial crisis would provide opportunities for astute real estate investors.

"I am pessimistic about a crash … but it is also the best time to get rich," he said. "Entrepreneurs are going to win."

Kiyosaki has dabbled in Australian real estate, including purchases in Sydney and Brisbane, and said he took issue with some local government policies around taxes.

This included negative gearing. "I don't like government support," he said. "I am a capitalist, not a Marxist.

"My concern is that … with negative gearing it's monetising debt and property values are overinflated … it's not real. It's got to make economic sense."

Ha, he doesn't like govt. support but I bet he doesn't complain about TBTF indirectly bailing out his investments.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.