Housing is now the most unaffordable it has been for typical first home buyers since interest.co.nz began producing its Home Loan Affordability reports at the beginning of 2004.

The new record in unaffordability levels was driven by a pause in the recent price declines at the bottom end of the market and ongoing increases in mortgage interest rates.

According to the Real Estate Institute of New Zealand, the national lower quartile selling price peaked in November last year at $670,000 and has since settled back to remain slightly below that level, remaining between $650,000 and $661,000 over the four months from December to March.

The lower quartile price is the price point at which 25% of selling prices are below and 75% are above, representing the most affordable end of the market which is usually of most interest to first home buyers on average incomes.

Essentially the latest data tells us that prices at the bottom end of the market have flattened out at levels very slightly below last year's peak.

However while lower quartile prices are catching their breath, mortgage interest rates have continued to increase at pace.

The average of the two year fixed rates offered by the major banks increased from 4.20% in February to 4.41% in March, which means it is now at its highest level since August 2018.

That combination of high prices and rising mortgage rates is pushing the prospect of home ownership ever further out of reach for first home buyers on average incomes.

The first hurdle they will face is saving enough for a deposit.

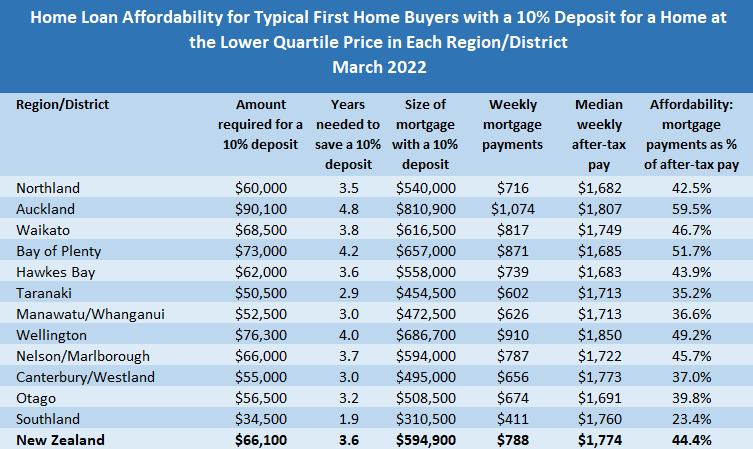

Southland is now the only region in the country where the lower quartile selling price is below $500,000.

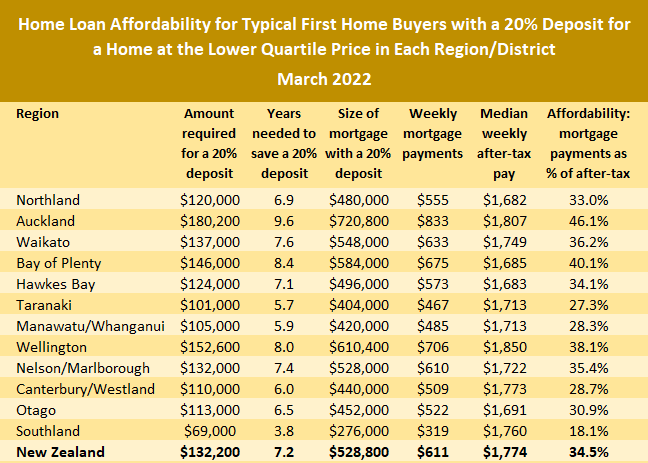

That means that apart from Southland, the amount needed for even a modest 10% deposit on a lower quartile-priced home ranges from $50,500 in Taranaki to $90,100 in Auckland. You can double those figures for a 20% deposit.

That problem has been made worse by the fact that house prices have been rising at a much faster rate than incomes.

The Home Loan Affordability Reports estimate the combined median after-tax pay for couples aged 25-29 in each region, assuming both are working full time. The national median has increased from $1712 a week in March 2020 to $1774 a week in March 2022, up by 3.6%.

Over the same period the national lower quartile housing price has increased from $480,000 to $661,000, up 38%.

Because the rise in house prices has occurred over a period when immigration-driven demand for housing has been almost zero and the supply of new housing has been increasing, it appears likely that the cause of the massive jump in housing inflation lays at the feet of the Reserve Bank and its policies, such as forcing down interest rates to record lows, the (temporary) easing of loan-to-value ratio mortgage lending restrictions, and pumping cheap money into the banking system via quantitative easing, or buying government bonds.

While these policies may have been mana from heaven for the trading banks, they had what should have been predictable effects on house prices and housing affordability.

One effect of the surge in prices at a time when income growth remained modest has been that the amount of time needed to save a deposit on a home has increased significantly.

Based on the national median wage figures used in the Home Loan Affordability reports, if a young couple were able to save 20% of their combined after-tax pay each week, the amount of time it would take to save a 10% deposit on a home purchased at the national lower quartile price has increased from 2.7 years in March 2020 to 3.6 years in March 2022.

You can double those figures for a 20% deposit.

At the same time, any benefit that initially occurred from lower mortgage rates has been more than wiped out by rising house prices, with the mortgage payments on a home purchased at the national lower quartile price with a 10% deposit rising from $505 a week in March 2020 to $788 a week in March 2022.

As a percentage of take home pay for typical first home buyers, those mortgage payments would have eaten up 29.5% of their weekly pay packet in March 2020, but by March 2022 that had risen to a record 44.4%.

Mortgage payments are considered in unaffordable territory if they take up more than 40% of take home pay.

In Auckland the mortgage payments on a lower quartile-priced home purchased with a 10% deposit would have taken up 44.5% of typical first home buyers' take home pay in March 2020. By March 2022 that had risen to an astounding 59.5%.

That has effectively ruled out any hope of first home buyers on average incomes being able to afford a home of their own in Auckland and in the rest of the country it's increasingly marginal.

So first home buyers can feel justifiably aggrieved.

The flow-on effects of the Reserve Bank's actions over the last couple of years have effectively thrown them under the housing bus.

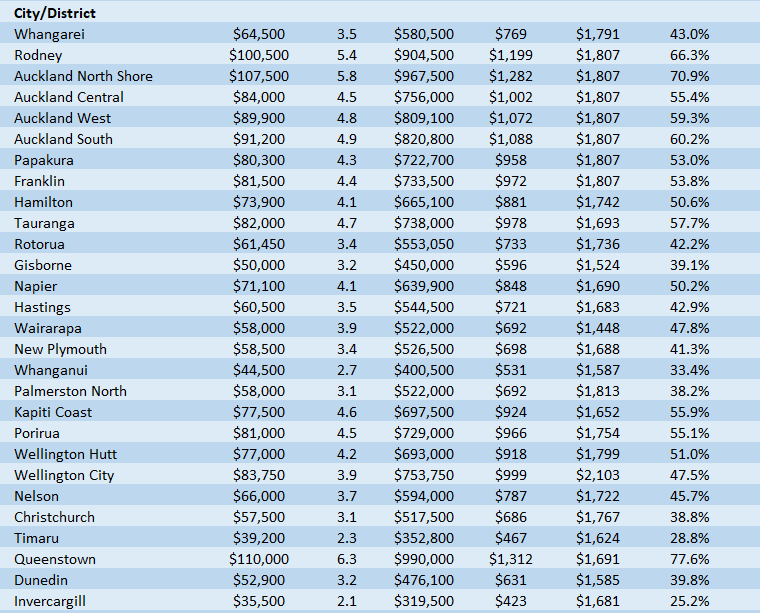

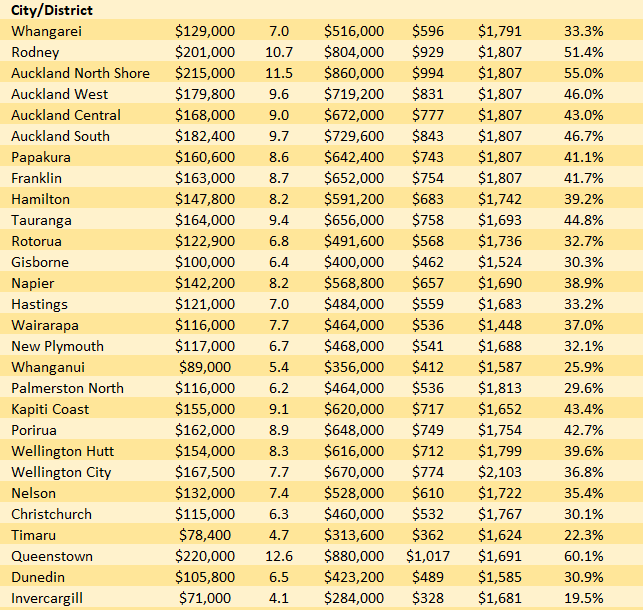

The tables below give the main affordability measures for buying a lower quartile-priced home in all New Zealand's main urban areas, with either a 10% or 20% deposit.

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

150 Comments

Last one out turn off the light...

Considering first home buyers are basically shut out of the market now due to high prices and interest rates not quite so stupidly low, and investors are being taxed now and have negative capital gain, that is like 66% of the market dried up? And then even existing owners looking to move must be very cautious; they don’t want to buy something new and not be able to sell their place for the milions they expected.

Hard to see how that ends well for house prices. Tony Alexander sees some upside though.

I cannot recall a bigger blunder in the history of the RBNZ than their ongoing decision in 2020-21 to gradually crush the OCR into the floorboards ... thereby triggering an avalanche of cheap debt to inflame the simmering inferno of the NZ housing market ...

... I very much doubt that Don Brash or Graeme Wheeler would have behaved so recklessly as Adrian Orr has ...

Well ... its poo our nappies time , isn't it , Adrian !

Orr will be remembered as one of the worst RBNZ Governors in the history of NZ. His un-necessarily ultra-loose monetary policies will be remembered as the primary cause of massive unbalances and systematic risks in the NZ economy. He should have never reduced the OCR down to 1% in the first place, and the further reduction of the OCR down to 0.25% in 2020 will be remembered as one of the most stupid and counterproductive decisions ever made by the RBNZ. The temporary removal of LVR limits, and the whole QE program, were utterly unjustified and stupid beyond belief.

Yip - I think he played his part in helping the country avoid a depression....but thought it was bonkers removing the LVRs....as you say it might go down in history as one of the biggest errors of a governor in the history of the RBNZ.

Whilst you ignore how Robbo changed the RB mandate.

Not one of the worst, THE worst.

How much has Grant got to blame here. After all he is the Finance Minister and wanted as much lolly to play with as possible!

Aided and abetted by a clueless finance minister...

... Robbo's the smart , articulate one in the cabinet ... tells ya how utterly hopeless the rest of them are ....

Oh,I know someone who knew of him (but didn't like him) at uni. Pretty average intellect, apparently.

Nothing to do with intellect. The broken inflationary debt-based monetary system and perverse incentives have bamboozled most people.

I knew someone who knew "of him" comments best kept for facebook. This is a discussion about finance. Apparently.

It's a refreshing change seeing someone argue folk on the Left aren't intellectual enough.

Lowering the OCR was a defendable decision during the middle of the uncertainty surrounding Covid. But removing the LVR limits was unforgivable at the time, and it looks even more foolish in hindsight. Delaying the capital adequacy requirement changes - that were designed to protect from a 1 in 100 year event - DURING a 1 in 100 year event looks reckless. And keeping the OCR at emergency low levels while the economy was overheating and inflationary forces were building was also idiotic.

Exactly!!!!!

It was truly batty and many of us submitted letters to the RBNZ telling them exactly that.

I suspect as it was under Bascand's area of "expertise", that his exit may have had something to do with this. The timing was a little too coincidental that right around the time the effects were being felt, he "resigned" from his position.

Prices lag OCR changes. The full effects or rate rises will take years to permeate the market.

Housing Bubbles classically take 3-5 years to go from peak to trough. Such bubbles can be maintained through destruction/debasement of a nation's currency.

this was a useful comment.

the days of arguing about the crash are over. The thinking now should be about surviving the mess and picking the bottom of the cycle. my feeling is 3 - 5 yrs is probably about right, but that is purely gut feel - not based on any science.

It depends if a crash in housing causes deflation or not. It may be that if we are in a higher inflation environment globally and prices don't bounce back rapidly. In 2008/9 low inflation allowed Reserve Banks to use rates extensively but it would be remiss of us to think of this as simply a repeat.

Housing bubbles do normally take time to deflate. I worry that NZ's bubble, having been accelerated so drastically by the RBNZ's reckless policies over the last couple of years, and the speed at which inflation is pushing up rates, could result in the deflation occurring considerably quicker. This will make it far more rapid, painful and catch more people unawares.

Yes, but the effect on first home buyers who rushed into a frenzied housing market when cheap mortgage rates were being pushed thanks to the 'Adrian Orr move to negative rates' experiment will hit REALLY hard come late this year.

Well he did tell them housing is a 'consumption good'.

? the CPI views housing units as capital (or investment) goods and not as consumption items. Spending to purchase and improve houses and other housing units is investment and not consumption.

? the CPI views housing units as capital (or investment) goods and not as consumption items. Spending to purchase and improve houses and other housing units is investment and not consumption.

This sounds like a good TV debate between you and Adrian

Only if they where on a short-term fixed rate agreement.

Typically in a true housing crash the market freezes up on the way down because banks curtail lending to prevent losses. The market is heavily credit-driven. My worry in New Zealand is that we may get the same effect Ireland had where net migration reversed due to housing which put further pressure on house prices.

In addition to migration reversals, Ireland suddenly found that they had an oversupply of houses because many "ghost" houses flooded the market.

An Irish newspaper report from the time says this:

"Why the sudden surge in supply? The most likely explanation is those who had invested in property but had not sought a rental income are now doing so. As interest rates rose, so did debt servicing costs, while at the same time capital gain evaporated as prices stopped rising. The likely result - those who had been willing to forego rental yield are less and less willing to do so."

We may see the same thing now in NZ.

https://ww1.daft.ie/report/dan-obrien?d_rd=1&d_rd=1&fr=touch

Better pump up the immigration numbers, keep the Ponzi going.

This isn't news - we're living the nightmare.

The flow-on effects of the Reserve Bank's actions over the last couple of years have effectively thrown them under the housing bus.

They'd already been thrown under the bus. The RB just decided to drive back and forth over them for good measure.

✈️✅

CWBW - Be Quick

2020 - 7%

Brock - Flee NZ

All spam.

Or different people expressing a view.

Or the same person farming different views for entertainment

Or different people spamming their view over and over again.

I can't recall you being offended by TTP or P8 or the property spruiker gang...so in order to be consistent in your behaviour, do you want to attack them also for spamming their views over and over again?

Or do you only want to silence the views of those people who threaten your overextended leverage against the housing market?

CWBW - Be Quick.

Literally the first thing I said.

Both extremes that spam are just as obnoxious as each other.

Also, nice of you to assume my financial position.

You're way off the mark champ.

Brock Flyers. Brock Landers.

Plenty of room for upward valuation? Be quick?

Haha. Upward bank profit and mortgage listing.

Beak wick? More like beak earful.

Young couples will leave to make better life abroad or will be renting for years. So basically only couples earning 300k per year can buy in Auckland not many of them around, at some point the housing market needs to crash and will by 60% or this is the future for our kids basically just surviving.

I'm still struggling with the, 'median after tax $1700 pw' average pay bit. In reality, most people on the minimum wage would only be taking home maybe $700 bucks pw. Or have I interpreted that wrong?

The $1,700 pw is for a couple, so two people on slightly more than minimum wage.

What an ORRful legacy.

Whatever, still the Inflation is way higher than RBNZ mandate of maximum 2%.

It's a bit rubbish comment saying the rbnz has thrown fhb under the bus.

The entire home owning public have been merrily doing this for the last 3 years.

It was credit creation that's driven the bubble and its credit tightening that's required to fix it.

The only ones about to get steam rolled are those who have overly extended thier credit lines, assuming that emergency rates were here to stay, but that's not limited to fhbs. I'd wager that the most exposed are middle aged.

Fhbs who are more realistic, would look to weekly payments affordability not based on emergency actions born from a pandemic, but what you were always going to end up paying in 10, 20 years time, the average rate over the course of your loan.

Those fhbs would/should be very happy right now. Watching existing property holders sweating over big mortgages, inventory and days to sell pile up.

Good financial management is about options, keeping them open. So whose smarter, a fhb buying at the peak last year, whilst now finally on the ladder (but cursing the rbnz for raising rates) or a fhb still sitting on a deposit, watching prices adjust and the available stock increase each week?

Have cake, want to eat.

"The entire home owning public have been merrily doing this for the last 3 years."

You act as if many OO would have been thrilled about the stonking amounts of debt they were needing to take on to own a home, but as pointed out repeatedly, the decade of inaction from bankers and even recent comments by the PM/Finance Minister indicated that all the stops would be put in to ensure house prices continued to rise, albeit at a small rate.

At this point, given the scale of the debt involved and the open contempt shown for the idea of prices coming down by decision-makers, a rational action is to move to avoid being left behind. In the end, it has taken an external shock to do what the political and regulatory institutions were not prepared to do.

At some point, many will have just begrudging accepted they were just along for the ride, and that life could not be put on hold any longer, especially given how long many may have been waiting on the sidelines for a correction that was already many years overdue. Damned if you do, damned if you don't - someone in NZ will always find a way to make something your fault.

Even if the everyday owner/occupier had any joyful thoughts of a booming housing market, the sentiment is surely going out the window pretty quickly now. Many uneasy circumstances in this population at the moment. Those who have taken on massive DTI, and those who have bought with intention to sell.

I visited an open home last weekend. Was the only one there. Owners had already bought and moved. There was a single conditional offer on the place waiting for the buyers property to sell since February. I wonder if there's a conditional offer on the buyers place too.

Not very merry.

Except 'responsible' FHBs thinking about future rate rises, etc., have simply been unable to buy. Being sensible has not been an option. Hence FOMO.

Precisely. The market was only encouraging the short-sighted or those crazy from FOMO to buy. Sensible, responsible buyers were missing out.

People just delay their lives. Arrested development kicks in and young adults dream of van life instead of families. Birth rate plummets. More immigration. The whole thing is so grubby.

We've been led down the garden path, hollowed and cored since 2008. I for one am furious.

I would say the FHB who already bought in the last couple of years is smarter. They managed to get their finance and hopefully locked in a super low interest rate for possibly as long as 5 years. The one sitting on their hands/deposit may find that even if house prices do come down, with tighter credit, they will be able to borrow much less, and when they do their repayments are probably going to be higher than the FHB that bought in the last couple of years and fixed on a low rate. I would say the FHB sitting on their hands will end up very disappointed - and as rates continue to go up, their disappointment will continue to grow as once again they use the excuse of waiting as they think their will be a massive "correction" in prices.

Idoubtit if someone purchased now in two years they would have lose deposit and be in negative equity, why are you giving bad advise or are just daft.

@DTRH I am not sure how you consider this to be advice given we are talking about something that has already happened. And even if prices are to go down no one is losing any deposit - they may be in negative equity, but that won't matter unless they have to sell. And if they fixed for more than 2 years then it is likely that even with lower house prices their repayments will be lower than someone who may buy after the speculative price dip. So perhaps it is you, rather than I, that is daft.

That argument is perfect if someone has a home mortgage of 2 or 5 years. But if you're going to be paying for 30 years with inflation eating up your income and interest rates perhaps never falling to emergency levels again.. well, what then?

And if you bought a 1 mil house with a 20% deposit, then your deposit is in effect wiped out should the house price drop to $800,000. Gone. This is already busy happening to those who bought last year.

Depends on how the bank behaves when coming up for a renewal of a fixed period i.e. will they allow someone to fix their mortgage even if they're negative? If so, it'll cost the borrower.

E.g. Someone buys 12 months ago @ 80% LVR x 2.5% fixed for 2 years. In 12 months time when they're due for refinance prices fall 30% and the lowest interest rate is 4%. But now they also have a low equity premium of 2% (according to ANZ) so 6.5% effective rate. $1k per month extra on $500k loan.

All of the banks have come put publicly saying they wouldn't do that; whether you believe them is another story

Yea perhaps in the short term those who have fixed for 3 - 5 years will be ok, however even if these FHB attack the principal of the loan as hard as they can during this time, when that term ends and they refix their interest rate will still be astonishing. Those who have waited may have to bear high rates for a period of time but will have more flexibility to work the principal down in the 5 - 10 year period. I don't have the time to do the math, but you get the idea.

@malamah my point is that those that waited might still be waiting, as with tighter credit they may not be able to get even close to the finance they would have got previously. And with DTI restrictions likely to be added in 2023 also. In the chance that they can still borrow, their "flexibility" to work the principal down in the "5-10 year period" won't be any different from someone who has already bought in the last couple of years - in fact it may be more difficult as someone who bought November 2021 may have fixed for 5 years at a low interest rate :)

FOMO talk.

@tuisbest - I wouldn't say FOMO talk as there is no longer a fear of missing out. Those people have already, in my view, missed out.

Missed out on what? The mortgage distress looming large on the horizon?

FOMO's been replaced by FOBI ... " fear of being in " ..

Yea it's true those who waited are no longer waiting by choice. There will either be a sharp correction or a long drawn out stalemate. Either way, inflation isn't going anywhere any time soon. It really is a matter of strapping into your belt buckle and riding the wave over the next few years for a fairly significant number of Kiwi.

... except around 60% of mortgages are due to refinance within a year. So no, most did not lock in long rates. The vast majority of FHB had to stretch themselves to buy - with longer repayment terms (30 year terms increasingly common), rates on the short end (cheaper) and had to buy with smaller deposits (see the explosion of lending when LVR's were removed). They are, as a group, very very susceptible to increased servicing costs.

These are the people who (along with highly leveraged investors) are about to feel the brunt of higher rates and falling prices.

@Miguel - 30 year terms are not becoming increasingly common. In New Zealand, loan terms have primarily always been taken out over a 30 year term and certainly is the case unless you request a shorter term which will in itself affect the bank's affordability assessment.

40% of loans not coming off fixed rates within the next year is still a large portion - perhaps those 40% are mostly the FHBs who, as you are say are susceptible to increased servicing costs and therefore were hopefully savvy enough to choose longer fixed terms. The 60% coming off could very well be made up by a majority that only has a small portion of FHBs. Certainly the FHBs that I know that purchased in the last 18 months fixed at very low rates for as long as possible.

Cool, so your whole argument is based on reckons and fhb that you know. Solid.

30 year terms are not becoming increasingly common

https://www.stuff.co.nz/business/128432333/over-half-of-new-home-loans-…

40% of loans not coming off fixed rates within the next year is still a large portion

Is it? Given that only 6% of fixed mortgages are fixed for 3 or more years its not a high proportion of people who have fixed long term. You should try actually doing some research and base your opinions on some hard data, rather than relying on anecdotes and guesses.

https://www.rbnz.govt.nz/statistics/s33-banks-assets-loans-fully-secure…

That assumes those fhb keep their jobs and are not impacted by a recession. They are locked into their house and will not be able to move to seek work

100% agree. It’s starting to really annoy me when every keeps using the tag line ‘but unemployment is so low’ yea that can change, its generally what changes in a recession.

Last time unemployment was this low was just prior to GFC…when the economy was also overheated…we can cure that as well with rising interest rates..and a market crash.

And these figures are for 'the lower quartile price'. Crazy.

B-b-b-b-b-but back in my day we had 22 percent interest rates and 3 mortgages. There were no carpets or insulation, houses didn't come with concrete driveways or grass. Our "lounge suite" was made from swappa crates and an old mattress.

Buuuuttt we purhcased on a single income and the price was only 3x income.

If interest rates go up to 22% again we may see house prices at 3x income again.

I had this grief from an elder last year. The kicker was when they explained their first purchase. Helped by their parents into a $20k home with $10k income. What has happened...

... " there were 122 of us living in shoe box in middle of road ! "

" Cardboard box ? "

... " aye ! "

" Luxury ! ... you were lucky ... best we could afford was to live in a rolled up newspaper in a septic tank down at town rubbish dump ... "

Ha yeah but back then houses were valued as homes to raise a family in, not get rich quick schemes or "nest eggs".

Most of the blame could be placed on the narrative over the past two decades, almost a form of brainwashing and conditioning far removed from any fundamental social values.

FOMO is a nice buzzword to shift the blame and create division. Most buyers overpaid in the belief of making the same gains they paid for. So just as culpable in contributing to the problem. But what were they to do, they were only following the example set before them.

I ran the numbers a few years ago and even with low interest rates, it did not make financial sense to own a home unless it made capital gain. The premium for security has inflated beyond reason.

5 Years to save 90k in Auckland so saving 300 a week for five years while paying huge rent and what if a baby comes along, by the time have saved enough the be to old for 30 year mortgage it also looks like rates will be at higher than the 4.41% more like 7%

What if you got hit by a truck?

What if you got a promotion and paid more?

What if you lived in your car to save rent?

What if rates go to 7%

What if there is a recession and rates go back down?

What if? What if? What if?

What sort of truck ?

Repo'd Ford Ranger.

From the driving, it appears the R in Ranger is redundant.

If you get hit by a truck go on ACC, then have 6 kids and be provided with a new home and guaranteed income.

This is NZ's new economic strategy and replaces the now defunct house flipping path to wealth creation.

And when the offspring hit the magic 7th birthday, send 'em out to the malls. At night. With tools. And an order list.

What if you looked at facts and understood you don’t really have a clue about house prices or finance. Maybe watch sesame street might help you with numbers

The flow-on effects of Reserve Bank policies have effectively thrown first home buyers under the bus

Whilst it is sad to see home ownership so difficult to achieve, it's also disappointing to see that Interest is progressively giving in, to the mostly socialist, righteous and blame loving commenters of its site. Maybe Interest should change its motto from "helping you make financial decisions" to "building a better social world".

Where can one turn for a true financial website in NZ?

Great read, cheers GBH.

Thanks GBH

An unbelievable piece of writing, thanks GBH. Left me speechless. What an epic mess.

"Socialism" for the property market...yet the ones who point it out are the ones in the wrong, apparently.

Is this statement not correct?

How about a novel concept, we take responsibility for our own actions and reap the rewards or pay the price for these decisions?

The headline could just as well read "RBNZ rewards FHB's who bought before 2020 handsomely"

Or another one:

"People who have repeatedly warned that houses were overpriced and advised others not to buy over 2011 to 2020 have thrown FHB's under the bus"

See, it's all in the eye (bias) of the writer

I guess it is easy to see it this way when you stand in the right side of the fence.

Almost all non home owner are people that could not buy.

A very small minority could make a choice.

The game played by RBNZ and Govt is... shut I really need to challenge the limits of my english to find the corrective adjective! Nothing represents well enough how much I despise them.

Not wanting house prices going down today means being antisocial and sociopath.

You are mentioning often free market, but I don't think you really mean that.

In real free market houses would have not been so much legislated on. Where you can build, what you can build, how "green" must be, consents, consents, consents...

It isn't a fair game. We are at aristocracy level now.

The NZ I grew up in felt egalitarian to me.

Previously, I wouldn't have said that the average Kiwi had an antisocial or sociopathic bone in their body.

But this recent housing crisis and boom has shown an ugly, ugly side to our society. Many people have been happy to "get ahead" by throwing renters under the bus. People farming is repulsive. Market rents are simply too high, and anyone who charges market rent is, quite frankly, repulsive.

So what rent do you charge your tenants Fitz?

Very true.

How about a novel concept, we take responsibility for our own actions and reap the rewards or pay the price for these decisions?

That is what people have long advocated for the property market instead of it being welfare-subsidised and protected from risk.

Instead, NZ has had a "socialist" model for property investment, wherein it rides free as working Kiwis pay the taxes, where it's subsidised with welfare, and where when hard times hit it is protected from risk rather than reaping the rewards or paying the price for decisions.

Meanwhile, younger Kiwis are paying taxes that fund a socialist universal benefit to many older folk who received affordable housing thanks to previous socialist build efforts.

I'm a homeowner who has benefited from the wealth transfers of the last few years. I'm surprised at the lack of self-awareness in the initial post.

If you don't want to read other people's analysis of the facts, then don't read the commentary in the articles or the comments. It's not that hard to skim to the tables and just read the figures if that is all you are interested in.

Lol - the socialists appear to be the property investor types who expect the government to socialise the losses on their investments via accommodation supplements and emergency interest rate drops! All funded by labour/working class citizens....

So not so sure you've got your aim right on this one Yvil.

And many of the people on here are investors of capital...so might be more capitalists than socialists.

If you want capitalist and free markets because you hate socialism (by the sound of the post above)....let abolish all accommodation supplements immediately (ie a socialised benefit that goes to the hands of landlords)...how does that sound? That would be another significant factor that would allow property prices to fall even more!

Maybe we could legislate a reduction in rent based on whether the tenant is receiving an Accommodation Supplement as we slowly phase it out.

E.g. Asking rent: $500 per week -> tenant signs up receives keys -> if tenant is entitled to AS then application to MBIE -> new rent becomes rent minus AS -> tenant keeps AS payments but gradually reduces to $0 over 12 months.

If tenant is not entitled to AS then rent = rent. A tenant "lottery".

Accommodation Supplement is/was a very misguided tool aimed at helping low socio-economic groups but ultimately ending up in the pockets of the landlord. A crude offer in lieu of state housing alternatives. Generalised rent controls would be preferable, and then those who received the Accommodation Supplement would actually benefit from it. I'm not sure how you'd best approach that, but the current market is anything and everything at maximum dollar. Now there's only so much blood you can squeeze from a stone.

Yep and working for families just trickles straight back up or into property investment.

Problem is, how can a more equitable sharing of surplus be regulated? It's ultimately driven by the individual's or organisation's personal demand for more wealth.

It has to be a cultural/societal value.

These figures are with low interest rates less than 5%.

The figures are going to look real sick when interest rates move up another 40% (2022 ;) )

The main banks along with the bank of M&D are going to be squirming at that.

Told you so. As did many. Feels gre....

Sad

"Hear ye, hear ye!"

I just checked your account to see if this was a new account, I think our dear friend may have been banned.

What extreme measures will be used to save the market? Because it always gets saved due to political necessity.

Massive FHB buyer grants will 1 mil value cap and no income testing?

Government guaranteed mortgages at low/long fixed rates up to 1 Mil cap?

Tax deductibility for Mortgage interest on owner occupied homes up to a cap ??K per annum ?

... if the body is in the casket , there's no point in jumping up at the funeral and shouting " hold everything ! ... I know CPR ... stand aside , I've got this ... " ...

RBNZ and the Government might get together for a spot of necromancy.

Well, they already do haruspicy.......

yes the damage is done. The next madness will be an attempt to socialise the losses .. spread it out and make the responsible pay.

Coupled of course with more immigration madness.

Imagine if tax deductibility existed for Owner Occupiers. What an incentive that would be for a Government to keep a lid on house prices, if people can reduce their tax bill against their housing costs.

I mean sure, I'm deriving an income from my home by having somewhere to sleep in between work hours. I would likely not have a job if I were unwashed living under a bridge.

Yeah. I think the next election will mostly be National and Labour competing to offer the biggest rescue package to struggling property owners.

Meanwhile, inequality will be worsening, crime increasing, unemployment rising, but it'll be all about the lollies for 'FHBs' (and coincidentally investors).

Things always revert to long-term averages. The affordability % isn't a problem, it is a beautiful indicator of how rapidly house prices are going to have to decline to get back to a number that makes sense.

While the example is based on FHB's, these obscene affordability %'s are the same for anyone looking to buy with a mortgage. The top end of town is currently being supported by people moving from house to house, so benefiting from a greater fool buying their house at an inflated rate. Unfortunately, the bottom end of town has dried up, so they are going to run out of people to fund their next move.

Remove the bottom card and the house comes tumbling down.

No more tax rinse, Dti in the works, LVR to stay, Banker now personally liable, Banks rejecting loans, and considering you maxed out on all your approved credit capability when you are not.

What do the banks think is happening...?

I thought you measured housing affordability as " median house price / median income ". Just report that.

Ignoring mortgage rates is blinkered thinking

Worst home loan affordability in the 18 years of interest.co.nz's survey

It was worse and now is worst....does it matter to FHB.

Not to shed crocodile tears as this is not bad but good for FHB and is bad for so called invedtors, speculators and real estate industry which thrive on FOMO and.......

The economics of investment housing is about to change, an investor is losing deductibility while cost of mortgage is increasing, this will be compounded by deposit rates increasing. The yield on the house versus money on deposit will be looking increasingly poor if capital gains are reduced or reverse . The relatively low risk and hassle of money on fixed deposit will be looking increasingly attractive.

isn't that what we asked for?!

I hope all the tenants have their deposits saved up

The best time to buy is when the news is so bad that nobody would in their right mind buy.

Are you saying that is now?

I think he is saying you would need to be mental to buy a house right now.

Don't worry! The labour government will come to the rescue of all mortgage strugglers. It will offer relieve for every mortgage holder who chooses so by lending them some money in the form of interest deductability. It expects to be paid back in the form of a sales tax when the mortgage struggler sells its house. One caveat: house prices need to keep on rising above the mortgage rate to protect the capital gain but it avoids the mortgagee sales.

I've had a big day, and all I can bring myself to say - which I think is more than enough - is that as a country we are rooted.

Slow hand claps for successive governments of the past 20 or so years...

The country being rooted is about as DGM as it gets 😂

Where are P8 or TTP to tell you that we just need house prices to go up a bit more to save us all from our mess and there’s no need to be so negative.

From a relative position, the country is looking pretty good.

Many facets of our perceived way of life are at an existential cross roads though, and we lack any form of vision or consensus to do much about it

Yeah Thanks Mr Orr & Mr Robertson

Money is the root of all evil. The MONEY itself.

Money is a nice tool. Is supposed to be the most fungible asset.

Every religion anyways condamn excessive desire (namely greed).

In a non moral/ethical way buddhism has the most convincing vision on desire. It makes you unhappy and makes the world a miserable place.

The vast majority feels that they need to have more.

Wise people feel rich when they have enough.

Enlightened people feel rich with whatever they have.

"A Zen Master lived the simplest kind of life in a little hut at the foot of a mountain. One evening, while he was away, a thief sneaked into the hut only to find there was nothing in it to steal. The Zen Master returned and found him. "You have come a long way to visit me," he told the prowler, "and you should not return empty handed. Please take my clothes as a gift." The thief was bewildered, but he took the clothes and ran away. The Master sat naked, watching the moon. "Poor fellow," he mused, " I wish I could give him this beautiful moon."

Makes me think of this quote:

“My riches consist, not in the extent of my possessions, but in the fewness of my wants.” -Joseph Brotherton, 1783.

wonderful :)

He didn't have to live in a damp overpriced home and pay the bank for the privilege. Or maybe he did and was happy. hmmm

Need little, want less, love more.

"...they [banks] had what should have been predictable effects on house prices and housing affordability".

Do you mean the same banks that said house prices could crash by 20-30% in March 2020? They were only out by around 40-50% - or more depending on how you calculate it. Add inflation, supply chain issues, war. All pretty predictable if you are a real world planner and not an ivory tower keyboard planner safe in your job.

The people that do this sort of things for a living on six figure salaries have less clue than most of the commenters on this website, regardless of their political and economic persuasion.

Nobody is coming to save you. The govt, the financial system, banks and advisers are all looking short term (next election) and are not interested in a fair system. Money talks, it always has and always will.

To be fair, nobody predicted early vaccines, money printing, helicopter money, low interest rates and so on. But again, these are the "professionals", why do they get it so wrong? We are no longer in a free market. We go along with it because we think they know better - yeah right.

I think nearly everyone, including the retail banks, underestimated just how insane the RBNZ response was going to be to the prospect of deflation and falling house prices. What central bankers have done to prevent depression and widespread debt defaults in 2020 is to create a bunch unintended consequences however that appear to be lurking around the corner and the not too distant future....no free lunches in an economy....you can't print your way out of trouble...the only way to improve your lot is to improve productivity...(and as PDK and a few others point out, there are limits to that also within the contraints of available energy).

Agreed. Problem is its the governments all around the world that are in charge of monitory policy. Mostly lay people. Awesome.

Well I was with the banks in March 2020, it was a guaranteed housing price crash. Then out of left field the RBNZ came to rescue and my -25% prediction went to +30%. Makes you pretty hesitant to make any form of prediction on the housing market because honestly everyone is just guessing at this point in time.

That's why I think it is really unfair for people to criticize those who bought in the last year or so as being stupid or deserving what's coming because they took their chances, etc. Sensible decision making with regard to the property market is/was impossible against a background of government/RBNZ making completely bizarre decisions, seemingly to prop up property market at cost - until they suddenly decide not to. Predicting when and whether the Govt would swoop in and pump up house prices yet again, or refrain from doing so, was nigh on impossible.

I would never criticize someone who bought in the last year or call them stupid or deserving of financial pain.

But someone who sees what is coming, and still dosen't try to sell, dosen't take action and call a rea and list their place.... well then yeah they probably do deserve the title of "stupid".

The crash hasn't happened yet. This is just the "itsy bitsy little gully" stage right now.

If people think it's gonna happen, then they should take action. Otherwise its like a man standing in the middle of a busy intersection and complaining loudly about the fact that he might get hit by a car. "It's so unfair... all these cars might hit me.... I deserve to stand in the middle of this busy intersection and never be hit by a car, wah wah".

Nothing is guaranteed in this life. We all must make our decisions and own our risk.

There were sensible decisions: Vote for a different government. Start a petition. Protest. Leave the country. At the very least, don't buy!

The other possible government party is the party of property investors....hardly a more sensible option for young Kiwis.

i wonder if the big four will still pay traders bonuses after bailouts?

Last year we were experiencing the lowest interest rates we had ever had in New Zealand. They were emergency rates. They were not going to last. The housing market was crazy. People were climbing over the top of each other to buy real estate. In South Auckland many became paper millionaires overnight. When markets get that silly and frothy it is indicating the top or near to it. Why buy then? You risk all or part of your hard earned deposit and you are borrowing more than you would need today. Some unfortunately will lose their homes. You could not tell them anything last year. The agents have a lot to answer for. For many the fear of missing out is too hard to resist.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.