‘This time is different’ are the four most dangerous words to string together when talking about economic trends and asset values in markets, and this time is no different.

New Reserve Bank Chief Economist Paul Conway gave a detailed and comprehensive speech this week about the housing market, in which he was hopeful the tide had turned on the ‘one-way bet’ thinking behind the obsession New Zealanders have with buying property as an investment above all else, which in turn has made our housing the most expensive in the world.

Here’s the core of his argument (bolding mine):

“Over the years, the demand side of the New Zealand housing market was boosted by strong population growth, steadily declining neutral interest rates and a favourable tax system. The supply side, however, has been held back by strict land use regulations, and a construction sector prone to boom-bust cycles, while carrying very high building costs. Excess demand led to New Zealand’s experience with some of the highest house prices relative to income in the world.

“A sense of ever-increasing house prices – along with a lack of other quality local investment alternatives – may have also distorted the investment options of New Zealanders. The share of housing on household balance sheets is very high and commercial banks hold a high share of mortgages on their balance sheets.

“Rapidly increasing land prices may have also led to a transfer of wealth to people who owned land as prices were rising from landless younger people and future generations, who have to spend more to buy land. This means that they save less, reducing the amount of alternative capital they own and possibly lowering lifetime consumption and incomes.

“Are these dynamics likely to continue in future? Since August 2021, the Reserve Bank has been tightening monetary policy, lifting the Official Cash Rate, to rein in inflation. This will likely see actual house prices move back towards sustainable levels that are more in line with market fundamentals. Indeed, in the May Monetary Policy Statement, we forecast a 15% decline in house prices from their peak, which would bring them roughly back to sustainable levels.

“Over a longer time frame, there are reasons to think that some of the core market fundamentals that determine sustainable house prices may also be changing. On the demand side, as the pandemic slowly recedes and international travel restrictions unwind, many New Zealanders are heading overseas seeking new experiences. On the other hand, immigration is unlikely to return quickly to pre-pandemic levels, contributing to slower population growth overall.

“In the tax space, the removal of interest deductibility and the introduction of a capital gains tax on sales of residential property owned for less than 10 years – the ‘bright lines test’ – will have closed some of the gap between the effective tax rate on housing and other asset classes.

“At the same time, urban planning rules are being freed up to unlock more housing supply. The Resource Management Act is being replaced and the National Policy Statement on Urban Development directs councils to remove overly-restrictive planning rules and to enable higher housing density, which is a critical part of the solution.

“In the construction sector, the Commerce Commission is carrying out a market study into competition for residential building supplies in New Zealand is working well and, if not, what can be done to improve it. These changes are consistent with more houses being built and currently high building consents translating into more actual houses. They also imply that housing market dynamics in future are unlikely to be the same as in the past. Given the importance of housing in our economy and national psyche, this will be a huge change.

“For several decades, we have traded houses among ourselves at ever-increasing prices in the belief that we were creating prosperity. But the tide may well have turned against housing being a one-way bet for a generation of Kiwis. We need to keep building a new approach to housing and economic prosperity in Aotearoa-New Zealand.” Reserve Bank Chief Economist Paul Conway in his first major speech yesterday.

Let’s check those assumptions

I suspect the Reserve Bank is being premature and a little too hopeful in saying the tide is turning. Here’s why:

-

longer term mortgage interest rates here may have already peaked and it’s not clear at all that the multi-decade fall in ‘neutral’ interest rates is about to be reversed;

-

migration may have stalled for the last two years, but the political drivers to unleash 2%-plus per year increases in population through migration of temporary workers remain firmly in place;

-

construction industry confidence has collapsed back to 2008/09 levels in recent months as house prices have started falling and bank lending has dried up, which means assumptions about supply becoming more flexible are premature, especially given industry structures, staffing and productivity remain predicated on such boom-bust cycles;

-

infrastructure funding to allow councils to pay for the pipes, roads and other services for their newly-upscaled district plans remains unresolved and NIMBY-dominated councils continue to push back and water down the Government-ordered intensifications at every turn.

-

the Government’s insistence (both National and Labour) on keeping net debt and the size of the Government’s tax share at or below 30% of GDP has prevented the Crown from funding the transport and water infrastructure to enable the intensification, and will do so for the foreseeable future;

-

the tax incentives powering the ‘over’ investment in housing remain in place, with both Labour and National seeing capital gains and wealth taxes as unacceptable to the median voters that decide elections; and,

-

the assumption about the Commerce Commission (and ultimately any Government) actually acting to improve competition in building materials to reduce construction costs is optimistic at best, given its track record with supermarkets was to abandon an industry breakup proposal with its final report.

Haven’t we been here before?

The broader problem for the Reserve Bank in trying to reset expectations is that it has tried before and this latest warning risks being another ‘boy cried wolf’ moment.

As I’ve reported before, here’s the lineup of boys crying wolf:

-

April 1998: Reserve Bank Governor Don Brash warned rental property investors expecting unending and high capital gains would be disappointed: “Far too many people still see getting heavily into debt to buy a second property as the best way they can save for their retirement, even though, in my view, they will be disappointed.” House prices have risen 330% since he said that.

-

August 1998: Brash said house prices were likely to rise in line with other inflation of around 2 per cent: “Property investment is not a low risk activity in a low inflation environment, and urging people of limited means to borrow heavily to undertake it puts them at risk of serious loss in today's circumstances.” House prices have risen 328%.

-

September 2003: Reserve Bank Governor Alan Bollard said after house prices rose 14 per cent in the previous year that rental property investors should soon expect real deflation: “I'm concerned that this could end in disappointment, especially for unsophisticated investors rushing to get on the housing investment bandwagon.” Prices have risen 218% since he said that.

-

September 2004: Bollard said the success of housing as an investment depended on the prospects for capital gains in the coming years because yields from rents were so low: “A reasonable view is that house prices are unlikely to rise much further over the next two years, and some falls are certainly possible, particularly in some regions,” he said. Prices have risen 174% since he said that.

-

June 2006: Bollard told central bankers in Switzerland that New Zealand house prices would start falling by the end of 2006 as higher interest rates took effect. House prices have risen a further 118%.

-

February 2015: Reserve Bank Governor Graeme Wheeler warned there could be a sharp correction in house prices. Prime Minister Sir John Key supported that warning, saying: “We are building a lot of houses in Auckland now. People can get a bit carried away with the fervour of these things and believe it is all going in one direction. History shows you house prices go up and down.” Finance Minister Bill English said: “There's no asset price that can go up at over 10 per cent a year forever, so sometime it will stop. And in this case we are really starting to get more supply coming at speed into the market.” Prices have risen 58%.

-

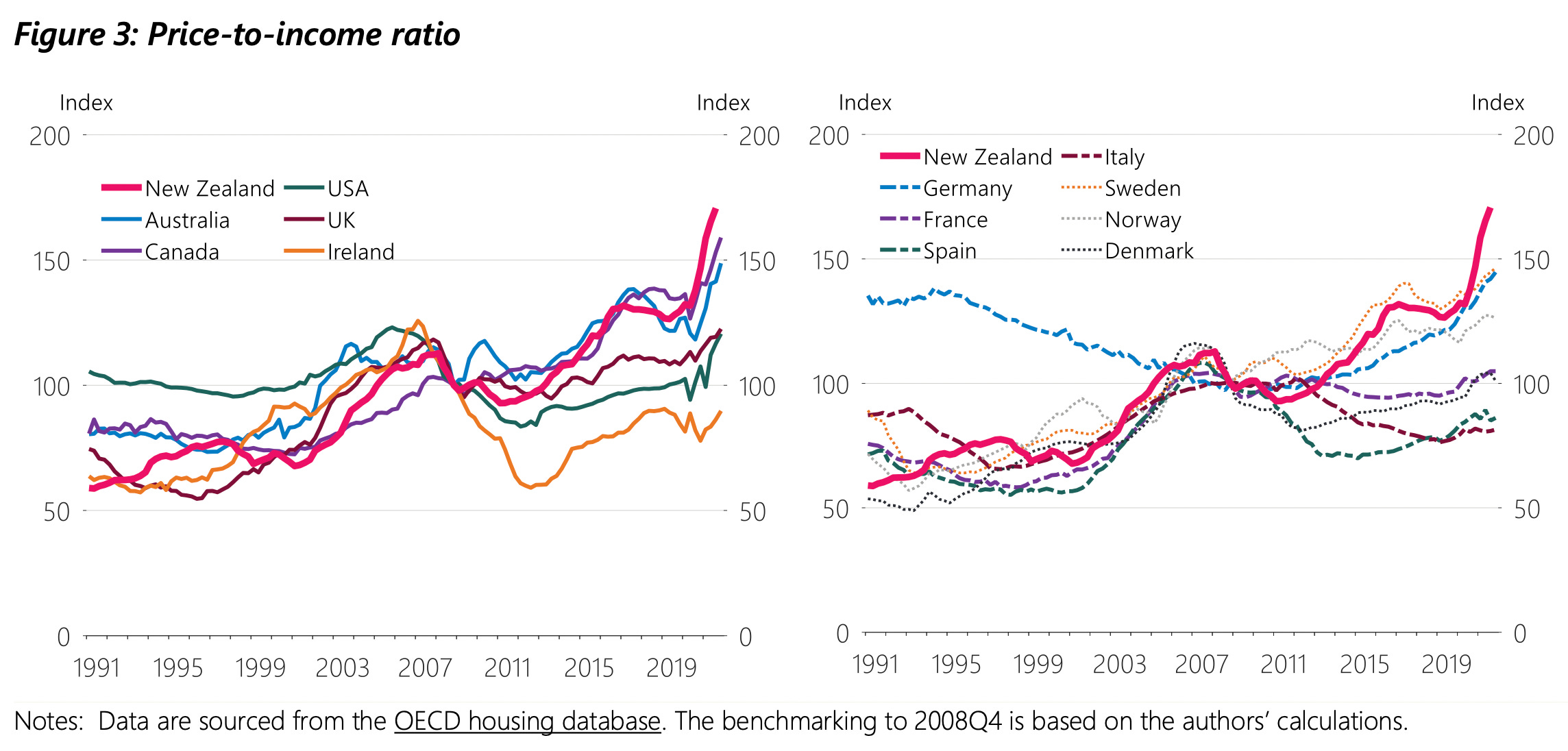

September 2015: English said the Auckland housing market was on fire and people needed to be careful not to get burned when prices fell. Wheeler also told MPs that month that Auckland house prices were not sustainable. “The house price to income ratio for Auckland is at nine. It's twice that for the rest of the country. A ratio of nine puts you, according to Demographia figures, in the top 10 most expensive cities in the world. This is just dangerous territory.” Auckland prices rose a further 38.6% since they said that and Auckland’s house price-to-income multiple is now almost 11.

-

March 2017: Wheeler said Auckland house prices faced a heightened risk of a sharp correction because of the risk of higher interest rates and the number of homeowners with high debt-to-income ratios. Finance Minister Steven Joyce said the tide of rising house prices was turning because of rising supply and a likely rise in interest rates from 50-year lows. “People would be mistaken – while you can never pick the turn of the market – they'd be mistaken to think house prices will keep going up the way they have.” Prices have risen 25% since they said that.

-

September 2017: English and then opposition leader Jacinda Ardern in an election debate were asked if they wanted house prices to fall, English said: “I want them to stay flat while incomes rise.” Ardern said: “We don't want them to lose their value, but we want more affordable housing in the market as well, and that is what is missing.” Prices rose 23.9%.

The too-big-to-fail problem

The other bigger problem unaddressed in Conway’s speech, but still in the back of everyone’s mind, is that even if the Reserve Bank thinks house prices are over-valued and therefore likely to fall, the housing market is different to other asset classes in three major ways:

-

our banking system is now reliant on house prices remaining elevated to support its profits and asset base, with a serious slump (50%-plus) to properly affordable prices being unthinkable from a financial stability point of view;

-

the Reserve Bank’s own research has shown that a collapse in net wealth because of a crash in the housing market would rebound into the real economy as home-owning consumers would be expected to reduce their spending by around five cents in every dollar of wealth destruction; and,

-

a crash of 50%-plus would not be acceptable politically and would trigger a change of Government and or policies to stop such a fall.

I hope this time is different, but this isn’t my first rodeo. Assuming a hands-off approach to asset prices, I expected the Reserve Bank and the Government to allow house prices to fall 30% in 2008/09. They didn’t, and they repeated those actions in 2020 to stop a collapse. They would do so again, possibly even before the year is out.

Realistically, the housing market is not only too big to fail. It is too big to be allowed to fall too far. The Reserve Bank has already said a 15% fall from November’s record high is far enough to be ‘sustainable’. That would take prices back to where they were in early-2021 and mean home owners ‘keep’ at least half the 20% rise between the March 2020 interventions by the Government and the Reserve Bank and that peak in November 2021.

A Reserve Bank that believed house prices should and could return to affordable levels would expect and not intervene to stop a 40-50% fall to levels relative to incomes and rents last seen in 2003. The fact the bank and the Government baulked at the idea of including affordability (rather than ‘sustainability’) in its mandate tells you everything you need to know. Neither have even suggested which level of affordability they prefer to use or where it should be.

A Reserve Bank that was determined to reset expectations would use its tools to drive actual prices to those affordable levels, which it could do with interest rate and/or bank capital controls. The last time expectations about prices (CPI inflation) were out of control was in the 1970s and 1980s. The collective response then was to rewrite the Reserve Bank Act, give it independence and allow it to create a brutal recession to drive expectations lower. Neither the Government or the bank intervened to reverse or stop the political and economic pain. Those resetting of expectations then were a feature — not the bug.

More jawboning to try to convince homeowners they are wrong to keep seeing houses as the highest returning investments7 will fail unless it is backed by the political and regulatory changes to make it happen. Hoping it will happen is not enough. We’ve been here before. It didn’t work before and it won’t work again.

So how could it be done?

These are the things needed to actually return house prices to affordable levels:

-

changing the tax incentives for residential land ownership by taxing either the capital gains for all homeowners, or taxing the value of land, especially unoccupied residential zoned and serviced land, as well as capturing the capital gains from rezoning or public infrastructure investment through ratings uplift capture rates;

-

changing the collective political views about acceptable levels of public debt and the tax share of the economy from the current ‘consensus’ of at or below 30% of GDP for both net debt and the tax share of GDP so the Government and Councils can invest in housing and transport infrastructure; and,

-

collectively deciding to target a housing affordability measure and giving independent Crown agencies the power to drive house prices and rents there, regardless of the effects on household wealth and inflation.

Median-voting homeowners can’t see any other way. Yet.

None of these things are politically viable in the current environment. So I wouldn’t expect much to change, and most median-voting homeowners know that in their bones. That’s why they effectively have accepted the National and Labour policy prescriptions over the last 30 years to keep net Government debt and tax at around 30% of GDP and to keep capital gains on owner-occupied residential land tax free.

The only way that might change is if those same median-voting households realise they are enabling and supporting the creation of an increasingly unequal two-tiered society split between home-owning families and renting families. The biggest pressure point for those home-owning median voters is the situations of their children, and whether they are prepared to keep donating equity to children for deposits, and/or having to watch their grand-kids grow up on skype or whats app, or on brief visits to Australia etc.

So far, none of the polls or policy prescriptions I’ve seen would suggest we’re anywhere near that sort of tipping point.

159 Comments

No mention of:

- impact of people leaving NZ? Are professionals here being replaced by fruit pickers?

- external factors like interest rates overseas - either we keep up or NZD declines meaning imported inflation means less cash in the economy for housing

- general confidence/sentiment - as you note people don’t do what experts think should happen - feels low right now….

Not every house is the same - quality clearly will retain value over older smaller houses with maintenance issues so I see a fragmented market.

Well researched and insightful article.

The idle chatter about a housing market collapse is misguided nonsense.

TTP

Tim, youve conveniently ignored our winning streak against the Irish on the biggest decline in house prices in a 12 month period. Odds are we will continue to win. On reflection, the RBNZ now knows how to REALLY create epic bubble. Odds are they won't be able to safely deflate it - go NZ! 🤑

NZ are very good at whipping the oirish - go NZ

If Crash Crusader (aka Retired Poppy) says there's going to be a crash, then we can be assured there won't be.

Consider his record of forecasting accuracy. He's always wrong.

TTP

Looking on the bright side, RP is consistent... always wrong

BH complicates his argument with lengthy bs to make it plausible. In the end like RP he is also always wrong. Maybe they are one and the same person haha.

Accountant Matthew Gilligan in 2014 stated the numbers that owning beats renting and investing. Except in the lowly Rotorua, but even that would have proven to come out on top in the last 8 years. Link below

Renting versus owning: Is home ownership bad business?

https://www.gra.co.nz/articles-by-matthew-gilligan/the-cost-of-renting-…

Matthew Gilligan got things horribly wrong in recent years though.

He made the basic mistake of thinking that rates would stay low, and discounted/ignored the risk of rates rising. Essentially, he thought that houses were "worth" more when the OCR was at emergency low levels. Any clients who listened to him and took on large debts to buy property at low rates will be sweating bullets soon enough.

Retired Poppy was not "wrong". He was early. There is a very big difference.

Retired Poppy acknowledged risks, and was risk adverse. Matthew Gilligan saw dollar signs and chased them.... "woo-hoo! Money scramble, fill your boots with cheap debt!"

Following RPs approach may mean that your portfolio does not perform spectacularly during a boom. Following MGs approach may lead to financial annihilation and bankruptcy.

2014 😂

It was better to own than rent with the DTI back then

HW2 - Dont you own several rental properties - how are your rents and values holding up?

Are you buying more at the moment?

I might have, oh how terrible.

MG wasn't an accountant just charging an accountancy fee, was he? He has also a developer and selling properties to his database.

But was doing it as per the rules of the time, ie no laws were broken. But the law can be a bit of an arse, and one issue that can be misrepresented is that it shows today's figures and extrapolate them as an averaged trend over time.

And while that may be the best guestimate you can do, most of the clients assume that is a given, and as we know it never is like that, taking into account that many clients' personal circumstances also change (who would've thought?) so with hindsight many are disappointed, some greatly, and most are ok, or at least not disappointed enough to complain about it.

Not dissapointed enough... yet.

Every VCM in 2021: Property prices aren’t going to fall

Every VCM in 2022: Property prices aren’t going to crash

Every VCM in 2023: -30% isn’t a crash, it’s a correction

Every VCM in 2024: The property market is dead. I now work in ‘__________’

That’s my prediction.

House price’s have never been 12 x average wage couples annual income for small 3 bedroom house in run down area in Auckland. Only way market is going is down now the bubble has burst prices will just continue to fall over next few years, and most people in the country are happy to see this happen this will be a once in a lifetime crash, this is not DMG just facts if you are over leveraged sell what you can or become insolvent but stop complaining and ignoring the fact that bubble has burst and house prices are crashing at quickest speed ever seen. Rates and inflation are climbing NZD is tanking marking inflation higher RBNZ can’t do anything about crashing house prices as most of the population can’t afford to buy if they do not own a property already.

It’s no DGM - it’s simply basic economics and fundamentals - no one likes to lose money and anyone holding an average NZ house at the moment is losing circa $600 a day!

No one believed in January that the Auckland REINZ index would be down 13.5% by June but it’s happened

As it only takes one seller to meet the market and it resets prices in the street

This is the crash playbook… look at every property bubble burst in history and we’re actually tracking faster falls

So what’s going to support the market and stop the falls?

Only demand/buyers can, but where will they come from?

FHB’s? - They can’t get the finance, because the numbers don’t work - and if they can, no one wants to lose their first 10 years of principle repayments (20%).

Investors? - Everything is stacked against residential investment. The numbers simply don’t work when you’ve got 4% yield for term deposits. Do you know any investor that are looking to buy more?… everyone I know is trying to sell some and pay off debt.

Owner Occupiers - have no real demand impact

I think the property market is actually quite resilient at the moment because alot of people still think it’s only a correction and not going to crash

Once the herd accepts the reality (when the headline says we’re -20%), there will be a stampede for the exits from Mom & Dad investors - my guess is this is mid 2023

That's when you'll accept $400-500k for the apartment you wanted $850k for last year.

But who's going to buy it?

I suspect that both you and Bernard are right, so take note young Kiwis, there is absolutely no hope or future for you in New Zealand. Get your qualifications and leave as soon as you can.

Industry and employers may well follow them. The salaries that they are going to have to pay to retain staff that can afford housing in NZ will severely damage their ability to compete. Certainly, staff and employers best hope of remaining in NZ is to move out of the large unaffordable cities, as we are starting to see.

Gentrification of the provinces, here we come!

“impact of people leaving NZ? Are professionals here being replaced by fruit pickers?”

Wrong assumption we’ve been making for the last 20 years. This is one of the reason why we are where we are today. Many immigrants are “loaded” or are very good “savers” and they are all very determined to make this country their new home.

No examples of people expressing concern about house prices falling between 2017 and 2022. The government should have signaled strong warnings during the main pandemic period of money printing.

That said there is a lot of hysteria in the comment threads. There was hysteria before the pandemic about dramatic price falls which eventuated to nothing, in fact the complete opposite. There will be hard times for some but not to the extent some people are imagining.

Yeah I agree there’s a fair bit of hysteria here. While falls of at least 20% are quite likely, some people here are talking 50% plus and I think that’s highly unlikely.

I dont think we'll see 50% but I can easily see 35%, which would take us back to pre covid prices or a median of $850k in Akld

Actually if you do the maths if the market appreciated 35% it only needs to drop approx 25% to get back to the starting figure.

The implosion of the New Zealand property bubble will occur when the government is unable to prevent it.

It is well beyond the point of inevitability, just a matter of time now.

Let's hope that the victims that Printer8 led to their doom enjoy the intrinsic value and pride that comes with being deep in negative equity.

Most of what is cited is noise.

People tend to get too hung up on migration, the cost to build, and general demand.

The key driver is inflation.

NZ inflation tracks US inflation. The only direction this is heading is up. This has direct consequences on interest rates, affordability, demand, migration etc etc it’s pretty simple.

In short there is little that can be done to prevent this overinflated bubble bursting.

What if the rb printed another 20 bil?

Or the government subsidized building priduct to lower the cost of building houses.

There are plenty of ways the government or rb can support their voter base.

It would make inflation worse as more money chasing same amount of less goods as production will not increase in step with poor investment..

"What if the rb printed another 20 bil?"

Well this is a real possibility, but they wont print until inflation is somewhat tamed. We will be in recession before that happens.

It would seem stupid to invite more inflation and start inflating bubbles again right after youve experienced the bursting of your last bubble, but it is the only playbook they have.

To me its inevitable, and we are in for a reality check that none of us have seen in our lifetimes!

Lol Alec. "The key driver is inflation". Ah, yep, that would be right. But guess where you should put your money in inflationary times? Yeah, that's right, real assets. Like property. In NZ, property prices have outstripped inflation from 1964 until now, with only one minor blip, the 1973 oil shock. And then only for a short time. No one can predict what will happen in the short term, but in the long term, prices have never failed to reach previous highs. So, if you think there is going to be a crash, sit on the sidelines. See how that goes for you because I'd bet you won't be able to predict the bottom, nor when it will rocket back up. But good luck.

Agree - I have watched property for over 40 years - & you are quite right

The notion that you can’t predict short term is flawed. Further OCR increases this year are almost certain. The momentum is clearly downwards. Sadly many people are over leveraged.

A 20% drop in house prices, is a 100% of many purchasers deposit. That’s the risk of buying. Given Auckland and Wellington have already dropped 12% they don’t need to drop that much further for it to look ugly.

Property certainly is not the low risk option. You could be waiting 5-10 years before you recover your investment. Until then there is a reasonable probability it’s a millstone weighing you down.

The only way house prices increase is if wages increase substantially or inflation goes down. Neither are going to happen quickly.

Property is a secure bet if you can wait long enough. During a downturn that’s when there is greatest opportunity and cash is king.

Hi Brock Landers,

Again, you’re inebriated with the exuberance of your verbosity.

TTP

Brock : it stands to reason that NZ has the most incredibly priced houses in the world ... because this is the most fantastic , awesome , go getter country on the planet ... isn't it ...

... which explains why a generation of younger Kiwis are heading off to Australia & beyond ... they're just gagging on too much wonderfulness in this splendid land , girt by sea ... we're 110 % purely the best ...

“... which explains why a generation of younger Kiwis are heading off to Australia & beyond ... they're just gagging on too much wonderfulness in this splendid land , girt by sea ... we're 110 % purely the best ...”

…and many regretted and eventually returned to NZ realising grass isn’t exactly greener on the other side ? They sadly ended up with nothing much and sometimes don’t belong to anywhere…….

We often hear they say “ I’ve been living in Aus/UK for the last 20 years…oh and I decided to come back…” and that’s when you see the “I’ve wasted 20 year of my life” look on their face. Tragic.

That’s not my experience. I came home due to ageing parents, to get my children through Uni and to make sure I qualified for Super. All done now. Children have gone overseas and only a few years until the taxpayer is supporting me.

NZ, a great place to raise children and retire. The middle years leave a lot to be desired. We are a tiny country at the bottom of the World. If you are narrow minded enough to think it’s the best the world has to offer, then the blinkers are firmly fixed.

I am lucky enough to have been here all my life and prospered. Not yet in my 60s, I could retire in style if I want but love being productive

“That’s not my experience. I came home due to ageing parents…….if you are narrow minded enough to think it’s the best the world has to offer, then the blinkers are firmly fixed. ”

Good for you and sorry that you had to give up and come back for family reasons.

Perhaps people considering leaving should learn from your case and consider their parents in the future?

NZ is not the best place in the world I know but it’s one of the best place, I have lived in a few places and I wasn’t born here so i don’t taking things for granted in this country.

Thanks Rex, a good comment. Like so many I know who have gone overseas and then returned. Best place to raise kids and retire. Quite correct. Issues for youngsters are salaries, taxation and Labours fixation with supporting bludgers and criminals.

Gee the DGM's don't want to wake up and choke on their Sunday morning coffee reading this !

Scary that we have a the world most overinflated housing market and the only reason we have for predicting that it will not drop too far is that it is deemed ' too big to fail'. Thus we confidently predict that someone will surely do something to stop it happening if it slides ...

I do get that inflation might peak and the ocr predictions might be correct and the exchange rate might stablise in a reasonable range. However all recent predictions havent been very accurate so will i probably be very conservative in spend and investment while it plays out.

First the CCCFA changes were saving grace for the housing market downturn. When it’s obvious that wasn’t going to work, people are turning to interest rates and ocr peak. It’s really not certain what will play out at all.

In my honest opinion thinking that “this time is different” is better aligned with thinking there will be some saviour to house prices to keep them afloat. Are there any other examples in the past where a housing bubble which was among the most expensive in the world popped and was supported almost immediately after?

To my knowledge, a greater correction/crash is the most common scenario here and thinking anything else is thinking that “this time is different”.

Denial is the phase prior to panic on the bubble model. Numbers of people now listing and heading for the exit suggests something is happening. Even Ultra Bull TA wrote once the herd panics, logic no longer applies.

Place you bets, spin the wheel, double down on debt, stack those rot boxes at millions of risk denominated dollers. If not, why not...?

Is it Time To Panic, or is it Time To Profit...?

“once the herd panics, logic no longer applies.” - in this case it might be the only time logic applies.

After I was so wrong predicting a house price crash at the beginning of the pandemic I don't think I will ever bother to try and predict another. From here I see rates level out by Christmas to historical norms and then flatline to protect the housing market. Places like Auckland and Wellington will get hit with 15% drops then slowly recover over years like the GFC. Those predicting a huge crash will be disappointed yet again.

Agree!!!!

Agree. The popcorn eaters (DGM) will be upset……

Mind you, they’re getting used to it. 😰

TTP

I wouldn’t feel confident in guessing what might happen this time. I think Hickey is pretending like asset price crashes are logical things based on quantifiable factors but Behavioural Economists have a much stronger proven track record for tracking market behaviour than any “normal” economist.

What will determine the degree of correction this time will be psychology. People like to make comparisons to circumstances and conditions but the world is a complex web of relationships. We have had an unprecedented era of rising property prices and not even the GFC shook the Kiwi heart felt belief in the security and reliability of their housing market.

But if prices drop sufficiently and for long enough to spook the herd? If the recession leads to job losses? If stagflation leads to conservative mindsets?

That’s when the current almost certain 20% drop could worsen to a 30-50%.

And there are variables not being mentioned by Hickey too. Whereby a sustained era of stagflation leads to a long slow bleed in house values. And a long slow correction in rents etc. A longer war, escalating de-globalisation. These are huge factors of significance that RBNZ and the government was powerless to address.

I was in the UK during the GFC, centra bank interest rates quickly raced down but commercial banks just wouldn’t lend. It was the credit crunch that prolonged the correction (which was in large part psychological). There are many more factors than Hickey mentions.

Agree ginger - people appear to be trying to rationalise irrational behaviour.

Believe it or not even the DGM know the market will eventually come back, times like these are the “feel good” times for the DGM so just let them.

We have been here before, in the mean while just grab some popcorn and relax.

Is that 15% off peak? Both around 12% now. This would be 0.5% per month for the rest of the year and currently trending at 2-4% per month. True impact of rate hikes will take time to settle in but I can’t see an easing of the OCR having an immediate upward impact on house prices.

No DGM, but with all of the current data it would require a serious handbrake to stop at 15% by the end of the year. Agree with others though that I can’t foresee 50% peak to trough. The worst still to come and we’ll have a clearer picture after that

What about places outside Auckland and Wellington? Is an average house in an average suburb of Palmerston North really worth $700k? It’s hard to see how either the land or the building could be worth anything like that.

It will drop more than many on this site want to admit purely because of the large numbers of young people leaving NZ for a bigger income and a chance to save for their first home. Nurses, doctors, tradespeople and teachers. People we can ill afford to lose. Us baby boomers who have been incredibly greedy have caused the problem we now face in terms of unaffordable housing. Look forward to travelling overseas to meet and see your grandchildren.

Where will they go though? Of the 6 English speaking countries, only the US has affordable housing, and only in the states run by religious nut cases.

They earn more in Australia. Considerably more. Pure and simple. What more they earn they can save for housing. And let’s not forget that 12per cent super. If they decide to buy their first home in NZ and rent it out there’s a currency imbalance in their favour currently. NZ dollars buys 91c Australian currently. Personally I know of six who have left for Europe, Middle East and Australia. 3 teachers, one builder, an it specialist and a marketing professional. The builder went to Australia with 3 mates who are all tradies. This is just the start. It is all very well houses coming down in value but those rising interest rates are making it harder to borrow what you need to buy especially for FHBers.

Surprised about the builder, having had some tradie quotes recently I don’t know why anyone would leave when you can make 2k for a days work. The teachers will be an issue, surprising that a labour govt have been so stingy on the public service salaries.

Don’t know if Aus is a great option for builders right now, if anything construction is slumping quicker in Aus than here.

He won’t care as his hourly rate has nearly doubled plus super. Their dollar is nearly 10 per cent stronger. Warmer, some things cheaper such as petrol. Cheaper rents where he has gone and rentals are warmer there. He has done renovations on my home. He is only in his late twenties. A very good builder and a hard worker. He will do well there. His boss here is gutted he has gone but we don’t compete with wages over there. We are a poor country as we have put too much emphasis on housing for investment. I Australia they have 3 trillion invested in their super schemes.

He'll probably care when construction companies start going bust though and he's no longer employed

Agree, I’m also thinking the government (be it labour or national) will come in shortly with some sort of deposit guarantee scheme to get the punters back in at the bottom especially now banks aren’t touching anyone with less than 20%, this is the only way to keep the ponzi going.

stewinz,

You are clearly unaware that before next year's election, legislation will be enacted to provide just that- a deposit guarantee up to $100,000 per person per qualifying institution.

When they said (more or less for every issues they had) that there is no silver bullet what they actually say is that they can't predict the consequences of doing anything.

You might be right, they might do something like that.

Predictable consequences:

- house values up (maybe)

- rents down (very much)

- inflation up => ocr up

- etc...

Govt will always be accountable for actions, inactions are always more defendable (sad, right?)

So, that's to say, I don't think they will do such a thing

Carlos who is going to buy even with 15% off. FHB and average wage couple have no chance only people who can afford to buy is those selling and buying in same market and as prices fall this will become harder, with rates and inflation going up and NZD tanking we will see larger falls until the general population can afford to purchase.

rates level out by Christmas to historical norms and then flatline to protect the housing market

So your prediction is now that regardless of inflationary pressures, NZD, global factors/influences the housing market will be protected?

Yeah I'm with you Carlos, I get tired of the doomsters. Everything goes up then down, so what. Get used to the way the world rocks. Thing is, just keep focused and carry on with your ambitions. Things may not always work out how you invisage but if you don't give up things always turn out alright.

In a nutshell - the problem is us - a population too stupid to forgo $ now (property as a tax free gain) in order to achieve a far better (productive and wealthy) collective outcome tomorrow.

But mostly that stupidity is encouraged by weak leadership who will continually give the spoiled kids what they want every time they stamp a foot (election time) - as a result we’re continually getting what’s not good for us - but we wouldn’t for a second accept a govnt who didn’t roll over every time we threw a tantrum.

One of the tricky bits of a democratic system.

Were in this mess because elections (both national & local) are a popularity contest. Most candidates are not up to either job and in reality they are just front people, as the main decisions are still made by those in the departments the elected officials supposedly control. We have a political system that allows the next lot that gets into power to undo anything the previous lot did just because it doesn't fit their narrative. There needs to be more cross party co-operation as governments should be working together for the good on NZ, not just their respective ideology. It may also help if there was more long term thinking involved, rather than only looking forward to winning the next election which is difficult when hard (unpopular) decisions about our collective future need to be made.

Can't tax gains without inheritance taxes and you'll never have seen the BBQ committee purse their lips and shut up as fast as when you ask them about paying 39% on the proceeds of the sale of Mum's house.

Can't do THAT, they need THAT windfall, they've been waiting AGES. Farmers and investors are one thing but this wouldn't be fair.

Indeed! Far better to strip family assets and have a public spend up on the latest political vanity project.

Bernard, if the argument is that to be affordable, house price should fall by 40% to 50%, you are correct as both RBNZ and government will panic, if it to happen and are bound to throw everything in their power to boost ( as have done earlier) but that is if the situation can be controlled as one has to remember that no reserve bank and government of the country will like to see house prices falling by 40% to 50% BUT still it happens - though agree with you that NZ will not see 40% to 50% fall but this taking argument in extreme as even 20% to 30% will be big, which seems to be happening.

Also do not think that RBNZ is talking about 40% to 50% fall, it is just saying that notion that house prices will always goes up - specially speculators / flippers may be disappointed. Home owners do not worry about about monthly / yearly fluctuation as are mostly in for long term.

You are talking about 15% to 20% fall, which has already happened, so can you be bold enough to say that this is the end of the fall and also mortage rates will not move up - much.

It will be bold of you to say that mortage rates have peaked or literally peaked and house price fall has peaked or literally peaked.

Sorry, 15-20% hasn’t already happened. At worst, places like Auckland are down about 11-12%, so far.

Auckland was 11 - 12% down according to REINZ index in MAY. We're already in July now..

Fair enough but that's just Auckland what about on a national level ? My prediction is for Tauranga not really interested in Auckland for several reasons.

I heard a joke last year that I only find funny now: At an open home, a couple asked the estate agent whether she could show them something in a slightly higher price bracket. She replied that she'd be happy to show them the same house again 'tomorrow'.

Well, that scenario is definitely playing out in reverse now. If you don't like the price now, just wait a week or three..

I assume then Bernard you have invested all of your personal wealth in the NZ housing market?...if you believe what you have written it is the only logical thing to do.

Unsustainable means exactly that, the only unknown is the timing.

Didn't Bernard call -30% after the GFC?

Well he was wrong then, which was lucky for him because his profit on the sale of his Epsom home set him up for life ...

The first 15% fall is just the hot air from the last half of last year, probably a non issue to the sensible investor who would not have paid the crazy prices last year. Auckland cannot sustain a 3 to 500k premium over Australian cities. It would be healthy for the Auckland average to correct to 900k to a million in many ways.

Hickey has called all sorts of things and pretty much been wrong every time. Mainly because his political biases seep through everything he has to say. I have found In general, that it is good to listen to what economists say, then ignore them.

RNZ 12 August 2008

Bernard Hickey, from financial website interest.co.nz, says predictions of a minimal housing market slump are not credible, and predicts a fall in nominal house prices of 30% over the next two years.

If you read the article he said:

I hope this time is different, but this isn’t my first rodeo. Assuming a hands-off approach to asset prices, I expected the Reserve Bank and the Government to allow house prices to fall 30% in 2008/09. They didn’t, and they repeated those actions in 2020 to stop a collapse. They would do so again, possibly even before the year is out.

When you've seen the same thing play out over & over again, why would you now expect a different outcome...

To be fair, economists predict falls and never anticipate the level of government intervention.

In early 2020, when covid was coming into public consciousness, economists were predicting all sorts of calamity, only to have their jaws drop at the level of financial injection provided by government entities.

But yeah, I'd pay attention to an economist, but only if they have a track record of years or decades of 10s of millions of dollars of financial success predicting markets.

An excellent Chronicle of serial stupidity. The median voter has little Choice in an election as both main parties are in lockstep on housing. I suspect you are right and the government will not allow housing to fail perpetuating the ponzi. Only if outside events take the decisions or options away will we see a substantial fall these could be if financial turmoil arises from war or financial disruption such as runaway inflation and interest rates as in the eighties.

I had more sympathy for these views last year. Indeed, the housing market being ‘too big to fail’ was one of the key reasons I predicted a peak OCR of 1.75.

But I still think it is too big to ‘fail’, it’s just that the threshold for ‘failure’ is higher than what I was thinking.

The threshold might be falls of 20% plus rather than 10%.

I think that come the end of this year the OCR hikes would have ended, and by May 2023 they will start reversing. Because the country will be in deep recession AND prices would have fallen at least 15-20% and at danger of falling further.

I don’t buy the too big to fail, I doubt the RBNZ will prop up the housing market, it’s not really their job to do so. Maybe if there was a banking collapse they may consider it.

But it is likely that these high rates will cause a recession which will kill off inflation and allow the RBNZ to reduce rates again. Same outcome, but different reason.

Apart from the fact that up until today the RBNZ has been clearly protecting the housing market. Your blind if you cannot see the softly softly rates rises over the course of a whole year giving people the time to refix for 3 to 5 years was clearly intent to create a soft landing. Ultimately only very few people will have lost significant money and they will not care. I bought a house in 2005 and never even noticed the 2008 GFC and 5 years after that nobody cared less.

But the majority of people have not been refixing for 3 to 5 years. The vast majority are still on shorter term rates, and will need to refinance at much higher rates in the next 12 months or so.

Exactly, Carlos you are an outlier, not the norm.

You may find this hard to believe, but a large portion of homeowners are probably unlikely to watch mortgage rates on a daily or weekly basis. Most of them are too busy with their day jobs and topics that interest them to be concerned. A lot of them could tell you what their monthly mortgage payment is, but would have to dig up their loan documents to tell you the interest rate.

all of which makes some sense -- if not for the elephant in the room -- Inflation - as long as there is 7%+ inflation almost all traditional prop up government interventions are basically unworkable in an inflationary environment in the last year before an election? There can be no mass printing press activity - no huge spending - no large tax breaks -

And i dont see inflation easing anytime soon -- the cycle of price increases is now well established -- we still have further currency pressures -- and the Russians are not stopping anytime soon - ant eh EU and USA dont seem to have the inclination to actually address the invasion -- They would be quite happy to concede Ukraine territory to Russia to end it but Catn see Ukraine agreeing to that!

Not a very convincing argument from Bernard Hickey who's more or less saying that the NZ ruling elite has the power and ability to prevent asset price crashes when no other bubble pop in history has been predicted and prevented by its ruling elite. If anyone has evidence to contrary, please enlighten me.

It does look like just another example of the ol' Kiwi exceptionalism, which is ultimately a product of the bubble economy anyway. Bernard probably believes that our banking system's ability to create credit and manipulate buyer behavior is omnipotent.

Discounting the possibility of a property crash is for the foolish IMO.

The Japanese have been trying to get their mojo back for decades.

I guess a question still revolves around what is a ‘crash’? Some say 20% some say 30%.

I think it’s contextual, probably in current context I would say a crash would be 25% plus, 20% would be a very significant correction.

I definitely wouldn’t write off 25% plus, but I think 20% is more likely.

25% is the equivalent of an $800,000 unrenovated 1960s 3br house in Dunedin dropping to $600,000, when the same house was worth just $450,000 in 2018. I’d be surprised if it levelled off at 25% tbh.

How you can write an article of this length about current situation in the housing market and completely ignore the role of inflation and the massive spike in interest rates?

I have enjoyed a lot of Bernard’s writing, but he is displaying a breathtaking blindspot. I believe he is still talking about inflation being “transitory” months after that line of thinking was proven to be completely misguided.

All of the previous “warnings” about the housing market there was always the flexibility and conditions that allowed rates to be lowered to avoid or cushion any price correction. That flexibility is gone as inflation is triple the target level.

Yes agree. Bernard also does not see the fact the the US Fed is now belatedly, yet finally, resolute on taking the now re-sharpened Fed axe to attack the out of control US inflation.

NZ has no choice but to follow and raise our OCR at larger rates. If we don't, it will be $250.00 to $300.00 to fill the "fuel empty" warning dash flasher - in the multiple family vehicles everyone now has.

The NZD must be defended - The RBNZ only has tough and tougher options currently! Higher OCRs are a dead cert.

Bang on NZG great post. I know a few 'mum and dad investors' and people who are stretched mortgage wise on houses in NZ.. they are happy riding out this interest rate rise as they see it as a blip.. and truly believe the government will intervene if things get bad in the housing market or economy generally.

The issue is that we cant control overseas events and our hands are tied if inflation overseas gets worse or draw out (and i think the key players of russia / china / Mid East who can help are not in a mood to assist becausr it doesnt meet their needs to do so - in fact they gain in a lot of ways from our inflation) and if the fed raises rates to really high levels we surely have to follow. Its a massive risk.

I dont understand what we expect we can do locally to counter this. If we try to drop our rates while everyone else is raising theirs then we will get unacceptable massive inflation and social unrest from a resulting huge drop in the kiwi dollar.

Its a risk that in most markets would affect prices substantially.

Yes we are definitely very exposed to offshore inflation. I don’t personally see that panning out, my guess is that oil will be cheaper in 1yr than now, but if it did keep increasing as you say the RBNZ would have to match the US feds interest rate rises to prevent the Kiwi falling off a cliff (it can’t fly by itself).

From what I am reading i cant see why oil will drop in price.

- Russia is happy selling its oil to India and China, and not in a rush to end the war in Ukraine. Its had it with the West

- The Saudis and rest of the M.East is concerned about the push by the west to drop oil consumption for climate change reasons (its their economic engine) so is not keen to ramp up production, high prices suit them going forward.

- The US oil industry is struggling to recruit as they lost their revenue from the US government and scaled down.. expecting demand to keep dropping until new energy sources kick in. People arent keen on a career in oil or to invest in oil for that reason. And people who switched career dont want to come back. so they will struggle to ramp up again.

Coal and gas probably in similar situations due to climate and ukraine.

Food will follow a similar trajectory due to Ukraine and China (supply chain prices) has stated an intent to keep lockdowns in place and covid out.

I am keen to see how we kill inflation without killing demand (via rates rises and recession) in the west.

I think there is a chance that inflation has peaked though. At these prices there should be new supplies of oil coming on board, we have probably hit the peak of the building boom so material prices should in theory stop increasing, and people are feeling pessimistic so probably not asking for 7% pay rises. There is actually a chance we could get some big deflation once the heat comes off; it will be hard to sell building materials at crazy prices once the building industry collapses, shipping prices should eventually come down, and oil prices could come down particularly if the Ukraine war ends. Things could change very quickly. Or they may not who knows.

The economic "ëxperts" failures are renowned, year after year. They are often out of touch with the trades, soccer mums, average Joes.

I take my actions from having as many common man (myself included) and Main St touchpoints as possible.

Our thinking is as good as anyones!

I think we should expect Black Swans, from any direction. Expect uncertainlty, like never before!

Russia to continue to wield its energy power, retaliate in many directions, cut supplies, nationalise assets.

One major storm in the Gulf of Mex would likely shutin millions of barrels of US oil/gas production. (This is Europe's major new energy supplier hope - of the future)

Oil markets are incredible tight. De-globalisation/Inflation will rattle us for the future imho- until a crash ofcourse, destroys demand.

https://www.bloomberg.com/news/articles/2022-07-01/jpmorgan-sees-strato…

I seem to remember about a decade ago oil prices climbing at similar rates, lots of predictions on here of “peak oil” etc. but then a lot of fracking in the US became viable at those prices and then prices dropped massively. I doubt all those frackers will be quite so keen this time as they no doubt got very burnt, but the more viable ones probably will.

And the regimes of Venezuela and Iran will become suddenly more acceptable to the US and its allies.

Yeah I agree that there is case that inflation has peaked. And well put Jimbo.

people also need to keep in mind the fairly obvious fact that inflation is the change in prices. Prices may remain around very high levels, and increase a little bit more, but that would mean inflation has slowed very significantly. If you catch my drift.

with demand starting to slump I consider that further significant price rises in many sectors will not be possible without ruining businesses.

I think of some of our favourite Asian eateries. Typically their mains have gone from around $15 to $18-$19 in the past two years. Already, me and my family are pulling back in how often we go to these places. If those mains were to go to $20-$21 I reckon we would almost entirely cease going to them.

Another obvious example is construction. Many projects have quickly turned infeasible over the past 12 months. Projects are and will increasingly be cancelled. With resulting drop in demand for materials and resulting easing of inflation.

Food prices may not rise as much, the supermarkets are on notice and seem to be making an effort (a rather cynical one) of moderating price rises.

meanwhile it looks like rental inflation could be close to zero over the coming 6-12 months, as we lose population and large supply comes on line.

Yeah I think it is easy to assume it will keep compounding, but there is a good chance a lot of it is a one off or may even be reversed, particularly the big contributors; construction, oil, shipping. I really think it’s possible that the reserve bank will be battling deflation next year and rates will be back to almost 0%, but I wouldn’t call that a prediction just a possibility.

Yep and while I primarily think the RBNZ is hiking the OCR to contain inflation I also think there is an element of them restocking the ammo to address the recession and possibly low inflation / deflation that might be here in a year. I wouldn’t be surprised if the OCR was close to zero within 2 years. And close to zero also potentially means negative. But I wouldn’t be betting the house on it! I would be more confident that the OCR will be somewhere between 0.5 and 1.0 within two years.

HM it would be good if you understood that rates are already negative with inflation running at 6% that’s 4% negative in NZ in other countries it much worse.until inflation is under control people are losing purchasing power, all assets prices are falling lifting rates is only way to put value back into currency. House prices falls just take more time to show in system by end of year 30% falls will be normal this will continue until inflation is under control.

Entitled to your opinion, just as I am to mine.

I thought they were also raising to protect the currency?

Well inflation of raw materials such as steel and iron has not peaked. Another price increase at the wholesale level of between 8 - 12% (up to 30%) for August.

Also had a freight fuel adjustment factor notice of 33% from a linehaul supplier for July. April/May/June 23-25% respectively. March 18%, February 15%.

Essentially 'this time IS different'....the theory the banks (including Central) can control the leakage from asset markets in to the real economy has been shown to be time limited (interest rates can only go down for so long and initial ignorance from the wider public takes you only so far)....quite simply they have lost control of that leakage and now have to revert to proven blunt methods to reset.

And they have no choice because their privileged position as masters of the economy is under real threat.

Essentially 'this time IS different'....the theory the banks (including Central) can control the leakage from asset markets in to the real economy has been shown to be time limited (interest rates can only go down for so long and initial ignorance from the wider public takes you only so far)....quite simply they have lost control of that leakage and now have to revert to proven blunt methods to reset.

Actually, I am expecting more QE and cost of debt manipulation. I think it's almost inevitable. But I think the question is important: How long can this continue and at what point do the asset markets fail to respond?

Looking at the bigger picture, if the boomers start squealing about how the ruling elite is robbing of their lives' work, anything can happen. It might actually be playing out right now, I don't take my cues from Bernard Hickey.

Spot on comment Frank. Example of leakage from an asset market: a friend who got $200K more than expected for his house at auction went out and bought a Tesla the next day.

I think Bernard got so, understandably, whacked by his post GFC 30% property price crash prediction that he has mentally over compensated too far in the opposite direction. I think the truth will lie somewhere in between.

Agreed. He's too traumatised by the RBNZ and Gov't perpetuation of the housing bubble, in the face of all obstacles and sense, to believe that we could be in circumstances where they simply can't maintain the status quo.

Bernard got it wrong around the GFC as he was too bearish. Bernard might get it wrong this time around as well as he may be too optimistic.

There is much he has left out of this post above on factors that will put further downward pressure on property prices. Beyond those the risks are also high for further black swan events and shocks in this current environment as well given the ongoing pandemic, war and geopolitical divide.

One scenario I can think of which would be a major curveball to the NZ economy is a Chinese invasion of Taiwan. That would be a massive inflationary shock to the global economy and also impact a LOT of Kiwi exporters and importers. Lets hope that doesn't happen though but it is a risk none the less.

In a situation like that the Government and RBNZ may have their hands tied where they simply can't kick the can down the road any further.

As I have mentioned a 50% fall is very problematic, it will mean banks are likely to have stress in non residential lending as well due to the depth of the recession. We will follow the only playbook the RBNZ has, print and lend very cheap to banks to force down rates and cause zombie companies and borrowers, loose a decade or two as the principal is repaid..... we may see bank Nationalisations, and BS11 Separations.... With respect to how far properties can fall, as an investor you pull out you yield spreadsheets, with all the rules around interest not being deductable I think that their will be no serious investor bid even at 50%... the numbers are ugly indeed.

The interest deductibility rules will be removed as soon as national get elected which will be as soon as there is a recession. Interest rates will go below 0. In that scenario there isn’t much correction needed for investors, but they will need to believe it’s the bottom.

National reversing of Labours changes for property makes them an absolute no go for my vote.

Me too.

Labour's covid mandates to boot perfectly good nurses / teachers / policemen / prison guards / firefighters out of their jobs makes them unacceptable to me to vote for , circa 2023 ...

Labour's policies for rental properties were made in panic and they will regret them at leisure.

The most valuable point Bernard has been making lately is that young people need to just move to Australia and just forget about New Zealand. Life can pass you by. To quote George Carlin in reference to politicians “ They don’t care about you, they don’t care about you, THEY DON’T CARE ABOUT YOU!”.

The Labour Party just taxed the crap out of PIs, almost all of which are older people, in an effort to bring prices down for the young. They are also allowing significant density in areas usually protected for the rich. Interest rates are going up. Population is stagnant. Houses are being built at a very high rate, probably over building. Not sure what else they can do really.

They removed interest deductability, depreciation and added a 10year brightline.... its finally working they are not going to stop it now.... their policies are finally working.....

That is true. I still feel that we have a housing bubble/problem because enough New Zealanders wanted it. Interest deductibility and ring fencing is massive but it concerns me when National are so keen to unwind anything that hurts investors or property. Historically New Zealander vote for what protects property values, they don’t vote on values, so any positive changes will likely be dismantled with ease.

This time IS different. And the reason is COVID - a global pandemic; a disruption of the magnitude never before faced in our lifetimes.

We went into our first lockdown in March 2020. The stimuli started immediately and carried on - one new stimulus after the other.

At the time of the lockdown the REINZ Median House price was $665,000.

It peaked 20 months later (Nov 2021) at $920.143 - a 38% rise in 20 months.

In the prior 20 months (July 2018 to March 2020) - we experienced a 21% rise.

And in the prior prior 20 months (Nov 2016 to July 2018) - we experienced a 6% rise.

The interest.co.nz chart for Median House price only goes back to 2016, but my guess is that a 38% rise inside a 20 month period might be a precedent. It would be interesting to look back over decades, in order to determine this.

I recall prices at the bottom end took off when the Bolger National government started its state house sell off (alongside its policy of full market rentals for state house tenants) in the 1990s. This started our obsession/flurry of 'average Joe's, or 'Mom and Pops' entering the market to become part-time/speculative landlords. And then rinse repeat in 2015 - when the Key National government accelerated the sell off - bringing in more average Joe's and (hence) escalating house prices well beyond inflation.

But I just get the feeling - the 38% price rise over a 20 month period is unprecedented - and that is due to the COVID-related actions of both RBNZ and government.

And we will never go "back to normal" - this is a post-COVID world with a whole new set of challenges. The tourism market will not return; the int'l student market will not return; hospitality will not return; etc. to pre-COVID levels. Probably not for decades.

The value of the NZD against the USD benchmark/global currency will become far more important to the RBNZ and the government than local asset/house prices. They will let the housing market find its proper equilibrium based on debt/income ratio. A median multiple of 6 is likely where we will end up.

Our median household income (assume x2 FT salaries) is around $100,000 - meaning the median house price (as a minimum) will come back to $600,000.

Given our current median house price (May 2022) is $840,000 - I expect a 30% drop in house prices over the near term (to get to that 6:1 ratio). I think Gummy asked me to put a timeframe on that some months ago - and I said by Dec 2022. And I added that would be accompanied by a 50% drop in sales year-on-year.

PS - The bigger issue is whether or not rents will drop at the same pace as house prices - and I think not. Hence, to get to a truly equitable cost-of-living situation here for the non-homeowners (30% of the population) - rent controls are necessary.

Can we give the 38% back faster then 20 months.........

Perhaps! If you look at stock market crashes (big ones, such as 1987) - they are always faster on the downside.

Great comment Kate.

If the market is going to correct beyond 20% I think it will be declining beyond Dec 2022. If it’s a bigger correction, I’d guess the bottom might be this time next year and stabilisation beginning spring 2023. I imagine the steepness of the drop will ease off before then, we might have a period of stagnant prices too (which given the higher inflation, is still a loss).

Yes, I agree and think the nature of our housing market price drops will have a lot to do with whether or not our construction industry starts dropping off a cliff (or not) like AUS.

We are a bit of a nation of small business owners and many of these small businesses are in real estate-related sectors.

The hospitality sector, as we all know, fell off a cliff with COVID. AirBNB, Bookabach, etc. was a big part of that sector. How much additional debt, or personal/private capital injection, those that have survived have taken on, is anyone's guess, but I suspect its not pretty.

Stabilisation beginning spring 2023 might be extremely optimistic. I just can't foresee where the big upside in our economy would come from in order for that to happen?

there is cash flow stress in construction now, will surface shortly, dont be leaving tools on sites guys.....

I fear so.

By stabilisation I mean… nominally stable/flat prices (which would likely still be dropping in real inflation adjusted terms obvs).

Much will depends on the psychology of inflation and price expectation. People have very little memory of inflation, let alone stagflation.

Property investors endlessly repeat mantras (here and elsewhere) about how well prepared they are to buy back in to the property market if the discount is tempting enough. They all sound extremely confident that they will weather and then benefit from any storm. And that well might be true. Eventually investors do buy back in. But from my perspective, this time is different in so many ways. A really big crash in property has not occurred in the investment lifetime of most investors so the psychological impact might be unprecedented. Overconfidence can lead to a compensatory negative overreaction. Much will depend on how all this impacts lending. If the correction is painful then banks are going to be much more likely to want to lend to FHB with stable jobs and decent deposits than investors who have been leveraging up and recycling equity (equity that has reduced). That has been the pattern of other major housing market corrections. Property Investors in NZ seem to be under the impression that the banks will always lend to them.

Many industries are dependent on the housing market froth in one way or another too, as you suggest. There is a fair chance this correction will be a full on crash + recession.

Really enjoy your contributions. It is a fascinating time.

Kate said: "The value of the NZD against the USD benchmark/global currency will become far more important to the RBNZ and the government than local asset/house prices."

IF this is true, then this might be the key factor that makes it so that 'this time is different' say cf. to GFC etc.

Yes, and post-GFC, I think our housing market held up/bounced back reasonably quickly due to rampant immigration in the immediate post-GFC period;

- New Zealand immigration statistics for 2015 was 1,039,736.00, a 9.74% increase from 2010.

- New Zealand immigration statistics for 2010 was 947,443.00, a 12.8% increase from 2005.

- New Zealand immigration statistics for 2005 was 839,952.00, a 23.74% increase from 2000.

- New Zealand immigration statistics for 2000 was 678,813.00, a 15.32% increase from 1995

And just following the GFC, we ramped up student visas as well. We had a drop off from China during the GFC and the Key government moved to relax scrutiny (i.e., many entered with dubious language skills tests) and allow for student visa holders to work while studying. That period saw the big growth (a near doubling) of int'l students from India which more than made up the losses from China.

We had a very healthy trade balance and incoming investment from China after the GFC too. China has comparatively impressive growth then which also helped to shield both the economy and the housing market (which might be more correctly described as a housing market with other markets/industries attached).

There are a couple of ways of interpreting the data and restoring balance.

One is to remove waste in the system, which there is plenty of, eg land policies that allow land bankers to increase the raw land value by over 20x and make these super profits for adding no amenity value. Another is removing the monopoly that councils have to provide consenting and infrastructure etc.

This would reduce prices so, without incomes increasing, the median multiple will improve.

Another way is to have inflation increase wages faster than the cost of housing increases so the median multiple improves. However this hardly ever works because wages are not increasing faster enough relative to almost any cost increase measure, especially housing costs because they have, due to Govt. policy, become decoupled from the general inflationary increases and are increasing at a rate many multiples greater than the general inflation.

For the second option to work, the first option has to work, so rather than the house price falling and taking all the hit, it can be met with the right type of wage inflation meeting it halfway, so the median multiple is restored.

As soon median income multiple went beyond 5x median income, it was a red flag for dysfunctional housing policy, and policies should have been put in place to prevent any increase. But every measure they have put in place has made the situation worse.

I'm picking the majority of any correction will be by housing prices falling, and the numbers show that we are approx. 50% too high. And all the Govt. response will be is to limit the amount of this fall. BUT that assumes they have control and that they know what is the right course of action to take.

I don't think they have any more control and ability to make the right decisions on the way up or down.

Dale, I suspect you will know this, how does infrastructure costs work in somewhere like Houston? Let’s say I build 10,000 houses in the middle of nowhere, and for those people to get to work they need to add a 27th lane to the Katy freeway, who pays for that?

He knows, he just ignores it

It's a bit more nuanced than you describe.

Because as soon as you build in the middle of nowhere as you say, then it is also the middle of somewhere, ie many of these developments are being built in response to local employment opportunities. Ie they become their own destination. Plus many people that do move to these places, ie regional are doing so because they can work from home. IE it's not a given that any extra highway is needed.

Here is a good Texas example, now 100,000 people plus https://en.wikipedia.org/wiki/The_Woodlands,_Texas

But given that some contribution might be needed, if you have only paid say 4x median income for your house, you have plenty left over to pay for any amenity that you need or cause to be needed, which of course is in the form of taxes. It's a far fairer user-pays system. And at the end of the day, leaves more discretionary income for you to spend as you chose, not some bureaucrat somewhere.

What you don't get, like in NZ, is paying twice as much for your housing and all that extra cost mainly goes direct to land bankers, who don't have to pay for anything.

What your saying makes no sense whatsoever

"you have plenty left over to pay for any amenity that you need or cause to be needed, which of course is in the form of taxes. It's a far fairer user-pays system."

Who is paying for this amenity and how?

If you have the right land-use policies, this allows developers to buy the land closer to its next best economic use-value. On the edge of a city, this is mainly the rural value.

So eg, the developer would pay approx $50,000 per ha not $2,000,000 ha when the land has monopoly restrictions like they do at present.

This would give $1,500,000 per ha that did not go to land bankers and is thus available to help pay for infrastructure costs and/or the developer can add extras into the development to give their project more market appeal, eg lower prices, bigger parks, etc. Councils can then levy the developer direct, just like they do now. In our present system, they should be taxing the land bankers direct on this, ie a value capture tax, but they don't. They let the land banker make superprofits without adding any amenity value, AND then wants to charge the developer and ultimately the end-user with the infrastructure costs when the money was there all along, but they allowed the land bankers to take it unearnt.

I think the best system is to free up the system so there is no value capture needed by the council because otherwise, we have just passed the gain from the monopoly land banker to the monopoly council who are not that efficient or quick in responding to the market and plus are their own restriction in the system.

This is exactly how it happens in jurisdictions that have less restrictive land-use policies.

And the reason the land can be bought at closer to its rural value in this example is that when you have fewer land restrictions that allow to build up and out, and at any moment in time, there is always many times more potential land available for immediate development so the supply is always more than demand. IE land bankers cannot buy and thus capture a monopoly on land. And since they can't, they don't even try to because there is no speculative rentier gain to be had.

Gst on 10k houses?

As someone who owns 16H close to motorways etc etc, I love your thinking......

Apart from the pertinent points in the article there are a few more worth noting:

a) Direct house prices were removed from the CPI. This is absurd as it is the largest consumer good. The OCR would have never fallen so far had they stayed in.

b) The reserve bank is directly responsible for the blowoff market peak as it let the OCR fall so low (asset values are proportional to 1/interest rate) and mortgage rates bottom at between 2 & 3%

c) Recourse mortgages make it a one way bet for banks and skew investment towards housing rather than business. They should be banned.

point c - try getting a business loan without property security..... this will be huge for hospo and small business who after covid are negitive equity...... non recourse house loans will cost more as well, risk is always paid by the borrower....

I think all assets will have to be weighed up against against term deposits at 7-10%.

This will see peoples kiwi saver balances halve and house prices fall by 65%.

The fallout from all of this is going to get ugly.

Many will lose their homes & their shirts.

But for many life will go on.

Credit will be very difficult to get for speculative investments in a few years.

Residential property investors are going to learn about snakes and ladders, and that houses don’t always double every ten years.

For those who can't be bothered reading the article, here's a summary of Hickey's key arguments as to why house prices won't crash:

- Because some people made incorrect predictions about it happening in the past

- Because the consequences of it happening are too dire to bear thinking about

- Because unlike previous property bubbles, this government has magical powers to prevent it from happening

... beautifully summarized , Mr chebbo ...

House prices cannot fall much in NZ , unlike how it does in other countries because we are special ... annointed by the gods of real estate ( G.o.r.e ) nothing bad ever happens here ..... it's like a cosmic teflon coating which causes price crashes to slide off us , they can't stick ...

To me the cornerstone of house price gains remain the clamps on supply. Mainly that has been local councils via district plans limiting rezoning of land and densification.