Historic investment booms that ended with "reversals" causing "economy-wide recessions," offer "instructive parallels" to the current artificial intelligence (AI) boom, the Bank for International Settlements (BIS) says.

AI is a key topic covered in the BIS annual economic report, released over the weekend. The Switzerland-based BIS is the central banks' bank. Its shareholders include the Reserve Bank of New Zealand with a 0.6% stake.

"Historical episodes of investment booms offer instructive parallels. The canal mania of the 1830s, the British railway mania in the 1840s, the electrification exuberance of the late 1920s (roaring 20s) and the dotcom boom of the late 90s all shared one common trait: a genuine technological breakthrough that attracted capital in excess of what commercial returns could ultimately justify," BIS says.

"These episodes ended with an eventual reversal in investment, inducing economy-wide recessions. The scale and pace of the current AI investment boom accompanied by expectations of large productivity payoffs bear resemblance to these precedents, highlighting potential downside risks in the near term."

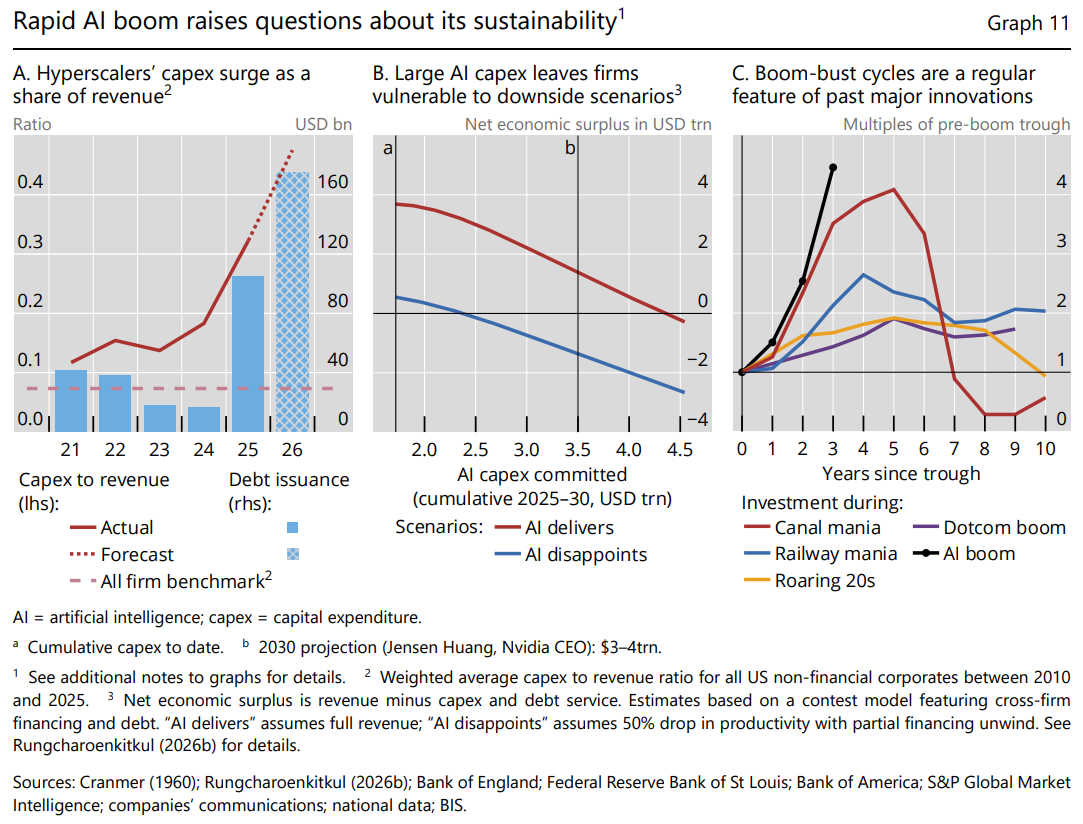

BIS questions the sustainability of the current economic expansion, noting the five largest hyperscalers - big cloud computer service providers who own and operate data centres - are expected to spend more than US$1 trillion on AI-related capital expenditure during 2025 and 2026.

"These commitments are outpacing earnings and the free cash flow of these firms, leading some to issue debt to raise additional financing. This investment race may be partly driven by the perception that only a small number of players with superior technology will ultimately dominate the market shares. The intense competition raises the risk of firms over-committing resources to investment projects with still uncertain returns, leaving all firms vulnerable to disappointments in AI payoffs."

"Model analysis based on such contest motives highlights the downside risk of current AI exuberance. As competitive pressure drives capex [capital expenditure] higher, the net economic surplus – the total payoff less investment costs – declines for the sector as a whole and could turn negative in adverse scenarios. Disappointment in returns could trigger a sudden pullback in financing and turn the capex boom into a protracted investment bust, with potential knock-on effects on financial conditions," BIS says.

Another risk BIS highlights is the AI boom running into what it describes as a supply side roadblock. AI data centres require lots of electricity to power their servers, and lots of water for cooling.

"The AI buildout has recently been facing growing bottlenecks in electricity, advanced semiconductors and grid equipment. Fast-growing demand for computing power is already pressuring electricity prices and input costs, with potential spillovers to inflation. Looking ahead, these temporary shortages may also amplify overinvestment, as firms attempt to lock in future capacity through long-dated contracts that further expose them to any disappointments in demand," BIS says.

AI could 'augment the production of knowledge itself'

BIS does, however, say AI has the potential to "differ fundamentally" from earlier technological progress.

"Previous general purpose technologies, such as the steam engine, electrification and information technology, raised workers’ productivity by providing them with better tools. AI could go further by augmenting the production of knowledge itself."

"If, at some point, AI systems can improve their own capabilities and 'create' technology and ideas, the macroeconomic consequences could be profoundly different from past innovations. A key constraint on long-run growth, namely the rate at which humans can generate new ideas, could be lifted," BIS says.

It cites recent research making the case that if AI capital becomes a sufficiently close substitute for human labour, the economy could; "transition from the regime of constant exponential growth to one of accelerating super-exponential growth."

"As machines autonomously improve themselves, the economy acquires a self-reinforcing engine of growth."

Erosion of the consumer base?

But BIS also notes supply side oriented frameworks focus on the productive potential of AI, assuming consumer demand keeps pace with supply.

"But as AI advances, automation increasingly diverts income from labour, which is spent on goods and services, into further AI investment. The consumer base could erode as productive capacity expands. Forward-looking firms, recognising the shrinking future market for AI-produced goods and services, may find it unprofitable to invest in innovating and automating the next task. Productivity stalls not because of technological limitation, but because the demand to justify further capacity expansion is missing. The demand bottleneck becomes the binding constraint," BIS says.

Thus there are significant risks in a transition to a more productive AI-driven economy.

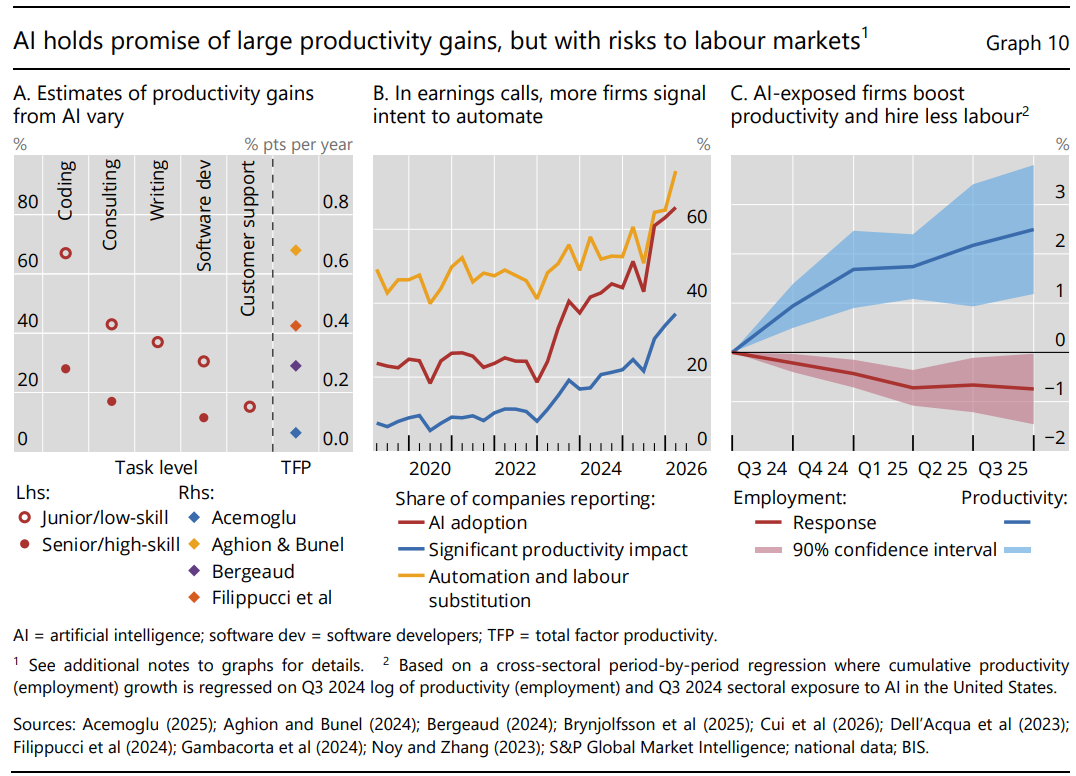

"As more capable AI tools find applications in more tasks and occupations, labour displacement could intensify. Whether or not AI advances create new jobs, or expand demand for existing ones, sufficiently to make up for such displacements remains uncertain," BIS says.

"Unlike past general purpose technologies, AI competes directly with human cognitive abilities, possibly narrowing the scope for workers to move up the value chain or find new non-disrupted tasks. To date, such disruptive labour displacements have yet to occur at scale."

"But there are signs of possible adjustments to come. In earnings calls, more firms are acknowledging potential productivity gains from AI, signalling their intent to automate an increasing share of production processes and engage in labour substitution. Consistent with this, US sectors with higher exposure to AI have also seen higher productivity gains, partly at the expense of lower employment growth relative to other sectors."

Graphs 10 and 11 in this article come from the BIS annual economic report.

*This article was first published in our email for paying subscribers early on Monday morning. See here for more details and how to subscribe.

5 Comments

Bitcoin miners are repurposing their infrastructure into AI and high‑performance computing data centers because AI workloads generate much higher and more stable revenue per megawatt than Bitcoin hashing, especially post‑2024 halving and amid rising energy and capital costs

Core Scientific, Hut 8, TeraWulf, Cipher, IREN have been reducing hash rate exposure and signing multi‑year AI/HPC hosting and compute contracts, often in the multi‑billion‑dollar range. Facilities originally designed for ASICs are being upgraded with GPU clusters and general‑purpose servers, turning “mining farms” into cloud‑style compute campuses for hyperscalers and AI startups.

Disclaimer: I only own IREN and consider myself early in to the play. Selling ratty / crypto crap and going all in IREN would have been life changing. Most of the crypto degens never took this path.

The AI monster that's been created is an adjacent issue.

AI boom is ok.......

Its different this time....

It might be the bubble we need to have to take us in to the depression we surely deserve.

The debt either has to be paid back or written off, there will be no debt Jubalee.

The coming El Nino is going to cause international food inflation.

The big cloud providers are already swamped by current AI demand, it will only increase from here. Many businesses are only scratching the surface in terms of integrating AI into the processes and software. And there are plenty more use cases we haven't thought of yet (maybe AI will think of them for us). I'm not convinced there will be an AI crash other than some businesses that have become overvalued based on potential income.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.