By David Chaston

In the past few days equity markets have tumbled worldwide. A major correction is underway in both the bond and stock markets.

Reading the headlines will make anyone nervous about what is ahead for investors. If you are a KiwiSaver you may well be wondering what to do, too.

As a direct response to the uncertainty, the answer is 'nothing'. Sit tight.

We may well be facing something akin to the Global Financial Crisis - or we may not be.

For a KiwiSaver, it actually shouldn't matter. You certainly should not rush out and change your investment strategy to try and avoid what you might think is an impending downturn.

Three things are important.

1. Firstly remember KiwiSaver is a long term savings program.

As Retirement Commissioner Diane Maxwell says, "KiwiSaver is a long game that will have bumpy patches, but will pay off in the end and make a huge difference to your retirement.” Try not to look at your balances too often - about once a year is enough (and ignore them on your banking app - that sort of visibility can set you into a short-term trader mindset and that is completely wrong for this type of investing).

2. Secondly, understand that it is a regular contribution system. While yesterday's investments may decline in value temporarily, you are also getting a powerful advantage because today's contributions are buying into your investment plan with an enhanced impact (your contributions buy more).

3. And thirdly, remember, we have been through this before. The next financial crisis won't be exactly like the last one. However it plays out we will emerge on the other side just fine and the transition will be relatively quick (a few years at most) and far shorter than your investment horizon.

The most important thing you can do is recommit to a long-term retirement savings strategy. You are hopefully invested in a type of KiwiSaver program for a good long-term reason. Impending volatility isn't a good reason to change that.

But this is not to say you should stay with an under-performing scheme. That is the power of our unique regular savings analysis approach. You can use it to compare how each fund performed (their track record) over the past ten years. And you can use this relative performance data to shift to a manager that has shown better achievements for their members within the equivalent investment strategy. That is, don't change strategy for your long term saving, even if you shift to a better performing fund.

We are now into the second decade of KiwiSaver and members now have more than $50 bln invested. Your regular monthly savings contributions will keep your balances growing. Now you need to realise that the value of what your fund manager can add will become increasingly important. Up to now, the bulk of your holdings are contributions - from you, and matching amounts from your employer, and for a while, the Government. But increasingly from now, the health and speed of growth in your nest-egg will rely on fund manager performance. Choose wisely.

There are two aspects to the choice: the risk profile you want to take, and the manager/fund you will use within that risk profile.

Unless you are close to retirement, you should not stay in a default fund. Adopt as much risk as you can tolerate because in the long run that will give you the best returns. Think of 'risk' as a tolerance for volatility; don't equate it with 'greed' because it isn't anything to do with that. Low risk is not wise because you will struggle to do much better than holding the funds in a bank - and to be frank, that is not really investing, nor will it help provide for a very long retirement. What you need to be seeking is the extra that comes from not being passive. This is the part that will be valuable in retirement.

Finally, try and ignore the 'fees' issue. We have the tools to look past that aspect. It is obvious that what you need is the after-all-taxes, after-all-fees returns. And this is exactly what we are measuring below.

Fund managers have had a good year to September and their overall performance has improved over the year to June. And that applies equally to default KiwiSaver schemes.

As we have noted before, the evidence is that many cash, conservative, or moderate funds actually don't deliver after-all-taxes, after-all-fees returns better than default funds. There are exceptions, but interestingly, very few. And that is why you need to do some 'work' to figure out where and why you would move your investment. Also remember that track record isn't everything. You would be best to move to a fund that has better future prospects rather than just a good historic track record.

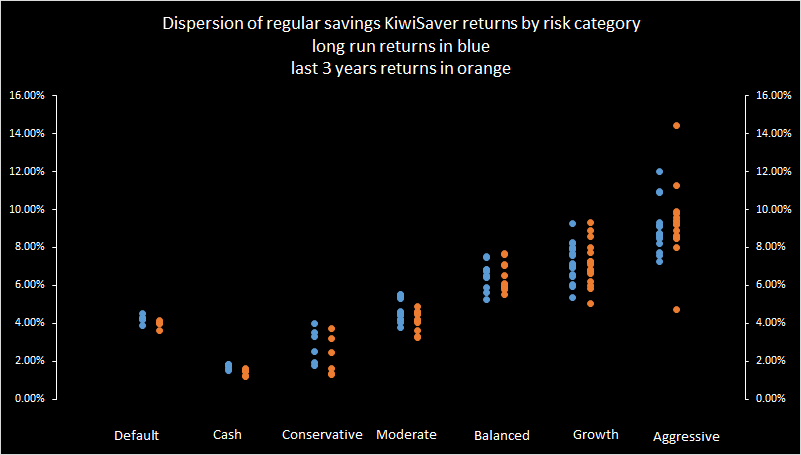

How far out the risk curve is visually suggested in this updated chart.

Return range of all funds, as at September 2018

Here are the updated results for default funds.

| Default Funds |

Cumulative $

contributions

(EE, ER, Govt)

|

+ Cum net gains

after all tax, fees

|

Effective

cum return

|

= Ending value

in your account

|

Effective

last 3 yr

return % p.a.

|

|||

| since April 2008 | X | Y | Z | |||||

| to September 2018 |

$

|

% p.a.

|

$

|

|||||

|

|

|

|

|

|

||||

| Mercer Conservative | C | C | C | 33,253 | 8,613 | 4.5 | 41,866 | 4.1 |

| ANZ Default Conservative | C | C | C | 33,253 | 8,163 | 4.3 | 41,416 | 3.6 |

| ASB Conservative | C | C | C | 33,253 | 7,953 | 4.2 | 41,205 | 4.0 |

| FisherFunds2CashEnhanced | C | D | C | 33,253 | 7,932 | 4.2 | 41,185 | 4.1 |

| AMP Default | C | C | C | 33,253 | 7,239 | 3.9 | 40,492 | 4.0 |

| Funds with a later start date ... | ||||||||

| BNZ Conservative | C | C | C | 20,695 | 2,598 | 4.1 | 23,292 | 4.2 |

| Kiwi Wealth Default | C | C | C | 15,951 | 1,414 | 3.9 | 17,365 | 4.1 |

| Booster Default Saver | C | C | C | 15,951 | 1,310 | 3.7 | 17,262 | 3.8 |

| Westpac Defensive | C | C | C | 15,951 | 1,290 | 3.6 | 17,241 | 3.7 |

| --------------- | ||||||||

| Column X is interest.co.nz definition, column Y is Sorted's definition, column Z is Morningstar's definition | ||||||||

| C = Conservative, D = Defensive | ||||||||

If you are not about to retire in the next few years, you should seriously review why you are in a default fund. We will review the track record performance of other classes of KiwiSaver funds over the next week or so, but being in KiwiSaver is a long term commitment and you should be applying long-term strategies to this investment.

That may well mean accepting some higher level of risk to gain a higher level of returns. Over a long-term, that is usually a sensible strategy. Sure, bumps in the road do come around (like the Global Financial Crisis) and they can knock growth fund returns. But as we have seen post-GFC, the bounce-back can turbo charge your results.

Here is where these managers have your default funds invested.

| Allocation, approx. | Mercer | ANZ | ASB | FF2 | AMP | BNZ | Kiwi Wealth |

Westpac | Booster |

| % | % | % | % | % | % | % | % | % | |

| Cash | 34.6 | 22.1 | 23.7 | 21.1 | 46.9 | 38.4 | 38.9 | 34.4 | 27.7 |

| NZ fixed income | 14.9 | 17.6 | 32.6 | 38.3 | 16.5 | 10.1 | 17.6 | 22.9 | 27.9 |

| Intl fixed income | 29.3 | 39.9 | 23.8 | 22.9 | 16.3 | 31.5 | 23.6 | 23.3 | 23.9 |

| NZ/Aust equities | 3.7 | 5.2 | 10.1 | 5.1 | 7.2 | 6.0 | 0.5 | 7.6 | 5.6 |

| Intl equities | 13.8 | 12.0 | 9.8 | 7.5 | 13.1 | 14.0 | 19.4 | 8.5 | 13.9 |

| Listed Property | 0.4 | 3.2 | 3.3 | 1.0 | |||||

| Unlisted Property | 1.3 | 5.1 | |||||||

| Other | 2.1 | ||||||||

| ---- | ---- | ---- | ---- | ---- | ---- | ----- | ----- | ---- | |

| 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 |

If you want your money allocated differently, you will need to change funds, either with the same manager, or with another. But before you do that, get some proper investment advice from someone who understands your investment goals and tolerance for risk. That involves work on your part. But it's not a good excuse to just leave it there because it seems too much effort.

KiwiSaver default funds are only part of a broader range of conservative funds available. Many of the 'traditional' conservative and cash funds are under performing the default funds. We will look at the rest of the conservative funds in another article.

For explanations about how we calculate our 'regular savings returns' and how we classify funds, see here and here.

There are wide variances in returns since April 2008, and even in the past three years, and these should cause investors to review their KiwiSaver accounts especially if their funds are in the bottom third of the table.

The right fund type for you will depend on your tolerance for risk and importantly on your life stage.

You should move only with the appropriate advice, and for a substantive reason.

30 Comments

A great pep talk for the troops David. Readers will recall that we had a similar situation at the beginning of the year and if you had transferred your funds to cash then you would have missed out on the gains that came later.

It's hard not to look at your balance when it is part of your banking app. I generally don't consider KiwiSaver to be part of my savings and will just round it down to the nearest 10K in my mind. Reviewing all your assets once a year is a good idea. Maybe commit to not changing KiwiSaver more than once in a year.

I'm certainly glad I took up KiwiSaver yet did it a few years after it started. I had heavy mortgage commitments at the time but that was no excuse.

Not sure if I completely agree with the strong faith in the long term health of the markets.

However, for those of us who have retired early, it may be worth considering putting in your $1040 topup well before the end of the financial year if there is a big dip over the next few days/ weeks.

Very good article. Short term volatility means nothing in the long run. Where there is risk there is opportunity, so I’ll be leaving my KiwiSaver in an aggressive managed fund no matter how bad the next financial crisis is.

But surely if you could predict a crash it would make sense to sell up, wait for the crash and then buy in again. So the question is can you predict a crash? I would say yes to some extent.

It is exceedingly difficult to accurately time a crash and recovery. Even the CEO of the NZ Super Fund acknowledges this - http://www.youtube.com/watch?v=h1SdW8KmJrk&t=7m59s

You have to take a long term view. Someone that invests in an aggressive fund and leaves it there untouched for 40 years will almost certainly come out the other end better off than someone that chops and changes, attempting to time the market. I’ll stay the course and leave it to my fund manager to adjust their ratios as they see fit - perhaps a bit more liquidity when trouble looks to be on the near term horizon. My KiwiSaver is 73k today, and I won’t bat en eyelid if it is 33k tomorrow. Yes, aggressive funds will take more of a short term hit in the event of a global financial crisis, but it is the long term outcome that counts.

Most of the people that happen to accurately predict a crash are people that are constantly saying that a crash is just around the corner for years on end. And when one finally comes along they say “I told you so”. But the reality is that even a blind squirrel will find a nut every now and again, and even a broken clock is right twice a day.

Ironic. An article basically stating "shares always go up" and no one jumping up and down.

Literally the very first sentence of this article is “In the past few days equity markets have tumbled worldwide.”

Yes, but the underlying message is stay in shares i.e. they will recover and continue to increase.

I am merely pointing out the hypocrisy of many of the posters on this site.

Started in a Cash Fund, and staying in a Cash Fund.

I prefer to place the risk in other vehicles for more growth-oriented investment.

If you’re not comfortable with the volatility of investments that are linked with the share market, then good, old-fashioned property (land & buildings) may be a better choice.

For most people, a bit of both and some money in the bank is probably reasonable.

TTP

I don't see the pull in property (as an investment, not a home).

High maintenance, bad yields, just as susceptible to a crash as the market is, and very hard to enter into at a lower price point.

I think so many people in NZ gravitate towards it because they're financially illiterate.

'Don't panic Captain Mannwaring.' Is the usual call from those that are heading to the hills themselves , leaving others to drown in the Tsunami. When the tide goes out they waltz back down to the beach and pick the pockets of the drowned.

You can see that the rats have already left the property ship, John Key, Mike Hosking, Double GZZ. Stocks are no different, if you believe their is a crash ahead, you reduce your risky holdings and get some of your fund into cash, then you can buy stocks at 'value' when the distressed sellers appear.

Those that do the best, invest, but they don't hold all their chips in stocks when the market turns. Buffett and Munger are sitting on piles of cash at present, why? because there are times when there is no 'value' to make drip feeding worth while, so it's better to pile your cash for big 'value' purchase in a downturn.

er, no. Bershire Hathaway has only 8% of its assets in cash at the moment. It is slightly elevated, but certainly not by much.

But have made no significant purchases recently.. They're just letting the cash build up.

And tend not to buy the 'fads' that most fund managers purchase into.

It strikes me that certain people here may be trying to talk down markets only because they have personal agendas to fulfill - such as being able to buy in at lower prices.......

TTP

Just trying to educate that things don't always go up and sometimes holding is a mistake. Best move I ever made was being out of property at the end of 2007 and having cash for the stock market in 2008. Where the stock market goes the property market will follow. The recovery in stocks is usually a lot faster than the recovery in property though.

Worth reading Kindleberger's Manias, Panics and Crashes. Timely reading under current conditions. Re-visiting this book after 10 years ...

Thanks CN - will take a look.

If you look at Schiller's graphs of real US S&P 500 ex Irrational Exuberance over the long term - the market did not recover from it's 1970's peak for about 20 years.

Interesting as I don't think Kiwisaver investors who have had an indian summer of ever increasing stock prices since investing from 2009 onwards - including our superfund that think they can walk on water - has ever seen a long slow recovery lasting many years.

Given the extremely high valuations today - way in excess of 1970 levels - this could be what awaits us.

A great opportunity to purchase an interest in public companies at lower prices.

Because they have personal agendas to fulfill? Sounds a bit like the pot calling the kettle black, TTP.

Remember that Berkshire Hathaway is in the insurance business and owns operating subsidiaries. It is very different to an investment fund holding minority stakes in listed securities.

To look at the percentage of assets in cash as an indication of its investment positioning and view of listed markets as one would look at an investment fund wholly invested in listed securities would lead to a misleading conclusion.

Buffett has stated that Berkshire would maintain a minimum of US$20bn for liquidity purposes to be available for insurance payouts.

1) 15% of total assets are in cash (Treasury Bills are counted here as they can be easily sold at or near face value, whilst cash at the utilities and finance businesses are excluded as they are assumed to be for their own working capital needs) - excluding the US$20bn for insurance payouts, then this leaves 11.7% (US$83bn) of total assets which can be invested in either minority stakes of listed companies, control stakes of unlisted companies, other investment opportunities (such as the preference shares with attached warrants on Goldman Sachs, loans to Harley Davidson, financing for Mars to purchase Wrigley, LBO financing for Kraft Heinz, etc)

2) 24% in minority stakes in listed securities

3) 61% are in assets of wholly owned / controlled subsidiaries which are operating businesses. There is no way that these assets are going to get sold and the proceeds reallocated to other investment opportunities.

Buffet does have a history of using cash equivalent fiscal products in lieu of actual cash to avoid the taxation associated with the “profit” from the “sale”

Everyone should sell up now and invest in NZ petrol companies. I've heard, on good authority, that they are fleecing it.

My recollection is that Kiwisaver funds have available as a mandate the ability to short shares use leverage and other tools and fx to enhance returns on short positions. I personally do not have a Kiwisaver account, but similarly I do buy and short shares, use leverage and other . The notion that someone should not review their account more than once a year is worrying and frankly negligent financial advice, similarly the notion that one should hold onto positions / assets/ Kiwisaver funds all the way to the bottom is herd mentality/ group speak, and somewhat nonsensical if Kiwisaver itself can take short positions . Yes Warren Buffet is an exceptional investor across multiple asset classes but to use his name as reason to hold positions , because its " for the long term ', is nonsensical. I hold multiple short positions ,including all four Australian banks, and have done so for more than a year . I simply saw a sound investing opportunity , no doom or gloom..

Cowpat - If one follows Buffett's advice with his favourite holding period as forever - one need not review other than in the very long term. So there is nothing nonsensical about not reviewing at all.

The trick is to do the very extensive reviewing prior to purchasing good companies at fair prices and then go to sleep.

As Buffett states - he's tried the opposite !

As a reminder, over 99% of Warren Buffett's wealth is in the shares of only one company that he manages - Berkshire Hathaway. He has donated shares in Berkshire Hathaway for philanthropy, and not sold any shares in Berkshire Hathaway for his own personal needs.

Warren Buffett, as Chief Investment Officer has sold shares in the investment portfolio owned by Berkshire Hathaway. For example, Berkshire Hathaway has sold shares in Wells Fargo, and IBM in recent years.

For non professional investors in the stock market, Warren Buffett recommends using low cost index funds. Here is the relevant excerpt from one of his annual letters.

Most investors, of course, have not made the study of business prospects a priority in their lives. If wise, they will conclude that they do not know enough about specific businesses to predict their future earning power.

I have good news for these non-professionals: The typical investor doesn’t need this skill. In aggregate, American business has done wonderfully over time and will continue to do so (though, most assuredly, in unpredictable fits and starts). In the 20th Century, the Dow Jones Industrials index advanced from 66 to 11,497, paying a rising stream of dividends to boot. The 21st Century will witness further gains, almost certain to be substantial. The goal of the non-professional should not be to pick winners – neither he nor his “helpers” can do that – but should rather be to own a cross-section of businesses that in aggregate are bound to do well. A low-cost S&P 500 index fund will achieve this goal.

That’s the “what” of investing for the non-professional. The “when” is also important. The main danger is that the timid or beginning investor will enter the market at a time of extreme exuberance and then become disillusioned when paper losses occur. (Remember the late Barton Biggs’ observation: “A bull market is like sex. It feels best just before it ends.”) The antidote to that kind of mistiming is for an investor to accumulate shares over a long period and never to sell when the news is bad and stocks are well off their highs. Following those rules, the “know-nothing” investor who both diversifies and keeps his costs minimal is virtually certain to get satisfactory results. Indeed, the unsophisticated investor who is realistic about his shortcomings is likely to obtain better long-term results than the knowledgeable professional who is blind to even a single weakness.

If “investors” frenetically bought and sold farmland to each other, neither the yields nor prices of their crops would be increased. The only consequence of such behavior would be decreases in the overall earnings realized by the farm-owning population because of the substantial costs it would incur as it sought advice andswitched properties.

Nevertheless, both individuals and institutions will constantly be urged to be active by those who profit from giving advice or effecting transactions. The resulting frictional costs can be huge and, for investors in aggregate, devoid of benefit. So ignore the chatter, keep your costs minimal, and invest in stocks as you would in a farm.

My money, I should add, is where my mouth is: What I advise here is essentially identical to certain instructions I’ve laid out in my will. One bequest provides that cash will be delivered to a trustee for my wife’s benefit. (I have to use cash for individual bequests, because all of my Berkshire shares will be fully distributed to certain philanthropic organizations over the ten years following the closing of my estate.) My advice to the trustee could not be more simple: Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund. (I suggest Vanguard’s.) I believe the trust’s long-term results from this policy will be superior to those attained by most investors – whether pension funds, institutions or individuals – who employ high-fee managers."

The S&P500 is a diversified equity index for the US.

Some non US investors will extend this approach and apply this approach to their own country and buy passive equity index funds for their own country. (E.g NZ, Australia, UK, etc) which may not be as diversified.

For these investors, it is worthwhile understanding what the index constituents are, particularly those companies with the highest weighting(s) in the index. Some country equity indicies have heavy weightings on some large individual companies, or certain industries and thus the investment returns are highly dependent upon the underlying performance of these businesses.

If one investor had applied this approach in Iceland, it would have resulted in a significant loss of their financial security. Why? The local stock market index for Iceland was heavily weighted towards the shares of the three local banks. The shares of these banks subsequently became worthless.

The stock index is 75% below its highs.

Repeated for emphasis due to its importance and current stock market valuation levels ...

"The main danger is that the timid or beginning investor will enter the market at a time of extreme exuberance and then become disillusioned when paper losses occur. (Remember the late Barton Biggs’ observation: “A bull market is like sex. It feels best just before it ends.”) The antidote to that kind of mistiming is for an investor to accumulate shares over a long period and never to sell when the news is bad and stocks are well off their highs"

Investing on your behalf.....How kind....How uplifting....how...utterly ...bewildering.

https://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=12143860

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.