The message is clear: interest rates are going lower and will stay down.

RBNZ Governor Adrian Orr said this at the Monetary Policy Statement briefing. The central bank will do what is necessary to push wholesale rates down further. They see this as necessary to encourage businesses to invest and consumers to spend.

For term deposit savers, that probably means after-tax returns - and returns in general - are about to vanish.

So before banks activate the signal, now is an appropriate time to review where they have fallen to after the broad decline in the past six months.

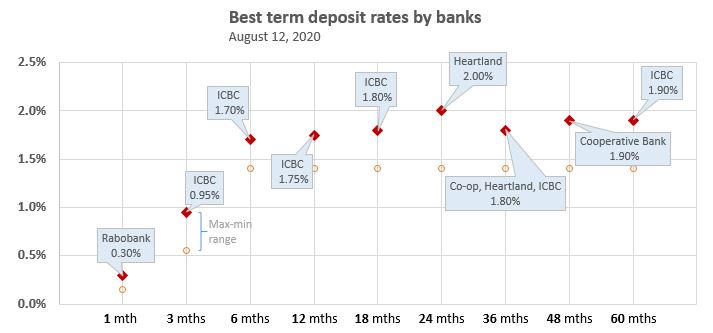

Retail rate offers from banks aren't linked by formula to wholesale rates, but the relationship has been close all the same.

Banks must price their offers to attract sufficient funding from customers to meet their funding obligations to the regulator. But the five large banks dominate the rate setting landscape.

These five large banks can source funds from wholesale markets as well as retail markets, giving them more duration flexibility - and access to even cheaper funding sources.

The locally-owned minnow banks don't have that flexibility and rely almost entirely on depositor funds.

This is why the big banks can maintain margins and offer historically low rates to borrowers - especially house borrowers.

The local minnows have to match or stay close to these low loan rate offers just to make enough loans to survive - but don't have the option to bid up the rates they pay depositors without killing their margins.

As the chart above clearly shows, there are no main banks offering 'premium' rates for any term. This is constraining the ability of local banks to make any market share gains.

Lending is the life-blood of any bank, and the new lockdown in Auckland will stifle any resurgent growth in the mortgage market. Without lending, the need for deposit funds diminishes, and the rates banks are prepared to pay sags.

Expect term deposit rates here to fall to Australian levels, which are currently:

| 12-Aug-20 | 6 mths | 12 mths | 18 mths |

| pa | pa | pa | |

| ANZ | 0.65% | 0.75% | 0.75% |

| CBA | 0.50% | 0.70% | 0.80% |

| NAB | 0.65% | 0.85% | 0.85% |

| Suncorp | 0.80% | 0.80% | 0.85% |

| Westpac | 0.75% | 0.80% | 0.85% |

These levels are about half what is on offer in New Zealand today.

The Australian offers come with deposit insurance and that feature is costly to banks and helps drive rates down. But even without that, Australian deposit rates are much lower than New Zealand rates. But it is worth keeping an eye on Australian rates as they signal where ours can go given we have similar regulatory settings and central bank objectives during the pandemic.

The odd thing is, low rates don't discourage consumer saving. If anything, they encourage it. Maybe it is just the times, but household deposits are rising at the rate of +7.9% per year. Bank lending is up only +6.0% in a year.

But fewer people are bothering with term deposits themselves (-2.1% shrinkage in a year), just leaving their funds in transaction accounts (up +32% and that is not a typo) or very low-returning savings accounts (up +15%). That customer reaction of course enhances bank margins if they don't have to pay anything for customer money.

There is a good chance household deposit levels will grow faster in the immediate term while bank lending struggles to find any growth. It is an environment where there is no chance of "a decent return".

26 Comments

Perhaps time to switch the TD to a managed fund... at the rate the reserve bank is going, I can't see bank's needing my deposit and thus giving any real returns any time soon.

I'm not worried about yields at the moment, i'm just focused on preservation. I don't like the smell of any of this volatility.

Oh, totally! Which is why I can't understand why we're being encouraged to borrow even more.

to create jobs and buy some time...

everything is now on the tab - there is no actual growth and no more road for capitalism (return on capital is effectively dead without faked growth)

without more borrowing, consumption falters and jobs disappear

I reckon lower interest rates will further heat up the housing market...... It might not be by much (because of bank lending constraints etc) but, on balance, the housing market seems destined to become even more buoyant.

The rationale for many people will be, simply, that TD interest rates are completely unacceptable - but neither will they accept the risk inherent with equities and (share-linked) managed funds.

The housing market is set to roll on - with even more upside in housing prices.

Sorry to those (including me) who don't like this outlook. But it's the most realistic prediction that I can offer at this point in time.

A caveat is that if COVID-19 turns really nasty (which it could) things could become really negative in pretty well all consumer and investment markets. In my mind, the best investment that individuals - and the nation as a whole - can make are measures to control/combat/eliminate the virus.

TTP

True but still painful to watch as your wealth deteriorates with inflation.

1.9% over five years isnt actually that bad. NZGs are what under 50bps. That's a 140bp credit spread on a AA rated credit (with a semi implicit govt gtee).

In 2018 the difference between 4 yr bank td rates and kiwi bonds was about 1.6%. Now it is about 1.15%.

NB. Kiwibonds have compounding interest quarterly so they are not bad from that point of view.

So the gap closes. And will almost certainly close further.

No wonder bitcoin and PMs are going nuts. Retirement dreams of many are going to dissipate over the next decade.

Adrian Orr knows that at Zero or close-to zero interest rates, people will not go out to borrow and spend .

There is much empirical evidence of this , which seems counter-intuitive to us , but we know that reduced interest rates in times of uncertainty lead to "hoarding" of cash that is not immediately needed.

Alternatively , people use the breathing space to pay down or retire debt .

Its further compounded with prices falling , commodities ( other than Gold and Silver ) are at cyclical or historic lows , the minerals boom that Aussies benefitted from is over , gone.

The lower prices of inputs leads to the PPI ( Producer Price Index) falling .

We see this in the lower diesel price at the pump .

An negative PPI will lead to deflation , that's inevitable , and not amount of persuasion will make us go out to borrow and spend when there is a perception that prices are going to fall

He's trying to deflate the currency and ease the WHOPPING 163% household DTI burden.

Debt to income?

Nah, That's all locked-in in NZ dollars.

Quote: "The odd thing is, low rates don't discourage consumer saving. If anything, they encourage it."

It's not odd at all. You have to save more to compensate for the lack of expected interest.

Well put.

We are told that retirees used to try to live off the interest (only) of their term deposits. Well for a start that is an artificial strategy. The remaining td will lose value due to inflation.

So the change now is that you can pretty much forget about the interest. You just use up the savings over time. Spin it out if you can. Use some internet 4% rule if you wish or dream up some sort of curve where you use more at the moment leaving you with less for when you are really old and don't need it anymore.

Well actually right now is not a good time to do anything with money other than living expenses. This latest lockdown has shown that to book and pay for any accommodation or travel up front now is too risky.

This will kill any travel local strategy

It's a bit like a wealth tax.

I gave up on term deposits a year ago and went gold...i havent regretted it.

Great picture.

Would have even more impact if there were a couple of picks and shovels leaning against the wall.

Zero and Negative interest rate by themeslves signifies the challenging timez ahead.

Is this positive to asset class bubble which is growing rapidly despite ecomoy downturn world over.

Unchartered territory best to wait and watch as anything is possible or gamble.

Any companies out there got any exposure to the safe manufacturing business? I want in...

Just put a large chunk in a 12 month TD at 1.55% so thats time to see where the market is heading. Fact is now that rates are so low you can just pull it with 30 days notice and get minimal penalties if you need it anyway for say a house.

It is a few months that I have not initiated new term deposits (I have not been renewing any expiring term deposits for the last few months), so I might not be 100% updated on this, but watch out that in many cases early termination of a term deposit is subject to approval by the bank. This condition is on top of the standard notice period of 30 days and of the penalty interest.

I would recommend that you check the T's & C's of the term deposit, just in case you really need this money at short notice in the near future.

Yes and this 30 day notice period change was brought in with no compensating increase in term deposit rates.

With virtually no return or negative returns after tax and inflation on Term Deposits you may as well put your money into Bonus bonds. At least there is a chance of a prize and the money is available after 2-4 days. It can be used as a bank account!!

It's no more protected against an OBR though.

Anyone investing with Squirrel - can get upto 4% and they advertise as they have lost on any lending ..yet

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.