Inland Revenue advised the government to couple the introduction of a new top income tax bracket with an increase in the tax rate on trustee income.

Inland Revenue, in a regulatory impact statement, flagged concerns over those earning more than $180,000 a year using trusts to avoid paying the new rate of 39%.

It recommended the 33% trustee rate be aligned with the 39% rate, to take effect from April 1.

Robertson open to increasing trustee rate

While the government hasn’t changed the trustee rate, Revenue Minister David Parker on Tuesday told a few journalists he would monitor whether trusts were used to avoid paying the new rate.

“If that behaviour becomes apparent, then we’ll move to increase the trust rate to avoid that being used as an avoidance loophole,” Parker said.

Asked by National’s shadow treasurer Andrew Bayly, in the House on Wednesday, whether he agreed with Parker and would consider hiking the tax rate on trustee income, Finance Minister Grant Robertson said: “If we see evidence that trusts are being misused then yes we would consider that.”

Ahead of the October election, Labour said: “We are not going to increase the trust rate because there are legitimate reasons for people to use trusts.

“But if we see exploitation of the trust system then we will move to crack down on those people who are exploiting it.”

Inland Revenue makes case for consistency

Inland Revenue maintained a hiked trustee rate would see the government collect an additional $1.5 billion over the forecast period to 2024/25.

It forecast a higher income tax rate on its own would generate $2.2 billion by 2024/25 - less than the $550 million a year estimated in Labour’s 2020 election manifesto.

Inland Revenue said the “unintended integrity impacts” resulting from the top income tax rate being higher than the trustee rate were “significant”.

It noted companies and portfolio investment entities (PIEs), which have a 28% tax rate, would also continue to be potential vehicles for getting around the 39% rate.

But lifting the trustee rate would “leave taxpayers with significantly fewer avenues for tax-driven restructuring (and would eliminate the easiest way to sidestep the rate)”, it said.

Inland Revenue recognised hiking the trustee rate might impact some lower-income beneficiaries.

"There are ways to mitigate this, such as distributing income to beneficiaries on lower rates as beneficiary income (so it is taxed at their marginal rates) rather than accumulating it in the trust," it said.

"However, these will have their own costs and may not always be feasible."

Inland Revenue didn’t recommend lifting the top PIE rate.

It said: “This was set due to a concern that, unless the top PIE rate matched the company rate (28%), taxpayers would use unit trusts (unit trusts are taxed at the company rate) and avoid dividend taxation at their personal rate by having the managers of the unit trusts buy back their units.

“Buy-back arrangements like this are not treated as dividends and the taxpayer’s profit from the buyback is usually a non-taxable capital gain.”

Inland Revenue went on to explain: “Even with a top marginal tax rate of 39%, the gap between the company tax rate and the top personal rate of 11 percentage points would be smaller than the gap in most OECD countries.

“However, New Zealand is particularly vulnerable to a gap between the company tax rate and the top personal marginal tax rate because of the absence of a general tax on capital gains.

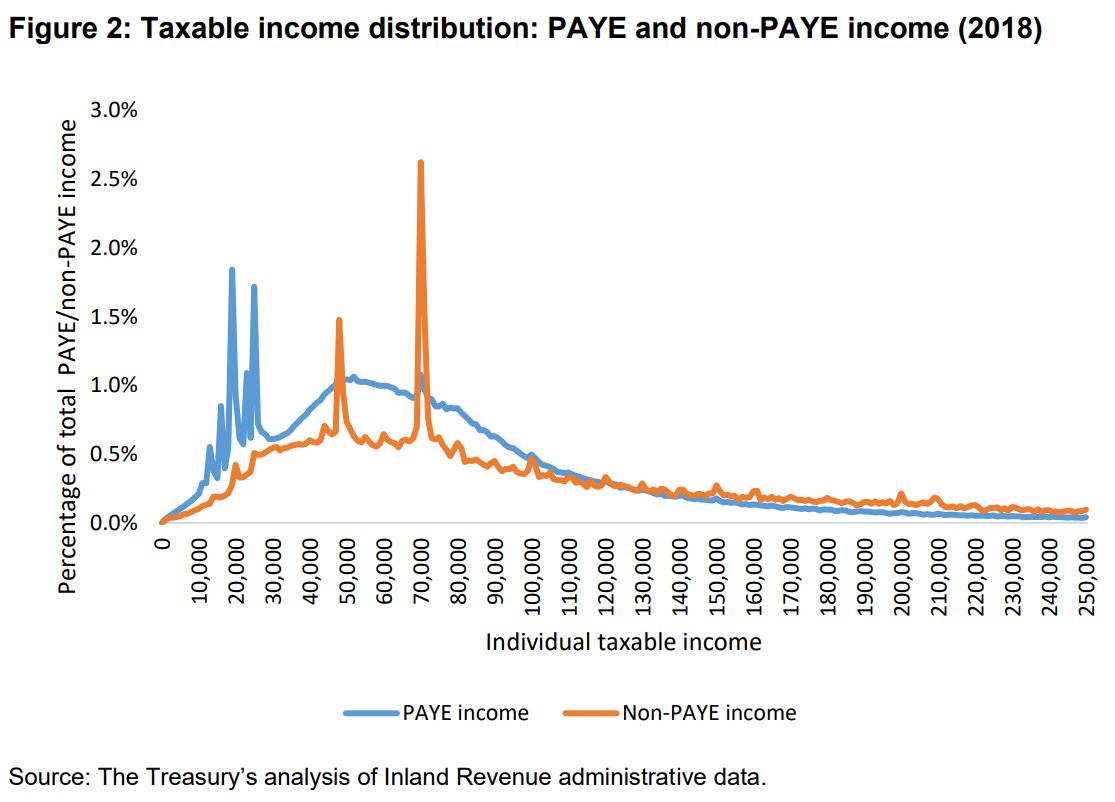

“There are already existing concerns arising from the differences between entity and personal rates in the current system. The bunching of self-employed people at the current tax thresholds in Figure 2 suggests that structures are being used by taxpayers to avoid the current top personal rate:

“Inland Revenue considers that a higher top personal rate will increase integrity pressures. Evidence to support that expectation comes from the increased avoidance of the top personal tax rate that occurred in response to the increase in the top personal rate in 2000…

“The bunching of self-employed people at the new threshold after 2000 shows that there was substantial movement by the self-employed to avoid the higher top personal rate.”

36 Comments

Tax tax tax.

Kindness was the cover of Labour's marketing brochure but tax was in the fine print.

. ... oh ... so , you don't agree with the Greens that " tax is love " ? ..

Jacinda & Robbo just wanna spread the love .... how sweet of them ... how very kind , team of 5 million ...

Poor trustees, my guess is 98% of the population will be quite happy if this goes ahead.

Absolutely right, After all it's only fair that the wealthy and Overseas Investors should pay the maximum tax rate they owe.

Sure, wealthy individuals spreading their investment income over multiple non-earning members of their families to pay lower taxes deserve kindness from lawmakers.

as long as it extends to Google, Amazon, Facebook etc I'm happy

I agree. There is more merit to tightening up rules around tax avoidance than the additional public revenue.

Much harder for local ICT providers to compete on pricing and content when foreign competitors do not have taxes cutting into their net margins (think Lightbox vs Netflix).

Also, many digital service providers have very little physical presence in NZ, which means they are sucking out revenue from here but incurring most of their staff and procurement costs elsewhere in the world. We keep discussing profits when in reality a figure closer to the company's annual revenue is being siphoned offshore ever year.

The softening up process has started.

Trusts will paying higher taxes under this govt despite pre election promises and all under the guise of a handful higher earning individuals might try to shift income to trusts.

Tax just causes new problems.

Sounds reasonable .. but how about lowering taxes .. even a 'Flat Tax' AND forcing councils to up rates to reflect needed infrastructure costs and profligate spending.

All well and good trying to balance business, personal and trustee taxation .. but it's just tinkering. Definitely impactful to a trust's beneficiaries though.

To the surprise of nobody...

Yes Labour has the clear mandate. No argument there. Except the agenda was long in place before the mandate was actually delivered. Folks we are now in for three years of 180’s and pet projects galore and denial of promises. Why? Because in reality there is no effective opposition and this government is about to launch themselves unfettered into the land of nod. You see we have to ask the RBNZ how to fix a housing crisis that we were going to fix easily in 2017, we have to implement their advice on tax reform differing to our manifesto. Being in government with absolute power thus means we can make it all up as we go. It has dawned on this government that they are unassailable, unaccountable. This is all confirmed one might suggest by the po faced Mr Webb in the caption photo, down mouth emoji in person. Watch this space. God defend New Zealand.

Accountants are rubbing their hands together with delight

So by this logic they will have to look at the company tax rate as well, interesting how they see no problem moving from their promises without a second thought...

Ability to utilise profit or assets for personal benefit more difficult with a company as it creates dividend issues. For example, a beneficiary living in a house owned by a trust rent free is fine, that would be a dividend to a shareholder.

The increasing difference in corporate and personal income tax is probably a good thing.

The way I see it, investors will either pay higher taxes on dividends, invest in growth ventures/assets or retain more earnings on their balance sheets; the last option being the least attractive in the current low-interest environment.

So by this logic they will have to look at the company tax rate as well, interesting how they see no problem moving from their promises without a second thought...

Given Robertson was advised by IRD the trust rate would also need hiking the outcome was pre determined, yet they continued to spin the line there would be no new taxes. Todays clumsy theatre is designed to deceive the masses into believing their deception that it is only in reaction to the surprise revelation naughty tax avoiders may spoil the party that family trusts are to be pillaged. They knew this would happen all along. Parker claiming his blatant threat to hike the rate was not really a threat is pure farce, largely unchallenged by a pliant media.

Yup, this is on par with the 'No hike in GST - oops here you go' that STILL gets sludged against the Key Govt all these years later - and rightly so.

However, crickets on this. If you make a change to the tax system that is going to create avoidance risk to the extent you have to backflip on your promise of 'no further changes to taxes' then you should be pilloried for it.

Dumbarse question: is there a difference between a trust tax and a trustee tax?

No, a trust needs trustees who are the legal holders of the assets and derive the trust's income. Reference to the trustees is to the trust. Income derived by the trust/trustees either remains with the trust/trustees and is taxed at the trustee rate of 33% or can be distributed to beneficiaries and taxed at their personal marginal rates. However, distributions to minor beneficiaries (under 16) is taxed at 33% to stop family trusts using kids to divert income to lower tax rates.

And yet the biggest tax loop hole of all (capital gains tax on investment property) remains wide open...

As I said before, this is a dumb move. You can see the unintended consequences a mile away. It'll force distributions to beneficiaries, or alternatively force the purchase additional property to soak up trustee income (via interest payments on the mortgage).

fat pat. Agree the consequences of this hike are not unforeseen. Robertson knows ratcheting up the marginal tax rate by a whopping 20% is a powerful motivator to adopt a more aggressive tax strategy. I have been reasonably relaxed in my approach to tax but am aware that if I were to pay more attention to tax minimisation I could significantly reduce my overall tax liability compared to what I was paying previously. Robertson and Parkers blustering threats and dismissiveness now provide that motivation.

All for a higher tax bracket, $70k is woefully low for the top, but it ideally would have been revenue neutral, and at least accompanied by brackets pegged to some inflation measure. We get an income tax raise every year.

"No other tax hikes"... Yeah Right....

Hah. Tax. If there is a loophole, of any kind, it will be exploited. End of story. None of this "if we see exploitation of the trust system". Rest assured, tax accountants are very good at hiding said exploitation, and I don't think even the IRD's multi-million $ digital system is going to help. They will always go after the low-hanging fruit.

They are gearing up in anticipation. The Taxation (Income Tax Rate and Other Amendments) Bill was introduced on 2 December 2020. Here is just one provision -

"Proposed section 59BA(2)(e) would require trustees to provide information on those with the power under the trust to appoint or dismiss a trustee, to add or remove a beneficiary, or to amend the trust deed. Requiring this information is necessary as “appointers” or those with power to amend the trust deed would not be disclosed otherwise....."

game on I'd say..

This Labour government has confused weakness with centrism.

All the leadership ability of a wet paper bag. Zero conviction.

Heaven forfend that electorates should have to get message that investment in public infrastructure , flood protection, sewers roads, public housing COSTS MONEY and hence taxes to pay for it.

I guess a lot of us thought we were paying for stuff like that already.

Tax on productivity (income though creative or productive activity) will just drive more dead debt based speculation on property, with an extended land bank period to be tax free. Just get on with the land tax (anti speculation) and reduce tax on working (promote productivity).

Simple. Unavoidable.

Sounds like a new tax Jacinta baby !

I think we can solve the "Trust" problem, by simply renaming them "Dubious".

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.