The Reserve Bank (RBNZ) is remaining tight-lipped over whether it believes the Government should empower it to restrict the use of interest-only mortgages.

Finance Minister Grant Robertson has asked the RBNZ for feedback over whether it could support the Government’s goal of making house prices more “sustainable” if it were to be given the power to restrict banks from issuing interest-only mortgages to investors.

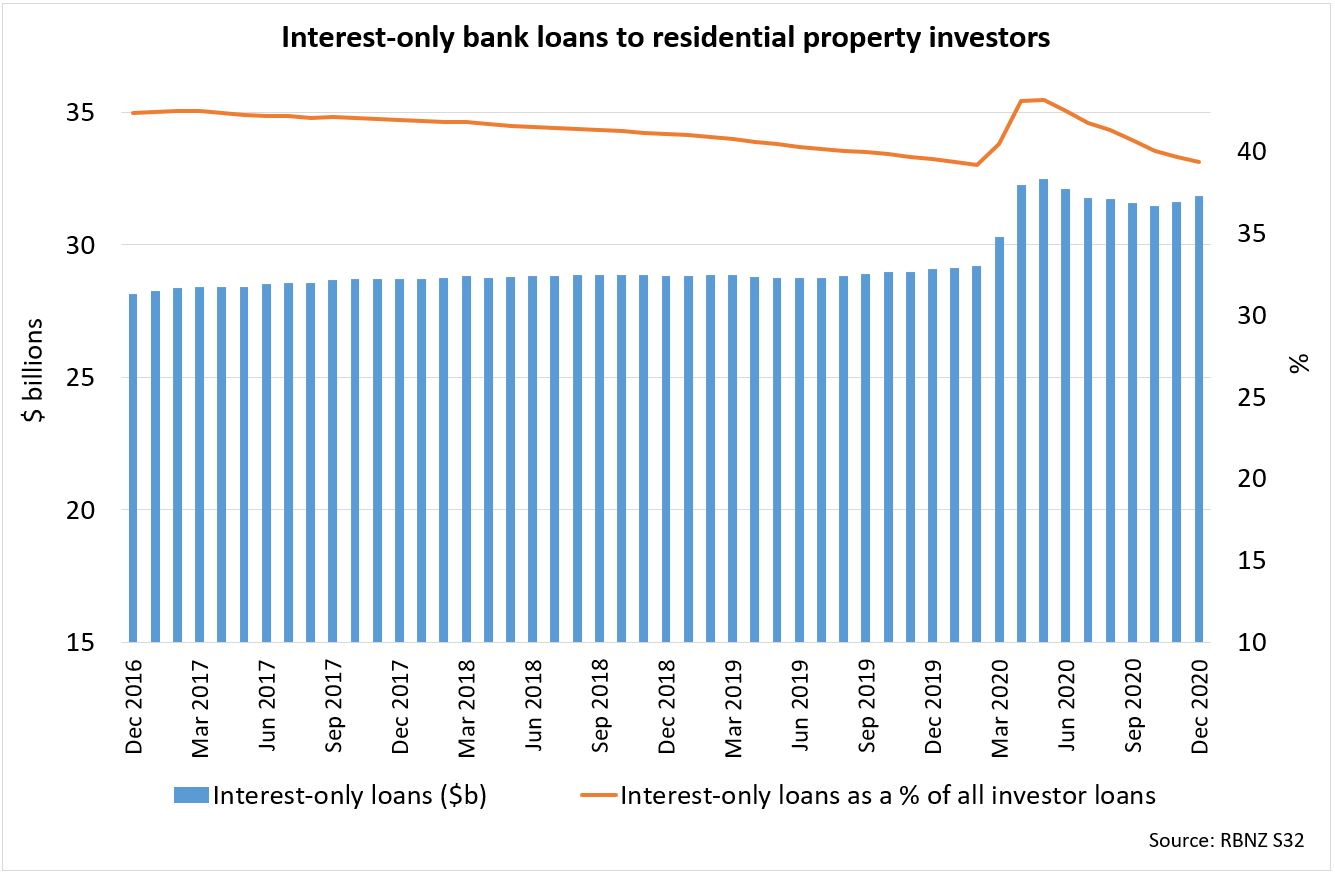

As at December, 39% of bank lending to residential property investors, worth $32 billion, was interest-only.

That portion was on par with where it was pre-COVID-19 when there were a lot of mortgage repayment deferrals (orange line in graph).

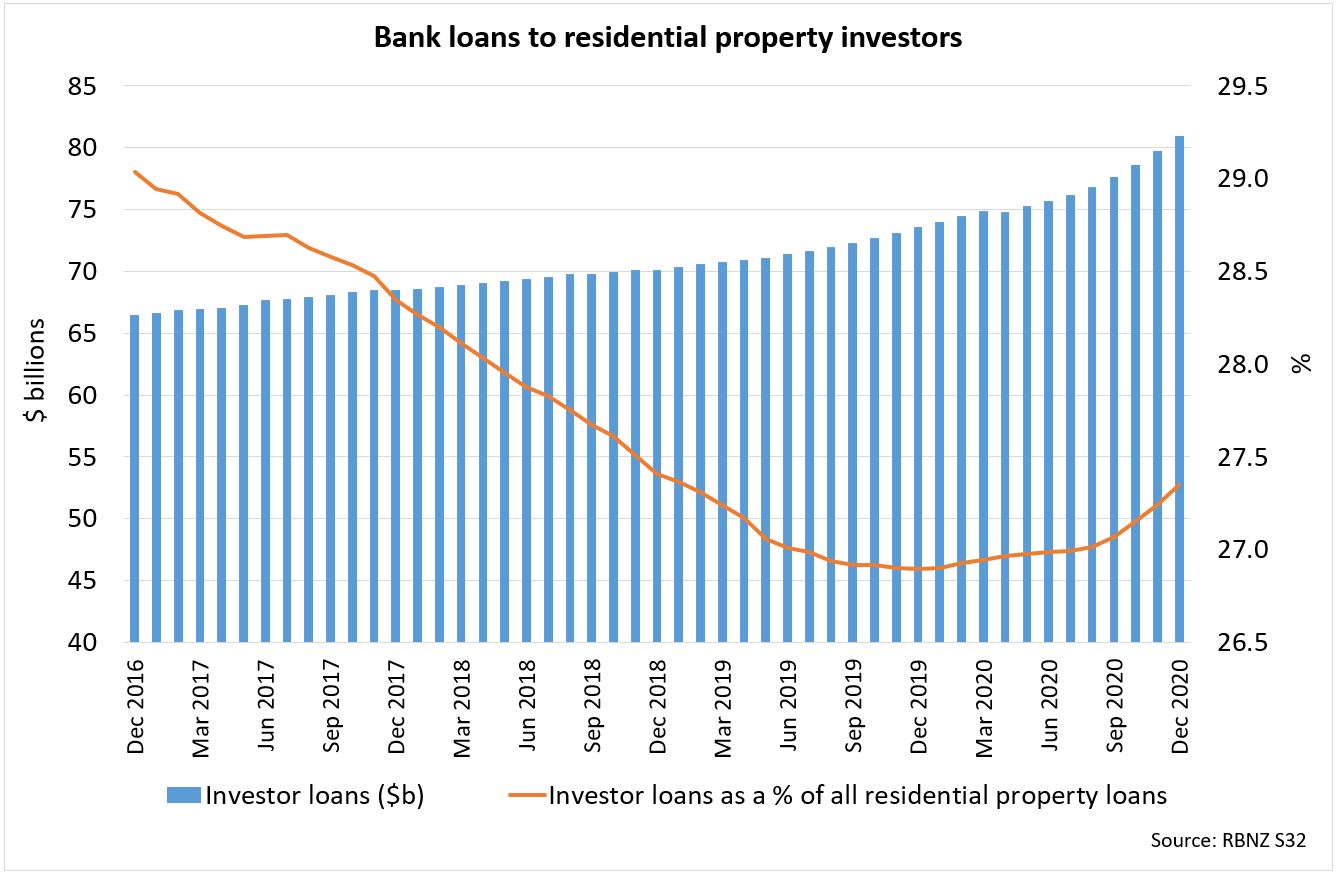

Yet because investors have borrowed up a storm over the past year in particular (graph below), the value of interest-only mortgages taken out by investors has plateaued at a level about 10% higher than pre-COVID-19 (blue bars in graph above).

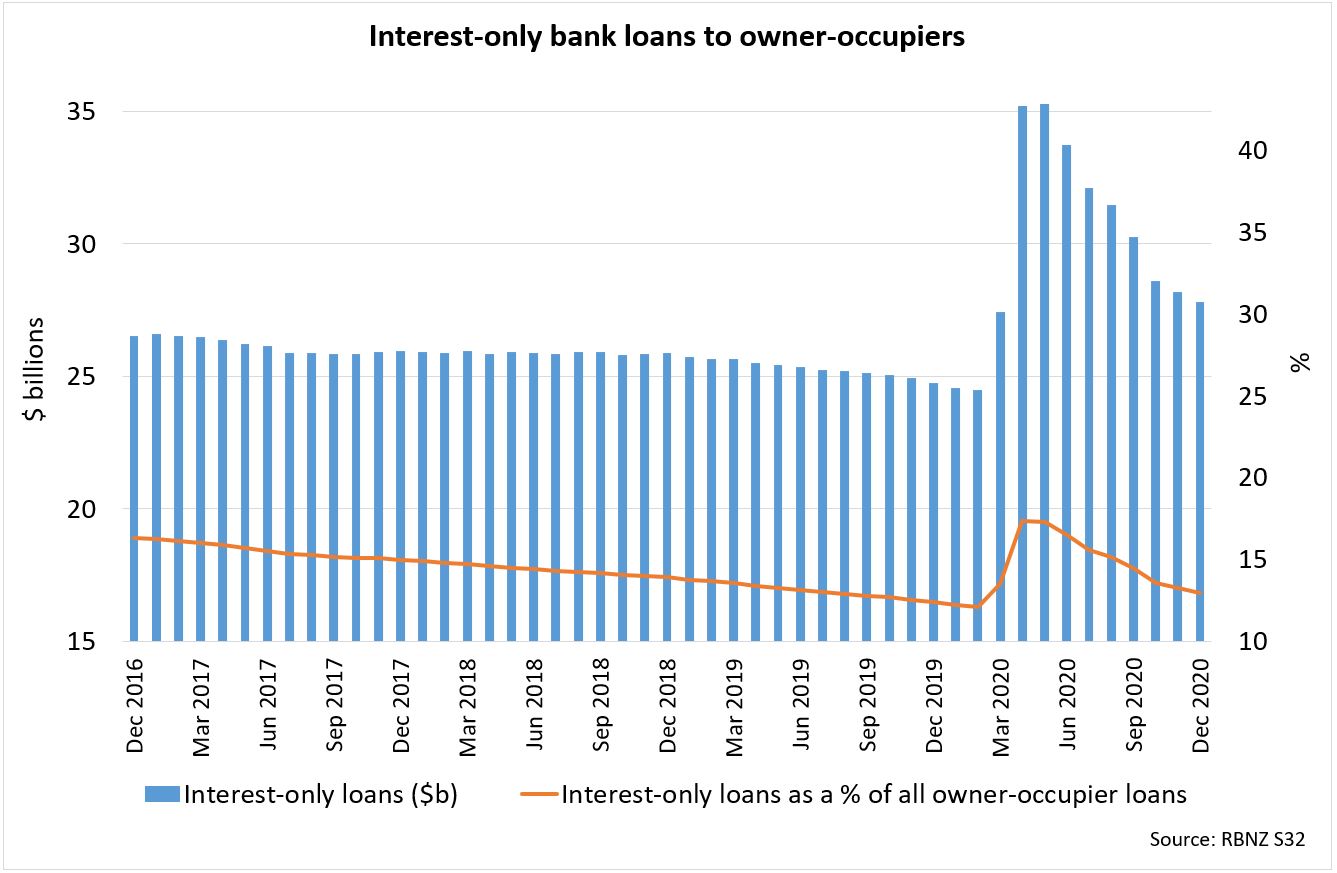

Only 13% of owner-occupier lending, worth $28 billion, is interest-only. Yet the value of interest-only mortgages held by owner-occupiers is about 12% higher than it was a year ago.

Asked by interest.co.nz whether he believed 39% was too high a portion for investors, RBNZ Governor Adrian Orr said the RBNZ hadn’t formed a view on that yet.

He said the RBNZ was looking at whether interest-only mortgages were being used too much and were causing “high price variability” and “extreme risk taking”.

Speaking to interest.co.nz earlier in the week, RBNZ Assistant Governor Christian Hawkesby said the RBNZ would need to consider how restricting interest-only mortgages might fit in with the other tools the RBNZ deploys to restrict bank lending to maintain financial stability.

He questioned whether restricting banks from lending to borrowers seeking a lot of debt compared to their incomes would sufficiently address concerns around leverage.

The RBNZ has long wanted debt-to-income tools. Robertson is asking it for more information on whether these could be targeted to investors.

RBNZ considering making LVR restrictions permanent

Addressing those gathered at Waikato University for the 2021 Economics Forum on Thursday, Orr said leverage was a “significant risk”.

His “gut feeling” was that loan-to-value ratio (LVR) restrictions would become a permanent fixture.

When the RBNZ introduced LVRs in 2013, they were only meant to be used temporarily to restrict high-risk bank lending.

However, LVRs remained in place, in some shape or form, until the RBNZ removed them in April 2020 to remove an impediment to bank lending. The RBNZ then reinstated restrictions at the beginning of the week.

Most owner-occupiers need a 20% deposit and most investors a 30% deposit, with this investor requirement formally being hiked to 40% in May.

Orr said the RBNZ was doing work on whether LVRs would become permanent.

“We have to really ask, what is the optimal setting?” he said.

“Is it zero, or is it something that is always on? If it’s something that’s always on - small but positive - is that a much better position for long-term sustainability? I’d have to say, my gut feeling is… yes.”

Banking sector and tax setting could be in for a larger shake-up

Orr was “very worried” about the asset price inflation caused by loose monetary policy, even though the RBNZ effectively planned to pump these up to create a wealth effect to stimulate the economy.

He stressed this was a global phenomenon and the RBNZ would not change the way it sets monetary policy to help meet the Government’s housing policy goals.

“In understanding fair value [of asset prices], we’re going to have to do a lot of work, which is going to unveil a lot of policy settings that explain why we are so heavily invested in housing in New Zealand,” Orr said.

“Some of those settings are going to come down to uncomfortable facts, like access to leverage, the structure of the banking sector, the favourability of some loans versus others and taxation.”

RBNZ reluctant to exempt owner-occupiers from borrowing restrictions

Orr reiterated what he’s told interest.co.nz before - that it’s “incredibly difficult” to target the likes of debt-to-income ratios to certain types of borrowers like investors.

“But that doesn’t mean it’s impossible,” he said.

Orr said the RBNZ would highlight to Robertson how it could target debt-to-income restrictions, and point out how people could get around these rules.

Robertson said: "It’s important that any potential restrictions do not disproportionately affect first-home buyers and low-income borrowers."

Yet Orr said the RBNZ was generally reluctant about targeting these, as they lose their effectiveness.

176 Comments

"Asked by interest.co.nz whether he believed 39% was too high a portion for investors, RBNZ Governor Adrian Orr said the RBNZ hadn’t formed a view on that yet."

How much more time would the RBNZ like?

How much more time would the RBNZ like?

Now, all of a sudden, they're concerned.

FFS. This is real banana republic stuff.

I swear he looks more stressed now than he did during the initial phases of the pandemic. He has a terrible poker face.

I agree. Such a far cry from when he was first appointed he reminded me of an actor energetically and enthusiastically bouncing up the stairs to receive an Academy Award. Now he's continuously flustered and red faced, verbally empty, and body language to suggest 'get me out of here.'

Terrible time to take over the role - especially if Dalio is correct and we're at the end (or very close to the end) of this long debt cycle.

Liked Dalio's presentation, clear, concise, humble easy to understand. 2+1=3, unlike NZ economic vested interest; 1+1+1+1+1-1-1=3

He's up shits creek without an oar...

Anybody know where the horse is?

Orr's incompetence is eye-watering.

It is not Orr who is incompetent, it is the Government that is irresolute. LVRs for property investors no longer suffice. The property craze has reached the point where we need a total ban on lending to property investors who want to buy existing homes. And those investors who do manage to borrow from somewhere should be denied any tax credits. Only investors building new homes should be allowed bank loans. These are decisions only a government can make. Do we have a government?

Could not agree more, but wealthy vested interests are at stake here and they control Government policies

You could be right but then landlords might claim they should charge beneficiaries a higher rent in order to reduce the number of people on a benefit. That logic is just as sound as higher taxes based on employment class or race.

If it looks like a ponzi, smells like a ponzi...

.. then It's probably a NZ wealth creation.

https://www.stuff.co.nz/business/124438249/gale-force-economic-warning-…

LVR's are permanent....until the next downturn!

"People should be very worried about soaring asset prices that have been driven by low interest rates, Reserve Bank governor Adrian Orr says.

Responding to questions at an economics forum hosted by Waikato University in Hamilton, Orr suggested people were not pricing in risks in the share market and housing market correctly."

That's LITERALLY YOUR JOB you numpty. To set the playing field so that people don't take extreme risks. It's literally your job as you have a mandate to ensure financial system stability. Blaming others for a lack of YOUR ACTION on people being able to take too much risk is blame shifting at its best. And instead of doing something intelligent, you are throwing gasoline on the fire to try and put it out (in the form of printed money).

(pasted from another article)

Those graphs make for some scary reading. Interest only loans should not exist at all IMO, unless you are a developer (even then I would consider them risky). They are predicated on the idea that house prices will only go one way, UP! As soon as house prices drop, they could trigger a financial crisis as banks would be underwater.

Reserve Banks are like the crazy person with multiple personality disorder and you don't know which person you are going to meet on any given day.

One day...'well we need to keep lending and get more debt into the system so banks please lend lend lend'.

Following day...'well leverage is a significant risk to the financial stability of the entire economy but we need more debt creation to avoid a depression type situation unfolding'.

Next day....'so we've lowered rates more so that we can create more leverage'

Next day....'we're worried people aren't assessing the risks properly but we're encouraging everyone to load up with as much debt as possible please'.

Are you #%@#@#$ mentally retarted? You can't be the arsonist and the fireman at the same time without going to jail and spending some time in a psych unit - unless you're a central banker.

Yes. This is bordering on schizophrenic behavior.

I don't have anything against Orr personally - I think he' a nice enough guy and doing the best he can in the circumstances. But his hand is forced by the Fed who set the direction of monetary policy. And Orr can't fight that without significant consequences - so he's screwed either way.

And Orr can't fight that without significant consequences - so he's screwed either way

Oh, I'm aware of that. But they need to be open and transparent about it. Tell the public that we're all part of the system and they cannot stray far from the dogma. Most people really don't have any idea so emphasizing the consequences at least makes people think and can even force the hands of Robbo and Princess Leia to act.

Those statements from him like 'people aren't assessing the risks' is the warning.

If the house of cards tumbles, he can say - we'll I told people they weren't assessing the risks correctly - see.

Those statements from him like 'people aren't assessing the risks' is the warning.

I'm not tracking this comment but my feeling is that it's only recently been used. Furthermore, he's on record at least twice now for stating that 'housing is a consumption good' (the banks will be a little dark on him for saying things like this).

If my memory serves me correctly he's stated that a few times since LVR's were removed and we saw investors piling into the market.

He also said it was a good problem to have

Compared to the alternative, in the RBNZs view (and I suspect most everyone else) it is.

Compared to not removing LVRs and ringfencing low interest funding to productive enterprises?

Dp

Good observation.

I completely, wholeheartedly agree. Clearly Orr has got to go. Now. Yes he has been given a mandate that is becoming progressively more convoluted and possibly contradictory, but he does not seem to me to be up to his job, given his unbalanced, shortsighted and panicky actions.

no, risk management is the investor's responsibility . However RBNZ has surely overdone it's job on muting that risk and then suddenly after busiest months and thousands of FOMOed FHB entered the market they remind about risks . Nice!!

That is a cop out. Greenspan sat idle and let the sub prime crisis happen. His excuse at the end was he thought it was in the commercial bank's own interest to lend more prudently. Orr's main responsibility is financial stability.

Neoliberals always want market freedom, until something bad happens of course, then they ask daddy state for help because they were allowed to mess things up. Bad boys!

agree, FHBs aren't investors so don't have to think about risks

andreas

“FHB . . . don’t have to think about risks”

You are joking surely?

Hmmm, I meant in classic terms, no strong obligation, they are buying to live in it , so SHOULD assess risks. Oh that’s a play of words , of course they must not borrow more than they can serve. Hope you know what I mean, anyway RBNZ can’t expect the same risk assessment level from FHBs as from investors. But who cares anyway

prior to the 2008 GFC, the great interest rate hikes when under Bollard, there was a saying around the traps that the RB would arrive too late at the party, do too much and stay too long. Seems that is a mantra then, embedded into the mission statement then, still in play now.

Financial system risk management is the RBNZs job. Ergo if too many people are taking stupid risks, it's their job to fix that problem. Else they shouldn't have that mandate.

And the retarted thing is that they've been taking those risks because the central bank wanted them to (because if credit stops expanding 'we're looking at a depression type situation') - by removing LVRs and dropping interest rates.

You couldn't make this stuff up.

Even more retarded is weve seen the consequences of excessive risk taking recently.. anyone remember the GFC?

I lived through the GFC and the property bubble bursting in the US in 2008 (and the aftermath). What we have in NZ now is on a completely different level.

It wasnt long ago at all (unless you're a millennial) and people pretend it never happened. Just look at USA now. This is going to make GFC look like a test run

excepting that you cant regulate for stupidity

No, you're missing part of the picture Andreas. While any buyer must understand their personal risk when taking out a mortgage, and sell it to a bank to get their mortgage, and with the banks working on individual risk profiles, there is a huge risk that they are loosing sight of the overall market risk and not seeing international trends. Until now they seem to have largely operated on a belief that inflation was still a long way away, but current signs are that it is ticking up, and possibly faster than most expected. This is where the RBNZ steps in.

The trading banks have screwed up by being too greedy and not recognised the risk of their operating too close to the risk margins of their clients and the market, but the RBNZ should have seen this and acted to limit or prevent it, or at least advise the Government to do so. The RBNZ has informed us that it mandate is to manage risk for the whole economy, not just housing, but then it has also told us (contradicting advice given a year ago) that a house price collapse would threaten the security of the banks. Thus by their own admission they have effectively dropped the ball in maintaining oversight of the risks to the economy. The Government is highly dependent on it's experts to advise them, and ignores that advice at it's own peril. the problem as i see it is that the RBNZ has been as much at fault as the trading banks, and likely too soft in it's advice to the Government.

He's been taking notes from Jacinda (deflect to citizens) . His job is to cause a financial crisis by pumping money into asset bubbles then flipping the switch. And with every crises comes opportunities

I give up on this contradicting clown

My question is, 'how the hell did he get that job'.

Problem is he's a slave to the Fed - its not his fault personally. He's simply taking his lead from them and can't move in a different direction (without significant consequences).

So why have we given over our monetary sovereignty to a foreign power????

Being the reserve currency gives the Fed the ability to dictate terms. Don't like it - have a war and become the new world power and set the rules of finance/trade. Until then, if they devalue the USD, what are you going to do? Not devalue your own currency? The Fed don't care that we have a massive housing bubble in NZ which is getting worse every time they dropped rates and we had to follow.

The race to the bottom has reached the bottom as a tie.

Excellent question! RBNZ's stock answer is they don't want the NZD to appreciate too much. But what is worse: a NZD that is painful for exporters of price-sensitive goods (we should be aiming to export high-end products) or a highly destabilising crisis like the US property market crash in 2008?

He got the job because of his apparent ability to "pick winners" as head of the NZ Super fund.

Hold up. Would cheap credit flow to property in the same way if there was a CGT or any measures to treat income from housing the same as income from other ventures? The lady with the big teeth chose to maintain the tax code thusly. Credit will find the best returns. That would be NZ property. RBNZ can't change that.

Now, now Blob.. be kind. You're well aware that DTI tools always rejected by both govt, despite requested by RBNZ, they only got the chirpy LVR in 2013, then 2018 Labour added 'unemployment' mandate, apart from OCR, now.. the verbal mandate (not written/legal yet/PR stunt) about the housing, even the DTI still being uttered as consideration/study for 'investor' only. All, despite an on-going clear rejection of CullenCGT/slap in the face. If CGT suggestion a bit like Cancer verdict, then govt. 'just followed' the patient voters of 'denying it' - Took me weeks and months, to truly understand Mr. Orr geniuses.. oversize QE/LSAP, LVR removal, hopefully OCR still go to negative.. stall it, stall it...stall it - C'mon guys, support him & the team - he got short time mandate to do so, unlike the Pope, leave the frowning PR to other/s.

Interest only loans are a recipe for trouble. Should be outlawed.

It's the thrill of gambling!

I personally believe gambling should be left to the derivatives market - not something so crucial to the well being of a society like home ownership.

What could possibly go wrong? House prices never fall.

I knew this would happen. Everyone getting worried now...https://www.stuff.co.nz/business/124430525/adrian-orr-frets-over-soarin…

If property owners fail on their mortgage obligations, there better not be bail outs...for god sake give FHB and non asset owners a fair chance on a market correction. Stop F@%king pampering asset owners. Mr Orr you have already boosted their paper wealth, what are you going to do about the ones that are left behind, apart from pushing them to take on huge amounts of debt.

No Property Investor Left Behind! Indeed they are pampered pooches, until they aren't

I am extremely confident that property owners will be bailed out, at absolutely any financial and social cost. Labour and National politicians alike would rather destroy the vestiges of a productive economy than see a big nominal fall in house prices.

I would bet the house in it, if I had one.

This makes me physically sick. Investors must stump up 50% in cash not equity and no interest only for investors. Then see how FHB quickly get on the property ladder.

Toothless government, incompetent RBNZ and forever filled with greed, unethical banks making New Zealand unfriendly to its own citizens to live and thrive.

Passerby

Not valid - leveraging is simply converting equity to cash.

What for? cash is no longer the king... property is... NZ is not that far where, properties can be valued/bartered/traded for medication, groceries etc. - cash is just senseless numbers, that non-intrinsic, cannot be touch, cannot give peace of mind to raise future tax payers etc. It's just that I still trying to understand.. from every CBs/RBNZ to Banks of the so called developed economy...much of them issued, hoarding all those senseless numbers, hell they still even entice future tax payers/kids to save... what is that F*zz all about? - but grown up advise is the opposite?

"Show me the incentive and I'll show you the outcome."

"Orr said...the RBNZ effectively planned to pump these up to create a wealth effect to stimulate the economy."

One day Adrian will look back on that fallacy and weep.

Higher Asset Prices backed by Higher Debt isn't Wealth! It's ....more debt...which makes us poorer!

Wealth, is more jobs; better productive incomes (more productive businesses making more things employing more people in other words) and LOWER national debt, (both Public and Private).

I get the feeling that 10-20 years from now the current situation (fiscal and monetary policy management) will be the focus in many econ and finance uni papers.

Central bankers are turning into the modern day Enron of the world - but with nobody to audit them or police them.

Most likely.

Adrian is just sticking to what he was taught; what they were all taught. And look where it's got us!

Right here.

If those like the RBNZ Governor can't look at 'results' as evidence of past policymaking, and see them for what they are, then there is no hope for a 'gentle landing'. Maybe they genuinely think they've done a good job? "Look. Without our intervention do you know where we'd be?". The answer is "No one does!" but we do know where we are now as a result of what they have done. And 'somewhere good' isn't it.

When you've spent your whole life and reputation believing that the World is Flat, what else should we expect from those charting our course into the future?

And there will be a documentary called Princes of the NZD (doesn't have the same ring to it as Princes of the Yen) with Orr playing a starring role

Watched that again a few months ago - its hard not to see the similarities between late 1980's Japan and what is going on in the economies of the anglosphere.

Will be interesting to see how long this plays out. Watching America

bw.. Doubt that Orr will look back and weep. I mean the man does own 4 or 5 houses (that we know of)

Is there any requirement for reserve bank staff (or key decision makers) to put their assets in blind trusts? (preferably in offshore assets).

Without that, they truly are a self licking ice-cream cone. 'Were here to serve you, the public, but really we're just here pampering our own portfolio values'.

I've only been able to find a unit in wellington and a house in Pukehina. None of the companies he is associated with are directly linked to property ownership. Under what vehicle does he own the other 2-3? between them worth about 3M, but I don't find that overly shocking for someone who has spent their career in economics.

Access to leverage: to him that hath and screw the renters.

Similar to inflation v wage growth and house price rises v wage growth.

It would be nice if we got any indication from RBNZ or the government of them taking an iota of notice fo what they are doing to society: people will have fewer kids. Immigration levels will , again, see the new arrivals having 3 kids compared to Pakeha having 1.7 and fewer. This changes the make up of the society. Also, wages are higher and houses overall cheaper, in Australia, so young remotely ambitious leave. None of this, it appears, is allowed to enter public debate or be mentioned on news, or stated to be of concern to Kiwis (which it is)

The food in NZ is getting better though.

Fiddling while Rome burns

Orr fiddling..eeeewwww

Yip, minus the spec, wearing toga.. bowl of sour/wine grapes in the front table... fiddling the harp.. wait wait.. about to sing.

Central banks deliberately inflate asset prices to generate the so-called ‘wealth effect’.....then express alarm at high asset prices.

Sounds the arsonist wants to escape responsibility for the fire he lit. Are central bankers now going to try to slither away from the impending carnage they have created? Turmoil in the bond markets is perhaps the first sign that the stitching is starting to come apart.

Thirty years ago we thought Japan was crazy for having 100 year mortgages. These interest only mortgages repay zero principal so are infinity year mortgages. Btw the japan housing crisis of thirty years ago did not end well.

Japan didn't have immigration to "refill" it's population and keep house prices trending upwards. In New Zealand we just need to hold the gates open to avoid devaluation.

Indeed but I wonder if the demand influx is all its cracked up to be when so much 'demand' (people) flows into living with parents, bunking on freinds couches etc (I know of one young working couple sleeping in their van in a friends driveway), hotels, you name it. These people are not behaving the way property investors would love ie bidding up rents

Japan where apartment dwellers fold futons up against the wall during the day to create living space, I was taught in primary school class-project in the 80s, this was a quaint oddity of polite Japanese culture. But now I understand what led to the tiny apartments and that practise. Amazing to think people would sign up for 100 year mortgage. I'm guessing the bank inherits the property when the owner passes away

The idea was your son and then grandson paid off the mortgage.

KK..Japanese housing crisis has still not ended has it? If you bought in the early 90s you might get 75% of what you paid for it today.

If you hold a deposit in a New Zealand bank you really have to ask "Can this bank take a punch?" If the answer is "No" then you are playing with fire and will likely become a bond holder.

Also LVRs are a joke when property is fluctuating in value this rapidly. If you want to get over 40% just wait five minutes.

squishy... I am pulling allor most of my TDs as they mature. Will put them in foreign banks with a Govt guarantee just in case. NZ banks will probably be OK but better safe than sorry. And as I already have shares in ANZ and CBA I will be better diversified by having the money abroad especially when NOBODY has any idea what will happen to the NZD.

Looking forward to govt announcement in mid March.

BOLD govt announcement, that in no way was delayed to wrap in with meaningless supply promises because it won't be BOLD at all.

don't hold your breath

Totally going to be delayed. What was their reason for the last delay...?

Praying for another outbreak to distract us from thier #1 policy promise. Don't ever forget. This is the main reason they where originally elected.

In a very odd way Orr is acknowledging his mistake of removing LVR restrictions by saying they might be now permanent, however the lack of action regarding the OCR level is not compatible with his concern about over leveraged investors and households.

So he gets told to worry about house prices, and so he does. Sort of fair enough.

I'm glad he is at least openly worried. Baby steps

Mr Orr if you were reading comments about Interest Only Would know that genuine investors are not on inyerest only but is mostly high speculators are - SO WHAT YOU ARE SAYING IS NOTHING NEW - NOW WHAT IS IMPORTANT IS WHAT AND WHEN ARE YOU GOING TO ACT ON IT.

Nearly 40% of bank lending to residential property investors is on interest-only arrangements - RBNZ tight-lipped on whether this is too high, but raises concerns over leverage

Governor of RBNZ when concerned about house price fall last year acted immediately and now is concerned about high liverage and interest only loan STILL only talking about concern and highlighting Interest Only Loan but not acting.

This sums up, how serious RBNZ and Government is in controlling the housing crisis. IF daily price rise os $1250 per day is not an emergency, what is ? Jacinda can you answere it - know such questions will be answered by straight face (smile missing) but do not mind, how you answere but answere

OH MY GOD

Australia addressed interest only loans and what they were doing in overheating the market back in 2017 and tightened lending standards - the result was a 10% drop in the Sydney and Melbourne housing markets- a correction that was needed.

Meanwhile in NZ a correction like this could have huge ramifications - but not to fix the issue with interest only loans could have even more devastating effects when interest rates start to rise - especially if the housing shortage corrects at the same time making it difficult for rents to rise to cover the increased interest charges.

Clearly we are set to re-learn the lessons of the Financial Crisis.

Did we ever really learn them here though? Or just look offshore with a smug smile and our 'rockstar' economy....

A 10% drop would be nothing here. Take us back 7 months. Do it now, or you bake in a 20% increase

But if I am right (which of course is highly questionable) a 10% initial drop would be very likely to feed off itself and become a much much bigger drop. I do not think the powers that be would be overly concerned about a 10% drop. They only reason why they are so overly concerned (in my view) is that they understand where that initial 10% drop is likely to lead and how long it may take us to recover from it.

what amazes me in NZ is not just the high rate of interest only loans but the lack of offset loans. We were talking to a broker (we are thinking of upgrading) and mentioned we want an offset loan and he said only 2 banks offer them in NZ - Westpac and BNZ.

We used an offset loan in Aussie for our first house 15 years ago and we reckon we saved $200K (50% of our projected interest) having the offset loan. The advantage of paying off the loan faster by using your savings but still having cash for a rainy day ie illness, redundancy or just wanting to renovate or buy a new car - I don't understand why kiwis are so reluctant to use these types of loans.

Lending in NZ feels very behind the times and it feels like Kiwis think very short term when it comes to their finances.

There's banks that offer revolving credit facilities aswell, similar concept...

Yes but even these according to the broker are rarely taken up - he said he mainly sees them when people are either building a house - to fund the purchase before selling their existing house, people who are using them as a bridging loan (particularly investors) or people who are doing major renovations.

Probably because floating rates are almost double fixed rates.

Our loan products are extremely simple here - check out the UK, where having more equity gets you lower interest rates. Not as a broker special, not as a deal you only get if you twist the right arm, an actual board rate that rewards you for paying down your mortgage quicker. Unthinkable here.

Haha yeah the opposite applies here, the more debt the better the rates you get offered.

Our banks have higher rates for low equity.

Take a look at the HSBC UK board - I'm not talking a punitive rate for having a sub-LVR amount, I'm talking rates that get better at 30, 40, 50%

An interesting article across the ditch. Record home loan applications - but debt levels are declining as Aussies pay off loans faster than they take them out. Compare and contrast NZ - this is what good debt management looks like.

https://www.macrobusiness.com.au/2021/03/aussies-are-taking-out-and-rep…

I'll bite!

Offset Loans should be banned in their entirety. (Disclosure: I have one, leveraged against our home and 100% OffSet. I've been to the Banking Ombudsman (a biased collection of individuals controlled by the banks) to argue the ambiguity of their product ie: Principal will be collected regardless of the amount of Offset. It's not just the interest component that's Offset as was widely advertised "Only pay interest on your outstanding balance" etc.)

They deny the country tax - normally paid on any saving surplus, and

They do as you suggest - stop people paying off their debts, faster.

They give people a false sense of security (read the small print. Banks can apply any surplus balance in an Offset Account against an Outstanding Loan at their will)

Sorry it took a little while to get the Sarcasm.

Given most savings accounts are paying about 0.20% interest - not sure much tax is going missing - but I agree heaven forbid young kiwis save money and pay off their debts faster - it might encourage them to join their parents in buying rental properties

Well your broker is wrong because Kiwibank also offer them, and given the floating rate is what is used for offset mortgages, and Kiwibank are 1% lower than the others, you should talk to Kiwibank first.

I'm awaiting a soft policy of limiting time frame of interest only per investment loan - eg. max 2 years interest only. Some banks have similar rules already but often make exceptions. This policy would be classic Labour PR to make it look like they're taking action but in reality is already status quo.

All politicans are same : Deny, Lie and Manipulate.

Weirdly when I enquired about interest-only mortgage for my investment property ~6 years ago with BNZ (had already had the mortgage with them for about 2 years at that point), they said they could only do it for 1 year because they had a limited amount of interest-only mortgages they could dish out. I ended up having another (otherwise pointless) meeting with another bank salesperson who tried to get me to take out life insurance, but she also put 85% of my mortgage on interest-only for 5 years with no quibbles and no questions asked, basically went out of the room for 5 minutes and then came back and it was done. I later got the remaining 15% put on interest only and they just made it match the larger chunk's duration for simplicity.

So now I'm quite dubious when a banker tells me something can't be done.

20 years ago it was near on impossible to get interest only. Even with good equity I was refused it several times. No problem. Just took a 3 month rent holiday every 2 years. As the "ladies" with big hands and feet say in Thailand. Same same, but different.

Those ladies with big hands have witnessed many a foreigner fall over the balcony.

KK... indeed, there are a lot of "suicides", often by jumping off balconies in Thailand. Don't believe it. As far as I know many death certificates in Thailand still list "heart stopped" as cause of death. Having said that it is generally a pretty safe country.

Banks will only approve interest only for a set period (e.g. 5 years), if you then want to extend they'll make you disclose your financial situation again. This is for the reasons:

1. If house prices fall they can force you to sell before you get into a negative equity situation which prevents or limits losses.

2. Of your income is diminished to a point where you would struggle to pay the loan they can force you to sell and prevent or limit losses.

What you saw before the financial crisis of '07/'08 was interest only terms without these safety features for banks.

Meanwhile ASB CEO indicates people may have overextended themselves.

Even as many homeowners’ paper wealth and confidence has been boosted by low interest rates, ASB chief executive Vittoria Shortt sounded a different alarm.

"Shortt told the conference the bank was closely watching a worrying trend over the past two months of more customers having difficulties making payments and running low on cash.

“Fewer customers have what we would describe as ‘a rainy day savings fund’ of $1000 or more, which is a pretty low bar,” she said.

Is it possible that young ones are running out of disposable income as they try to pay hefty mortgages. One of my team members who has bought off the plan has cancelled her wedding as she's worried about how she will pay her deposit at the end of the year. FOMO and doing anything to get a house may result in hits to the hospitality, tourism and retail industry as peoples incomes are spent on housing. Thankgod NZ exports are pumping otherwise we would all be thinking What a disaster

Meanwhile Shortt gets paid a $1000 an hour (don't know exactly but probably not far away) to create the mess she mentions - just goes to show how broken this current form of capitalism is.

Why would ASB care? They can hedge out the risk of default using CDS (taking into account counterparty risk of course, as we learned during the financial crisis.)

Low interest rates absolutely *guarantee* rapid house price inflation - especially when NZ has tax and regulatory settings that pour petrol on the fire. Orr can fiddle round the edges with LVR but it will take braver political decisions to get us back down to earth. Fat chance?

Oh, and a plea - can we stop saying that 'printing money' is causing house price inflation? 1. QE / LSAP is not printing money - it is swapping liquid financial assets (cash) for less liquid financial assets (bonds). This doesn't add to the broad money supply (check the RBNZ balance sheet and you can see this clearly). 2. There is no clear link between this QE / LSAP asset swap and house price inflation. QE / LSAP does however leave some financial institutions with cash to invest in other things - hence the growth in share prices.

Why hasn’t quantitative easing produced inflation? The answer is rather simple: quantitative easing is nothing but an asset swap. It doesn’t change the total amount of government liabilities in circulation. It only changes the form of the government liabilities that must be held by the public. The Fed buys Treasury securities from the public, and replaces them with currency and bank reserves (base money) that someone has to hold, at every point in time, until the Fed sells its bonds and retires the cash. All monetary policy does is to change the mix of government obligations held by the public. Only fiscal policy – specifically deficit spending – changes the total amount of those obligations. Link- scroll down to 'How to needlessly produce inflation'.

{kind=link}

Banks extend 60 % of their lending to one third of already wealthy households to speculate in the residential property market because the RBNZ offers them an RWA capital reduction incentive, to do so. Which causes bank loan concentration risk.

{kind=link}

The creation of bank credit is the driver of household residential property price inflation.

Bank lending to housing rose from $50,788 million (48.36% of total lending) as of Jun 1998 to $295,957 million (60.02% of total lending) as of December 2020 - source.

Expressed another way...the real economy lacks the wherewithal to support the delusions of the finance sector.

Exactly:

But from the point of view of the bank, it has acquired the security without giving up any cash; the counterpart, in its balance-sheet, is an increase in its liabilities. There is expansion, from its point of view, on each side of its balance-sheet. But from the point of view of the rest of the economy, the bank has ‘created’ money. This is not to be denied. Hicks (1989, 58)

We start with the idea of credit creation, specifically a swap of IOUs between a bank and myself involving a bank loan that is my IOU and a bank deposit that is the bank’s IOU. Nothing could be simpler, and yet the mind rebels, especially the well-trained economist’s mind, because this simple operation increases my purchasing power without decreasing anyone else’s. It seems like alchemy, or anyway a violation of some deep conservation law. Real productive resources are the same as they were before, and the swap doesn’t change that, does it?

Spending of the new purchasing power adds another layer of perplexity. If spending increases but real resources do not, then it seems logical that the increased spending must exhaust itself in higher prices—that is the intuitive appeal of the quantity theory of money. My purchasing power may increase, but everyone else’s decreases because their money balances buy less. From this point of view, the alchemy of banking seems like a kind of theft, something to be deplored in the name of economic science and if possible outlawed in the name of the general good. Link

These newly created numbers on each side of the banks balance sheet, this is where 'money creation' occurs nowadays, yes?

Money is basically created into the economy when (a) Govt spends or (b) private banks lend money to customers (in exchange for IOUs of equal value). Govt spending is a fairly minor contributor - private banks add 9 to 10 times as much money into the economy. This Bank of England article is great at explaining most of it... https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creati…

Thanks. You know, I understand completely why banks and investors love this property bubble. But JA and GA - whats in it for them? They own one home each,hardly enough to justify the inaction. House price increases surely are a drain on the economy. Does someone just need to sit them down and explain?

What's in it for them - political popularity. Its a shallow (and short term) game. They're not really leaders at all (nor was John Key 'at the end of the day'). They're pursuing self interest (political popularity), while the average kiwi pursues self interest (rising house prices).

Well if this is what is truly popular then NZ deserves whatevers coming. I say that as a 6th generation kiwi

I agree - unfortunately most in NZ have no idea what its like when house prices fall significantly after something like this. Think lockdown was stressful - try being in negative equity on a house while people are losing jobs left right and centre and the bank is breathing down your neck (not me, but many in the firm I was working at in 2008-2009).

No idea compared to U.S

The problem is when the govt talk to the business community the lobbying is done by groups like Business NZ and the EMA.

Phil OReily and Kirk Hope , current and ex CEOs have both come from Westpac. The govt aren’t really talking to the business community, rather their lobbyist that has been hyjacked by the banks.

And they will paint a vision and story that suits the banks and big business. Considering how much money the banks have been making I’m pretty sure they want to keep the status quo.

Remember these organisations didn’t support the notion that we have underinvested in our manufacturing and real economy. But they do tell us that our PMI is great from time to time.

If we have a major downturn it’s not like everyone can get a shift at the local factory... they all closed down twenty years ago.

Yes we have a tech sector and a much more diverse economy today but without increasing house prices what would our economy be.

Could we have immigration at all if we had ten percent unemployment?

Maybe thats what scares the hell out of the pollies?

I do have one doubt here. Govt spending through issuing govt debt is only hoovering existing dollars in the system.

This can be from commercial banks who later flip the bonds back to the RBNZ which creates more reserves for the bank.

So this does not 'create' money. My understanding is that only lending to individuals and businesses 'creates' dollars resulting in monetary expansion which when it accelerates starts to show in inflation. Therefore I am merely expecting a blip in inflation as we come off a low based and money moves to parts of the economy that was starved of it during COVID.

The purchase of government bonds by the banking sector can add to deposits in a similar way to the extension of credit to businesses and households.[2] Banks have purchased some of the newly issued state government debt. In the first instance, those borrowed funds are held by the state governments as a deposit with a commercial bank until the funds are spent.[3] In addition, when the banking sector purchases state government debt in the secondary market from the private (non-bank) sector, it credits the deposit account of the seller to pay for the transaction. In both cases, new deposits are created. Deposits have risen in recent months, as banks' holdings of state government debt have increased and as state governments have issued debt (Graph D.3).

Banks' holdings of Australian Government Securities have also risen recently, alongside an increase in Australian Government borrowing, which has contributed to the rise in bank deposits. However, the process of deposit creation is slightly different when the banking sector purchases debt issued by the Australian Government, since the Reserve Bank is the banker for the Commonwealth of Australia. When the Australian Government borrows from the banking sector, it holds the borrowed funds as a deposit at the Reserve Bank until the funds are spent. As the Australian Government spends these funds in the economy, such as in the form of JobKeeper payments to businesses, it adds to deposits held by businesses and, subsequently, to deposits of the household sector through employees of those businesses. Link

Just last week one his One Roof podcast, "property expert" LOL, Ashley Church stated it was unusual for investors not to have interest only loans. It was rare for them to be paying principal I think he said. I guess he must be completely unaware of how 61% of the people he is representing are structuring their loans. Expert??

I actually agree with Orr that its not his job to "control house prices". It shouldn't be their mandate, particularly as so many factors are outside the RBNZ's control.

But it absolutely IS his job to ensure financial stability, and he is failing spectacularly at that job. 40% of lending with interest only terms? That would be a bad figure with normal interest rates. But with ultra low rates its is much much worse as it greatly increases the difference between P&I and IO.

This is shaping up to be our version of subprime.

I would say it’s much easier for them to control house prices than the price of a TV etc. I doubt interest rates would be this low and house prices so insanely high if they were required to keep house price inflation below 3%.

I'm a bit of a schadenfreude. Wouldn't mind seeing this whole thing collapse.

I don't know, sounds like you actually have everyone's long term best interests at heart if that's what you want.

Interest only loans will level the playing field for first home buyers.

First home buyers frequently lament about being priced out of the market do not understand how to get into the market unlike their investors counter parts. Part of the blame comes from the tardiness of the mind.

Interest only loans acts as a call option, futures or insurances. It guarantees the house price you will pay in the event should you decide to complete the transaction in the future. Entering a interest only loan agreement gives you the right to buy the house priced at today's market value and shield you against price inflation due to market forces for a fee. It is a proven and effective way to acquire an asset that is vulnerable to rapid upward valuation.

Curtailing interest only loans doesn't benefit FHB and instead penalise other market participants. Proponents of this kind of policies are either having a crab mentality or arithmetically challenged.

If people do genuinely care about FHB getting onto the ladder, they should instead encourage FHB to go the interest only route- that would level the playing fields for all market participants.

Happy house hunting!

CWBW.....I thought you were a chess player? Your post sounds like it comes more from a Chinese checkers player. LOL.

I'm sure you must be the reincarnation of TTP with the amount of spruiker tripe you dish out daily.

And you must be the reincarnation Prince Albert whose self obsession are caused by an undiagnosed medical condition.

Holy moly, FHB's should get interest only loans in the hope the future value of their asset is higher than the current value? And value is decided on the sale of that property right? What if it's lower? Or what if their asset value is defined as the price of similar assets sold in a similar area? Then they can easily be in negative equity as their asset is priced below what they paid for it. Negative equity affects banks balance sheets, so the banks start asking those FHB's to provide capital... which of course they don't have.

Your assumption is based on house prices always going up. Truly ponzi stuff.

Buying a house are meant for adults. Too scared? Don't buy.

Be a bit more condescending, that will definitely get more people to approve of your opinion.

You are essentially asking people who don't understand the complexities of the financial system, to be aware of all the risks of the financial system and to prepare for them. Because if a very large cohort of FHBs went interest only AND you wanted a stable financial system long term, you would need them to understand the risks and be prepared for the eventualities. As you are dealing with young people from lots of different fields, this is highly unlikely.

Hence why RBNZ has rules around what banks can and cannot do regarding lending, to support financial stability. Your idea would make the system incredibly fragile.

Still wont stop asset price inflation because the RBNZ are still printing money calling it QE which really is the biggest Ponzi scheme out there. Old Bernie Maddock would be impressed. Government cant stop spending so to keep the Ponzi scheme going just gotta keep on printing which will eventually create massive global inflation. Its quietly growing if you have notice prices certainly are decreasing they are increasing. So keep buying assts which produce income because these assets will be the fastest doubling in our history and Mr Orr and Mr Robinson wont be able to do a thing about. The fire is already out of control has been since 1971 when the dollar was taken off the gold standard creating a Fiat currency.

I really need you to describe how QE is 'printing money' - i.e. how it adds to the broad money supply. If you can give me a credible explanation, I will be forever in your debt (pun intended).

My understanding, and I don't claim to be any sort of expert at all, is that RBNZ can simply create money. They don't actually print it of course as it's all done electronically. In (over) simplistic terms, Mr Orr just edits the spreadsheet that contains the RBNZ bank balance. Then they use this money that they magically created to go buy bonds or whatever.

No doubt someone will correct me if I've got the wrong end of the stick.

Bank buys Government Bond (IOU). Government fritters bank's money away. RBNZ adds some zeroes to their bank account, and offers to give them their money back in exchange for the Bond.

Could the property bulls please jump onto this stuff comment section and cheer up the negative sentiment there?

https://www.stuff.co.nz/business/124438249/gale-force-economic-warning-…

I'm afraid my DGM personality disorder would only add fuel to the fire.

First comment I see:

I’m pretty sure a 1% rise can be offset by something as simple as getting a boarder or renting out a room. There’s always a way as long as there’s the will to find it.

Imagine what that'll do to rental demand.

it wont do anything - because that same person will also contact a friend who lives overseas and convince them to immigrate to new zealand - its all very simple you see - NZ is immune to all economic realities

IO

While disagreeing with you in the past, I have never considered myself a property bull but have previously seen upside to market direction.

However I am probably not able to console your dgm bent.

As I posted later part of last year, I do see the market cooling this year and as for 2017 expecting a turn end of summer.

Interesting, reading Tony Alexander’s Premium out today there was a note of a possible significant turn - for the first time since his survey started mid last year, a net number of REA are reporting more investors bringing properties to the market and also for the first time a decrease in investors looking to buy.

Always said that investors, whose consideration is the market, are more reactive to likely changes. Expect to see less investor activity and that will have less to do with LVRs (for which a majority isn’t a hinderance anyway) compared to the market sentiment.

I appreciate RBNZ expecting a cooling in the market but that seemed to be later in the year and after a period of continuing strong growth. I feel that it may be coming earlier than RBNZ expects especially as there is no longer the expected downside for interest rates. (Amazing that discussion relating to getting one’s head around negative rates has all but disappeared.)

Personally, not expecting a significant correction like you have previously posted, but rather a prolonged period of relatively flat prices - much like dairy land following a decade of strong growth pre GFC.

Has that cheered you up even a little?

How much impact do you think investor and speculator sentiment will have on the market once they think the peak has been reached? FOMO has caused a lot of people to jump in helping drive prices up. Do you think the same sentiment can help cause a shift down in the market when people want to start selling? I assume there'll be a lot of people that have bought property for the sole purpose of capital gain rather than having TD's. If those speculators think the peak is being reached there's the possibility of a lot of them wanting to sell to realise the paper gain. Considering the fast price gains in the market over the last 6 months or so I personally don't see it flattening once it turns. Especially if longer term rates start increasing. That's not something exuberant buyers have had to consider for quite some time.

Exactly FANGO is more powerful than FOMO when you are mortgaged up to the hilt

What does FANGO mean? Similar to FOPR?

Tony Alexander's 'premium'. My god.

The epitome of junk research.

Ooh! Ooh! I know this one.

The 'market' will correct itself.

Ooh! Ooh! I know this one.

The 'market' will correct itself.

Just another attempt to scare the wanna be FHB from joining the protected elite group of 'wealthiest', over leverage investor borrower. Once again NZ is not a nanny state, so leave the current binge the way it is.

All of this should have been forseeable when Mr Orr and his MPC colleagues decided to cut the OCR to record low levels and to reinforce a low interest rate structure via asset purchases! And then remove LVR safeguards. Utter recklessness on their part.

The first thing Orr should do is sell off the Govt bonds that he bought to artificially lower interest rates, let the cost of capital find it's TRUE price and watch house prices fall.

The blame thrown at Orr for this disaster is completely misplaced...he was appointed 2018.

This disaster has been building since the deregulation of the finance sector in the 80s and 90s and the real opportunity to correct presented by the GFC was ignored...Orr was handed a hospital pass and has consistently warned of the RBNZs inability to row against the international tide ...but no one listened.

We are getting the results of what we have voted for the past few decades...no one to blame but ourselves.

Which means he should have understood what he was stepping into when he took the job, and known that some correction was needed. Instead he continued BAU. It is possible it was at the government's direction, but as his role is to advise the Government, he should have had a view that there was an issue and said so, and this would be discoverable as a part of the RBNZ advice to Government. So he is culpable for as long as he has been silent or stated that there was no issue. He certainly knew there was public concern.

You may wish to review what the RBNZ role is...

"The Reserve Bank manages monetary policy to maintain price stability, promotes the maintenance of a sound and efficient financial system, and supplies New Zealand banknotes and coins"

They are not politicians, they dont write policy...their primary function is as stated....they (attempt) to ensure the financial system operates (as efficiently as possible)...that sort of precludes crashing it.

Note in your statement "...promotes the maintenance of a sound and efficient financial system...." Ask yourself how he does this? In part it will be applying the tools he has in his hands such as the OCR, and in part it would be through providing advice to the Government. The Government would consider his advice when formulating policy.

Just by looking at his management of the OCR in the face of what was happening, there is the very strong suggestion that he was wilfully ignorant of what was occurring and the impacts of the tools he could apply. 'Wilfully' because he would have had to just plain stupid to not know, especially as in 2019 when talking about stress testing the banks, he indicated a 50% correction of house prices was survivable by the banks. So in just that one statement he tells us he knows there is an issue, and pending crisis. In addition taking your statement; there was no price stability in housing, it was inflating out of control and had been doing so for a number of years, so he would have been unable to suggest that there was a sound and efficient financial system as it was being threatened by an unbalanced economy. So his head was so far in the sand he could be accused of being incompetent!

The RBNZ does not operate in a vacuum....interest rates are not determined solely by the domestic market, nor is QE.

We are an open trading economy with the free movement of capital and a persistent negative trade balance....all actions the RBNZ choose to take are constrained by these facts.

No he should shoulder plenty of blame. He neglects his mandate to ensure financial stability in the long term, for short term inflation/financial stability goals.

He only thinks of the short term need to avoid a deflationary spiral, but ignores the systemic risks he is building up in the system long term by encouraging massive accumulation of unsustainable debts.

He could have easily reduced interest rates without relaxing LVR. This would have increased peoples disposable incomes, without encouraging further high risk debt based speculation. He was lighting quick to remove LVR restrictions, but glacially slow to reintroduce them. Each time he encourages further high risk debt accumulation he staves off short term risk of a deflationary spiral, but makes the inevitable reckoning far far worse.

I fear you have a distorted sense of time....the past week should show you the relationship between short and long term goals.

In hindsight the removal of LVRs appears a mistake....it may have been, but IF it was, it was a mistake to the prudential side.

Nothing about the RBNZs job is easy especially when unconventional central bank actions are du jour in the worlds major economies AND when the second largest economy is what could be described as 'opaque.' at best.

I suspect their game plan is to hang on as long as possible and hope one of the major economies cracks first....maybe then we will face less scrutiny.

From the Financial Times appropriate advice

Changing regulation and reforming planning law is a more sensible way to address the deficiencies of the housing market than running a monetary policy that would not be justified by the inflation and unemployment data.

https://pointofordernz.wordpress.com/2021/03/05/financial-times-chips-i…

Interesting to note that when they bought in a DTI in the UK it applied only to owner-occupiers and not to buy-to-let (ie investor) purchasers.

So when Robertson tells you that they have this in the UK so we should have it as well, you can tell him the real story.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.