Rating agency Standard and Poor's has expressed concern about New Zealand's "shallow" debt markets and its lack of capacity to fully fund bank liabilities, which has forced banks to borrow around 30% of their funding from offshore.

It also labeled the country's economic imbalances as "high risk" because of "persistently high current account deficits, high external debt to current account receipts of about 200%, increasing level of private sector debt, and occasional periods of rapid growth in house and equity prices".

These heightened concerns could mean the creditworthiness of New Zealand's banking industry was more risky than it assumed last year, Standard and Poor's said. The ratings agency is currently "significantly" reassessing the way it calculates industry risk, placing greater emphasis on a country's economic imbalances.

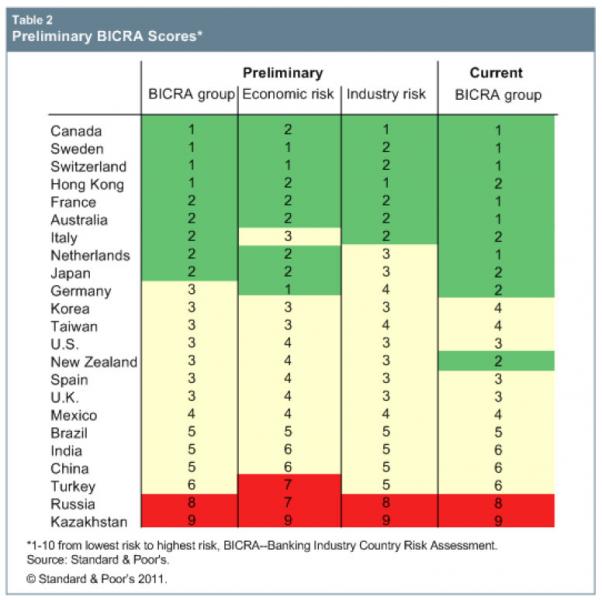

In a commentary piece on its methodology for how it calculates its monthly 'Banking Industry Country Risk Assessments (BICRAs), S&P released preliminary assessments for 23 countries, showing how its new methodology could produce different results from current assessments. It is seeking comment on the new methodology by early March. Changes would have "modest impact" on banks' credit ratings and could move ratings by one notch or more, S&P said.

Significant changes for excess credit growth, asset price bubbles and current account deficits

S&P said the report described "various significant changes" to its methodology and placed weight on "economic imbalances, such as excessive credit growth, asset price bubbles, and current account deficits; the degree of riskiness of certain banking products and practices; and the system wide funding profile of a country's banking industry".

"Under our proposed BICRA methodology, we treat growing imbalances during periods of economic expansion and limitations in a banking industry's systemwide funding profile as weaknesses, particularly when an economy and banking system are characterized by excessive growth in credit and significant net external borrowing," S&P said in the report.

In a BICRA scale of one for low risk, to ten for high risk, New Zealand's banking industry scored a two under current criteria, S&P said. However, the proposed criteria moved the country's BICRA out to three. The overall score was based on two sub-scores, economic risk and industry risk.

Economic imbalances "high risk"

New Zealand's preliminary economic risk score was four, S&P said in the report. "This score takes into account our view of New Zealand's economic stability and resilience as "low risk," its economic imbalances as “high risk," and credit risk in New Zealand's economy as "intermediate risk,"" S&P said.

"We consider that the strengths inherent in what we view as New Zealand's open, flexible, and well-developed economy, and its relatively high per capita GDP, partly offset the weaknesses associated with dependence on agricultural commodity exports," it said in the report.

"A stable, transparent policy environment, strong institutions, and sound public finances (foreign currency sovereign credit rating AA+/Negative/A-1+; local currency AAA/Stable/A-1+) also support New Zealand's economic stability. Independent monetary policy settings also allow New Zealand's external imbalances to adjust. We expect that the central bank will be successful in maintaining inflation within the 1%-3% annual average target range over the cycle.

"We assess New Zealand's economic imbalances as "high risk" because of its persistently high current account deficits, high external debt to current account receipts of about 200%, increasing level of private sector debt, and occasional periods of rapid growth in house and equity prices. These risks are, in our view, partly mitigated by effective hedging of external debt. We also note that FDI funds a sizable part of the current account deficit," S&P said.

'House price correction mitigated by strong labour market'

"In our opinion, the risk of house price correction is mitigated by a strong labor market, and by the modest recent rises in prices following the fall in house prices in 2008," S&P said in the report.

"We expect that credit and impairment losses and nonperforming loans will remain low, reflecting the conservative lending practices and legal and taxation frameworks that support creditors. In our view, these factors partly offset the high levels of private sector debt at about 150% of GDP and the concentration of lending to agricultural sector, including the dairy sector," it said.

'Gaps in regulation'

The preliminary score for the New Zealand banking sector's industry risk was three, S&P said in the report. "This score takes into account our view of New Zealand's institutional framework and competitive dynamics as "low risk," and our view of New Zealand's systemwide funding as "intermediate risk.""

"We view the banking regulation environment in New Zealand as conservative, transparent, and predictable, supporting a stable financial market. We note that in the recent years, the Reserve Bank of New Zealand has strengthened regulation and oversight, particularly for "systemically important" banks and the nonbanking sector," it said in the report.

"Nevertheless, we consider that regulation is still evolving for some parts of the financial sector, and there remain some gaps in coverage.

"New Zealand's banking industry is supported by what we view as good efficiency, limited use of predatory or aggressive commercial practices, and absence of distortions from government-owned banks. We believe that the probability of a material change in the competitive environment is low, and that the four large Australian-owned banks are likely to continue to dominate the New Zealand banking sector through their ownership of the majority of the sector's assets. At the same time, the pricing of loans and savings products at a number of nonbank financial institutions is aggressive, in our opinion," it said.

Shallow debt markets

New Zealand's debt markets are shallow and lack the capacity to fully fund bank liabilities, S&P said.

"New Zealand's banks consequently materially rely on offshore wholesale borrowings, which constitute approximately 30% of banks' total liabilities. The ratio of customer deposits to total funding is relatively low at about 30%. In our view, these weak points are partly offset by good currency risk hedging practices and the strong franchise of the major banks. While a number of nonbanking finance companies have failed in the past three years, bank failures or bank deposit runs have been extremely rare," it said.

Not in Borat country

New Zealand was one of seven of 23 countries whose preliminary BICRA score under the new methodology was three, alongside Germany, Korea, Taiwan, the US, Spain, and the UK. Leading the group of 23 was Canada, Sweden, Switzerland and Hong Kong, each with one; followed by France, Australia, Italy, the Netherlands and Japan on two.

Mexico scored four, while Brazil, India and China scored five. Bringing up the rear were Turkey with six, Russia with eight, and Kazakhstan on nine.

11 Comments

"In our opinion, the risk of house price correction is mitigated by a strong labor market, and by the modest recent rises in prices following the fall in house prices in 2008," S&P said in the report.

"We expect that credit and impairment losses and nonperforming loans will remain low, reflecting the conservative lending practices and legal and taxation frameworks that support creditors" S&P

And in the above statement you have the real reason why people must be determined to find their own pathway out of trouble. You must avoid mortgage debt and indeed any kind of debt. As a borrower you are being targeted not just by the banks but also by the govt and RB, both of them determined to keep the banks fat and safe from you not paying your interest each week.

The banks were neglegent and reckless for several years bloating these property bubbles which blight the economy today. The bubbles allow the banks to suck the wealth from the economy. The govt and RB are there to support the banks. They are not there to help you.

If you want help, you are expected to go to a bank and get a loan.

The economy is in or near recession level activity because the wealth is being sucked away. Savings where they exist, must go to clear mortgage debt. Savings cannot go into retail spend or export investment. It will take a long long time to clear the household debts and the banks will fight any such trend every step of the way with advertising aimed at porking property activity and pumping a new wave of capital gain greed, with the help of the govt and the RB.

This is why the govt will not bring in capital gain laws. It would remove a weapon from the hands of the banks. You must remain a viable target for increased lending.

Just where are they getting this information "strong labour market"!It beggars belief,unless they are comparing with the US.Its a common belief that the real % of unemployed/on benefit is around 10.4 in real terms.And like most things here,still trying to find out which bank had a run on deposits in 08-09!

Everyone is lying like bugger ian. It's being orchestrated for sure mate. Next up will be bank survey shite pointing to recovery and growth and the end of recessions in our time....doh

I see Mish is focusing on putative problems in the Aussie economy. He highlights the surge in property listings in Aus in 2010:

http://www.smartcompany.com.au/economy/20110110-44-jump-in-property-lis…

I imagine a fall in the Aussie housemarket might be bad for the Aussie/NZ banks?

S & P Track record .....

We should also remember S&P's recent track record in predicting anything.

Enron, Hanover Ireland RBS etc etc ...

These same dudes were rating absolute crap sub prime AAA not so long ago.

They are blessed with hindsight and that's about all.

Hi JB, have you read The Big Short?

Fantastic book, just makes you more angry with the ratings agencies every page you turn

Cheers

Alex

Wasn' the core funding ratio meant to slow down banks lending from overseas? it seems they have just carried on, but at longer terms.

Which is probably only marginally safer, but not really any safer for depositors as they are behind the covered bond holders in the queue if things go pear shaped.

Ah, it's all a conspiracy etc etc!

You are correct , muzza , in that every era in humanity uses scape-goats to excuse itself of being indolent , whilst others around it ( " them " ) , strive / succeed / and prosper .

Races such as the Jews , have been vilified for millennia , being thrifty , crafty , and successful .

Industrial classes such as the merchants , were despised through much of medieval Europe , despite the fact that their endeavours enriched whole nations .

And today ? .......... " Generations " is the latest conspiracy theory . The " war of the generations " as promulgated by our own Bernard Hickey , and many other financial journalistic hacks around the globe .

........... There are no " generations " ........ It is a figment . A convenient construct to pidgeon-hole groups of people , and then to sit in judgement upon their collective behaviour as a group .

You are full of shit , Bernard ! The generations do not exist . Merely many individual people , making a zillion individual decisions about their lives and their finances . ....... There is no " Generation Baby Boomer " , nor " Gen X " or " Gen Y " .........

....... they really don't exist . The generation vs generation " war " marlarkey , is pure fantasy ........... but hey , it sells newspapers , it gets air-time on TVNZ , and it keeps interest.co.nz ticking over ........... So I should shut the feck up , and let the circus roll on .......

This will make a few anal sphincters twitch.

You guys are too funny

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.