The Reserve Bank has softened its restrictions on bank lending to Auckland residential property investors a little in its final policy position.

The restrictions will now be introduced from November 1 rather than October 1, and banks will have a 5% speed limit, something they lobbied for, rather than a 2% speed limit. The Reserve Bank is also introducing an exemption for high loan-to-value-ratio (LVR) lending to finance leaky building remediation "and similar cases."

"As announced in May, the Reserve Bank is altering existing LVR rules to focus on rental property investors in the Auckland (Council) region. The alterations mean that borrowers will generally need a 30% deposit for a mortgage loan secured against Auckland rental property. The new rules will become effective on 1 November 2015. This is one month later than initially proposed, to enable banks to adapt their systems for the new rules," the Reserve Bank said.

"Restrictions on loans to owner occupiers in Auckland will continue to apply, with banks allowed to make up to 10% of their new mortgage lending to such borrowers with LVRs exceeding 80%."

"Restrictions outside Auckland are being eased after 1 November. Banks will be able to make up to 15% of their new mortgage lending to borrowers with LVRs exceeding 80%, regardless of whether the borrowers are owner occupiers or residential property investors," the Reserve Bank added.

The central bank and prudential regulator said it had "modified" its proposals in response to feedback about compliance challenges and special cases. Meanwhile, Deputy Governor Grant Spencer will expand on the Reserve Bank’s view of the property market in a speech on Monday.

'Little evidence NZ investors are riskier'

Responding to submissions, the Reserve Bank defended its decision to introduce restrictions on loans to investors, but acknowledged there's little local evidence investors are riskier than owner-occupiers.

"The Bank acknowledges that there is little New Zealand evidence that investors are riskier at any given LVR, but consider this to be a natural consequence of the housing market having had only mild downturns since the early 1990s. The absence of a severe housing market downturn in the last 20 years is not evidence that one could not occur," the Reserve Bank said.

"House prices have reached unprecedented levels relative to income in Auckland, so historical New Zealand downturns may not be a good guide to the consequences of a future severe downturn. This leads us to look at other countries that have had severe downturns. While (loan) origination practices in the US and Ireland differ from New Zealand in important ways, we still consider that the empirical evidence from those downturns is relevant to considering what would happen in a severe New Zealand downturn."

The Reserve Bank also said restrictions on lending to Auckland landlords are unlikely to dramatically change the landscape for Auckland house prices.

"However, we consider that the factors that make housing scarce at present may reverse in the future (e.g. supply may loosen, migration flows may reverse and interest rates are likely to increase from current low levels), and that this could lead to a different demand/supply balance and tighter origination practice."

'Placed in the most restrictive relevant category'

In terms of bank customers with mixed collateral such as an owner-occupied Auckland house plus Auckland rental properties, the Reserve Bank says bank treatment of such customers must see them "placed in the most restrictive relevant category."

"In our judgment this makes the restrictions easier to implement without greatly affecting the overall extent to which the policies constrain lending. By ensuring that all banks operate in the same way, there is a more level playing field and the data obtained will be easier to interpret," the Reserve Bank said.

Banks will have a six month first compliance period meaning they'll first be tested for compliance with the new rules at the end of April 2016. After this banks that lend less than $100 million per month will have a six month measurement period for their LVR restrictions, whilst the larger lenders will have a three month measurement period. Banks told the Reserve Bank the cost of upgrading their systems to implement the new LVR policy range from $0.25 million to $0.50 million for small banks to $1.2 million to $5 million for big banks.

The Reserve Bank also noted that some investors might be able to restructure their funding in order to reduce their LVRs below the 70% limit whilst still buying new properties. The regulator said, however, these investors will also tend to be more resilient in a severe downturn than those without additional equity sources, so the Reserve Bank doesn't see this greatly compromising the effectiveness of its policy.

"Something like 50% of Auckland investor loans are currently at LVRs above 70%," the Reserve Bank said.

RBNZ would like to 'potentially remove LVR restrictions outside Auckland'

Meanwhile, the case for LVR restrictions outside Auckland has "significantly diminished."

"The Reserve Bank would like to be able to ease these restrictions and potentially remove them completely in the future. In order to be able to achieve this, it is necessary to ask the banks to develop data systems so that they can rigorously identify the location of lending as well as the investor/owner-occupier status, which is also required for capital purposes," the Reserve Bank said.

It estimates this could cost $10 million across all the banks, but would allow mortgage credit to the Auckland market to be monitored much more closely than in the past.

"Given the divergence between the Auckland market and the rest of New Zealand, this has the potential to be useful in other contexts such as capital modelling, stress testing and internal bank decision making."

In terms of Auckland the Reserve Bank said the housing market has remained hot for longer than it expected when the initial LVR restrictions were introduced in 2013. (Here's a story I did in 2013 on how long the LVR restrictions might be in place for).

"So LVRs restrictions are likely to remain in place for longer than expected in 2013. We think the costs this imposes on prospective home purchasers are larger for owner occupiers than for investors, as investors have the option of buying outside of Auckland or buying a different sort of asset while prospective owner occupiers have to buy a home in the region they live."

Debt to income data not harmonised between banks

Once again, the Reserve Bank also weighed into potential alternative tools it could use rather than LVRs restrictions. It again described restrictions on debt to income as "administratively complex", noting the definition of borrower income isn't well standardised among banks whereas LVR is. It noted however, as Bernard Hodgetts, head of the Reserve Bank's macro-finance department told interest.co.nz in May, it has been working with banks to obtain standardised statistical data.

"But it is not clear the data is sufficiently harmonised to allow for prudential limits at this point."

Meanwhile, capital based tools such as sectoral overlays on housing risk weights would help to make banks more resilient in a downturn, but wouldn't materially affect lending practices unlike LVRs.

Banks will have 12 months from November 1 to reclassify existing lending to Auckland property investors.

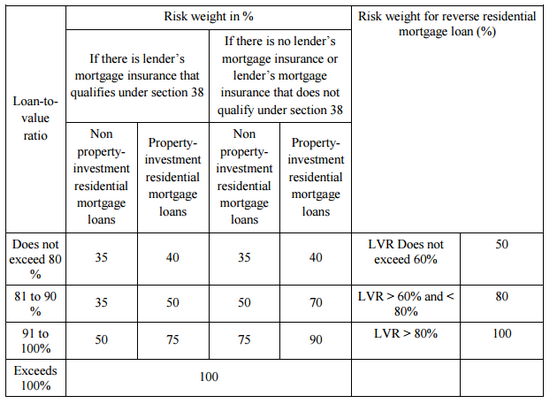

Reverse mortgage risk weights

The Reserve Bank also released a response to submissions on its plans to introduce specific bank capital rules for reverse mortgages. These plans had previously been put on ice. At the moment there are no explicit capital requirements for reverse mortgages with the Reserve Bank estimating banks hold between $400 million and $500 million worth of them.

"The Reserve Bank proposes to introduce an intermediate risk weighting category for reverse mortgages with LVRs between 61% and 80%," the Reserve Bank says.

Here's the Reserve Bank's summary of submissions on the LVR changes, and here's its paper of reverse mortgages.

85 Comments

You see.

A falling house price is NOT a friend to anyone in power in NZ.

That just means we need to change those who are in power.

It would be the same if you were in power.

You are not wrong and it's funded with other people's at risk deposit money.

"Restrictions on loans to owner occupiers in Auckland will continue to apply, with banks allowed to make up to 10% of their new mortgage lending to such borrowers with LVRs exceeding 80%."

How this policy trickles wealth down to the poor defeats me.

or even to the rest of the economy (which indirectly helps the poor)

Even with these slight adjustments, the RBNZ's measures are still too draconian. I don't think these landlord 'rules' will stick for very long. Keep your eye open for an article a few months from now moaning about rent increases in Auckland.

Landlords clearly aren't doing a very good job of keeping prices down with rent growth running at 3 times income growth in Auckland.

Lets see your cost analysis

“In Auckland, the median asking rent was $495 a week in July, unchanged from June but up 7.6% compared to July last year”

http://www.interest.co.nz/property/77155/rents-trade-me-property-flat-m…

Annual wage inflation at 1.6 per cent.

http://www.stats.govt.nz/browse_for_stats/income-and-work/employment_an…

7.6 % / 1.6 % = 4.75 X

.c.o.s.t. no wonder the wages are bad, the workers are idiots.

split that $495/wk down into the _landlords_costs_ and returns, see how much the _landlord_ is actually getting on their investment, make sure you budget for 2 weeks empty, cleaning, upgrades, repairs too.

You sell you labour right .. you walk away with what $9-$10 an hour in your pocket. lets see what yield the landlord is living their life of luxury off.

S.u.p.p.l.y and d.e.m.a.n.d.

Tell the farmers “cost” sets the prices.

Yields can be negative from what I hear, Property speculators are in it for capital gains anyway.

"Landlords clearly aren't doing a very good job of keeping prices down with rent growth running at 3 times income growth in Auckland."

poster claimed landlords not keeping price down.

landlords very much keeping rent and costs down.

external parties are not keeping costs down.

now stfu if you can't answer the question, re cost analysis

- or are you trying to claim "rates", or "insurance", or "repairs" etc; all the landlords costs, are "s.u.p.p.l.y.and.d.e.m.a.n.d. Once we strip out the costs, and we can see what the landlords share is, then we can start talking supply and demand.

Tenants housing costs are inflating 4.7 X faster than wage inflation is the real point.

Your cost argument in a speculative market is a red herring.

incorrect. do the math or stfu

Pity the poor landlords. If only there was a reputable charity I could donate to to support these poor unfortunates.

Oh, wait, I already am. Taxpayer-funded accommodation supplements.

those supplements go to government beneficiaries not landlords. If you can't even realise that, how can anything else you say have any value.

They go to landlords VIA the people govt have chosen to be the beneficiaries, Another govt could have chosen to make landlords do the applying and I reckon that is how it should be. It IS welfare for blasted landlords, whether you want to hide behind how it comes to you or not!

I say may as well abolish it seeing as how as a landlord I can conclusively say I have no need of that particular bit of welfare (assuming that it is for landlords). I mean if it isn't for the benefit of renters and the landlords don't care about it, then clearly we should abolish it, saving the government some money and leveling the playing field by depriving them greedy landlords of yet another of their benefits!

No they don't.

because it doesn't matter if the person is a beneficiary or not, the landlord is not permitted to discriminate the price on that basis; nor are they permitted to refuse a tenancy because the person is unemployed/beneficiary.

so the money goes to the beneficiary - what the beneficiary does is their business. got NOTHING to do with the landlord (exception Housing Corp). price is the same no matter what so it goes to bene.

I'll make it a point to get back to you on that. ie I dont believe for one instance landlords are not already charging the top dollar their tenants can pay.

do you believe in gravity too?

Unfortunately just because you believe it, doesn't make it true.

The problem here is that investors are now looking at the regions. To be blunt - Jaffas are welcome to come and live in the regions, but Jaffa investors just buying property are closely akin to an unwanted viral infection. they need to consider the markets. If they are buying to profit from capital gain, but through their paying inflated (in many cases significantly) prices they are pricing the property out of the range of most locals, and are then reliant on other investors coming in and seeing potential for more capital gain. They will have already shut out much of the market (Locals) meaning the market size for them to make their gains is seriously shrunk. A good solid business model? I wonder if the banks understand this? My perspective is probably not, just more suckers for the banks to get their hooks into. And again they are forcing rents beyond what most can afford.

If you think that you are paying too much for the place that you are renting then why not just move to a cheaper one?

If it is because other people are willing to pay a similar amount for all other dwellings of a similar standard then no one is forcing rents anywhere, it is just good old fashioned supply and demand at work :)

A cheaper one has to be available. Remember that there are many factors that identify if a home is suitable and rent is just one. I am becoming more convinced that there does need to be some form of rent control in place.

Plus Jaffas investing in the regions become the regions FHBs. The regions do NOT need the Auckland phenomenon exported to them!

If a cheaper one "has to be available" then why complain? Just move. I raise the rents when I percieve that there is still demand at the higher level, it is just economics.

Rent controls skew the market.

If you are a married couple with two children and the only homes affordable to you are single bedroom ones, why would you just move? The attitude you present - market economics - reflects the greed that is associated with property investors and the flaw in the economic model applied. The assumption of the model is that there are always alternatives for the customer to go to, in otherwords competition. In the Auckland property market (and elsewhere) the only competition is who is greediest, and there are many people out there who have neither the power to influence the market as individuals nor capability to make a choice into another environment, hence the auckland market being able to spiral out of control. Rent controls are a solution as the property investors have clearly demonstrated that they lack the morality, or the ethics to consider the victims of their greed.

Please explain why you think a married couple with two children are owed more that they can afford just because they want to live there.

Are they also owed a bigger car? Longer holidays?

Surely they should be expected to contribute more if they consider their needs are greater than others?

The assumption in the model is that if someone wants more (eg from their life circumstances) _no-one_else_owes_it_to_them_. thus if they want such nice things they either have to pay more, provide more, or expect less.

A roof over your head, especially if you have family is an absolute necessity. Having people denying it with a "go live in the streets if you can't afford to pay the rent on the house I outbid you on" is just gross and strengthens my belief the rentier class needs dealing to - pdq

sure its a necessity. so is food. don't pay your tax and rates and see how "necessary" the gov thinks they are.

Oh, I absolutely fine with folks like yourself personally meeting the shortfall, if that's the way you believe.

My experience, having been on the street without said roof over my head; is that I do not owe the roof I struggled to have to anyone else. Also your charity can also be misinforming and market deforming - and worst of all it can be enabling - why just yesterday I was talking to a young, thin, classically attractive woman - she claims she is a "free spirit". Never had a job (30yrs old), thinks the system is totally corrupt and enslaving, and can't understand why everyone else works for a living as she prefers travelling, which she usually does with a boyfriend.

The thing which is gross, is that there is no lower end lifestyle/living conditions, due to government "job creation" through certifications and bureaucracy of standards, puts the price of reach for those on low income. shifts the market up

he was saying a cheaper one has to be available to make the market idea work. (which is incorrect).

at a certain point demand for scarce resources means competition pushes up price - just because something is wanted or even needed does not mean everyone is going to be graced with the ability to pay - ask anyone with a sick relative or friend, or whose been through their own business failure. sometimes wanting and working hard aren't enough to keep up. Question is how reasonable is it for the public to give a damn ... and how much should government and politicians personally profit while destroying that ability for people?

I suppose that I wouldn't be opposed to rents being pegged to prevailing retail interest rates. For example if the average floating interest rates across our 4 largest banks are 5% then rents get pegged to 5% of the value of the property on the market.

Do we peg groceries too?

Groceries don't need to be pegged as they are sold in a (relatively) free market. You can even grow your own in your garden.

Try building a home in your garden and you will see how free the market is.

It's a government controlled market, through land control. They exert artificial constraints on supply forcing prices up, supporting those they represent (corporate interests, wealthy baby boomers). If they were to represent the masses, they would implement controls forcing prices down.

You started off so well... and then stuff up at the end.

Why would they impliment all those cost adding controls (land control, artificial supply pressure). supporting those they represent the WFF, the government employees, the cost-and bureaucracy adding "job creations". Then turn around and put rent controls on that make the whole "job creation" mess unworkable...where do you think the magic money comes from to pay for everything that makes houses happen??

That's why you can't have mob control for government - if the mob believes they're all entitled, then who's the mug that gets to do the supplying (with controlled, below breakeven or below Term Deposit, , EBIT ). Who? and before you say "magical government" - think - they're the very people you've just accused of corruptly running the existing system ! You think will -more- power and -more- control they're going to do better? You think those who can't even work the existing system, are going to come up with a better solution when they can't even identify the basic needs now (and form their own working collective - do their own developments).

WHERE are you going to force down??

force rates down?? is that the landlords costs you're going to reduce when the prices come down?

or is insurance, especially with earthwuake issues and re-insurance pass on costs, is that going to go down?

Are the repairs for the tenants breakages and messes left behind going to be cheaper - most landlords do that labour for free or pay contractors by direct disbursement?

Are the upgrades going to get cheaper. are there going to be less call for fire alarms, insulation, paint, roofs, stoves, heat pumps?

Good agents are worth their weight in gold and actually operate quite cheaply, why would their services get cheaper?

Do you think interest rates are going to get cheaper? Can you guarantee it?

you want to "force prices down".... the landlord is making between 2 - 5% on full market price GROSS.

The landlord probably makes about 10-15% of gross revenue BEFORE TAX.

Have you seen to wins in "rent control areas"?? We are in the Internet world, look them up. Look at the housing, the communities. This is not a coincidence - who wins in rent control land? The big company who can spread costs across a hundred or thousands of tenancies - like a bank does with its defaults. So how do they get ahead? Because they do lousy maintenance, don't respond to calls, lose paperwork, use in-house "cheap" (enforced cheap budget) repairs and work. Because that's the only way to have economic viability or sustainability under rent control !!

Stop thinking with your f...ing entitlement. Use your brain kiwi. do the maths.

And some places like Auckland people have big career incomes, they don't need or want rent control - they're happy and have the income to pay for fancy places.

It's only self-entitled morons who would think that just because someone else [on a big income] lives there that means everyone should be able to live in the same place with the same privileges and you have a dumbass government who will tax your stupid asses to the hilt so they can pay you off to do so , and keep you voting and paying them.

I am guilty of over simplification, but when the only other alternative amounts to an effective tent how is that the markets working? Remember that the market is a societal phenomenon that is supposed to serve society, not just those who control an essential product. When it fails to address the needs of that society because greed prices the commodity beyond the reach of most in that society, how then is redress achieved? Is it that only the few who can afford it are entitled to a roof over their head? Why should land lords get rich from the public purse by forcing their tenants to go to WINZ for an accommodation top up? There is much here that doesn't belong in a society that I would be proud of.

" Remember that the market is a societal phenomenon that is supposed to serve society,"

hahahhahahahaha

NO. The Market is a place where potential buyers and sellers meet. If a buyers needs one thing more than they value what they have...and the seller values what they offer more than they value what they are willing to part with then they trade. That is a market.

Saying it's a "society phenomena to serve society" is like saying "God X exists because in a truly perfect world God X would have to present for it to be perfect".

And YES only those who can put a roof over their head deserve a roof over their head!!

Unless they can con some other fool into doing the work for them (which if they succeed, means they have succeeded in "putting a roof over their head".

Landlords aren't getting rich from the public purse.

Landlords are NOT forcing their tenants to go to WINZ or anywhere else, that is entirely up to the tenants...like many landlords, I'd rather they didn't go to WINZ, didn't create a social market for the government to pay its people money, to take more money off me, to give to people to pay me. I'd much rather they just go bid on the market like everyone else, find places they can afford, and hold the government accountable for the economic stress !

WE'RE NOT HERE TO MAKE A SOCIETY FOR *YOU* TO BE PROUD OF.

If you wish that service from us, we will have to discuss contractual terms and obligations ! (hint: if you really want it , it's not going to be cheap !! demand and supply and all that. )

ps redress assumes something is owed. life and nature don't owe them, or me, anything.

Sure, the government has had nothing to do with allocating who has property and who does not? How legitimate is it that the State grants some few people with 1,000s of hectares of land, while the majority have none? Please tell me how you would become a landlord without a State investing you with your land title under the Torrens land registry system? Capitalists are absolute hypocrites,most especially "libertarian" land owning capitalists.

And how much would your precious property be worth without State built roads, State built telecomunications infrastructure, State built sewage and water utilities, State built electricity supply, and State built schools. Bugger all, that's how much.

come and break into my property and find out :)

My property would be very precious without State built roads, State built telecommunications, State built sewerage & water utilities, State electricity, State schools. Because all of that can be done better, more effectively and more efficiently by private means, and is frequently done.

Why you would be just as well off to say what would I have done without Church to guide roads, Church to set up communications, Church to order sewerage and water rights, Church to control lighting and heating, Church built schools, Church to mandate the values in your life.

not libertarian, Anarkist...

Sad to hear that you think you need a State to run and make those things happen for you. Would have thought you more gifted in thinking and working collectively than that.

I meant in MONETARY terms. This is the very basis of our debate. How much landlords can charge their tenants. If people could build their own homes they wouldn't need to rent from you, would they? Whether or not you identify yourself as a libertarian, your comments bear all the hallmarks of "libertarian" dogma.

"Because all of that can be done better, more effectively and more efficiently by private means, and is frequently done."

Do tell Cowboy. Pray tell me where in the world public utilities infrastructure has been built by the private sector without massive land grants and eminent domain, if not direct State financing. And I'm not talking about a corporation, which began as State Owned Enterprise until privatized by corrupt neoliberal charlatans.

"Sad to hear that you think you need a State to run and make those things happen for you. Would have thought you more gifted in thinking and working collectively than that."

Sorry I thought we were talking about the real world, not some hypothetical libertarian fantasy land.

How much can landlords charge? as much as they like...because they have to find a point _with_the_property_they_are_personally_responsible_for_ where it's not getting rented out or it is getting rented out. It's their call. Ask instead what is the _least_ a landlord can be charging, how much should they expect to support their business and labour?

I am not a libertarian. And in the cases of those things you've identified if it sounds libertarian perhaps it is that on that one thing the libertarians might have a point - they don't but for the same reasons you don't have a point.

Ask instead _why_ should the State provide some of those services.

Because it's not about money (trade).

Do you not see the intrinsic difference in service between a School and a Road?

the former should be private now we're not a bootstrap colony, the later is often done privately by developers at high cost but when might it be most appropriate for a neutral third party to own the asset. Similar to the electrical grid, or core communications...except those two were take _off_ the State owned and operated list because the State did such a terrible job of running them to a commercial level - expensive, slow to respond, chasing political goals, poor upgrade, poor pricing to clear project debt, poor implementation of technology not to mention _never_ (pretty much by defintion!) leading technology..... Am I a critic of State run business? Lets re-ask some of those Landcorp questions. And then we can move onto Bridgecorp and Solidenergy.

Do you even understand where most of the Infrastructure in the US came from?

Not State owned.

Real world huh. Place where you're not smart enough to see the value of personal freedom. To recognise the critical importance of correctly acknowledging costs as they enter the market.

Perhaps you should read more Marx Anakist, look harder for the things he mist.

I thought you had to have a job before the government can tax one's income and then transfer it to someone else. Weren't you unemployed and now studying cowboy?

yes indeed I am, and also have income (I'm currently on leave using 6 years accural of State enforced annual leave) and a small amount of passive income and making a few dollars a week off my FX.

I don't wish that service from you. As other commenters have stated you show the extremes of capitalist hypocrisy. Wages in Auckland are no better than any where else in the country and if you're only earning $700 a week, how is $450+ for rent affordable. Get a better paying job? How and where? What do you pay your employees?

Everyone is entitled to a roof, if you can get a job, even better but that roof has to be affordable - Rent controls!

Everyone can afford a roof, even on the dole. What they can't afford is a roof in any arbitrary pace that they feel entitled to live. Auckland is in high demand therefore the prices in Auckland are higher. Pick a cheaper city if you want to pay less rent!

You have to be able to get a job there to move! Most employers would be much better off if they moved to the regions, their infrastructure costs would be less, their employees would have a better living standard and less stress. And no everyone can't necessarily afford a roof. Many go to WINZ for an accommodation top up which goes straight to the greedy LL. How many properties do you own that are rented by individuals needing a top up? You'll know because you will have had to provide a letter to WINZ. Tell me again why the tax payer should subsidise your greed?

At the minute none of my tenants get a WINZ top up as far as I'm aware, but some of my property is now managed by rental agents who would probably deal with such things on my behalf. All my properties are at this time making a loss and I don't ever intend on selling any of them (precluding the capital gains argument). My goal is to retire once I reach about 30 and property is simply a way to ensure a passive income once I do retire, so that I don't end up being a burden on the taxpayer.

That is the sort of delusion doesn't forebode well. Not a burden to the taxpayer, give me a break. There are only two types of work sadr001, that where you produce something and that in which you don't. A landlord is just another type of beneficiary, or burden, to those who do real work.

oh rubbish.

And what do you expect to do with all those non-workers? supposedly who didn't save and not consume the results of their labours.

Does the landlord do less than the CEO of a corporation? At least the landlord takes all the risk themselves.

you dont get to make the call on my private business re:rent control. Go control petrol/oil prices instead - logistics is a key price point and food gets bigger margin than rent.

You provide homes yourself if you truly believe in lower rent prices - btw, yes, been there done that too. Now I dont do it any more - because I -know-, I have had the experiences, now I have the knowledge.

if $450 is the local rent, and you can't afford it. either buy local, or ... move.

Clearly there is enough demand and people _are_ paying those prices, therefore by ALL the rules of fair trade, many people consider that a fair deal. If they didn't they won't entry into the trade, until the price dropped.

Proof of "Everyone is entitled to a roof" sits on you murray. I said no. I gave proof of why that is the case. Prove your claim or stop making it. Or is it religion, and you reject the science of the matter. Since now you not merely -claim- that "everyone is entitled to a roof" but "that roof _must_ be affordable"!!

If they skew the market so that the ranks of landlords are thinned then skew away, baby

you do understand that lower landlord numbers, with same housing stock == higher rents, right (less competition, more high end dominance)

Fewer landlords pushing house prices up. more people able to own their own homes, less demand for rentals, rents go down, end of landlording as something to aspire to.

you folks got to do the maths.

it's not going to be "more people owning their own home" unless the price of ownership drops.

Since it's already one group for one dwelling changing the nature of ownership for that dwelling doesn't change the the demand for rentals, as the pool of available rentals shrinks as fast, if not faster (many women homeowner who flat would refuse to share their own home, certain in the numbers currently flatting), than the pool of renters. thus demand is is steady or rising. Thinking that changing the ownership states effects the pool positively, that's politician level thinking.

All you're doing is handing the renting business to smaller, larger, less competing, group of landlords.

You're right landlording (what were the benefits again?) will no longer be something to "aspire" to, it will now be solely the domain of corporate entities with shareholder funding, dividends and heirarchial salaries to pay, and no way for everyday New Zealand normal people to enter and compete in; nowhere for human compassion, only corporate policy which works out so well in all other industries doesn't it................................................ Do The Maths.

rent controls = landlords keeping properties empty because the "wear and tear" on the property is higher than the benefit gained from renting. While the land lord did buy to rent rent controls would justify them holding property for capital gains even though that was never their original intention.

"Rent controls skew the market"

ditto

Accomodation supplements (the tax payer fuded landlord subsidy) skews the markets.

So abolish the accommodation supplement and reduce taxes accordingly? Not sure how well that would go down with most people but I personally would be apathetic to that change (as far as finances are concerned, morally I'd be somewhat squeamish because that policy would disadvantage the poorest in favor of the middle class.)

Likewise. wont make much difference to market, its those working and struggling who will be hit. AFIK none of my tenants on it anyway....

Just move eh, find another exhorbitant week's rent to go straight into the rental agencies pocket as commission another cough up of a bond, another cost of moving all your gear. You know what, I am sick of the greedies who think their ability to invest is more important than others being able to have a home of their choice, that they can call their own. Change is on the way.

Sure it's got nothing to do with the Reserve Bank and both local and national governments rigging the system for the benefit of the nascent landlording class.

landlords aren't making anything out of it. Think you might mean the banking clans.

Then why bother doing it, get out of the market, let houses again be owned by the people living in them, as it should be and go put your money into something more lucrative, like a legitimate business

What legitimate business? I'm in a legitimate business servicing a need required by the customers at a fair price. Do you know what is involved, actually -really- involved in a start-up? You know without an existing income, or boyfriend/husband/family backing it/you (eg giving you a roof over your head).

What got me into farming when I had no money? I had solid assets to use as security for the loans to start my "legitimate business", and just enough cashflow to run the vehicle after house bills were paid. What you don't know is I started doing FX so I could get $50/day extra money so I could hire a relief milker.

I'm not putting people out of houses. I paid fair price for these properties - all on retail sales. No mortgagee purchases, or backdoor network; no mum or dad saying "at least take a few houses so you've got money".

And I am looking at putting money into higher return operations.

You are, _of_course_, aware that no sizable investor has had a growing portfolio without some low return "core/nest investment". Right - you are familiar with basic strategies of investment and business...

But if I'm looking for higher return opportunities, they've got to pass the risk test.

In you start-up how far out on the limb was it for you to hire employees, R&D to market a product?

Remember we're not talking "having money stashed from last job/inheritance/family support". the money in those houses is "it" (apart from FX which can't be relied on)

--

"d both local and national governments rigging the system for the benefit of the nascent landlording class."

and we're talking the rigging of the system, remember.

Here's who gets stuff out of it - overpaid papershufflers.

If I want to clean my driveway, because it has a bunch of dirt and grass (a friend's driveway actually).

Then I could manually do it, or I could hire manual labour to do it for me.

If I'm lazy I might do that anyway.

But if I'm a papershuffler who gets $25/hr to fill out reports then if manual labour is $17/hr I'm going to be off to shuffle more paper, make more reports, clock up hours "sexing up" my reports and pay the cheaper people to do the real value add.

But give it some more thought: who is going to have the nice houses and spare disposable income?

The manual labour on $17/hr doing productive work, who probably don't feel like spending all their off time doing more labouring work for free - but it's not affordable for them to pay someone else?

Or are all the useless overpaid papershufflers going to have the presentable expensive houses full of other peoples' labour, and since they don't have to do the manual stuff, and have disposable income, they have pleasant choices in their life.

So you tell me who's benefiting from the "creating bureaucratic jobs" business?

It's not the pittance yield going to the landlords, especially those homing the cheap labourers!!

Renting houses back to people you managed to outbid for is not a legitimate business in my eye, too many people now unable to house themselves properly because of it, and serious measures must be taken soon to stop it in its tracks. The culture of this country where housing goes has changed dramatically, very much for the worse

(1) My tenants aren't bidding on these properties and neither are any other owner-occupiers willing to pay the open market price.

(2) every other "legitimate" business involves buying the materials, equipment and staff, and then on-selling to public demand.

that -is- what business -is-, kiwi person. What do you think business is about??

one person purchases at market, does their thing, sells to customers unable or unable to do it themselves.

There is no entitlement, kiwi.

Landlords have no secret gold, Farmers don't get given farms to their families, Business Owners aren't a divine class of privilege bestowed by angels. We all got circumstances, we're all out there on the same mucked up uneven playing field.

the only changes that are happening in housing are (1) Bigger companies provide flasher materials giving faster build times (thus less labour return), (2) tools allow specialists to leverage their time considerably but this means they get through the job-equity-reserve faster this was noted even by Adam Smith that a specialist needed more population so a machine enhanced one needs even more, (3) Your government has a policy of "job creation" that creates cost-add bureaucrats that get paid more than the people doing the labour and a *lot* more than the landlords passive investment return.

thus to exist a landlord needs more to get buy, but house building can keep up with build growth. but the cost-add gets passed to the landlord and has no limits on it !!!

That's why I keep saying "do the maths". The council put in a road or a shopping center, so the property values go up - so the rates go up (a) from council legacy spending + (b) new spending + (c) raising council internal costs. That and all the other costs must be passed on.

that's why I keep saying about cost of compliance/bureaucracy.

Once you take your rent, and take out the council, take out the insurance, take out the regional council, take out a portion for repairs, take out a portion for upgrades, take out the interest on a 50% LVR, there is bugger all left for the landlords - so it's not the landlord gouging or pushing people off.... it's all those costs that the landlord has to pass on.

this government wants to spread the pain beyond auckland so everybody shares, just thank your lucky stars you are not getting the traffic congestion to go with it

..you mean not yet!

This Government is rapidly losing it's credibility on many many fronts. An astute politician with influence and control in any of the other parties (or several of them) could have a significant impact in the next election.

As evidenced by national gaining over 7% in the latest roy morgan polls? They are now at just over 50.4% on their own!

that poll was only 900 people the margin of error would have been huge. i would take it with a grain of salt

The power of the powerful

The powerlessness of the powerless

The banks lobbyist the Bankers Assocociation lobbies the RBNZ and gets both a delay in implementation and an increase in the speed limit

The central bank and prudential regulator said it had "modified" its proposals in response to feedback about compliance challenges

The banks have had two years to bring their systems up to scratch. They are so profitable they have enough financial muscle they could have thrown everything plus the kitchen sink at it and got to the finish line 6 months ago - if not earlier

Noone will do anything to fix it. It is pathetic how they pretend that they are 'doing something' - another red herring. LVR was a joke, all the rules are in favour of overseas buyers and investors...

low interest rates are a remedy for the economy but are also spreading the disease. (bubbleitis) :)

low interest rates lead to investment of capital in low risk investments i.e property.

higher interest rates would have the capital investing in higher risk investments to get a greater return.

Actually one would think the opposite to be true. I would imagine low interest rates would drive those seeking higher returns than those offered by conventional investments would seek high risk financial instruments which offer a correspondingly higher risk premium.

Funnily enough people do seem to behave opposite to the rational course, such as the dumb greedy fools who invested in high risk finance company debt when the banks were offering historically high interest on bank deposits (2006-2008)

No, I dont agree here, low rates tend to make investment in poor returning undertakings worth while. What we see is investment in property because of the significant gains expected. Frankly even if the OCR was 7% with 10~20% return possible the OCR makes no difference with that sort of margin.

Some proof, look at the junk bond market, or shale oil, huge investments happening in there to get a high return.

It would be good if the rbnz and the banks turned their focus to business, grow something useful for the masses, not the few. Capital gains in property don't create jobs or a future.

This is really the job of the Govn not the RB or banks. Banks are a business their one and only interest is to make a profit for the shareholders. RB is there for bank stability which is a good single focus for it IMHO. So really its up to us the voter to vote in a Govn that will grow something useful for all and not a profit for a few.

for the voter to vote in such a government, there needs to be a party that has that policy as is capable of delivering (without having other freaky agendas/hangers on)

agree a classic example is the gaming industry, we have a few in NZ but they don't get any government support with spending on training or R&D funding because they fall outside the box.

they are a future industry that staff get paid well so we should be encouraging it

why should the government throw public money at a particular industry when they're likely to generate returns on their own in any case? What happened to government shouldn't be picking winners? Better to create a level playing field for all rather than capitalists pocketing profits at the public expense.

Landlords, poor souls, do not make a loss for any other reason than they fondly believe that they have a property of a certain market value and want a return. If the landlord is geared up, that is his problem.

For example an immediate drop of say 30% in the market would make absolutely no change in the rent charged. Ungeared and geared owners would feel nothing until competitors who had bought under the new market conditions began to charge lower rents that their cheaper cost price would allow. Only geared owners would feel pressure and that would be lender demands.

In the end, Mister Market owes you nothing!

One thing that landlord does feel is pressure on expenses from what outsiders ignorantly think is a free money setup and that somehow being a landlord is a world of wealth; and thus price and require stuff involving landlords and property _as_if_ they had lots of money. Just learnt to day that there is now a metal fitting plate that must be fitted for stud penetrations, something more to add to costs.

Why then are landlords rich?

Not many of them are - however for those doing well, their home is freehold and they don't pay significant non-deductible interest for living in their own home. It's not that they have huge outgoings, it's just in NZ they don't have large outgoings. The money they're NOT having to pay is therefore not-taxed - ie if they need $220 a week in rent, that's $315 of gross wages they don't have to part with.

Why are many landlords rich asians or old white people? because it takes wither good contacts with cheap money OR a long time to pay off that home, and get in a position to get a rental !! Young folk have other priorities and many other cultures/poor white people believe other people owe them somewhere to live/or that money is someone elses problem thus never put in the many years of sacrifice and focus required to own the first home early. I started working towards landlording at about 15yrs old.

Impressive :) . It is my personal opinion that almost any NZ student who has the option to live at home rent free during their tertiary education has the resources available to them to own property by the time they are 21. Simply draw the "student loan living expenses & course related costs" save them / dump them into kiwisaver and use that to buy within a year of graduation.

I know that it can be done because I did it and a few others whom I know have done it. All of us were from lower / middle income families ( parents made less than $80,000 a year between them).

To anyone who does this, my advise would be to get a rental agency to manage your first few properties, because you are very likely to mess it up if you do it on your own! ( You'll be surprised at what some tenants are capable of!)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.