By Bernard Hickey

The Reserve Bank surprised markets and economists today by cutting the Official Cash Rate by 25 basis points to 2.25% and forecasting another cut by the middle of the year.

The New Zealand dollar immediately sank by more than 1 US cent to 66.4 USc and by almost 2 Australian cents to 88.8c after the decision, which only two out of 17 bank economists had predicted. Financial markets had priced in only a 30% chance of a cut today and the surprise move was criticised by some as indicative of poor communications by the bank in a speech on February 3.

ASB Chief Economist Nick Tuffley said he gave the Reserve Bank a bouquet for cutting, but a brickbat for the reversal since the February speech.

"Back then the Governor essentially implied that people forecasting OCR cuts were responding mechanistically to low headline inflation and he heavily emphasised the flexibility of the inflation target," ASB Chief Economist Nick Tuffley said.

"In the 5 weeks since then, the only material shift has been the various inflation expectations measures. Moreover, the tone of that speech suggested the RBNZ was a long way from contemplating an OCR cut, and will have contributed to the extent of market surprise today," he said.

Citing a weaker global growth and inflation outlook, the Reserve Bank said it was concerned about the risk that falling inflation expectations in New Zealand became a self-fulfilling prophecy that drove future inflation even further below its 1-3% target range.

“Monetary policy will continue to be accommodative,” Governor Graeme Wheeler said.

“Further policy easing may be required to ensure that future average inflation settles near the middle of the target range,” he said, adding the bank would continue to watch the emerging flow of data.

He later confirmed that the Reserve Bank's forecast for the 90 day bill rate to fall to 2.1% by the June quarter indicated the Reserve Bank was expecting to have to cut the OCR one more time. The timing of the forecasts suggest another cut when the Reserve Bank releases its next Monetary Policy Statement on June 9.

The cut also surprised those who read a speech Wheeler gave in early February, where he said the bank would not make ‘mechanistic’ cuts to interest rates in response to inflation being below the bank’s target range, which was interpreted as making an early rate cut unlikely. Although, since the speech inflation expectations and dairy prices have fallen.

None of the big four banks expected a cut, although Kiwibank and Royal Bank of Canada had forecast a cut. ASB, Westpac and ANZ had forecast 50 basis points of cuts later in the year, while BNZ had expected not cuts. ANZ changed its view to seeing two more cuts to 1.75% by the end of 2016 after the surprise decision.

'Challenges for dairy sector'

Wheeler said the outlook for global growth had weakened since the Reserve Bank’s December Monetary Policy Statement due to weaker growth in China and other developed markets.

“This is despite extraordinary monetary accommodation, and further declines in interest rates in several countries. Financial market volatility has increased, reflected in higher credit spreads. Commodity prices remain low,” Wheeler said.

He also noted the domestic dairy sector faced challenges, but local economic growth was supported by strong inward migration, tourism, a pipeline of construction activity and low interest rates.

Wheeler pointed directly to the New Zealand dollar being 5% higher on a trade weighted basis than the Reserve Bank forecast in December, “and a decline would be appropriate given the weakness in export prices.”

'Auckland house price inflation moderating'

Wheeler also pointed to a moderation of house price inflation Auckland, “but house prices remain at high levels and additional housing supply is needed.”

“Housing market pressures have been building in some other regions,” he added.

Later in the news conference, Wheeler said the bank was watching the risks that further rate cuts could further inflate house prices in Auckland, but he said the Reserve Bank was not considering any further macro-prudential policy measures (similar to its two rounds of LVR restrictions) 'at this point.'

He also later said Auckland was still not building enough housing. Asked about political pressures on the Auckland Council to stop intensification of housing close to the CBD, he said: "Auckland needs more houses. It's up to Auckland's citizens and their Council to try and work this out."

'Inflation expectation concerns'

Wheeler said the main risks to the Reserve Bank’s forecasts were around growth in China, global financial markets, weakness in the dairy sector, a further fall in inflation expectations, continued high net migration and pressures in the housing market.

“While long-run inflation expectations are well-anchored at 2 percent, there has been a material decline in a range of inflation expectations measures,” Wheeler said in a departure from previous statements which have not emphasised inflation expectations.

“This is a concern because it increases the risk that the decline in expectations becomes self-fulfilling and subdues future inflation outcomes,” he said.

The bank forecast headline inflation would not rise back into the 1-3% band until the December quarter of 2016, having been below 1% for two years. The bank does not expect inflation to reach the mid-point of the range until the March quarter of 2018.

The bank said in its full March quarter Monetary Policy Statement that low headline inflation had contributed to falls in measures of inflation expectations. It included a special Box D (page 28) on inflation expectations to reflect its increased focus on the issue.

“A fall in expectations is concerning, because it will dampen wage and price setting behaviour over the time horizon relevant for monetary policy,” it said.

The Reserve Bank included its view that inflation expectations would remain anchored at 2% as one of its key judgements in setting the OCR, alongside modest trading partner growth, net migration adding 3.3% to the working age population and moderate house price inflation.

“If things unfold differently, the bank will revise its projection for monetary policy settings to ensure medium term stability is maintained.”

Economist reaction

ANZ Chief Economist Cameron Bagrie called the cut a clear surprise in a note titled 'Action Man', which also included a reference to a 'mechanistic' further cut in the OCR around the middle of the year.

"The recent shift down in inflation expectations does appear to have spooked the RBNZ somewhat," Bagrie said.

Bagrie said he now expected two more rate cuts before the end of 2016.

"Recent pressure on (bank) funding costs is not really a core part of the RBNZ’s central track (of one cut today and another down the track), but it was discussed as a scenario (and would involve an OCR well below 2%)," Bagrie said.

"Given recent funding pressures, and our view that more downside risks around the globe will materialise as the year progresses, we expect more than one cut before year end," he said, adding he saw the second cut to 1.75% late in 2016.

Westpac Chief Economist Dominick Stephens said he had wound back an initial prediction in January of a cut today because of Wheeler's February speech.

"Back in January we were actually forecasting that the RBNZ would cut at today's meeting. But then the RBNZ Governor gave a speech cautioning against focussing excessively on headline inflation. The strong language in that speech seemed to pour water on the idea of an imminent OCR cut," Stephens said.

"We became very uncertain about the timing of cuts, but in the end felt it was more likely that the RBNZ would hold off before actually moving. Not so - the Reserve Bank instead chose to move immediately," he said.

First NZ Economics and Strategy Director Chris Green said he expected one more cut at the June 9 meeting with the risks now "clearly skewed" towards a further cut to 1.75% later in the year.

NZIER Senior Economist Christina Leung said the Reserve Bank had proved NZIER wrong by cutting.

"In hindsight we took too much from Governor Wheeler’s speech in February that highlighted the many factors besides consumer price inflation, including asset prices, the Reserve Bank is required to take into account under its Policy Targets Agreement," Leung said.

"Our key takeaway from today’s decision is the Reserve Bank remains more heavily focussed on headline CPI and inflation expectations than we anticipated. Conversely it appears less concerned with asset prices and financial stability than we expected," she said.

ASB's Tuffley said the sharp decline in inflation expectations had "clearly rattled" the RBNZ and was a key driver for today’s move.

"We expect a further cut from the RBNZ, but it is likely to wait for the next suite of key inflation expectations reading before doing so," he said, adding a June cut with the next MPS was most likely, but an April 28 cut was 'live'," he said.

Mortgage rate cuts to follow?

Two year swap rates fell to 2.28% from 2.45% after the OCR decision, suggesting there may be room for banks to lower their two year fixed mortgage rates closer to (or even below) the key 4% mark.

Co-operative Bank cut its floating mortgage rate by the full 25 basis points, but banks had not reacted by late afternoon.

Reserve Bank Governor Graeme Wheeler said in a select committee hearing this afternoon that he expected banks to pass on all the rate cut to floating rate borrowers and most of it to fixed rate borrowers. Reserve Bank Head of Macroprudential Bernard Hodgetts said the impact of higher international funding costs had only been relatiely mild and they were funding most of their lending growth from local deposits. Some bank economists had argued before today's decision that higher funding costs might push up mortgage rates in the absence of a Reserve Bank, suggesting the banks may consider not passing on much of the cut today. See more in my other article today.

Political reaction

Labour Finance Spokesman Grant Robertson said the OCR cut showed the Government needed to step up and support the Reserve Bank with further stimulus.

Today’s cut came as a surprise to everyone. Hopefully it will shake the Government from its slumber," Robertson said.

"The domestic risks of serious weaknesses in the dairy sector and pressures in the housing market have been a feature of Reserve Bank announcements for a long time now. The Government hasn’t been able to do anything to address this," he said.

Green Finance Spokeswoman Julie Anne Genter welcomed the cut, but said it was overdue.

“For months the Governor has had to keep the Official Cash Rate higher than needed due to the National Government’s ongoing failure to address the housing crisis in Auckland," Genter said.

“National needs to be working in tandem with the Reserve Bank by introducing complementary measures that will contain house price inflation instead of leaving it all up to the Reserve Bank to manage," she said, calling for a capital gains tax on property excluding the family home and the building of more affordable homes in walkable neighbourhoods with better public transport.

Federated Farmers President William Rolleston welcomed the rate cut, which farmers had called for.

“It’s now up to the banks to pass this cut on to mortgage holders, and we urge them to do so on behalf of all New Zealand farmers,” Rolleston said, adding he welcomed the prospect of a further cut.

“Farmers’ cash flow is tight at the moment, particularly in the dairy sector, and anything that can ease the pressure on their bottom line will help get as many dairy farmers as possible through the current season," he said.

134 Comments

AUD currently up 2 cents or 200 pips against NZD

So Wheeler expects "lower inflation" ................. well he is telling porkies , he has suddenly realised that we have entered a cycle far more dangerous than inflation .... its called DEFLATION , and there are simply no tools in his toolbox for this one .

Seriously , we have to have some sympathy for Graeme Wheeler , he is a salt-of the earth hard working honest man who works hard to steady our ship , but he is facing really testing times

Deflation is an awful , awful thing to deal with, far worse then inflation , and takes for ever to sort itself out

Sop to dairy..?

It was a certainty he would cut particularly with the disaster that is Fonterra and the impact that the dairy commodity crisis will have on the governments books.

Wow, I wish I had the ability to predict certainties in financial markets - you must have made a killing on the forex market just now!

Big blue , the commodity price cycle has entered a deflationary spiral , we all know for example there is an endless over - supply of oil on the planet , so we don't need to stockpile it , and of course the prices will fall , and keep falling ...........

I'm guessing the year on year inflation figures are going negative for this early rate cut. Looks like things are bad, but my mortgage financing in the next month is looking up.

The question is how quickly will the greedy Aussie bankers drop their mortgage rates - there is no excuse now - we should be seeing 3.95% for 2 years fixed ASAP

Except offshore funding costs and credit spreads are significantly higher.. I wouldn't hold your breathe for fixed rate decreases unfortunately..

The talking heads looked a bit stressed when asked to discuss this point

HSBC is doing 3.95% now. I am more favour to Brit company rather then Aussie now.

HSBC are offering 2.49% to their First Time Buyers in the UK for a two year fixed at 90% Loan to value.

http://www.hsbc.co.uk/1/2/mortgages/products?pcode=A0040425930000000000…

And for remortgaging customers it's offering 1.49% for a two year fixed at 60% Loan to value.

http://www.hsbc.co.uk/1/2/mortgages/products?pcode=A0040425780000000000…

And it was only a year ago that HSBC were trying to offer me a 5.99% two year fixed here in NZ special rate. Which I was not impressed by, the mortgage rates here are a rip off!

But that down to less competition in the main. Always remember to negotiate with the banks to get better rates.

I struggle to understand why a comparison between UK interest rates and NZ interest rates matters unless you think the costs of both are the same and therefore relevant to your comments about "competition" being the issue

The gift the governor keeps giving - Bill Gross is proud of him.

The only bright light I see in the economy is tourism so probably makes sense.

And Auckland property of course.... Watch them prices rise and rise!

I would not bank on the Auckland property market , its run too hard and will lose momentum just like very other market that's gets ahead of itself.

There is a groundswell of opposition to immigration growing here , and National are losing touch with the electorate ...... the immigration policy will lead to their downfall

Deflation and negative interest rates are coming to NZ - we should have mortgage interest rates of around 2% to 2.5% just like the UK

Buy those government bonds, absolutely no deflationary price expectations forecast in this market.

LOL

What maturities? i.e. Do you think deflation will be the thing for the next year or 10 years etc?

Deflation is just awful , and it can drag on for decades

That implies what, <1% wholesale? Who will lend to NZ at that rate though?

I year USD Libor before currency hedging costs/credit risk premiums etc currently stands at 1.207%

What we need to keep in mind about UK is yes they have very low rates but massive mortgage set up/management costs. This is a trend we may see come to NZ

Quite right, often the rate looks very attractive, but once you add on the set up fees you can be looking at an APR of around 3.5-4%, so not significantly different than here. And then after the initial two year fixed period the rate will jump, unless you switch banks again, and pay the set up fees again ...

Thank you Big blue , I have been saying that since 2014 ,in my comments on this very forum .... its been like watching a very slow train-wreck

The fact is the PPI ( PRODUCER PRICE INFALTION ) is negative , is telling because it feeds into all prices over time .

All farm inputs have come down diesel , fertiliser , feed , electricity ( static ) and now their produce value has come down .

Its quite an unpleasant state of affairs

Confirmation our economy is going from bad to worse. The only safe bet is to buy more rentals in Auckland. No point in having money in the bank. I should have listened to Zachary.

So those prices won't come down then? Eight years on and you are still wrong...

True , there is no point in having money in the Bank , but I would not rely on the Auckland housing market as a safe bet right now

Renters must keep their jobs though. Will they?

“This is a concern because it increases the risk that the decline in expectations becomes self-fulfilling and subdues future inflation outcomes,” he said.

Simple solution, demand the working masses get paid more and provide a means to enforce it..

who needs work when you can flick houses?

Time to invest in tourism!

Will light the fire again under Awkland housing once mortgage rates drop in concert.

Eventually.

"Not planning on lvr restrictions outside of auckland.

Auckland price to income 70% higher than outside auckland. A lot more scope for prices to move higher outside auckland before rbnz gets worried."

Conclusion : keep buying high yielding p.n real estate

Whens the next election? November 2017 at the latest. Tactically it's a smart move to give a quick boost to the flailing Auckland property market. Boost tourism a bit, and lay the blame for dairy squarely on naughty naughty Fonterra's shoulders. Then give the OCR another little cut in Jan '17 for another quick boost to Auckland and stage the election in late April/early May. Bloody genius!

Genius? If you could recognise and write their entire strategy for 2017 elections in less than four lines then I think not.

So Governor Wheeler swallows a dead rat. The canary in the mine told him he had to.

Southlands GDP drops an incredible 9.9%

http://www.stuff.co.nz/southland-times/news/77722487/southland-goes-fro…

So they won't allow Tiwai Pt to die a natural death, esp in a true blue National electorate run by a cigarette salesboy??

RBNZ surprises? The only thing surprising is that fiat money is still standing.

Maybe then your economic model/outlook is wrong.

to signal another cut is telling me economy is worse than most think, we are very very quiet at work and as the industry that feels any downturn first i suspect we are heading to recession very very soon

Agree. Because inflation is so low for so long. Brace yourself

We DO NOT HAVE INFLATION ........... The RBNZ has been treating us like mushrooms , being kept in the dark and fed bull-$h1t we are in a DEFALTION cycle.

The prices of everything is falling everywhere

The construction industry is running at capacity at the moment. The low interest rates are having an effect once you can actually get a building consent. Of course the construction industry is too small to counter a recession.

Or maybe not too small , but if we slow down the rate of migration the construction sector could also find itself in trouble

Its not a surprise for me, predicted both recent cuts. What is a surprise is the possibility of even MORE cuts, now that's a worry.

Hello 2%. So the Q is how much lower can it go below 2%? 1.5% anyone?

Lets see the banks squeal as they cant keep going down.

I predict the NZD will fall a bit today, then recover completely. Such is the information resistant nature of the Kiwi dollar.

The NZD really needs to drop in value if we're to help boost our main export and tourism markets.

So true , but the Kiwi$ needs to drop by a huge % in tandem with the fall in commodity prices , and IT AINT GOING TO HAPPEN anytime soon

It's time all you savers face the facts. You are being made the victims. Time to pull all deposits. Let the banks find other mugs. Whatever you do just move it out of there hands cause one day you will find you have no/ limited access and a loss to boot

Yep pull the money out...

APART FROM HOUSING WHERE CAN I PUT IT?

Are you wanting a return *on* your capital or just a return *of* your capital?

I'm not greedy,i want a dollar each way.

Its your money, you decide.

In times past maybe , but not the case in a credit based system.

With the govt institutions threatening to tax gold and take away cash it's a worry. All the sheep are being herded into property.

Farmland is going cheap or will be. Put in some crops as people also need to eat. Purchase precious metals outside NZ where ird can't touch it. Just get rid of the worthless tender as interest rates here are never going up. Zero or even negative is where the world fiat is going. Property regardless of interest rates is way overpriced. Feeding the bubble just because credit is cheap is suicide because eventually jobs and wages fail to prop it up. It's already started. Up to you. No one will be absolute winners after GFC 2.0. The game is now to survive with minimal loss. Helps having dual citizenship also. You have more options

Well considering that investing in houses is no longer a sure thing these days and does require a huge amount of maintenance (As most Landlords will know).

There are other investment areas that are far less stressful such as: Silver, Science (including tech), Wine, Art and Gold. Which has the interesting acronym of SSWAG (To mean money and merchandise).

Apparently Wine and Art have been two major growth areas after the global economic crash, since they are less volatile and don't require any maintenance. You may want to check out some of the Auction houses in NZ such as Webb's or Saatchi art for online art investment.

Har Har Har Haaaa. For a really good laugh lets take a stoll down memory lane:

http://www.interest.co.nz/news/68256/rbnz-holds-ocr-25-23rd-time-says-w…

And only two days ago:

http://www.interest.co.nz/bonds/80449/roger-j-kerr-counters-arguments-l…

And HAHAHAHAHAH:

http://www.interest.co.nz/personal-finance/68865/bnz-economists-see-inf…

Always check track records. Always.

Boatman has got it correct almost every time!

Japan pulled the same stunt not long ago.....'definitely no rate cut'....and then suddenly negative.

There is not problem with Fukushima and our economy is doing great - Japan.

Looks like life's still good in landlord land.

Yes it just got cheaper to service the mortgage.....so you won't have to put up the rents so your tenants can afford to stay.....isn't there a bit of a trick going on though.....you make a profit you will have to pay taxes unless of course you buy another property but that only works if the values are increasing which means landlords can get stuck in a one way cycle of having to buy another property......a bit like our dairy farmers had to keep increasing in size until the point of a market glut.......so what happens when house prices hit a ceiling? which they will.....governments got enough debt problems of its own at the moment so do you think it can increase the accommodation supplement in a deflationary environment?

There's gunna be more oldies at the auction rooms than a free casino bus ride on a Thursday. Better add more mobility access in the bf takapuna office - the term deposit rates are just tanking it - soon theres going to be more "store of value" in a dick smith voucher - least the plastic is worth something. I got 10 of them - i swap you for a bottle of milk.

yes that will be interesting, if oldies say enough of this and start pulling their funds to invest in other things

Bonds, property shares, properties.

i would expect of a lot of corporates to go to the bond market to borrow shortly

If you think today's OCR rate cut is something special you ain't seen nothing yet.

Our OCR is still 200-300% higher than most major Western countries. e.g.

USA 0.5%

Europe 0.5%

Japan (neg 0.10%)

Switzerland (neg 0.75%)

Norway 0.75%

UK 0.5%

On the other hand if you want NZ to become a basket case then see which countries have high cash rates:

Argentina 13%

Brazil 14.25%

Russia 11%

Take your pick.

Yip. Lots of idiots are shorting the NZD because of this rate cut. Little do they know that the NZD is going up not down for the exact reason that most western countries rates are still MUCH lower.

Well we still 900% - 1200% lower then some others. :P

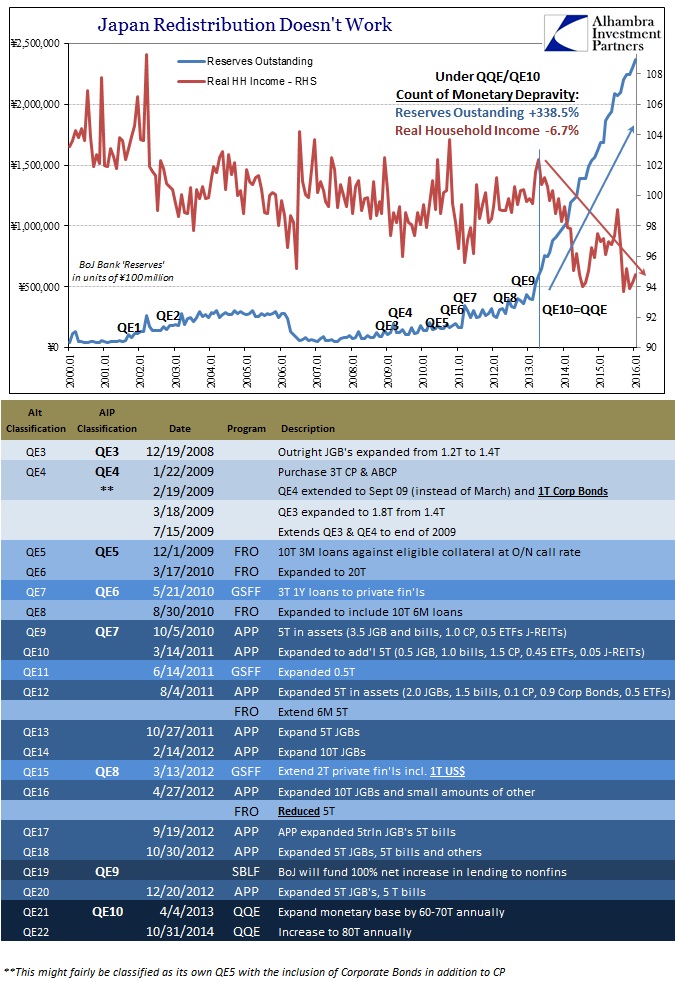

Be careful what you wish for. Income for the unexceptional Japanese citizen is falling at a dramatic rate given the low level of interest rates. View graphic detail

{kind=link}

You've got a serious deficiency in separating cause and effect.

Expect the next fuel price rise soon. Currency down; Brent $40.84, up 3%.

Maybe that will stoke some inflation!?

Interesting thing with the Meeting is the Governor seemed different than usual. He had the more beat up look - like the look you got when you lose or up all night. Usually he seems up beat - but today his manner was different than usual. You have to watch the meeting - i think there is more going on that we are told. Cant put my finger on it - his body language is different this time.

yes he came across as negative, and if think about it last time we were this low was 2008 when all hell was breaking loose

You make a good point, I noticed his downbeat demeanours well. I put it down to the fact Wheeler realises he is backtracking in a major way from his speech of 5 weeks ago ?

Told you so...

http://www.interest.co.nz/news/79079/rbnz-cuts-25-most-expected-leaves-…

Too bad there were no takers for the $100 bet.

Bonds offered a bigger and better guaranteed return.

This OCR reduction was always going to happen - some people shouldn't be getting paid for their expertise and opinion is all I can say! Wheeler has been far to slow in taking action to keep us at the same rates as other countries. Personally I think the world economies have reached a saturation point in the current system......when the individual wants and expects his/her cash to be his own but your Government already has dibs on it.....they have to work out a way to transfer it from your pocket to theirs.....inflation has been the tool until now......and I think they have gone as far as they can with this tool....

The big question is for how long can you keep pushing housing asset prices up when you have deflation? - what we are witnessing is a "systems" error - red alert bell should be screaming......Wheeler is enforced to lower rates he cannot hold or increase at this time and no-one is asking the right questions.....people need to stop looking 6 inches in front of their nose......everyone who is buying a house is helping the Wheeler....he needs you all to go out and splurge as it is the only string on his bow.....what happens when he runs out of OCR cards?

If cash is king when you are in a deflationary environment and you have loaded up with debt - what are your long term prospects for wealth generation using debt as the tool? Remember that house prices are riddled with artificial inflation and no-one knows what the real value is anymore.

Remember the days when NZ'ers were told they didn't have enough savings...but the reality is as individuals we have too much in savings.......the banks didn't hold enough capital for their derivative trading practices........and the ordinary people got blamed for lack of saving when they weren't even the problem......diverting attention is an old and well used trick.......crikey the religions around the world have been doing it for centuries.......

Is what we are experiencing now actually the failure of socialism?

Is what we are experiencing now actually the failure of capitalism?

Is what we are experiencing now actually the failure of neo-liberal economics?

Is what we are experiencing now actually the failure of free-market?

Is what we are experiencing now actually the failure of status quo?

Is what we are experiencing now actually the failure of ignoring externalities?

Is what we are experiencing now actually the failure of our current politicians?

Is what we are experiencing now actually the failure of our ponzi-based economic system?

So many questions...

With one simple answer: yes.

the free market has been dead since 2008 when the banks got bailed. Failure is a part of free market economics, lowering rates is just a continuation of the 2008 bailout. A bigger and harder collapse is being set in stone.

OMG what a sermon Plutocracy.....as long as there are believers the system we have is capitalism the longer the stupidity can continue.

The failure of extensive socialism has been a long time coming. It happened in the 80's when we were just about broke. Then came Rogernomics which was forced on NZ anyway. The next 28 years will see the rise and peak of the retirement age population. Retirement savings will have low returns and retirees will spend little unless they continue working. The pension everyone was promised was never sustainable.

Hopefully we can get through the next 2-3 years without exhausting the OCR or ending up in a liquidity trap. Otherwise we will be in a lot of trouble.

If you have debt the low interest rate environment is the best for paying it off. Even more so now that we are looking like we are in deflationary territory.

Remember the days when NZ'ers were told they didn't have enough savings...but the reality is as individuals we have too much in savings.

I guess this comment is a form of amusement to distract us from reality.

MasterCard said its survey showed that on average New Zealanders could last for four months on savings if their main source of income dried up. Read more

That article at a quick glimpse was written 2013 and refers to a quarter of NZers....I'm looking not at the individual cases but how we present on the whole as the countries stock.

If you look at the total savings of NZers which is around the $150 billion mark.

Then look at total mortgage with Household debt + business debt + agriculture debt = ? Approx $375 billion round it up to $400 ....someone can come up with the latest figures I don't have time at the moment.....then percentage wise the debt to savings ratio is not too bad at all in fact I think it is pretty damn good .....so why all the nonsense that NZ'ers don't save enough in general terms?

And we can't forget there are assets backing all this debt as well......

What we don't get presented with in NZ is a statement of position excluding Government so we have to manually extract information to do a rough approximation of what a Statement of position would look like.

It is what Governments and bankers have been doing that leads to crisis......so if we are going to finger point at least make sure the finger is pointing in the right direction!! I used to think we didn't save enough as I had listened to the political and bureaucratic mantra and then I started actually reading the banks disclosure documents and other information.

Bang....ooops shot my damn foot off now where's that ammo I need a reload.........

Honestly that piece David put up on 90 at nine by the IMF really signaled where a number of moves have come from including Billy Bobs and Theo's....

Wheeler would like to ease the pressure on permanently lower commodity prices through manipulation ...........good luck with that Im off to buy house

This will cheer you up mate.

http://ggc-mauldin-images.s3.amazonaws.com/uploads/pdf/OTB_Mar_09_2016…

Thanks AJ.......now Im scared, could explain the IMF's urgency in trying to look like they did something...gees bugger me

"explaining how the global system has fallen further and further behind in meeting the

legitimate aspirations of hundreds of millions of people on multiple continents, including

those related to economic betterment, remunerative employment, and financial security; "

It all comes back to that small incandescent bulb

https://www.youtube.com/watch?v=Bumx4AerJUQ

One question B. Who were the two economists that picked the move. 2/17

Markets may have cottoned on in the last few days, as the NZD was dropping yesterday in advance.

Grant Robertson seems to think the government should bail out dairy. Labour just lost another election in that statement. Where's the personal responsibility Grant for the gambling ? NZ dairy lost the hearts and minds of most nzders years ago. Polluting, ETS exemption, subsidised coal and water........ rip off domestic prices with no pressure put on duopoly supermarkets. Struggling public won't except bailouts without some kind of compensation. Labours answer to that is more social benefits I guess?

looks like he is going after the national farmer voter, but forgetting middle NZ again

Middle NZ just had their savings accounts pillaged to pay for poor lending decisions. State control is overwhelming where finance is involved. Nanny always knows best.

What? Where did he say that - have you got a link?

yesterday in the house a question was asked of bill english

Richard Prosser: Will the Minster’s Government support New Zealand First’s Receiverships (Agricultural Debt Mediation) Amendment Bill, which will provide our dairy farmers with a similar level of regulated debt mediation support to that enjoyed by farmers in Australia and Canada; if not, why not?

Hon BILL ENGLISH: No, we will not, because we believe that the parties involved in that debt are capable of working their way through it.

Still don't get the connection - the Bill you refer to seeks to establish this in law:

The purpose of this Bill is to introduce Agricultural Debt Mediation as a mandatory

step before the appointment of a receiver in respect of Agricultural Debt. The recent

mis-selling of Interest Rates Swaps, which saw the Commerce Commission reach a

settlement with affected banks, points to a need for mediation ahead of any action

under a security.

Furthermore, agricultural debt is a large amount of money concentrated into very few

hands standing at over $54 billion in the year to January 2015. Many farmers, according

to Federated Farmers, are dissatisfied with existing dispute resolution options

within the Banking Ombudsman Scheme. This Bill places obligations on the Banking

Ombudsman Scheme to administer Agricultural Debt Mediation and through the Receivership

Act, removes any financial limit for compensation.

It's not a bail out bill - unless I've misread something?

Anyway, that's not Grant Robertson, and not the Labour party's proposal either.

Grant was answering Guyon espiners question this morning Kate on RNZ is when he said it. They replayed the comments through the day on their news bulletin

Here it is;

http://www.radionz.co.nz/news/national/298593/govt-should-help-struggli…

Oh for goodness sake - ridiculous.

I suppose what a government could do is look back at tax records for the past five years or so for those faced with receivership - and provided their businesses had been paying sound returns in tax over the good years, then maybe it could consider some form of tax relief for those businesses during the bad. But the point I'd make about Robertson's comment is - no sense in just putting out a general comment about the government should do something .. surely as the lead opposition party they ought to be able to define what that something should be. Otherwise, the comment is properly seen as pure and simple propaganda.

If they help it will make things worse, they will keep production up, keep the inefficient in the game and prolong the day of reckoning, while they drag many efficient farming families into the mire.

I agree - which is why I felt one would only provide relief to previously efficient businesses - i.e., those that had a sound history of paying tax. Point being, as I understand it many farmers used increased debt/borrowings as a means to minimise/avoid tax - which to my mind is part of the rort that may have got many into trouble now. These businesses seem to me to be the least deserving of a taxpayer bailout (given they haven't been good tax contributors themselves). We really want to encourage those businesses that pay tax, not those who find ways not to pay tax.

OMG is this actually the thinking - that an efficient business is one that the State can extract money from????......it is a rort alright.....fraud against the business people of NZ and denying basic human rights to steal the loot and all......how about you paying for your own socialist crap yourself and leave the human rights of others in tact!

Would farmers actually be in difficulty if they hadn't been subjected to the billion dollar compliance industry? It is all this nod, nod, wink, wink got to keep jobs for the insiders at a Government agency near you that breaks the camels back!!!

Low mortgage or mortgage free rental properties would likely be the safest possible assets. Especially for older folks.

NIRP coming soon to the banking sector.

Dairy/Fonterra are stuffed and a lower kiwi is all that will help. Wheeler knows this, English knows this, Key - he has a flag you might be interested in. Just one more term please. Emperor/naked

Interest rates have been falling for decades in the West because interest rates must always be below the rate of return on productive investments. If interest rates are higher than the risk adjusted rate of return then the capitalist might as well keep his money in a savings account. If there is real deflation his purchasing power increases for free and if there is inflation he will park his money (plus debt) in an unproductive asset that’s price inflating, E.G. Housing. Sound familiar? Sure, there has been plenty of profit generated since 2008 but it has not been recovered from productive investments in a competitive free market place. All that profit came from bubbles in asset classes and financial schemes abetted by money printing and zero interest rates.

Thus, we know that the underlying rate of return is near zero in the West. The rate of return falls naturally, due to capital accumulation and market competition. The system is called capitalism because capital accumulates: high income economies are those with the greatest accumulation of capital per worker. The robot assisted worker enjoys a higher income as he is highly productive, partly because the robotics made some of the workers redundant and there are fewer workers to share the profit. All the high income economies have had near zero interest rates for seven years. Interest rates in Europe are even negative. How has the system remained stable for so long?

http://thesaker.is/capitalism-requires-world-war/http://thesaker.is/cap…

Link doesn't appear to work?

From the link itself it says capitalism requires world war.

I love war in a certain way, but only when we win

try this link

@andrewj I think I have a clue as to your question , I believe we have remained stable for so long for 2 fundamental reasons :-

1) The CHCH earthquakes have had the same effect as a war on our economy

and

2) We produce food as a commodity , and every human on the planet has to eat , we don't have to buy or mine gold , diamonds , platinum , coal , iron ore, bauxite , or copper to survive

unfortunately food production has it moments of oversupply. Shocked how poorly the Christchurch earthquake was handled by government.

Yes the earthquake turned out to be the smallest problem to deal with AJ. Too many Pollies and bureaucrats were paralysed by incompetence.....they are now puffing their chests calling themselves world experts on disaster management !!!

Yeah check out the price of food over time, a great market to be in. If only the costs of production went in the same direction...

{kind=link}

It is interesting how well it matches oil price for the last decade..

and how well it matches population.

So by your math the world's population went up 3 fold in a few years then magically disappeared over the last 2?

I dont know what you are smoking but can I have some?

Coal seems pretty important here in NZ...

"The recent shift down in inflation expectations does appear to have spooked the RBNZ somewhat," Bagrie said.

Bagrie said he now expected two more rate cuts before the end of 2016.

"Recent pressure on (bank) funding costs is not really a core part of the RBNZ’s central track (of one cut today and another down the track), but it was discussed as a scenario (and would involve an OCR well below 2%)," Bagrie said.

"Given recent funding pressures, and our view that more downside risks around the globe will materialise as the year progresses, we expect more than one cut before year end," he said, adding he saw the second cut to 1.75% late in 2016.

Why are bank funding costs rising, at the wholesale level only I guess, because of perceived higher lending risks?

If so why should domestic lenders shoulder the majority of this risk with lower deposit rates. Who and what borrowing identities/entities are chosen for preferential treatment by socialising higher wholesale borrowing costs at the expense of just domestic savers. Are the richer unindebted among us being targeted in a not too subtle manner.

May have to go to cash like the Japanese. Great article

>>

Demand for cash in Japan, always relatively high, has increased since the NIRP decision, according to

Naohiko Baba, Tomohiro Ota, and Yuriko Tanaka at Goldman Sachs. They note that demand for cash is

now very sensitive to interest rates, even to the point that cash and deposits are nearly perfect substitutes.

Since deposit rates are so low now, there is little penalty or downside in holding cash. Not coincidentally,

sales of household safes for storing (hoarding) cash have soared in Japan since the NIRP

decision.http://ggc-mauldin-images.s3.amazonaws.com/uploads/pdf/OTB_Mar_09_2016…

So with ANZ my new weekly payment on my $600k mortgage is $861 per week instead of $870 per week. Savings of $9 per week, I think I will buy a rental property.

There has been very little talk about the impact of reducing OCR rates have on the ability to retire. And lower OCR means less withholding tax income for the govt. So, $200k in the bank will only provide enough income to pay rates and insurance.

The other thing not commented on is, low or nirp has effect of pushing money into risky investments to generate yeild. And if that fails? - potential re-rate of credit risk and up goes the mortgage rates.

So when is the first major super fund in the world going bust? It's coming I am sure of that.

Buy all the houses you want. I'll buy it off you for 80% off in 5yrs time as you attempt to liquidate your debts in a deflationary spiral :-)

Someone who had a property he paid 500k for earning 4.16% yield would sell it to you for 100K so you could yield 20.8%. That would mean mortgage rates had shot up to near 20% in five years. It seems unlikely.

Property prices seem more likely to go up over five years rather than down. You could be right but it is a long shot. With rentals yielding more than bank deposits more people might want to get into this game. A lot of property has little or no mortgage too.

@guy So does this mean you would not advise buying any houses now, if deflation is to come? In deflation, is it not Good to have debt as the interest would probably be zero%? I'm confused...

Yes I would not.

Its not the interest rate that matters but the ability to service it. So a mortgage might be say 2% but you will be losing a) capital and b) the wages to pay it.

I agree. Not only that, you will be taxed on the tax (rates) and the insurance so there goes another 15%, bearing in mind that you were already taxed on the money before you spent it on these things ;)

50% LVR nation wide.

And for those with bags of cash who don't even know or care what LVR means? Do we just hope that the Fox Hunters put the fear of "Big Xi" in them all or can we expect "Big Waste of Time" to finally get hands on (at the end of the day- like)?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.