By Bernard Hickey

New Zealand's biggest bank, ANZ, has tightened its lending criteria for rental property investors and owner-occupier borrowers by reducing its Loan To Value Ratio limits, and by stopping lending to investors wanting to buy sections and apartments off the plan.

The move, which may slow development of new rental properties, follows news that bank mortgage lending growth rose to an annual rate of 8.3% in April, which was the fastest growth rate since mid 2008 and four times faster than wage growth. The Reserve Bank has also signalled its concern about risks to financial stability of fast-rising house prices and fast lending growth to rental property investors, who are buying more than 40% of the homes up for sale.

Finance Minister Bill English also confirmed on Thursday that the Reserve Bank had approached the Government to consider including a debt to income multiple limit on lending, similar to the one applied by the Bank of England, where lending over 4.5 times income is restricted. The Reserve Bank said last month that more than 60% of rental property investors had debt to income multiples of over 6.

ANZ communicated the changes to mortgage brokers on Friday afternoon and a spokesman confirmed the changes to Interest.co.nz.

"We are making these changes to ensure that ANZ is appropriately positioned in the current housing environment, taking into account supply pressure in certain areas and ensuring we continue to support New Zealander's financial interests," ANZ's Head of Mortgage Adviser Distribution Baden Martin said in a memo to brokers.

ANZ said it had reduced the maximum LVR for owner-occupier borrowers in Auckland to 85% from 90% and had reduced the maximum LVR outside Auckland to 90% from 95%.

It also said it had removed the combined collateral exemption for rental property investors in Auckland, which meant the maximum for new lending to Auckland investors would now be 70% of the value of the property. Previously, ANZ had allowed investors to spread their equity across their portfolio to ensure their combined loan to value ratio was under the Reserve Bank's limit for Auckland investors of 70%, which was applied from November last year. This meant some new loans were for LVRs over 70%, but were under 70% when considered right across an investor's portfolio.

It said pre-approvals for lending over 80% would now only be available to existing ANZ customers with three months of bank statements, while new customers could only apply if they had a signed sale and purchase agreement.

ANZ also reduced the maximum LVR for lending that was exempt from the Reserve Bank's LVR rules (new builds and refinancing) from 95% to 90%.

Investor lending for sections and off-the-plan apartments stopped

But the biggest change of interest to property developers and market observers hoping for new housing supply was ANZ's change to its criteria for new homes and sections.

"Residential Investment Lending is not available for the purchase of bare land (including where the intention is construction or turnkey). We will still consider construction and turnkey lending for Owner Occupiers," ANZ said.

ANZ spokesman Stefan Herrick later confirmed the change in policy also applied to rental property investors applying for loans for apartments being bought off the plan.

"The changes are ongoing fine-tuning to our lending rules to take account of current market conditions," Herrick said via email.

148 Comments

Governent n RBNZ hast to introduce strict regulationto aboid majot damage toecenomy when n if the housing bubble burst as it will n is onlya question of When.

A question for all you experts. Can the RBNZ introduce a debt to income limit just for investors? They are ones firing the market and 60% are borrowing more than 6 times their income so targeting them would take speculation out of the market, without preventing FHBs from entering the market. Or does it have to be a blanket measure?

There is absolutely no impediment to the RBNZ in requiring investors to meet different requirements than owner-occupiers. For instance, across the Tasman the banks are required to treat investors differently than owner-occupiers and all charge higher interest rates for investors - to provide more cover for the risk to banks..

These include the four major NZ banks - the only difference being RBA's more prudent approach in protecting depositors and favouring owner-occupiers versus investors.

I am not an expert, but, given they have been able to segment the LVR rules by investor/non-investor I'm sure the same approach could be taken for DTI.

Wonder if the other banks will follow or hang back in the hope of picking up new investor's business.

Is Anz winding back in anticipation of the RB announcing new limits on DTI?

The reserve bank is extremely worried about the economy currently. Read the latest financial stability report. This is just the start of many regulations to come. I would not be a speculator right now nor be bullish about property. There is only one ending here and you don't have to have a high IQ to figure out what that is going to be.

Is their sonething that we dont know otherwise why now.

I think they can see the risks are stacked to the downside in the NZ property market.

Australia is already looking very shaky, particularly off the plan apartment sales so they will be expecting losses to rise significantly there.

Dairy losses are surely only going to increase from here.

I think they are battening down the hatches and I'd expect most other banks to follow.

Not allowing combined collateral is pretty huge. In Australia, APRA don't tend to make big announcements about new rules, they tend to speak to the banks in private and have a stern word about what their expectations are. Maybe RBNZ are starting to take the same approach.

And our prevailing wind seems to come from the west, so I'm battening down the hatches :-)

That's a good way of putting it.

I think this will be driven from Australia - not New Zealand, and influenced by events from further afield. It could even be a tacit acknowledgement that the ANZ see the New Zealand housing market as being a bubble and trying to protect themselves.

On Stuff I see Tony Alexander has said there are 18 reasons why the Auckland housing market will continue to grow - all are internal and none are external to New Zealand. He seems to ignore external factors that are more likely to have a significant effect on the New Zealand economy and the housing market. Some are based on assumptions with no real facts e.g. "older people are splitting up and needing two houses" and one I would consider a reason not to buy housing "we Kiwis seem to suck at building houses which pass inspections and don’t leak".

EDIT - bankers are not your friend (nor bank economists).

It good to see them tightening up sooner rather than later. The only negative is that it will reduce the overall percentage of home ownership which is not great.

On the subject of investors a good percentage of them have very deep pockets so are cash buyers. Under the investor VISA rules you have to keep over $10m invested in NZ for over 3 years and most of them prefer to be invested in property rather than equities... a consequence of trying to be the Switzerland of the South.

I would expect the other big three to follow suit

I read Tony's marketing piece for BNZ. Read with a pinch of salt.

Not only did he exclude external factors he also made light weight of any potential new regulations imposed by the Reserve bank and government. Ie loan to income ratios

Tony Alexander is in the business of shifting his employers product: Mortgage Debt.

Huge grains of salt required.

[ unnecessary personal insult removed. Ed. ]

my sister used to work with Tony A when he was marketing consultant at the Mad Butcher

Hold up. Are we all in agreeance that there is a supply and demand issue in some areas of NZ and that NEW houses are required to provide much needed accommodation? Because if we are, then banks no longer lending to the very people investors who can afford to build new houses seems to me only to exacerbate the current problems and push current home values higher.

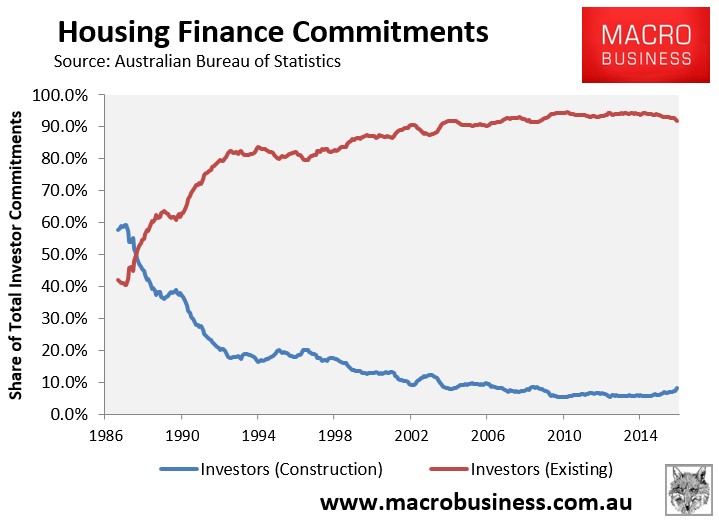

If New Zealand is anything like Australia, investors are not building new homes, they are buying existing homes;

http://www.macrobusiness.com.au/wp-content/uploads/2016/05/ScreenHunter…

{kind=link}

I reiterate that in my suburb in Ak there are a number of houses for rent that just are not being taken up.

Is there a housing shortfall at all?

House next door has been on the For Rent ads since November. Still empty. And it's in a good location handy to city, off-street carport, public transport, lots of retail and industry, and a large polytech. Have been keeping an eye to see how long they hold out before dropping the rent.

No. It is a demand issue. Which is why the govt is focusing on supply, it looks like its doing something, when in fact it is doing nothing - The Claytons approach.

If availability of mortgage finance volume reduces prices decline.

There's plenty of houses, just too many in too fewer hands! Hoarders, speculators and Non residents

Hold up. Are we all in agreeance that there is a supply and demand issue in some areas of NZ and that NEW houses are required to provide much needed accommodation? Because if we are, then banks no longer lending to the very people (investors) who can afford to build new houses seems to me only to exacerbate the current problems and push current home values higher.

And also add to that the idea of introducing income ratios for mortgages which will handicap low income earners too.

Bank showing govt. and rbnz who's boss and protecting their security by ensuring supply remains right

doubt it. the rbnz will be in their ear.

A big driver of the demand issue is loose bank credit. Turning down that tap wont stop houses being built. It just means that johnny landbanker may have a little less gold.

Has anybody down in little old New Zealand woken up and realised that lending at 6+ incomes is bats**t insane. The rest of the world has.

investors buy existing stock, generally its FHB and owner occupiers build new houses.

if you curb investors you reduce demand on existing housing stock

I never got around to posting about the housing crisis public meeting I attended. Life got crazy for me that very night, all partly as a result of my partner and I struggling with our different perspectives on the situation. But, I digress. What a sad evening it was. A mix of young and old (which was good to see, not nearly enough young though) Shammy Eaqub spoke passionately about how this situation has been gathering pace since the 90s (perhaps before). Alex Johnson of the youth advisory panel talked about his pain at having to speak at the Unitary plan and being heckled. He also showed some interesting images of where there was 'affordable housing' left in Auckland, 90% of the map blacked out. Phil Twyford spoke about his sheer embarrassment for his older kids not able to get onto the property ladder in any reasonable form. I looked around me at one point and I counted at least 3 people CRYING. Ultimately though, I left deflated. It was left hanging with the definitive hint of 'we're screwed, there's nothing we can do' attitude. I came to the realisation that for young couples and the next generation coming up who choose to live in Auckland or indeed have no choice, we only have one hope and it's a sad one. We can only pray that renting laws get better, that's it. It's over. Tonight as I drove home I thought about the fact that I can have as many kids as I like, no one is stopping me. Yet, I don't want any because of this situation, I can't afford them.But to make my life a little happier I would love a dog. A simple thing, yet I doubt I would be allowed, even if I was in my current situation what if I get kicked out. I know. It sounds pathetic but it's a rather dire outlook. I don't really know what the current climate is, as I lost track after that night at the public meeting but as far as I can gather nothing has changed and it stills seems no one cares. I say this about gov but I also say it about my peers. Where were they all at the public meeting??? I wish I had the time intelligence and gumption to start an uprising. Are we really heading towards an Auckland that only caters for the elite? Will they build a wall? Sigh.

Get out of New Zealand for a few years and grow out of the place. In the current environment your talents are wasted there.

Yup, I know. It's like a bad relationship that I'm trapped in for a number of different reasons. I'm beginning to wonder what might drive me over the edge, to snap. To leave Auckland - another 'man overboard'.

Part of getting out will be getting past the Stockholm Syndrome.

Buy in gloom, sell in boom.

hang in there.

its just a matter of time before the balloon pops, and there will be plenty of offerings on the table.

That's really advice for an investor. Even then you need courage to buy in a falling market. For example leaky homes and leaseholds are fairly gloomy - do you have the courage to buy? For someone needing their own home they should weigh up affordability compared to alternatives like renting and investing elsewhere. The return on the deposit should be the stability from having your own home while the interest payment should be around the price of rent and the capital repayments should be seen as a form of saving. Capital gain will be the icing on the cake.

Currently things are a bit out of whack due to unusual competition in the market. If supply is restricted and demand is strong then a pop is extremely unlikely.

"Currently things are a bit out of whack due to unusual competition in the market". Oh I love how you've phrased that Zachary. The "Unusual competition" would you be referring to the massive 40% of Overseas Investors (A lot of which seem to be connect with money laundering activities). Not surprising that the Auckland property market is so out of whack!

And yes, I'm aware that this isn't just limited to NZ and is happening globally but we have been a very convenient vehicle to harbour such ill gotten gains, that continues to fuel our property market.

Until effective AML (Anti Money Laundering) measures are put in place, I don't think we'll see any significant slow down in the Auckland housing market.

ZS - if you can correlate the 40% foreign investment to money laundering, which may not be too far wrong, and remove this demand from the equation overnight, which may or may not be conceivable - what do you think would happen to price?

As stated earlier

the chickens will come home to roost

prices can only go one way. and there will be opportunities galore

...''the property ladder.." .F*** the ladder. Most people would appreciate a HOME.

Let me register my agreement before you get edited for naughty words. After this craziness blows up like the meth lab run by monkeys that it is, I hope the next speculative frenzy is over something that the average person can opt out of, like comic books or vintage shoes.

Agreed. I'm one of them. Someone who would like to fill the home with something that would bring me so much joy. A little waggy tailed rescue dog, unloved by someone else but loved fiercely by me. I have that love to offer but everything is screwing me out of a simple dream. One that really shouldn't be that hard, even if the renting laws were relaxed a bit maybe I could have a piece of that joy.

This should be the basis of an election campaign ad for the opposition.

Ha! I am a copywriter as part of what I do, despite my garble above. Maybe they should hire me? ;)

Some one already wrote 'Euphoria is the Key'

May be we can add 'Misery is the Labour' ?

Hey Hardworker, you might want to compare notes with the Vancouver citizens who are also feeling the same property pain as us.

Last year Vancouverite Eveline Xia started a Twitter campaign under the hash tag: #donthaveamillion, highlighting their cities affordability crisis.

And they're experiencing the exact same housing situation as we are here in Auckland but worse. Please see the BBC article: http://www.bbc.com/news/business-36369108

very interesting link thanks CJ099...particularly parts about the study of electricity usage finding a lot of homes sitting empty in Vancouver; and the effect on young people there - they leave, they have to for economic survival

You mean property SNAKES and LADDERS.

Kiwis haven't had a snake for sometime (many on this site tell me we've never had one, who would have thought?!) so it will be quite the surprise when everyone drops down 10 rungs of the ladder at the same time. But this won't be monopoly, no $$ collection when you move past GO. In fact, the friendly banks might just take it all away.

I provide people with homes!

'Homes' that we can get kicked out of at the drop of a hat. 'Homes' where we can't hang bloody pictures on the walls or paint pink and blue for nurseries. 'Homes' that are damp and dingy, where we cannot have pets and we are inspected every couple of months like dirty prisoners in a camp, most likely constantly suspected of drug use may I add...You provide shelter that we pay you for for because we cannot save enough to get out from under your control. Yes the alternative is being owned by the banks but in a fair world we'd have the option of digging deep, being sensible and paying it off so we have somewhere to live when we retire!!!! So NO, they are not homes. A home is not somewhere you live and worry constantly about that phone call from 'your landlord' saying the family is moving back in and you have to get out. Thanks though, it's wonderful living in that kind of fear and stress. Keeps us alllll under control. My god I'm angry today.

That deserves a standing ovation.

Is there anything more revolting than self-satisfied parasitical exploitive scum patting themselves on the back?

It's disgusting and I don't care if it's been out there by a troll. I've tried to be diplomatic on here and listen fairly to all sides of everyone's stories. I even took a break from it all to deal with a personal issue and in the hope that out of sight out of mind would help me focus on other important things in my life. I come back to it and not only is it still being ignored its getting worse. im so angry. I'm so angry that I and many others are being 'forced out' of Auckland. Are we being 'cleansed' is that why no one is doing anything about it?

Push for grassroots change - spread the word among friends, colleagues that the current government is shafting a huge number of New Zealanders and the future of many young. Get politically active, be a dissenting voice etc.

The current state of affairs is dire for many but first we need to get rid of the stink of shit (National party) before things are going to improve. The last thing we need is apathy.

the only way that statement would have any truth would be

you built the house yourself

you financed a new build

you rent at below market rents and subsidize the tenant

otherwise you are just investing in rentals to make yourself richer because you are able to

Haha dream on, if you built new homes for rental you do. Otherwise you are simply hoovering up current stock that would be available for those who want a HOME... Maybe even FHB.

It's hilarious this view you provide a social solution - your actions and attitude are the problem!

A parasitic one no less.

Your Landlord - you say you provide people with homes. How many have you built? I bet it is zero. You are keeping people from buying their own homes more like it

The troll has been fed much to his delight.

Hardworker - I think this is much more than just a housing issue, western values, morality, greed and the lack of leadership for the vast majority of people. This world is about the 1 percenters, the elite - when idiots like the kardashians are held up as the ideal, you know we are in deep schtuck.

The only way to restore order is a revolution, taking to the streets. Somehow there needs to be a joining of hands, an uprising - off your phones, step away from the internet, look around you, breath deeply and do something... We need another John Minto

I hear you and god willing if I knew how to start this revolution I would. You know I speak to my peers about this on the regular and literally I get nothing from them. The last friend I spoke to casually mentioned that she'd buy a house in Nelson instead of Auckland to rent and then retire to. I wondered for weeks if she knew something I didn't know because I'm aware Nelson is getting pretty unaffordable too. I saw her two days ago and she mentioned she'd looked and was horrified that that was out of the question for her budget too. Most likely she's been watching too much kardashians and had NO IDEA what was going on. Honestly? I despair.

Don't worry Hardworker - many of the baby boomers will be dead in 20 years time and let's hope that this shallow, self centred, greedy mind set will leave with them.

There will be plenty of houses available when they're all gone - and all going well this current generation locked out of the market as a result of this experience will appreciate that houses are meant to be for people to live in and raise families in, and not something to get rich on and brag about their 'portfolio' at weekend BBQs.

Read the NZ herald article which exposes everything http://m.nzherald.co.nz/property/news/article.cfm?c_id=8&objectid=11649…

A couple of random 'lawyers' spouting drivel is hardly 'news'. If might be if they were testing these ideas in court, but they are not. Just acting as nimbys.

The content in the article is 100% valid.

Everyone who feel strongly should use all social media platform like facebook, twitter or whatever to expose.

Good post hardworker. The thing is it is part of a global problem, not just Auckland. It is exactly the same in London and many other cities where it is not uncommon for 3 or 4 generations to all live under the same roof.

The difference with Auckland is its meant to be about the quality of life....

I know. Which also begs the question, if I were to move on and do the job I do I'd probably have to go to one of the other centres with the same issues. Jaysus.

That is a very strange move by ANZ cause they are effectively giving a large advantage to other competing banks... I'd like to think it's because ANZ think it's the best thing to do but I doubt it... There is something we don't know...

It was done on purpose - most likely it is something they have been considering for some time - a few weeks at least. I suspect the other banks will be considering something similar.

then who will be able to build the houses that our country so desperately needs?

That's not the banks concern - they are answerable to their shareholders - not their borrowers.

Also answerable to APRA the silent assassin

Having read the article, and having followed recent moves in Australia by APRA, my conclusion is, in light of the APRA measures, the AU parent banking companies are reconsidering the exposure of their NZ offspring and how exuberantly out of step with their own domestic processes (NZ 8% lending growth in 1 month). It is both difficult and dangerous to have two subsidiaries of the same organisation following different systems and procedures. Easier to control and manage one set of rules

The government ? Like they bloody well did after WW2?

the State

Elizabeth - I think you mistakenly mean the houses that property investors need to purchase to grow their portfolios, opposed to houses that 'real' people need to buy/build and to live in.

Real people, you mean owner occupiers, can still get lending to build their off the plan houses and apartments - they are not disadvantaged by this change if I've read correctly.

But the country apparently needs housing, and cutting off the finance to investors to provide this just seems stupid at this time, because no one else is building them as fast as private developers are. Thereby reducing supply would just push current house prices and rents up would it not?

But here's the fundamental problem - real people can't afford to build those houses. That doesn't mean that therefore we need to allow investors to fix the problem - because in essence they have created it.

Because investors have pushed asking prices above what our society can support. We don't have wages to support current prices.

It all points to the fact that our houses are price higher than what they are worth. If 'real' people can't afford to build them, only investors who were leveraged using capital gains from other real estate, it just highlights that this whole situation was built on false foundations and will in time crumble.

Real people - FHB's = the process of council consent, designing and building a property is far more complex and challenging for someone not in the industry than most FHB's can manage without getting taken for a long ride. That is if they possess the 40% cash required to fund a new build, including all the reports, architects fees, council charges, cashflows, ongoing valuations, building overruns, delays etc.

Also since when did a FHB, have the ability to build one flat ? flats are multidwelling properties - and even a small 4 unit complex is way outside the reach of a FHB- who of course would then find themselves as landlords of three other properties.

Fact is - that fro flats and apartments - developers and investors are required to ensure these are built - FHB's cannot finance and build these - maybe the odd one - and we need 15,000 in Auckland this year unless demand drops and no sign that is even remotely likely to happen

...perhaps something radiical like ummmm making foreign investors build not buy?

Or if we could at least match our policies to Australia so we don't get lumbered with the bottom-feeder fraudulent overspill that they successfully deter?

I'm guessing here but I suspect that its the Oz parent who is directing the NZ branch to stop being stupid and pull its head in. It must be nervous about its potential liability and the bad press that its Oz parent would get if it let its NZ branch get into difficulty, not bail it out and the NZ branch go bust. In that situation its Oz parent would experience a run and would itself fail.

Over the last year or so the ANZ share price has fallen from $35 to $25 as a result of perceived investor risk to the AUS/NZ housing market.Major shareholders have probably said reign in the risk profile to increase market rating.

Share prices of all the AU banks are down 25%, not just ANZ

the shit hit the fan, mark the date.

Large portion of overseas investor use false foreign income to get loan – same thing happen here in NZ.

http://www.abc.net.au/news/2016-05-09/westpac-and-anz-approve-hundreds-…

Remember that NZ is a safe heaven for black money and many of that is channelized to buy property to make it legal and they do not want loan and also do not mind paying 10% to 50% extra as long as the unofficial worthless money is turned offical though at a premium. Government knows that but is afraid to touch as the fear is that may be NZ is surviving on that type of money.

nothing fires me up more than these self-confessed slum lords who own like 40 properties

Envious, sammnz ?

Yep I feel the same, though it's not just us, check out this article from the BBC about Vancouver.

BBC Article: Vancouver's 'Freak Show' Property Market

http://www.bbc.co.uk/programmes/p03vcz5j

Interesting quote from the BBC Vancouver property bubble documentary - " it's like the tobacco executives denying the connection between smoking and lung cancer - the same with economic commentators and banks denying that Vancouver,( Auckland, Sydney) housing market is being driven by the wealthy Asian purchaser, whether they be PR, visitors, students, immigrants, or just parking their cash".

Curiouser and curiouser! Alice peered in the hole "Oh my it's getting deep"... ANZ first to stop digging.

Wow - No combined collateral exemption! that's massive. If the RBNZ brings in DTI's then an epic crash will become a self-fulfilling prophecy. I suspect large pockets of Auckland dominated by Chinese buyers will be unaffected though.

How would that work? Just borrow cash up to 80% against outside auckland properties for 'travel' then next week use the cash for 30% of auckland property.

The foreigners/Chinese buying up all of Parnell, Remuera, Newmarket, Mount Eden DGZ etc.. those guys are not borrowing money from NZ banks to buy property. The price is set at the margin and those foreigners probably account for the majority of the market in those nice areas of Auckland.

Don't live in any of those "nice" suburbs but agree, also happening in my area - We are stuffed unless offshore investors are limited (and this includes short term residents mostly students and short term work visa holders who are funded by 3rd party offshore money AND who count themselves as residents or buying for own use AND therefore do not count as nonresident for the pathetic record keeping the govt has reluctantly intro'd .

Everyone knows except our PM.

I misunderstood you Simon, yes you're probably right. However, banks are being pretty nosy about what you're borrowing cash for these days, AML compliance I guess. I suppose you could request the maximum revolving credit the bank would lend. That would be an anonymous way of levering up your existing properties. I still think Debt to income ratios would have a devastating effect on prices in certain places.

Agreed!! Might pay to diversify ones lending into Auckland versus non-Auckland property at different banks no?

Save your energy people - don't post any more anywhere because the government is not listening to you. It's listening to the well organised lobby groups whose capital outweighs yours a billion to one - tax deductible (even avoidable). Bankers, developers and investors that's where it's at apparently. And those living in cars (if they can afford one) - well bugger them they got what they deserved.

How can 45% of 4 million sheep be wrong?

Off to count sheep and get some zeds...

Why go slow when you can go fast

New tax rule for buying and selling Aussie property begins July 2016

New rule, which will be put in place to prove the seller is an Australian resident, requires sellers of residential and commercial properties to obtain and present a buyer with a clearance certificate by the settlement date in order to be paid the full sale price. Without a certificate, the buyer will be required to withhold 10% of the property sale price and pay this directly to the ATO

https://au.finance.yahoo.com/news/the-bizarre-new-tax-rule-for-buying-a…

Go ANZ. Well done them. I am astonished. No central planners needed or wanted (they can go back to sleeping or playing very serious mind games with each other, or whatever it is they do during the day). Sensible banking from an Aussie Bank? Whatever next. Are they mad? Is their Aussie parent in dire straits and needs to reduce their loan book? What is going on?

It often seems that NZ is twenty years behind the United States. I watched a movie last night, Prayer of the Rollerboys, made in 1990 that expresses many of the fears of our young generation now. It's interesting what the leader of the Rollerboys, Gary Lee, says in his speech at just over a minute into the movie:

Before many of you were born, our parents caused the Great Crash. They were consumed with greed. They ignored repeated warnings, and borrowed more money than they could ever repay. They lost our farms, lost our factories, lost our homes. Alien races foreclosed on our nation while we... We were locked in homeless camps. Now America belongs to the enemy. Forget your parents. They didn't care about us. ....

Quite a good movie even if it only scores 5.4/10 on IMDB and view-able in its entirety on YouTube. The future?

hey zach :) interesting! I'm fascinated by the concept of life imitates art and art imitates life. Especially in film. I was just thinking this yesterday. Weirdly as I was driving into the city to work. I had in my head The Capitol from The Hunger Games. Where the elite live in wealth and they pitch the poor districts against each other. It made me think of your Elysium idea, where Auckland is headed. I'm not trying to be offensive btw, I just have a very active imagination and it all seemed poetically linked yesterday! :)

Yes, I think movies are more than just entertainment. A bit like the Greek myths they are trying to tell us something. Unfortunately people have tried to use them to re-engineer reality but that usually fails and ends up as a pretty forgettable movie. The good ones like many of the Zombie movies have a message I believe. Everyone should think of themselves as being the leading role in their own movie.

I dont understand why they would be halting lending to non owner occupiers commissioning new builds. Period. Can somebody explain?

Seems very drastic. What's up?

Just to add to your concern xelnaga... you should know that, as a long-term PI (and loving every minute of it, especially here on interest.co.nz) I am quite happy that the ANZ halts lending to "non owner-occupiers commissioning new builds."

Actions like this favour me very muchly, xelnaga. All banks should do it! Life will continue to be good in landlord land xelnaga.

Thanks for sharing that. However, I didn't ask if it favours you. I asked why ANZ are doing it? Why specifically sections and new builds?

Er, because it keeps prices high? I mean I know it sounds unlikely, but just maybe.

When the tide turns they don't want an oversupply of properties available with no one living in them.

How Ireland, Spain etc got into trouble. A perceived lack of under supply turned into excess supply when market sentiment shifted.

Didn't stop them lending to the mining and dairy sectors. Maybe they see investors / speculators as being more risky......

This move by the ANZ is both not surprising and at the same time is astonishing. I am sure some investors and speculators who hold Auckland property thought that the current runaway train called "rising Auckland house prices" was beyond control and would keep going faster and faster. Clearly the ANZ feels the train needs some restraining. The ANZ does not want to risk its loans getting into distressed circumstances. The word " losses" is not one banks like using. The ANZ is the biggest player in NZ. Look to more Banks imposing their own internal limits that should have been put in place by the RB and/ or government before now. Banks limit their risks. The ANZ feels risk has appeared on the horizon. This move by the ANZ will be the first of many by the Banks to restrict lending and could lead to RB intervention. Interesting times.

I doubt that ANZ suddenly developed a conscious and desire to restrain the runaway train - I suspect strongly that they feel the market is very overvalued and that the downside risks of a sentiment led crash would leave them exceptionally vunerable as you allude to later on.

if the other banks follow - as is likely we will be seing no new builds at all - as the new build financing for FHB's is incredibly challenging and requires a high level of cash flow and deposit - more so than purchasing

Please read the article in nz herald and support http://m.nzherald.co.nz/property/news/article.cfm?c_id=8&objectid=11649…

good article. I definitely support. Agree 100% with their analysis and position.

Aren't these the same banks who pre GFC lent property developers finance for anything from a hen house to an out house provided they could recite the alphabet and stand on one leg.

How times have changed.

It was developers over supplying the market that popped the Irish housing bubble. The ANZ move could further restrict new builds and thus restrict supply. When you think about it it may be in the bank's best interests to maintain constricted supply and slightly harden lending rules to effectively preempt a possible downturn.

You seem to look at as if it is only a supply / demand issue and ignore risk. I think the ANZ are looking at this in terms of risk and are concerned at what they see. I would expect nothing less from you to look at it in terms of supporting house prices rather than in terms of downside risk. Anything to support your narrow view - it's called confirmation bias.

If prices remain high there is less risk for bank and home owner. Keep prices high by controlling supply/demand..

Actually there is more risk. High prices mean that if there is a correction the banks have much more to loose. If it is an event outside their control - like the collapse of dairy and mining - this could have significant effect on prices or peoples ability to pay. Even in supply constrained city's like London there have been corrections. You seem to believe nothing can go wrong - it's not the known unknowns you have to worry about - it's the unknown, unknowns.

Wrong. Every instance of significant price falls in property globally has been a result of over zealous developers resulting in oversupply. Think shoebox apartments in auckland mid 2000s for a local example.

Currently in USA even prime markets like NYC area seeing developers getting carried away with low interest rates and signs of over supply.

ANZ know this is their only worry so are controlling it. They knew all along that they could do this. The rbnz can not force banks to lend $ to people they don't want to.

Bollocks. Every instance - that is a bold statement - all it takes is one instance to prove you wrong ( as CJ099 points out the Irish property crash had more to do with risky lending than oversupply. The same can be said of the US property market collapse in 2008 ( i.e. sub-prime - the banks didn't understand risk) or the London crash in the late eighties where people were borrowing 120 percent. New Zealand - Wellington in the last few months - is that a supply issue or irrational exuberance. ANZ is introducing these measures because they see increasing risk - not to protect you but to protect themselves or more accurately their shareholders. Under your logic the bank is reacting to risk - the risk over oversupply, To believe that the bank would engage in such Machiavellian tactics when there are other players in the market I think is simplistic. In the end who are your trying to convince - me or yourself.

We are just saying the Bank wants to keep the prices at least at the current level. Seems just like common sense to us!

Or maybe self interest. While the banks (and you) may want to keep the prices at current levels - life doesn't always work out that way. As far as I am aware there has never been a successful deflation of an asset bubble where no one got hurt. The measures seem mostly aimed at investors - the ANZ most likely see them as the most risky of property buyers ( David C has also been asking questions about income verification / loan fraud - which is just as interesting - why?). Maybe the ANZ see the current investors as being less investors and more speculators and they want to lessen their risk. We will most likely will never know the real reason.

By removing investors / speculators to a degree from the market - it removes some of the pressure from rising property prices ( as house prices rise the likelihood of a correction increases - especially as the DTI increases). You use the common sense argument - but many investors / speculators need rising house prices to "create" equity ( especially if interest only ) - other wise the investment becomes a lead balloon around their neck.

Most investors/speculators are in a much more robust position than you think. For many it is a way of life, a spiritual journey even. Look at Your Landlord comments. A few years of flat prices, even a decline, wont phase us at all.

This is why banks are more than happy to lend to landlords.

What evidence do you have prove that most investors / speculators are in a good financial position. You are presenting a statement that can not be proved ( the only group that may know are the banks). Are you willing to provide your statement of your affairs, but then that is only one person - and then there is no way of knowing if you are telling the truth. Your comment about it being " a spiritual journey" makes you come across as being in cloud cuckoo land. My Landlords comments come across as being smug and arrogant, but most of your arguments tend to use irrefutable logic and no hard facts or evidence.

Most of your arguments seem to be justifying to your self "it's different this time".

Many landlords are small time with only one to three properties and have been in the game for many years and have thus seen the equity in their portfolios increase massively giving them quite a bit of room for maneuver. Rent returns, while not great, are enough to service loans for many so they can hang out for a long time. Many have regular jobs and their wives too so have a reservoir of income to service loans at a loss for a long time if need be. They also tend to have large revolving credit facilities to draw upon in a crisis.

By spiritual journey I mean we see land as special like gold bugs view gold. I think the word spiritual to you has connotations with the supernatural but what I mean by that is it is a way of life. Landlords are in the game for their whole lives and wont sell to make an easy buck and even genuinely believe they fulfill an important role in society.

Most of your arguments seem to be justifying...... Same for you but in the other direction.

I wish I shared your optimism ZS. my very first accounting job was for a chap who lost everything - 30+ investment properties through overexposure during the last property crash. He was conservatively geared, did the right thing having exposures spread among numerous banks, was a professional .... lost his job, the market crashed and one by one he was called up. Destroyed him, his marriage. I suspect many investors out there are way less savvy. Probably have less disposable income to support a economic correction (to hang in there) The guy mention was a surgeon. Very sad.

That sounds like an extreme case. Surgeon lost his job? Sounds like he was hit by many things at once although I don't entirely believe this story as told as a general warning for all landlords. It seems I have heard the exact story from different people. Surgeon lost his job eh? 30+ properties is an awful lot for someone with an important day job.

Irish risky lending resulted in developers OVER BUILDING using immigrant workers who helped fuel demand further and give an artificially rossie view of gdp.

Gfc meant a halt to lending and developments, immigrant workers left, and we're left with more houses than people to fill them - prices fell heavily.

US markers same storey - actually even better examples as US is made of many different markets and it was only those which had over building during the mid 2000s boom that saw large price falls

NZ has had many booms followed by flat lining and mild falls - only in places like gisborne were population growth is negative have these falls been persistent or servere.

totally wrong. when a correction occurs. savvy investors look at yield, or salvage value when purchasing. yields on residential property right now are appalling, hence most sophisticated investors will prefer commercial right now. All the banks. and the RBNZ care about is financial stability. if 10,000 property investor lose everything provided those houses, and more importantly mortgages, or positions are closed out by new purchasers, and the financial system is maintained they couldn't care a toss about those investors who are bankrupted.

No I think you're wrong there Zachary about the Irish housing market crash in 2008, over supply was only a small part of the problem. Their crash came as a direct result of "risky lending" and when the GFC hit they went off the rails. The GFC also had a huge impact on other property markets especially on EU countries that had switched to the Euro.

The speculative bubble in the Irish property market was supported by a surge in bank lending, and the balance sheets of Irish banks grew disproportionately large relative to the size of their economy (Sound familir).

The Irish banks had traditionally relied on their deposit base to fund their lending activity. However, greater financial integration, spurred in part by the birth of the euro, allowed them to turn more and more to short-term borrowing from abroad, from so-called wholesale money markets (Remember Subprime lending from the US)

https://en.wikipedia.org/wiki/Subprime_mortgage_crisis.

This period also saw a global increase in risk appetite by financial markets, and Irish banks were caught up in this.

And was reflected in both a concentration of lending in property, and increasingly risky lending practices, both of which would prove highly damaging when the bubble burst. In addition, so-called ‘light touch’ oversight of banks meant that there were failures by supervisors and regulators to identify and act on risks that were emerging in the financial system. The growth in public spending also contributed to the exuberance in the property market.

Looking at the Wikipedia article on the Irish bubble the general impression you get is that demand dropped off due to over supply. Sure there were other factors but the article mentioned hundreds of thousands of empty houses and 12.6% of the workforce being involved in the construction industry, that sort of thing. Crushing over-exuberant new builds would be a logical step in forestalling a house price crash.

What about the crash in the US....

and the cause of over supply was credit and capital gains,

IT WAS RISKY LENDING ZACHARY!!! I should know I was there!! Nice that you try to sweep the main cause of the GFC under the carpet.

The main reason why property demand dropped in Ireland and the rest of Europe and other large parts of the world like the US was due to the credit stream being massively restricted and in some cases turned off. Once they switched off peoples ability to lend to buy or build houses by obtaining high loan to value mortgages and credit the whole system started to collapse.

The increase in construction in Ireland did help to boost the Celtic Tiger economy as it was known, the banks fuelled the boom through 'risky credit' (A trend started by the US banks), as they did with other countries that were also going through a construction boom like Spain, they were also hit by the GFC, so funding for new homes virtually ground to a halt and a lot of construction project were left unfinished, this in turn led to increasing levels of unemployment and a recession.

You have to look at the bigger picture to truly understand what's happening.

Just going on what I read in Wikipedia really. There was a huge emphasis on residential construction that included a very significant percentage of the workforce and GDP making it somewhat different to NZ's situation. Of course it was risky lending to people to build houses and apartments that couldn't be sold at a profit too.

I believe banks are going to try and avoid a housing crisis, which to me and them is a price crash, by carefully controlling lending. Nothing knee jerk, just adjust here and there like the ANZ is doing.

The last Paragraph sums it up, for me:

"The Government's reluctance to act might be due to the contribution that overseas investment makes to the economy", the lawyers said.

Seems like there are a few downsides though..

It will have minimal effect on invesrors. You can still increase lending on one property up to 70% to use as a deposit. Take the deposit to ANZ and borrow the other 70%. Most investors should be doing this anyway.

Why - that is just increasing your risk. You do realise that if there is a correction and there are significant losses - all your assets are at risk - not just your investment property.

Each investment asset with debt is individually at risk. If you are structured well. Your home would ideally carry no or little debt with corresponding risk.

Mortgages in New Zealand are linked to a person not a house. When you sign on the dotted line you are in effect putting everything you own on the line to guarantee that debt.

Not entirely true. You can get creative with legal fictions such as trusts and companies.

Careful there xelnaga... such things are supposed to be secret to us landlords :)

While true - they can be set-a-side. Companies will generally include a PG - trusts can be set-a-sie as alter ego trusts. While you can put property etc in other peoples name (wife , children , dog.....) - the final arbiter is the High Court of New Zealand.

Has this anything to do with the new CFO.

Previously as an investment banker they advised Slater and Gordon on their $1.3 billion purchase of UK firm Quindells. The company now seems worthless and the deal described as the worst in recent Australian history.

Add to that the bank seemed have a hand in sacking the stockbroker that commented Sell. And the whole thing turned into sexism in banking to boot.

ANZ the MSM report are now ready to appologise to the broker and pay damages.

http://www.theaustralian.com.au/business/financial-services/anz-set-to-…

Would the appointment have been run past the RBNZ?

In good hands we are. Too much information.

Unless the government brings a law and makes it nandatory for all bank, will not be much.

Hoping on 9th June RBNZ announces besides income to loan and other measures as is the need to control and protect NZ from financial disastor whic is comming, if not done anything now on priority.

By ANZ tightening up financing of vacant sections that just lowers supply of new builds and increases values further. The higher values go the less chance the banks will have of losing money as the real estate market seldom drops more than 20% in a crisis i.e. post GFC - Auckland only dropped 11% whereas coastal lifestyle and areas with less employment dropped around 20%.

So anything the banks can do to ensure that the LVR across the entire portfolio of lending is at say 30% to 40% then minimizes the chances of there being a mortgagee sale clean out further down the track.

Government may feel the same - the higher they can drive the prices the less the chance of fallout from a price collapse. Also more money available for those cashing up when retiring therefore not so reliant on government super and more money available to cover the health costs of the huge numbers of elderly migrants they are currently letting slip in to NZ so easily.

Property is only one part of the unjust system of globalisation, driven by greedy coporates and corrupt politicians. All we can hope for is a decent property crash that will collapse the financial system. A minor crash will only wipe out the first home buyers.

We need to first see an increase in unemployment and business failure to trigger that crash or a significant rise in interest rates. A tipping point will turn into a cascade from then on. Private debt will continue to grow if banks are willing to keep lending under such conditions. That maybe about to change if the ANZ is anything to go by.

Of course a significant government policy change could also trigger events.....phhhh....IF we had a government that willingly wanted change

RBNZ has to act as we are in critical time where government has failed.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.