Here's my summary of the key events over the weekend that affect New Zealand.

The international Demographia annual survey is out today for September 2016 and 7 of 8 New Zealand cities feature in its "most unaffordable" rankings. Demographia's data is a little suspect and a little dated but the overall general relationship is probably about right and it is the only international study in this detail. According to this metric, the most unaffordable city in their rankings is Hong Kong, followed by Sydney, Vancouver, Santa Cruz, CA, Santa Barbara, CA, then Auckland as #6. Last year Auckland was ranked #5. (You can find a more up-to-date review of "median multiples" for most New Zealand urban areas here and since the Demographia survey, we find the trend is turning.)

China's currency outflows have changed from a flood to a trickle with less than -US$1 bln in December and far less than the fast outflows reported in the previous seven months. New regulations and limits are having a dramatically quick impact on the ability of Chinese citizens to move money out of the country. That’s less than 2% of the record amount in September, and compares with an average outflow of -US$25.8 billion a month in 2016.

And staying in China, we are approaching the week-long Chinese New Year holidays, a time when banking system liquidity undergoes major stresses. This year their central bank has decided to offer major banks a 28 day liquidity facility to help them cope. It is hard to know why the regulator needs to provide such support when the banks know the stress period is coming. They should be making their own arrangements without using the public treasury.

In Europe, there is growing nervousness about real estate valuations. These are highly correlated to bond yields and as those yields rise, property valuation are very likely to fall. In fact, that is what the Europeans are now finding. A key indicator is now on the verge of falling below a technical threshold that has acted as a support since 2009, which would be a strong bearish signal. These market basics probably apply here too. The NZX Property index is now +13.6% higher than when it was formed in June 2015, and may come under similar pressures as yields rise.

Over in Melbourne ANZ is busy preparing its wealth business for sale. And all sorts of European, Japanese, and American businesses are lining up to bid to buy this division. The AFR is reporting that Goldman Sachs is doing the selling for ANZ, and that there is "pressure" to sell the life insurance part separately from the 'wealth' part. Last November ANZ group CEO Shayne Elliott said ANZ's NZ wealth business "will be considered separately" from ANZ's Australian wealth operations "during 2017."

In New York, the UST 10yr yield actually rose to over 2.51 on Friday, but then slid and will open this week at 2.47%.

Oil prices are a little higher today, now up to just over US$53 for the US benchmark, while the Brent benchmark is now just on US$55.50 a barrel. There was a big jump in the number of new wells brought back into production in North America last week. In fact it was the largest gain in 285 weeks, and the second largest in over ten years. Meanwhile, OPEC is claiming their output restraint is ahead of target. OPEC seems to be just making space for American frackers to profit.

The gold price rose just ahead of the swearing in of the new US Administration and is now just on US$1,210/oz. History shows that gold prices rise +15% in the first year of a new President in the US. But there are exceptions; that didn't happen for Reagan, nor for either of the two Bush's.

The New Zealand dollar has moved very little over the weekend and will open at 71.7 US¢. On the cross rates it is at 94.8 AU¢, and against the euro at 67 euro cents. The NZ TWI-5 index is at 77.5.

If you want to catch up with all the changes on Friday, we have an update here.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

64 Comments

interesting MSM are using table 7 to show Auckland as the 4th least(major) affordable city

is this something to be proud of with the resulting infrastructure and service problems, and now more costs for home owners to pay for too many people allowed in too quickly and the pollution that follows

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11786539

Based on one income of 83,000 when a couple buys with variable income. The other partner could be earning $120,000 giving a total of 203,000 so the survey is totally incorrect!

Ted the ratio is based on median household income.

Check with national government and like minded people with vested interest and will still come out with denial and manipulation (on unaffordable housing report).

How contrast government is with average kiwi to whom it is bad news but to government and their friends is good news - mission accomplished.

Election coming - wait and watch.

Auckland houses are the most affordable and are the cheapest ever in history (4.1% interest)

This demographia is totally false and based on one income which is a joke when a couple buy a home.

Dear God - please deliver us from Ted and his mindless spruiking - Amen

He is like a kid with a new toy.

But calling houses affordable based on a low interest rates makes this guy bloody dangerous.

The lowest mortgagee sales ever in New Zealand's history proves that houses are affordable!

Game Set and match!

To speculators, "investors" or foreigners, but not to Average Joe Kiwi.

Lowest Home Ownership rates in New Zealand's history proves you are wrong.

Are you implying that only a couple should buy a home? Then, once they've bought this home, both people should continue to work for the 25 or so years to see their mortgage out? I also suppose that they'll be able to keep that rate of finance for the whole mortgage never mind the next 12 months.

Sorry Ted, Auckland houses are NOT the most affordable or cheapest they have ever been in history, this is clear by any measure that you choose to use.

It is true that interest rates are low by historic levels, but the amount than first home buys have to borrow is significantly higher. If i look back to the first home we purchased we borrow 80,000 @8% (6400 interest pa), we were about earning 50k after tax (so 12.8%) , the same house is now "worth" 800,000+ if a starter has 20% 160,000 they will borrow 640,000 at 4% (25,600 interest pa), lets say they are earning 160,000 after tax (two highly paid starters) they are paying 16% in interest alone. to maintain parity they need to earn 200,000.

I guess when rates increase, as they are now, it will become even more of a struggle

Someone must be taking the piss. Nobody,not even a real estate agent,can be this stupid.

Exactly expert1 -Ted is obviously the first of the rank in the -psychological denyl there is a problem with housing affordability in NZ.

I predict that National will try to simultaneously deny and agree that there is a housing crisis. John Key used to be to do that sort of media gymnastics. I doubt Bill English can. Nick Smith will just go redder in the face to reflect the psychological pressure of holding too many opposing thoughts in his head.

The problem for National is some in their circles see rising house prices as a great wealth gift wheras others in the party agree with the majority of New Zealanders that their is nothing good about a basic need -shelter rising in cost faster than incomes.

Or............ could he be........... an alternative truther?

Or just trolling.

... you know those old westerns , the old movies , where you're looking down an empty street ...and the dust is blowing ... the old ramshackle red wooden buildings on either side are creaking eerily in the wind ... a tumble weed rolls across ... is it a scene of desolation , of emptiness ...

Well , it's kind of 'like that whenever Demographia release their housing affordability studies ... as amazing as Hugh Pavletich and the team are ... this government , whether it's Wild Bill English , or the Jolly Kid before him ... this government just aren't listening ....

.... a zephyr of a breeze ... and a tumbleweed rolls lugubriously across their empty heads ...

Let's hope they pay for that in the next election !

They wont pay for it , the Greenlabour coalition does not have a cohesive , clear or workable housing policy either

Gummy -Andrew Little (do you have a nick name for Andrew?) has given a robust response to Demographia -his street is full of activity -builders of scale, banners of foreign buyers, planners to eliminate land bankers, regulators to stop building material rorters.....

http://www.labour.org.nz/more_evidence_national_failing_in_housing

So far from Wild Bill and Red-face Nick it seems to be as you say ......a zephyr of a breeze ... and a tumbleweed rolls lugubriously across their empty heads ...

Well put Sluggy. Some people have their heads in the sand.

Time for a Vancouver Tax 15% in NZ on non-citizen buyers. Including foreign students & foreign temp workers !!! Yes they are foreign citizens also.

If it works great !

- Additional Tax revenue to pay for some of the infrastructure needed. ie Fix the sewage issue and rail etc

- This can reduce the amount NZ citizens will need to pay for this infrastructure.

- Housing affordability improves

If it doesn't work

- Additional Tax revenue to pay for some of the infrastructure needed. ie Fix the sewage issue and rail etc

- This can reduce the amount NZ citizens will need to pay for this infrastructure.

It is a Win/Win tax for NZ Citizens.

http://www.metronews.ca/news/vancouver/2017/01/12/greater-vancouver-hom…

Hey Joe, Yes I'm with you 100% on the introduction of the Foreign Buyers tax. Though now that it's becoming very obvious that these overseas investors have dominated the Auckland property market.

I think it would be ridiculous that any political party could ignore the benefits of such a tax to help boost our economy and to take the pressure of the housing market for the long term.

It also make me question just how many 'empty homes' are out there as well? Considering that the majority of Overseas Investors do tend to leave their properties empty to avoid the hassle of Tenants.

"It is hard to know why the regulator needs to provide such support when the banks know the stress period is coming. They should be..."

There is no free market left - only manipulation to keep a Ponzi afloat.

Last week, the central bank told financial institutions in China to balance their external flows of yuan. The directions, given verbally, require lenders to show at the end of every month that the amount of outgoing Chinese currency matches the sum coming in, said people familiar with the matter.

https://www.bloomberg.com/gadfly/articles/2017-01-17/what-doesn-t-go-ou…

Perhaps we could learn something there.

{kind=link}

The reversal of capital flows from China doesn't bode well for Auckland property.

Perhaps cessation of Chinese currency outflows is what Graeme Wheeler thought the market would find so "confusing".

Particularly the Real Estate market.

Going by the stone cold dead open homes I witnessed on the Shore this weekend, there must be some supremely "confused" REAs out there today.

China has ordered state firms to smash the decades-old system of providing cradle-to-grave welfare support, known as the country's "iron rice bowl".

http://www.reuters.com/article/us-china-debt-soe-insight-idUSKBN14700X

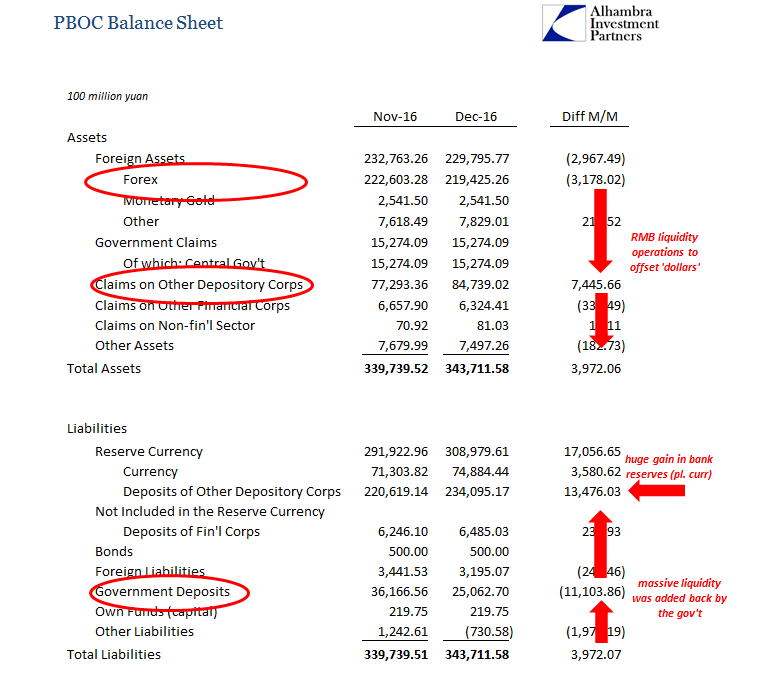

The amount of liquidity being added to the big Chinese banks has been astounding. The vast majority of it is coming from the PBOC itself. In July 2015, just before everything broke, PBOC funding of the Big 4 State-Owned Banks was less than RMB 100 billion. As of the latest figures for December 2016, it was RMB 1.17 trillion.

http://www.alhambrapartners.com/2017/01/20/china-rrr-surprise-but-no-su…

And staying in China, we are approaching the week-long Chinese New Year holidays, a time when banking system liquidity undergoes major stresses. This year their central bank has decided to offer major banks a 28 day liquidity facility to help them cope. It is hard to know why the regulator needs to provide such support when the banks know the stress period is coming. They should be making their own arrangements without using the public treasury.

Hmmmm....

The amount of liquidity being added to the big Chinese banks has been astounding. The vast majority of it is coming from the PBOC itself. In July 2015, just before everything broke, PBOC funding of the Big 4 State-Owned Banks was less than RMB 100 billion. As of the latest figures for December 2016, it was RMB 1.17 trillion.

Despite massive RMB injections, truly outrageous proportions, it has been easily overwhelmed by “something” else. According to traditional orthodox economic doctrine, that “something” does not exist. Under the closed system approach, there is only China being China, therefore everything is attributed to the PBOC no matter how inconsistent, with explanations reverse engineered after the fact no matter how absurd that makes them.

In reality, the PBOC is growing desperate because of what the mainstream refuses to see and understand, even though it is literally included and stated on its balance sheet. Read more and more and View PBOC balance sheet

{kind=link}

Stephen... Can u enlighten me how the PBOC providing liquidity to its Banking system has anything to do with its $US reserves..??.... a so called "dollar problem"

I've skim read thru those linked articles....

If I had to guess.... Maybe the Banking system in China is under stress from a run of bad debts..??

Maybe wholesale rates are rising simply because of perceived risk..??

When it comes to China...how can anyone really know..??

I will have a crack Roelof.

Credit already created in the boom times still needs the interest paid. Their economy is struggling to supply the yield required, so in part one way to pay is to sell down your assets. Bringing it back to money supply, (M.V)=i=P.Q will mean interest rates have to decline over time. But interest rates will climb to a peak during the rapid growth phase. China has passed that now, so is locked into the descending interest rate trend the rest of the world is locked into.

Declining interest rates and exponential growth of the money supply are opposite ends of the same stick.

The additional layer is that it seems the FED was supplying some of the money to prop them up, but now that tap has been turned off (at least in part) then they need other sources. Because the FED isn't printing, the shortage is pushing the USD up and the RMB down. Would you want to hold an asset denominated in RMB in this environment? Seems like sensible Chinese don't, and are selling off in favour of USD denominated assets.

PBOC is reacting by trying to hold up the value of the Yuan. Now they are trying to legislate outward flows.

Just my superficial thoughts on the matter, I would stand to be corrected if better evidence is presented.

thks Scarfie..

China is unique... Its' leadership can decree anything.

It still has massive trade surplus

Still has massive foreign exchange reserves.

Still has Capital inflows ( foreign direct investment )

Still has a , largely managed exchange rate

Capital outflows have slowed... like u say .. they have changed the rules..

They have a ticking time bomb debt bubble... and if it were a western country , we would all expect a financial crisis...and a CRASH..!! ... AND...who knows with China..??

Chinese leadership can dictate without to much fear of public reaction..??...

Aj.... great link to the barwerk article ...thks...

How do u find those Alhambra articles..???

I struggle to understand them most of the time... and often disagree with what they say..

The one that u and stephen linked makes no sense to me..??

I read those Alhambra articles a few times but over the years I'm starting to see where he is heading. I prefer him to Doug Noland who I find very dry. I like Bawerk the best.

Keeping it simple - when significant and growing Chinese exports to the debt funded buyers in the US prevailed, prior to 2007/8, the PBOC bought the USD export receipts from the domestic producers in exchange for unsterlised RMB. The situation in reverse demands the purchase/drain of RMB in exchange for delivered USD reserves, swapped or otherwise.

Yes... I get that. .... and... how is that a " massive dollar problem", as stated in that article..??

They say it is "something " that the mainstream refuses to see..??

China has huge FX reserves ...and being China, they can easily print money and spend into the economy... They are hardly going to run into the Capital flight problems of a banana republic..??

I would think unleashed inflation would be their nightmare and not so much the deflationary force of capital flight..???

The demand for USD (eurodollars in reality) is unending and apparently beyond global banking community balance sheet capacity - hence the very public negative basis swap quotes for YEN/USD. The PBOC is faced with creating a RMB fiat funded domestic growth scenario well beyond the realms of the USD reserves you refer to - hence they face a falling currency situation meeting the opprobrium of the US accusing them of premeditated currency manipulation. So called capital flight is associated with domestic Chinese banks paying up for scarce USD (inward investment?) for imported material goods demand - hence devaluing CNY. Inevitably rising inflation will be an issue as long as the currency falls in a desperate attempt to supplant one sure previous source of financing with another well beyond a few $USD trillion.

Thks for the response..

I still see the PBOC providing liquidity as a response to internal problems/liquidity issues , rather than anything to do with " massive Dollar problems which is beyond their capabilities of handling ", which the article alludes to..

Their problems come from their own flagrant debasement of their currency...especially post GFC..

https://fred.stlouisfed.org/series/MYAGM2CNM189N#0

http://soberlook.com/2016/03/chinas-wealth-management-products-q.html

(scroll down to see chart of China vs USA money supply growth )

As far as I know, China welcomes a weaker currency..??

I still see the PBOC providing liquidity as a response to internal problems/liquidity issues , rather than anything to do with " massive Dollar problems which is beyond their capabilities of handling ", which the article alludes to..

The demand for USD is certainly not diminished.

Banks create and destroy “dollars”, whereas the bond market trades mostly in dollars. Therefore, the bond market can only ever be a partial substitute no matter how large the potential size and depth of it. I will (and have) argue that is why in the overall context the US economy truly didn’t outperform Europe’s to any meaningful degree.

This contrast, however, is not a matter of purely historical debate. It is, as we see continuously, ongoing. Yesterday, Reuters reported (big thanks to Jason Fraser of Ceredex Value Advisors for spotting this) that the PBOC has started to encourage Chinese banks to issue more offshore bonds denominated in dollars. For the mainstream, this is a huge surprise and a confusing one; from the perspective of the ailing eurodollar system, it is merely the latest step in escalating desperation whereby the Chinese central bank cannot solve a monetary puzzle the mainstream doesn’t even consider as possible. Read more

Ted Talks ............... and everyone says its nonsense , but Ted Stanton makes a very valid point .

There are almost NO mortgagee sales whatsoever , which could mean that almost everyone who has bought a home and has a mortgage is either coping or getting along just fine

So his argument that Auckland houses are 'affordable " at 4% carries some weight , but this may not last .

A mortgagee sale only reflects a change in the conditions for the worse under which lending has taken place, so conclusion of more affordability does not logically follow a low rate of mortgagee sales.

The reserve bank has also recently changed the desposit requirements, which give a buffer to the mortgagee sale being initiated.

On top of this, the recent ramp up in Auckland prices has little correlation with the underlying Auckland economy, adding a further layer of meaningless to the conclusion.

If housing really was more affordable then more FHB would be buying homes and the home ownership rate would be rising not falling. Demographia and others who are saying that houses are unaffordable are right. Everyone else is in denial.

Surely mortgagee sales are a lagging indicator? I'd imagine it'd take months after the mortgagor defaults on a payment for the situation to wind its way through the bank's systems with several attempts to renegotiate and restructure the loan. I'd imagine the spike in mortgagee sales would take place 6 or more months after the market collapse/jump in unemployment/interest rate rise that ends up putting mortgagors in distress.

Spot on serious case of Denial ....

Chinas capital flight restrictions are working well, i wonder if we'll see the zombie hordes of chinese buyers in Feb like Ted said....

Not likely, considering how much Trump has been pushing for a 45% import tax. Why do you think those capital flight restrictions are in place.

No Fear - Going Gangbusters

Australian agents gear up for influx of interest during Chinese New Year

“I don’t think any lending restrictions will affect that market either. We have a lot of infrastructure set up today for Asian investors, and developers aren’t spending hundreds of millions of dollars on developments just hoping they’ll be able to sell; there’s a lot of confidence around.”

https://www.domain.com.au/news/australian-agents-gear-up-for-influx-of-…

Im not sure you will get much balanced information from a REA website

Agents like that will be the reason why the Australian housing market will eventually collapse.

The juwai.com survey found that 58 per cent of those Chinese New Year travellers are considering shifting to the country to which they’re travelling

Well I read another recent article that said only 30% of Foreign Buyers could afford to buy out right and the rest required a mortgage to supplement their funds. Considering that they've been clamping down on shadow banking a lot of foreign investors are going to become unstuck.

You'll probably see quite an influx of property coming on to the Auckland housing market in the next few months especially from the North shore area.

Nothing will change until someone has the GUTS to hit non-citizen buyers with a Stamp Duty like Vancouver has done.

Come on Greens / Labour... you want to win the election give us a reason to vote you in. Set a Vancouver Tax of 15% as one of your policies.

Doing nothing and turning a blind eye like National will not get you any votes.

What's wrong with banning foreign buyers unless they build new?

This is the Aussie policy and the NZ Labour party policy.

Whereas Joe Public the housing affordability policy you support is obviously the Canadian/Vancouver policy.

Both the Canadian and Aussie policies by themselves are not enough -I agree foreign buyers is an important issue -but it is not a silver bullet.

Auckland, Vancouver, Melbourne and Sydney all are well up there in the housing unaffordability charts.

Come on Joe, this is real misinformation. Labour's policy is to BAN foreign buyers from purchasing existing homes - they are not turning a blind eye.

LABOUR's Policy is very weak. As far as I am concerned they are not doing enough.

I looked at their policy and foreign students and temp workers can continue to buy existing properties. Vancouver tax would have the same result as a ban if you set the Stamp Duty rate high enough. Make it 100% if that is what you want.

http://www.labour.org.nz/housing

Here it is

"Ban foreign speculators from buying existing homes

Labour will ban non-resident foreign buyers from buying existing New Zealand homes. This will remove from the market foreign speculators who are pushing prices out of reach of first home buyers."

They have it all wrong. The focus should be on NON-Citizen not Non-Resident.

Under Labour Foreign Students and Foreign Temp Workers can buy existing properties. LINZ showed us they make up a good chunk of the buyers.

We need to follow AUSTRALIA's lead. Foreign Students and Foreign Temp Workers are both included as Foreign buyers.

http://www.sro.vic.gov.au/foreignpurchaser

Foreign purchasers

You will be a foreign purchaser if you are a foreign natural person, a foreign corporation or a trustee of a foreign trust.

Foreign natural persons

You are a foreign purchaser if you are not:

•A citizen or permanent resident of Australia,

•Or a New Zealand citizen with a Special Category Visa (Subclass 444)

You want them to water down their current position of a complete ban back to a more non-citizen friendly tax instead?

I am completely against Non-Citizen buyers pushing home ownership affordability out of reach of everyday kiwis. The higher the Stamp Duty the better I would say.

It is not doing NZ society any good and will only lead to long term pain in the future for hundreds of thousands of kiwis.

Can someone explain what the benefit to New Zealand for a non resident, foreign individuals buying a house in New Zealand.

As New Zealand was in part built on immigration, i think we should enable permanent residents to buy before they become citizens (it takes time) but if they are not going to live here and add to society, what is the benefit?

If there is NO benefit why are they allowed to buy at all?

Ideology.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.