Here's my summary of the key events over the weekend that affect New Zealand, with news that Warren Buffett is front and centre today.

But first, sales of new single-family houses in January in the US were +5.5% higher than the same month a year ago. But markets had expected an even better result, so there was a sense of disappointment about this result.

Also a bit disappointing was the latest American consumer confidence reading by looking like it has topped out. It also did not show a rise in inflation expectations.

In his annual report to shareholders, billionaire and investment icon Warren Buffett reported higher profits even as operating income slipped. He was his typically optimistic about the prospects for American business generally. However, in advice to savers and investors he delivered a black eye to the managed funds industry, urging ordinary investors to buy plain-vanilla index funds. He highlighted a bet he has on the matter with a large hedge fund manager which looks like it will pay off big-time. He also had harsh criticism of the current fad of companies who report earnings stripped of certain elements, claimed to be one-offs.

In Sweden, that have abandoned the centre-left Government proposals for a new tax on banks. It was strongly resisted and fears grew that Swedish jobs would be moved off-shore. Instead, they are to move ahead with a plan to force healthy banks to pay into a fund to cover competitors who fail. (Over the weekend, Sweden also abandoned a Green Party plan for a 'kilomtere tax' on heavy trucks.)

In Melbourne, there is some serious landlord pain. Landlords have been hit by steep land tax increases from soaring property values, in some cases more than doubling tax bills and making investments uneconomic. In the State, retail tenancy laws prohibit landlords from passing on land taxes to their tenants, unless the tenant is a listed company.

And staying in Melbourne, the ex-boss of ANZ has finally sold his Toorak home for AU$13 mln in a long-running saga where the original buyer from China failed to get approval to make close the deal. Mike Smith settled for a A$2 mln haircut.

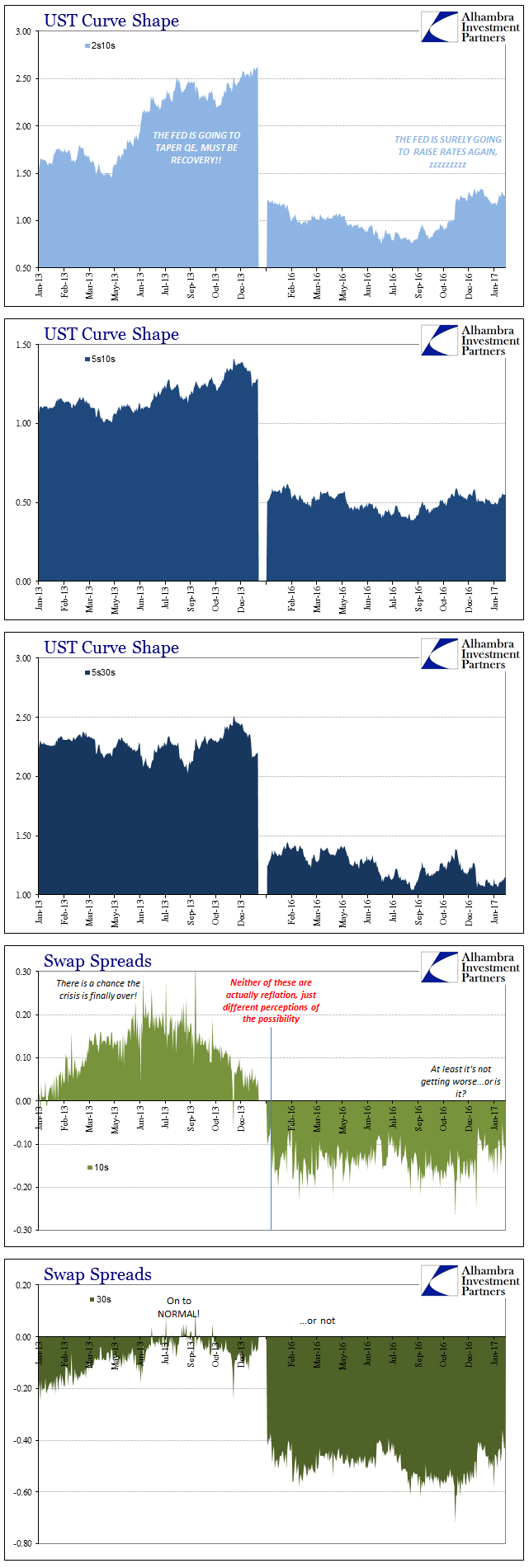

In New York, the UST 10yr yield is falling and now at 2.32%. There seems to be renewed downward pressure on interest rates. Bond traders are showing more concern about politics while equities traders like what they see on earnings. We should also note that the risk premium for investment grade Australasian debt continues to fall, as measured by credit default swap spreads. Bank wholesale debt transaction costs are going down. This mirrors the impressive position NZ sovereign debt holds in the same markets. We are pitched better than most large countries including the USA, Germany, Australia. and in a group with Switzerland, Sweden and Norway

Oil prices are lower and now just under US$54 for the US benchmark, while the Brent benchmark is just under US$56 a barrel.

The gold price is up a little further at US$1,257/oz.

And the New Zealand dollar will open the week at 72 USc. On the cross rates we are at 93.9 AU¢, and against the euro at 68.2 euro cents. The NZ TWI-5 index is now at 77.5.

If you want to catch up with all the changes on Friday, we have an update here.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

8 Comments

The managed funds sector in the US is a giant scam. Although people buying US indexes should be wary right now as expect performance is low.

Not surprised about the increase in house sales in the US. People are starting to recover and many people have dug themselves out of negative equity post GFC, and those that have built up unsecured debt have either paid it off or gone bankrupt already.

they are to move ahead with a plan to force healthy banks to pay into a fund to cover competitors who fail

How could that not be full of awful incentives?

We should also note that the risk premium for investment grade Australasian debt continues to fall, as measured by credit default swap spreads. Bank wholesale debt transaction costs are going down. This mirrors the impressive position NZ sovereign debt holds in the same markets. We are pitched better than most large countries including the USA, Germany, Australia. and in a group with Switzerland, Sweden and Norway

Are you sure you are not witnessing another example of a technically inexplicable impossibility that persists in the IR swap market - namely negative spreads to USTs? View chart data

{kind=link}

China

It means that Xi Jinping’s regime, facing acute challenges due to global economic and political upheavals (Trump, shrinking trade and protectionism) and the threat of instability at home (social unrest and intra-regime power struggle) has abandoned, at least temporarily, attempts to get control over the debt problem. The trend is confirmed by the data for January 2017, which shows new loans (TSF) hitting a new monthly record of 3.74 trillion yuan.

http://chinaworker.info/en/2017/02/21/14162/

From the Melbourne article on land taxes: "They were now weighing options and might look at divesting out of some assets to allow them to keep servicing their loans, he said."

We should keep a close eye on the effect of property prices and rents over there. Fall out for real estate could be a big-un.

I would bet a fair number of young Kiwis who are in the right sectors of employment are keeping an eye on this. Already you can get a somewhat better deal on salary vs. rent/price in many parts of Melbourne, so if things start tipping, you could see a fair few Kiwis jump over there again rather than stick around in Auckland.

No OBR style Greek "bail in" is acceptable to Germany. Read more

I wonder why?

If Italy or Greece (any country) were to leave the Eurozone and default on the target2 balance, the rest of the countries would have to make up the default according to their percentage weight in the Eurozone.

As of December 2016, if Italy were to exit the Eurozone, Italy would owe €356.6 billion to Germany, Luxembourg, and a couple other small creditors.

What’s the likelihood Italy could ever pay back €356.6 billion? Read more

Is this the reason gold is up 9% y-t-d?

Also a bit disappointing was the latest American consumer confidence reading by looking like it has topped out. It also did not show a rise in inflation expectations.

Elsewhere, central bank benchmark statistics supposedly underpinning inflation are being revised down.

Last week MPs asked four Bank policymakers how they could be so wrong year after year. They asked the question after the Bank’s monetary policy committee revised down the natural level of unemployment from 5% to 4.5%

It is easy to see why they would be perplexed. The level was 7% in 2013 when the current governor Mark Carney arrived and declared that he would need to consider raising interest rates once unemployment dropped to 7%. The thinking behind the policy was that once unemployment hits its natural rate, the labour market will be so tight that workers can almost walk into a job and in their newly confident state, start to bid up their wages. Read more

State agents certainly have no intention of disrupting capital's rising share of GDP taken from labour - a guaranteed recipe for greater populism?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.