In a world in transition from being American-centric to one that may become China-centric, New Zealanders will need to stay up-to-date with news out of the Middle Kingdom as it influences us.

And 'influence' may be the key phrase here.

To stay on top of these issues, this weekly specialist 'Top 10', curates China news that New Zealanders should know about. Please contact me if you have items that should be in this series. [ david.chaston@interest.co.nz ]

And to start this edition,

1. 'Systemic fraud'

Competitive publishing is an issue every university faces and every staff member feels the pressure of. There is nothing quite like it in academia. But generally the system works because those involved recognise that this competitive instinct provides an essential drive towards a greater good. But take away that mature outlook and things fall apart quickly, as the NY Times pointed out in China.

Having conquered world markets and challenged American political and military leadership, China has set its sights on becoming a global powerhouse in a different field: scientific research. It now has more laboratory scientists than any other country, outspends the entire European Union on research and development, and produces more scientific articles than any other nation except the United States.

But in its rush to dominance, China has stood out in another, less boastful way. Since 2012, the country has retracted more scientific papers because of faked peer reviews than all other countries and territories put together, according to Retraction Watch, a blog that tracks and seeks to publicize retractions of research papers.

Now, a recent string of high-profile scandals over questionable or discredited research has driven home the point in China that to become a scientific superpower, it must first overcome a festering problem of systemic fraud.

Most researchers in China's universities won't be guilty. Like everywhere else, most will be working with normal, sensible boundaries. But when you get a fringe that is growing, and infecting top brains, their's is competitive corruption that smears a whole education system. But let's not forget, we have had similar issues in the past. We grew up and out of them. Let's just hope China can gain that same maturity in those wobbly sections of its tertiary institutions. (And hope we can maintain our balance; we have our own issues with climate sceptics undermining science as one glaring western example.)

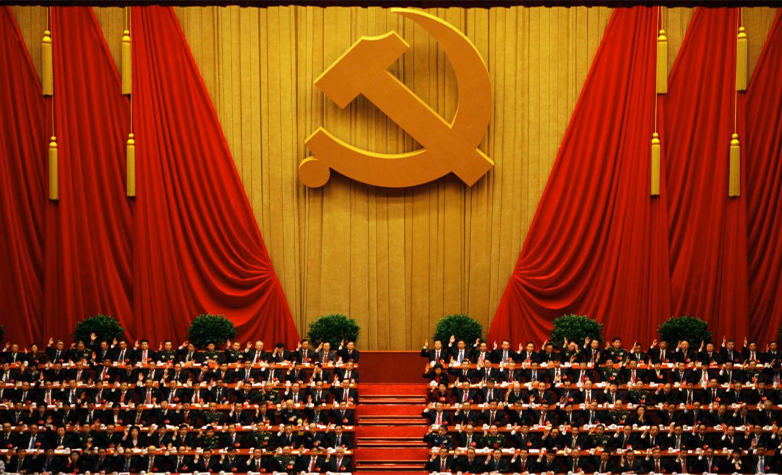

China is increasingly smug as it looks at the state of western democracies. I doubt it sees much threat as strident "eastern European" partisan behaviour infects the west (undoubtedly curdled by Russian efforts).

As parties in the West increasingly represent special interest groups and social strata, capitalist democracy becomes more oligarchic in nature. The cracks are beginning to show, with many eccentric or unexpected results in recent plebiscites.

Under the leadership of a sober-minded, forward-looking CPC, Chinese-style democracy has never been healthier and China has absolutely no need to import the failing party political systems of other countries.

After several hundred years, the Western model is showing its age. It is high time for profound reflection on the ills of a doddering democracy which has precipitated so many of the world's ills and solved so few. If Western democracy is not to collapse completely it must be revitalized, reappraised and rebooted.

3. How its neighbours view China

China's power rise, be it social, political, economic, or military, is viewed with some trepidation by its neighbours. A new survey of seven Asian countries (including Australia) puts those concerns into focus. Interestingly, among those countries surveyed, Australia was most sanguine. It's people were the least worried about China's rise. Japan, South Korea, Vietnam and India all have major concerns. The Philippines and Indonesia have concerns but to a lesser extent. The only area Aussies worried more about than Filipinos and Indonesians was the military expansion.

Australians are most positive about China’s economic growth; by a three-to-one margin, more people say China’s economic growth is good for Australia than bad. In contrast, only 20% of Indians see China’s economic rise as a good thing for their country.

4. Getting control of non-bank financial risks

President Xi is on an endless wack-a-mole track by "reforming" China's financial industry by applying prescriptive rather than principled-based regulation. He has found it easier to control the banks (most of which are SOEs after all), but given the entrepreneurial Chinese spirit, much harder to restrain the other intermediaries that pop-up in response to bank restrictions. Now they have a very large credit-creation machine running in parallel to the banking sector, essentially undermining their overall 'restraint' goals. Their answer? More, tighter prescriptive regulations. You can imagine where that will lead ...

China’s cabinet-level cross-agency committee for overseeing the sprawling financial sector is taking shape. The first task of Financial Stability and Development Committee, whose members include representatives from the People’s Bank of China and other financial regulators, will be to draft laws and regulations to clearly state the responsibilities of the central bank and the regulators in combating ballooning financial risks, a source told Caixin. The committee was created in July to lead and coordinate efforts among the central bank and other financial regulators. The aim, as central bank Governor Zhou Xiaochuan put it, is to contain risks in four areas: shadow banking, the asset management industry, internet finance companies and private financial conglomerates.

5. 'Restructuring' with Chinese characteristics

The level of corporate borrowing is monumentally large in China.

China’s corporate debts totalled US$18.3 tln at the end of last year. That 's more than 165% of the country’s GDP. It is much lower in the US at 72% and it is only 53% in Germany. Believe it or not in New Zealand it is a mere and virtuous 39%.

Much of it funds state enterprises that are unprofitable - borrowing to pay the groceries. That is unsustainable, even in the short term. Something will have to give fairly soon, one would think. To cut the debt burdens of these state-owned borrowers, China is resorting to “debt-for-equity” swaps. China is also encouraging private investors or financially viable SOEs to take stakes in troubled state firms through “mixed ownership” reform. But this risks infecting good companies with the bad ones, carrying real 'public health' risks.

And restructuring under their bankruptcy laws is an opaque and murky process. Bondholders in a recent case took a -78% haircut and had zero representation in the proceedings. Bond investors beware.

The more Beijing imposes micro-control on how Chinese companies operate, the more they will be regarded overseas as unreliable partner. How could you trust an undertaking, even a contractual promise from a Chinese company, if it can be over-ridden by a Beijing directive or change-of-heart? Dealing with Chinese companies carries substantial risks, ones we tend not to see. Anyway, that is the argument of Frasier Howie.

It could be argued that the state has saved private companies from themselves. They were often said to be buying dubious overseas assets at inflated prices, but was that really true? Many of the headline deals were for quality assets and ongoing concerns, not just speculative ventures. Since these are private companies, would it not have been a good time to make a clear distinction between public and private-sector risk?

Instead, the clampdown and direct interference in private-sector dealings shows that there is no clear distinction between the state and private companies. The state and the Communist Party have never relinquished control over any aspect of society, regardless of how open China appears now. There may be private ownership but there is never full private control. The state has shown itself more than willing and able to directly interrupt the operation of some of China's largest private companies.

7. Standing up to China-directed influence in our universities and beyond

The Five Eyes intelligence partnership is very focused on the projection of Chinese soft power in the region, especially the use of students to influence independent thought and work being done in our universities. These concerns are being talked about openly in Australia but our security authorities are watching here as well. We may be the smallest of the Five Eyes intelligence partners but are seen by analysts as a "soft" target for Beijing's growing "soft power" diplomacy.

Just how concerned the Aussies are is evidenced by a speech the head of their MFAT foreign affairs department gave to an Adelaide Confucius Institute last week. She pulled no punches when she told her audience, "The silencing of anyone in our society from students to lecturers to politicians is an affront to our values."

But this influence is much broader than just Chinese students in our schools and universities:

Ms Adamson's public appearance also provided a rare window into the Government's thinking about China's One Belt One Road initiative, which is an ambitious plan to build a vast network of new trade routes across the globe.

When asked about the initiative, Ms Adamson said Australian companies were welcome to participate, but the Federal Government was still examining the detail.

"We know from our neighbours in the South Pacific in particular that infrastructure projects can come with very heavy price tags and the repayment of those loans often can be absolutely crippling and that's why you'd expect Australia has an interest in governance arrangements," she said.

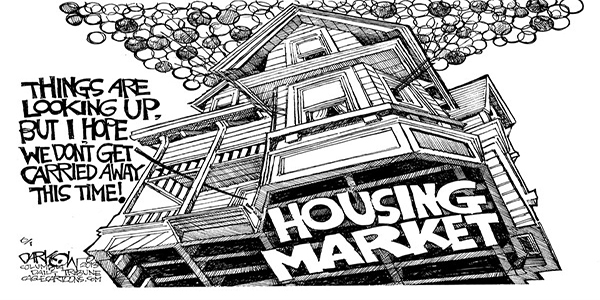

President Xi specifically referred to housing affordability and housing market stability in his 3+ hour opening speech to the Party faithful and pledged that authorities will help meet demand by adding more supply of homes.

"Houses are built to be inhabited, not for speculation," Xi said in his address at the 19th Party Congress Wednesday in Beijing. "China will accelerate establishing a system with supply from multiple parties, affordability from different channels, and make rental housing as important as home purchasing."

Home prices rose in fewer Chinese cities in August and declined in some of the nation’s hottest markets as authorities rolled out a series of restrictions to tame the property boom. Funds flows offshore have abated while much better capital gains have been achievable in domestic Chinese markets. If prices start falling everywhere at home, there will be more incentive in the future to seek such gains offshore.

More regulation of their rental housing market is on the way too. News of the latest government effort apparently turned investors bullish toward property management company stocks.

More evidence is emerging that Chinese banks have been gamed (or secretly enabled a channel to circumvent housing regulations) by mortgage borrowers. But the activity is now so big they are needing to restrain themselves. "Consumer loans" have been used to fund minimum deposits to meet tougher mortgage LVR regulations, regulations designed to dampen their housing market speculation.

Now some banks are requiring proof that consumer loans are being used as claimed.

“I am afraid a considerable part of consumer loans has flown into the property market,” said Iris Pang, an economist with the Dutch bank ING. “If you look at the structure of the consumer loans on the mainland, you will find it strange because a lot of them have extremely long loan tenures, like 10 to 20 years. What makes you need 20 years to pay back a consumer loan that enables you to buy a television? It is very likely that the money is spent on houses,” she said.

China is growing up, and readers here will know that a lack of proper reform has produced some huge distortions. The most well-known one is the huge trade surpluses being built up. Another is the huge excess on business borrowing/debt, much of it inefficiently invested. But a third major one gets relatively less attention, but is the result of the other two - a massive internal savings rate, said to be as high as 45% of GDP. Much of that is because China has very poor levels of social investment. People need to save aggressively there because the access to good health, education, pension and old-age services are very basic still. That impulse at the family level is causing great economic distortion.

In my recent visit to Beijing I heard some horror stories about their access to quality heath-care and education. I have read about some dreadful aged care provisioning.

A lack of confidence that these services will improve to the levels most people expect, and stay improved at a satisfactory level, will keep families saving aggressively to cover these life events. That won't make the quality of them better by themselves, but money can buy priority access in an emergency. It is a system fraught with corruption and inequality.

China has moved relatively fast in extracting itself out of widespread poverty. People appreciate that. But it has raised expectations about future lifestyles and life risks. No-one wants to go back. A consequence is a savings rate that is unnecessarily sky high which allows credit distortions to bloom and has people frantic for building wealth as fast as they can and certainly they know each person needs to do that faster than their peers of they will be left behind. That drives impulses that are not sustainable for everyone. The real estate frenzy is a consequence, one that simple regulation can't solve on its own. It also generates a culture of disrespect for the civil law.

As Brad Setser explains it, they have a 'savings trap' (a concept Kiwis will have a hard time processing). It is just another China distortion.

But I don’t yet see much sign Chinese policy makers are prepared to make the needed policy changes quickly enough.

I worry that will leave China in its current high savings trap. A trap that more or less means the economy is structurally short demand and only is in equilibrium when the government or firms borrow too much domestically, or when it borrows too much demand from the world. A trap that means China’s savings surplus either is used inefficiently at home, or dumped on the world. A trap that leaves China perpetually at risk of tightening too much and seeing its economy stall—absent a return to the very large pre-crisis external surplus.***

A better macroeconomic equilibrium—one with less credit and less (but hopefully better quality) investment, and much less savings—is possible. But getting there will be difficult, and take far more aggressive reforms—and by reform, I mean reforms that expand access to social insurance and raise transfers to low-income workers financed through progressive taxes, not just reforms to state banks and state firms—than China’s leaders have considered to date.

I consequently hope the IMF’s recommendations for bringing China’s savings rate down get the same kind of attention as its concerns about China’s credit excesses.

We are aiming to produce this review weekly. If you have items you think should be included, please contact us (the details are above).

25 Comments

A commentator on Al Jazzerra recently said that nothing happens in China without the Chinese Govt being involved.

I think we should be very wary of this regime and keep our distance.

Like accepting their having control over major basic industries here, such as Silver Fern Farms.

I'm assured Jian Yang left his post in a Chinese spy school, escaped the Communist Party, and came to be an MP serving on NZ's Foreign Affairs, Defence and Trade, Commerce, Transport and Industrial Relations and Health and Science select committees - without the involvement of the Chinese government. This surely means the commentator is in error.

another good article please keep them coming!!! This is the stuff i want to read on this site and in depth on the NZ economy...

Yes a good battery of articles and I assume you mean focused on China with some relevance to the NZ economy

South China Morning Post reports that the Chinese pension fund has us$317 billion to invest with a large percentage likelt to go offshore.

That amount can buy a lot of love anywhere.

China central bank chief warns of ‘Minsky moment’

https://www.ft.com/content/4bcb14c8-b4d2-11e7-a398-73d59db9e399

That article is behind a pay wall

just google it to get around pay wall.

The Chinese cannot right now de-dollarize, and so the best option among only bad options appears to be do whatever it takes to stabilize CNY if in the longshot possibility it restarts “dollar” inflows.

http://www.alhambrapartners.com/2017/10/19/officially-a-no-growth-world/

I am indebted to Interest.co.nz.

It is amazing how much indebted the World is.

I am amazed at how little a "Minsky Moment' only happens after a boom, but he was little recognised for this until a Bust..

I am amazed at how often History can repeat itself, but financially savvy people keep selling it and Mugs keep buying, like there is no tomorrow.

The thing is its like a game of musical chairs, all the gamblers and parasites believe they wont be the last one standing, some other "mug" will be. Quite how this is a great way to run an economy / financial system is beyond me........

Well according to this recent FT article, China seems to be extremely in debt mainly due the GFC where its manufacturing economy started to dissolve which is understandable since there was a huge drop off in demand.

So to try to stimulate their economy to give the appearance of growth, they ploughed in to easy credit going from 6 trillion dollars in debt to 28 trillion!

Lets hope they can fight corruption if the really want to get out of their debt spiral.

FT article: https://www.ft.com/video/e049ab63-a72a-41e6-af42-8c32d2aa87e1

One could also add in the trend towards a cashless society: http://www.atimes.com/one-third-chinese-see-completely-cashless-society…

One obvious corollary of a cashless society is total transparency (to regulators and Gubmints) of 'cashless' i.e. electronic trx.

Can't think what That could lead to.....

And David Goldman ("Spengler") has a wide overview of China vs America here: http://www.atimes.com/article/western-contempt-china-turns-panic/

Plus, an initial look by well-informed analysts at the Labour/NZF/Greens coalition. http://www.atimes.com/new-zealand-pm-change-another-nip-bud-asia-pacifi… Not a happy clappy take: there's more 'let's Don't it' than the reverse....

Mobile payment apps (Alipay and WeChat Pay) are from China's largest ecommerce and social messaging platform. China has adapted to cashless transactions, much like Kiwis adapted to EFTPOS. However, EFTPOS is now clunky and QR Code (an older technology anyway) works far better.

http://www.npr.org/sections/alltechconsidered/2017/06/29/534846403/in-c…

I'm skeptical on China continuing to boom.

I don't believe they are sufficiently 'different' or unique to avoid the kind of downturn or crash that every booming economy has eventually faced.

The question is when, not if.

Incorrect! They have only just begin - Here's why China is buying up so much of Australia

https://www.cnbc.com/2017/10/22/heres-why-china-is-buying-up-assets-in-…

That is disturbing news.

The politicians will look back and say "Oh, but how could we ever have known?" - all because it was benefiting them in the short term both personally and politically.

[Satire warning]

China is at a huge disadvantage compared to the West because of its lack of diversity. They don't have much diversity at all. This means they cannot think up new ideas. They all think as one and just do what they are told. This is very good for getting things done but not much else. It may look like they are doing very well but any day now you will see, boom, no more new ideas. They have millions of people doing research and experimenting, just looking stuff up on the Internet or just trying different things and choosing things that work. This is not a new idea. It's just same old.

Chinese democracy is remarkable too because of its lack of diversity. It only has one party. However when it comes to democracy this is a strength. Western democracy now has too much diversity. Western democracy used to be stable and strong (although very evil) with a two party duopoly which was very similar to Chinese democracy. Now the West is breaking apart as people stop thinking as one. Too much diversity has weakened Western democracy. People forming their own parties, having different ideas about things, no longer voting for the two party duopoly, will be the death of the West. The Chinese laugh at this in unison. If they had a vote it is certain they would reject Western democracy. So certain that no vote is even needed or will ever be needed. China is a political utopia and if you don't think so there is a strong possibility that you are mentally ill or have been watching too much RT.

The Chinese will soon become more mature and stop cheating, of this I am certain. We used to cheat all the time so it's all good. It is well documented, don't forget. Anyway now we have something equally as bad, some people ask too many questions and refuse to just believe. We have sceptics and this is equally as bad as cheating. These sceptics they are infected with a mind virus. Possibly Certainly of Russian origin. Again this is well documented. Everyone knows this. There is a strong possibility they are mentally ill. Sceptics are everywhere. If we were strong like China we would lock them up for their own safety.

If you visit China you will love China and come home and wax lyrical about China.

Enjoyed it all but the 1st paragraph is perfect. Next time I see the word 'diversity' used by an academic this paragraph will return to haunt me.

It is surprising China is doing so well with little gender diversity - if only they had a female leader China would be on an equal footing and able to compete with Germany, UK and New Zealand.

One suggestion on the sources of all your briefings is that have at least one or two points that are from non-western media.

I watch news from both sides and am astonished all the time how both can spin different shit out of the same thing.

#7 I do really enjoy teaching int'l students from both mainland China and Singapore. Early in my career, I recall one student among many in a large lecture theatre, who just smiled and smiled throughout my lectures. His smile was truly infectious... and his delight/amusement at the material was a complete curiosity to me. The topics included a lot of 'real world' case study material about politics/politicians in environmental management.

As the semester ended he approached me to explain how "amazing" he found the lectures and how much he had enjoyed the class because of the "truth speaking" which made him "very happy".

My first thought was of John Clarke; "We Don't Know How Lucky We Are".

Doddering democracy. How quaint. Democracy washes its laundry in public and the interest groups in society shift and change in an adaptive manner, for the most part. So there is lots of apparent turmoil on the surface reflecting the issues of the day.

Un-democratic systems operate largely behind closed doors. Decisions are made, it is not clear who by. People are told what happened and why by the official mouthpieces. Dissent is discouraged by personal ruin, imprisonment or death. The less undemocratic deny you a place at the government trough, the more undemocratic put on a show trial for "corruption".

The media (this site excluded) rather confuse the key issues. For instance, the election of a Trump like figure is what you get if you ignore the plight of a large enough portion of your citizens. It is democracy in action, not democracy in decline. Same in NZ; Jacinda and Winston are the champions of those who feel they have missed out and that something should be done about it.

The adaptive survive.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.