Auckland's housing market may have a recent history of second winds, but ANZ NZ's economists are not expecting it to surge forth again from its current slowdown.

In their latest New Zealand Property Focus report, ANZ's economists suggest households are coming to terms with what is sustainable for the Auckland housing market given affordability limits are stretched.

"Although the Auckland housing market has a proud history of second winds, we do not expect it to take off again. Consistent with the recent slowing, more moderate rates of house price inflation are now expected by households, consistent with continued low rates of house price inflation - perhaps just slightly higher than what we are seeing currently," ANZ's economists, led by chief economist Sharon Zollner, say.

"This reflects households coming to terms with what is sustainable for the Auckland market going forward, with affordability limits now reached. Investor caution alongside these affordability concerns will keep the market from getting a second wind. Although house price expectations have lifted a little, we are not seeing the type of sharp lift seen in late 2014, which presaged a sharp lift in actual house price inflation."

ANZ is New Zealand's biggest mortgage lender with housing loan exposure of more than $75 billion.

'Eye watering prices'

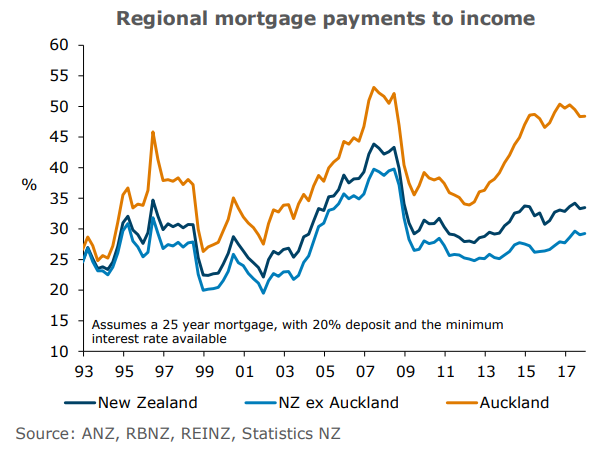

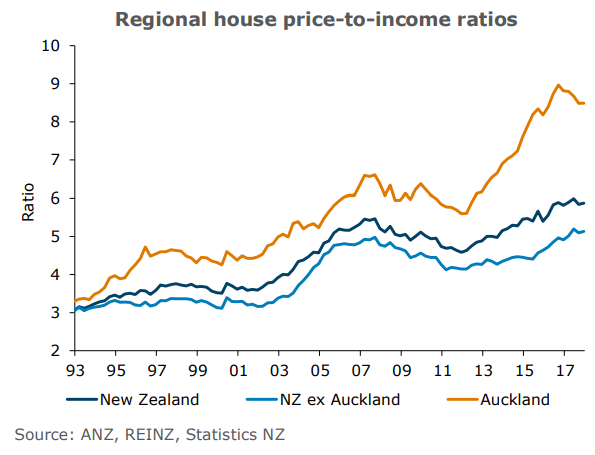

ANZ's economists note a key headwind in Auckland housing is affordability, or lack of it, with "eye-watering prices" holding the market back from resurgence. They note the house price-to-income ratio rose from 6 in 2008 to 9 in 2017, a 50% increase after adjusting for household earnings.

"This has moderated recently, but only modestly. However you cut it, Auckland house prices have increased to the point where they are unaffordable for many. A house price of 9 times income is a massive stretch for those on the average income, let alone those who are earning less," ANZ says.

"Mortgage repayments required to purchase the median house are 50% of average household incomes - the same level that prevailed at the peak of the last interest rate cycle, when floating mortgage rates were 11%. Should interest rates rise, this would increase. And resurgence in Auckland house prices would put further pressure on this metric, which we don’t think is plausible, affordability has its limits."

ANZ's economists point out that in most other parts of the country affordability issues are not so bad.

"Outside Auckland, the average house price-to-income ratio is 5, with house prices having broadly kept pace with income growth since 2008. House prices have barely risen over the past decade in some regions. While house prices in Auckland have doubled over the past decade, house prices have risen less than 30% in some other regions, including Manawatu-Whanganui, Taranaki and Southland, which equates to a real increase of only 1% per year on average. Mortgage payments are 30% of average income outside Auckland. This proportion peaked at 40% in 2008. While servicing this would certainly have been difficult for some, history suggests this ratio has room to go higher."

Interest.co.nz's latest Home Loan Affordability reports show Papakura and Franklin are the only parts of the Auckland region considered affordable for typical first home buyers. The only significant centre outside Auckland where housing is unaffordable for first home buyers is Queenstown.

Interest.co.nz measures changing housing affordability for typical first home buyers by tracking the monthly changes in the Real Estate Institute of New Zealand's lower quartile house selling price, the average two year fixed mortgage rate charged by the major banks, and the median after-tax wages of people aged 25-29 in each region.

Those figures are then used to calculate how much of a typical first home buying couple's after-tax wages would be swallowed by the mortgage payments on a lower quartile-priced dwelling in each region. The mortgage payments are considered unaffordable if they take up more than 40% of take home pay.

'Investors will continue to be wary'

Meanwhile ANZ's economists say for investors, property is a less attractive investment in Auckland than in the rest of New Zealand.

"During the strong Auckland housing market upswing, investors were willing to accept pretty low rental yields, relative to prevailing interest rates - presumably in anticipation of future capital gains. But the prospects for that have now been tempered. We believe investors will continue to be wary around the country, given possible changes to government policies, but particularly in Auckland," ANZ says.

"Going forward, the divergence that has opened up between Auckland and the rest of the country is expected to continue to ebb. But how - and when - this happens is uncertain. In previous episodes, it has sometimes taken a decade or more for regional divergence to be eroded. Then again, we haven’t seen a divergence as large as this in recent history, so maybe things will play out somewhat differently."

"Nonetheless, we expect this catch-up dynamic will continue to transpire gradually over the next 5-10 years, through a mixture of subdued Auckland price pressures and catch-up growth in the rest of New Zealand. Overall, house price inflation is expected to slow towards 2% over the next few years."

The latest monthly Real Estate Institute of New Zealand sales figures show the national median price was up 3.9% in February, year-on-year. The Auckland median price rose $31,000, or 3.7%, to $858,000. Although the 1600 homes sold in Auckland during February was 32 more than in February 2017, more than 2000 homes were sold in the month of February from 2012 to 2015, with 1819 homes sold in February 2016.

'House price inflation has found a floor and it’s probably just as well'

According to ANZ's economists other reasons why house price inflation won't gather pace from here, besides affordability, include; tightening in debt availability continuing, net migration being on the wane, and the effects of low interest rates in spurring housing market activity having largely played out, with interest rates unlikely to drop from here.

"We will watch changes in government policy closely, given their possible effects on market sentiment, activity and prices."

"But ultimately, we think house price inflation has found a floor. And it’s probably just as well. Any resurgence in house prices would increase the risk of a sharper correction - especially in Auckland. Debt levels are high and the Reserve Bank is on the watch for any housing market risks that may emerge and leave the financial system vulnerable. This is particularly relevant for Auckland, where house prices and debt-servicing costs remains lofty relative to household incomes. In light of this, we think that the Reserve Bank will take a cautious approach to gradually removing loan-to-value ratio (LVR) restrictions, with no policy changes expected in the near term," ANZ's economists say.

73 Comments

Yep already at peak rent. Wait for the new fuel tax and the new rates charges which are coming to a house near you soon on the new CVs.

Investors load your selves up, surely there will be some new factors to replace cheap overseas money and debt stacking legislation.

Phasing out internal combustion engines will have an effect also.

ANZs Chief David Hisco confirmed in July 2016 that NZ property is overcooked here; http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=116…

He says its peaked in Oct 2017 and conditions difficult for FHB here; http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=119…

Here we are in March 2018, Is NZ property still overcooked? (YES) Are conditions still difficult for FHB? (YES)

It's just not obvious to the greedy

how much of the divergence is due to foreign funded buying, which we will never know as it was kept secret by the last government and this government has not addressed in the way of a register.

Less than 3% is the general consensus.

haha that 3% of people without a NZ tax code, not non NZ, you might want to check how the national party got the form worded to hide the real figure.

BUT why has labour not had the form redesigned to capture the real figure is my other question

No need to design the form when they are being BANNED altogether.

They campaigned hard on the foreign buyer ban but 6 months on they've gone very quiet. I suspect the recently signed TPP and lobbying from various groups may have put the brakes on this ban making it into law.

If its not in place by Sept then I would say its not happening at all.

I think it is just being bogged down by the democratic process. The current coalition is not as good at circumventing that as the previous one.

They haven't been quiet at all it is definitely happening.

lol, we all know how the National government duped the public..

Do you think that's were this government got its ideas from?

the previous government had no ideas

dp

Due to the new fuel tax, I suspect we will now see more of renter's income diverted to improving Auckland transport corridors etc., thus away from darklord pockets. There is a limit to what renters can pay.

This should be filed under department of the bleeding obvious (except to missed the point and his groupies).

I have climbed back down the ladder ,looked below the inflation floor and found a snake,But,but ,but there is a housing shortage ,now I am told affordability is an issue

"House price inflation has found a floor and it’s probably just as well'

Isn't that meant to say: " House price inflation has found a CEILING...?

The ANZ report says floor...

Good, well balanced article.

Interesting mortgage payment to income graph, showing this ratio being not as bad as it was in 2007-2008 in Auckland and being much better today than 2005-2008 in the rest of the country

not as bad, but on much bigger loans

That's right, it's because of lower interest rates and if they go up it could start to hurt. Still what matters to most people is the "right now", how much cash do I have in my wallet? and the answer is "more than in 2007-2008 in Auckland and considerably more than in 2005-2008 in the rest of NZ.

Longer and larger loans means increased risk exposure. Needing two people working full time to just about service the loan in todays low interest environment is a recipe for disaster over an extended period.

People are desensitised to risk to a dangerous extent at the moment.

Agreed!

Well there not a cat in hells chance that China is going to lift it's capital flight restrictions at any time in the near future. Now that Mr Trump has finally put the US economies money where mouth is.

At the risk of trade tariffs will cause China to double down their efforts to restrict their capital from moving abroad. So that will again will further dampen Auckland's housing market. Sorry RE's you're just going to have to drop your commission rates.

2004/5 phase of cycle in Palmy... 2 more years to run at least. Very good buying

Yes, I read the ANZ report as follows:

"We appear to have reached maximum extractive capacity in Auckland. However, there is plenty of unused extractive capacity to go in the regions, and we expect to take full advantage of this."

The banks are the main beneficiaries of rising house prices as their income goes up with the increase in household debt. They are the primary mechanism whereby lower interest rates are transferred into higher capital values.

However, in the larger world, the tide has turned:

https://fred.stlouisfed.org/series/USD3MTD156N

Now you're starting to get it!

While aucklanders find finance drying up those fhbs in Palmy will be offered big mortgages as banks try to fill their orders by targeting secondary cities

One of the best kept secret in Palmy is it's wind!

it's no secret that Palmy's very own MTP has plenty of wind......

Agree with Simon. For a university city with excellent amenities, Palmerston North offers stunning value.......

Very livable 3-beddie family homes start at about $375,000.

Transport is no problem - and it’s a mere 90 minute drive to Wellington.

TTP

Friday funny?

Why is everyone making so much noise about fuel tax ? ...10c equates to the price of a coffee a week, on average it is only $4-5 more per tank ...! your supermarkets are occasionally giving away 40C per litter ...!!

However, More than half of the cars and trucks on the road are company vehicles - so it is an extra tax on Business !! -- so, practically it will have minute effect on ordinary households who use their own cars. We just want to know where that money will go and what it will be spent on?

Some of us here have been saying that the new Normal is low price inflation in Auckland for the next few years at around the rate of inflation and more in some special and attractive properties - so the ANZ report just confirms what our market experience taught us over the years and what we concluded from information and trends on the ground. Even the latest consumer survey pointed to that.

Affordability will gradually improve in the next few years as we are in a booming economy ATM . There will be more people moving up the ladder from average wage to much better pay with abundant opportunities to up skill and better jobs, .... almost like it happened in previous cycles. The house price train has slowed down and waiting for the passengers to catch up - and they'd better do because this train has previously showed us that it doesn't wait too long.

Like it or Hate it, this phenomena has been consistent during past boom and bust cycles and there is nothing so far suggesting that it won't repeat itself ! other than in the fertile imagination of the DGMs ...

It is a great time to spot and drive a bargain this winter for serious home buyers and lock in a low interest rate fixed terms for few years - Why? because Some people will need to move on and sell in a subdued market, so this is a window of opportunity before the train moves uphill again - expect to see average and median prices move up by 2-5% pa in Auckland, But Bargains will be easier to find going forward.

some decent points - but as ever fuel is a higher % of lower income household spend - and increased core costs for business is often passed on in increased prices. I would also note that you are not hearing any protests from trucking firms - who will fill up out of auckland and simply drive on through!

i dont remember the 17% interest rates - but certainly remember the pain of 10% when the last labour government left office - and less than six months in the signs are not great that we wont be seeing a jump in inflation that will lead to a significant rise in interest rates - which with the massive mortgages around now will cause unbelievable pain.

The high % wage rises being talked about for Nurses /Teachers and other public service workers - in reality will help very little as by the time a corresponding drop in Working for families and Accommodation supplements are factored in - there will be little in any changes in overall household incomes - so whilst i applaud removing people from middle class welfare - it wont soften the pain of interest rate rises

I do agree with you on overall prices - as the demand aspect is increasing faster than supply - and very unlikely that supply will be significantly increased in the next few years given the skilled labour shortages - if you can afford it with a 2% rise in interest rates - never a bad time to buy your own home!

low price inflation in Auckland for the next few years at around the rate of inflation and more in some special and attractive properties - so the ANZ report just confirms what our market experience taught us over the years and what we concluded from information and trends on the ground. Even the latest consumer survey pointed to that.

Sounds like you've created your own schtick by combining the persons of a desk editor, a Barfoots figurehead, the local MP of Blandsville (where prices have made its inhabitants feel "rich"), and the commission salesperson focused on closing the deal.

However, closing off with consumer sentiment is smart. Without it, the economy would be toast. You're likely not to really understand how that this is inextricably linked to house prices and asset bubbles, but trust me, it is.

Its another straw on the camels back of Aucklanders. A lot have any financial excess is getting sucked out in rent. Ill bet the petrol stations outside the super city boundary are back slapping themselves as they just have the golden ticket to a massive increase in sales as people chose to drive past the competitor inside the Auckland limit.

I would expect a lot of earnest conversations between trucking firms and truck-stops along the lines of:

TF: tell me, Ms TS CFO, wot sites you gots outside the tax grab boundary?

TS: well, there's X, Y, Z and AA for starters - they'll need another bay or three - you're the seventeenth request this morning. Can you see your way to a leetle trade - we'll supply you exclusively, 5% off average Sector A pricing - if you come up with $100K up front for capex, repayable over 5 years?

TF: 5%...oooh, Standard has offered 6% and only $50K down, and they will throw in five tanker trailers - fill up outside the boundary, tow 'em in, bingo.. Can you meet that?

TS: Yer breakin' my heart, baby, but yes. Deal?

TF: Knew yer'd see it my way. Deal.

Arbitrage across tax boundaries is the third-oldest profession.....

.

@kpnuts, interesting post,do you think that current low interest rates are reflection of last national Govt policies or being driven by financial climate in the western world mainly USA and EU?

Not related directly to this topic , there is data supporting the suggestion that House prices continue to rise in regions and cities like Tauranga , Hamilton, Hawkes Bay etc.

Is it simply the lag effect or has the unaffordability in Auckland and Wellington created conditions where people are moving out and leading to rise in second tier cities ? Any thoughts?

The continued rise in values of the regions is a normal occurance due to:

1) Some people moving out of Auckland into the cheaper regions

2) Investors not finding the capital or cashflow return in Auckland but being able to get a bit of both in the regions

3) Some migration into NZ settling into the regions

Uphill leg "regions have played catch up with Auckland"

Downhill leg "regions will play catch up with Auckland"

to all the non-believers!!!

https://www.newsroom.co.nz/2018/03/22/99198/governments-early-move-on-a…

Hallelujah, praise Twyford, it's not in the Bays.

Amen. It's neither in 1071 nor 1050.

for your folks sake, I wouldn't want prices to crash, else with personalities like yours, I wont be surprised you'll will end up committing suicide ..

Amen

DGZ, Ex Expat, are prefabs the problem here or your "unique" perception of the people that might inhabit them?

I am all for quality prefabs that are built properly but not the dodgy ones. However, I don't agree with putting them on a street full of early 1900's villas and bungalows like the one I am living in (NIMBY). It wouldn't look right otherwise ;-)

DGZ, I agree with you there has to be some uniformity in design with existing structures. I honestly think it's less likely there will be weather tightness issues after what the country has already been through. The Government through Kiwibuild would surely be in a position to claw back should there be. Let's collectively hope it works as it should :)

If I had to pick a street in Remuera for them it would be either James Cook Crescent or Maui Grove as they are the classic plaster disaster type streets. The entire Remuera Rise building, the Oakridge Apartment block, and the surrounding houses are all either leaky or plaster with no cavity.

"plaster disasters" are everywhere. Even the ones that have had remedial work completed, in my view, still carry the stigma based on their appearance. Its symbol of the desire for size over quality.

In a weak market, these are very hard to shift without heavy discounting involved.

Better to have dodgy, small prefabs than it is to have dodgy McMansions, apartment blocks and now, it seems, Middlemore Hospital. I believe that in a few years we are going to have a leaky homes Mark II, produced by the cowboys around now and for the last few years, except it could make leaky homes look like a bad paint job. At least small prefabs won't cost so much to fix/replace.

Retired-Poppy, I can't recall voicing an opinion on prefabs, but in my experience nothing built to a bare bones price is going to be something I want to live next to. On the other hand, the occupants might well be charming. In my time overseas I soon learned to separate manners from money.

Ex Expat, what did you mean by "Hallelujah, praise Twyford, it's not in the Bays" then? If that's not an opinion on prefabs then I don't know what is. The Joe public aren't yet privy to the designs yet you've already formed an opinion. Do you want to see the affordable housing crisis sorted or not? Its everyones concern there is currently a glut of unaffordable homes. Kiwibuild is an initiative that is so logical it should have consensus across all political divides but yet in this forum because of close mindedness, it doesn't.

Retired-Poppy, prefab is a method of building, it’s not inherently poor quality. However when the main criteria is low cost I’m not picking it will be anything I want to live next to.

As for the affordability issue, Twyford and co had years to formulate detail on their policy, to find the magic solution that the market couldn’t. My friends that have built and are building now can’t see how it can be done. Maybe he is the genius, but I suspect he’s faking it in the hope that he makes it. It’s logical that there’s no consensus across the political divide as there’s no sign the solution has been found. What worries me most is that we have a long history of building rubbish and whatever they do will be around for a long time. All the more reason to be happy that I’m not living next to it.

Ex Expat, you missed out the one key ingredient of the construction process - efficiency by way of automation. The less cowboy carpenters involved in the prefabrication, the better. In this instance I would expect to see nothing less than quality, just on a mass scale. I am confident this won't be a problem :)

I'm Mortgage free and have cash in the Bank. I'll be one of the last ones standing.

I am also mortgage free on my family home in DGZ, and also have cash in the bank but probably not as much as you, as I need to maintain my rentals. I will be one of the 2nd or 3rd last ones standing.

Double-GZ

you commented "as I need to maintain my rentals". That sounds like your properties are negative cashflow?

That sounds like I am a good responsible landlord, putting in pink batts, replacing old carpets and organising chem-wash etc etc. I actually look after my tenants so that they can have a place called home.

A noble farmer caring for his livestock. Salt of the earth.

Double-GZ, why have you got an unencumbered home?

The financial advice I can give you is that you should have borrowed against your property or properties to purchase assets that produce income!

You are not making the most of your financial situation!

TM2, speaks volumes about your personal debt to equity ratios. It's your bank plus unexpected events that control you, not the other way round. Its now an vulnerable road you follow.

" There will also be concerns at a new town of cheap houses crammed in a corner of a suburb where the average house price is well above $1m and, unless the density is controlled and the design is pleasing, it won’t be long before the Facebook crowd starts to mumble. "

This better be good .. it will be the first example of the kiwibuild --- better not be a slump !

The Big devil will be in Small details

Unlike the mass produced monolithic eyesores in areas such as 1071 and 1050, I am confident Kiwibuild prefabs on Unitec land will have no weathertightness issues to contend with. So much has been learnt from this ticking time bomb that it would prove political suicide to add yet another one!

I would prefer that Kiwibuild was delayed on the basis there were issued to be ironed out rather than done in a day like National Party are demanding, resulting in a mess.

True re the plaster eye sores. With nice homes now reaching over $2 million consistently many of those monolithic monsters have been reclad or redeveloped. Thank goodness for owner occupants and strong house prices.

ha-ha :) you wish! As we head down the other side of this bubble the leaky building time bomb will once again float to the surface under the guise and pressure from ever more critical buyers! The luxury of choice is once again presenting itself.

A member of my family got caught with one. It cost them six figures to do a patch up job from the inside and nearly ruined them financially and emotionally. It was not done as a complete reclad and it was nothing more than the driest leaky home in the street once it was finished.

Without a property inspection the new owners bought it in late 2015.

Interesting... let's wait for the anouncement and then... see how it can be done, both from a traffic perspective and a NIMBY obections point of view

Unitec will not get off the ground for a long time due to the many issues that the site supposedly has!

The sewer and stormwater issues, something to do with planting’s, the no. That they want to put on will have major problems and also the huge issue in regards to the traffic and neighbours revolting!

Twyford is an absolute dreamer!

For Aucklanders who are owner occupier buyers and purchasing property at current prices, spending 50% of a household income on debt servicing seems high to me. How much higher can it go or have we reached the upper limit? I thought traditionally bankers use to allow for 33% on debt servicing. How would these households cope with higher cost of living (such as fuel tax), or possible interest rate increases. Isn't there a rising risk of higher inflation in NZ (and consequently interest rates in NZ) with the US Fed raising their interest rates?

The only way to afford buying at these levels is to have a a lower mortgage and a larger deposit - which might come from the bank of mum and dad ...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.