Here are the key things you need to know before you leave work today.

MORTGAGE RATE CHANGES

BNZ today reduced its 2yr 'special' to 4.29%, mid-pack. It also reduced most of its standard rates, again to unremarkable levels.

TERM DEPOSIT RATE CHANGES

No changes here today.

RETAIL SALES GROWTH AVERAGE

Stats NZ headlinded its release as the "largest quarterly percentage lift in retail card spending since 2010". And it was for the quarter to September. But really, all that is because spending on petrol leaped, juiced along by big tax increases in Auckland, and higher prices due to a falling currency. But looking at the data without petrol, the rises were quite normal, up +4% year-on-year. Petrol was up +12%. One 'positive' is that the extra $200 mln being spent on petrol isn't restraining other spending yet. Hospitality spending in September was up more than +7% compared with the same month in 2017.

TICKING HIGHER

Growth in the tourist accommodation industry has been hard to find recently, mainly in the shadow of a banner 2017. But even though August is in the depths off the offseason, a spark back to life was seen with total guest nights up +3.4% year-on-year and the best rise since March. The average occupancy rate was 36.4%, the best August ever. The areas with the strongest growth in guest nights in the past year were Christchurch, Queenstown-Lakes, and Rotorua. Auckland region’s guest nights fell -1.4% following a record August 2017 year.

COST OF DOING BUSINESS

Today saw some regulatory action aimed at the personal loan industry, and especially the loan shark end. And the Commerce Commission has issued a warning to Rapid Loans NZ Limited about a loan it issued to a vulnerable borrower. It failed to comply with the lender responsibility principles set out in the Credit Contracts and Consumer Finance Act, according to ComCom. Rapid Loans NZ is a division of a Gold Coast company formed by ex-managers of Cash Converters. We plugged a $1000 loan into their on-line calculator, with weekly repayments over 3 years. The effective cost of debt for the loan is 93.6% on a per annum basis. It will be debatable how effective 'warnings' are when the incentive for the lender are so high. "Cost of doing business."

LOWER MILK PRICES FOR FARMERS

Fonterra says it's now forecasting a milk price for farmers this season of between $6.25 and $6.50 per kilogram of milk solids, down from its previous forecast of $6.75. International supply growing faster than international demand is a key reason. Compare all dairy companies here. Today's dairy derivatives market indicates that WMP prices may fall -1.1% at the next auction next week.

THE COST OF H&S

The Commerce Commission today filed civil proceedings in the High Court at Auckland seeking financial penalties against electricity lines company Vector for breaching its network quality standards. These arose from outages during 2015 and 2016 storms and Vector's decision to prioritise safety of its people by avoiding working on live lives wherever possible, which led to extended outages. Vector is now seeking to get the standards it works to modified because it doubts it can continue to meet them. It seems to be caught between liabilities of H&S legislation, and community standards for recovering from storm outages.

REBOUND

In early trading today, both the Hong Kong and Shanghai stock markets are up strongly, each gaining about +1%. The NZX will likely close down about -0.3%.

SWAP RATES UNCHANGED

Swap rates are virtually unchanged today. The UST 10yr lower at 3.21% with the UST 2-10 curve narrowing -4 bps to +32 bps. The Aussie Govt 10yr is at 2.76% (down -1 bp), the China Govt 10yr is at 3.66% (unchanged), while the NZ Govt 10 yr is at 2.70%, and up +3 bps. The 90 day bank bill rate is up +1 bp to 1.89%.

BITCOIN UNCHANGED

The bitcoin price is now at US$6,594 and down less than +1%.

NZD FIRMER

The NZD is firmer again today, now at 64.9 USc. On the cross rates we are also firmer, even if marginally, at 91.2 AUc, and 56.4 euro cents. The TWI-5 is up to 69.

This chart is animated here. For previous users, the animation process has been updated and works better now.

Daily exchange rates

Select chart tabs

19 Comments

Real Estate .co.nz figures

The stock of unsold property available across New Zealand continues to climb and now stands at 34,665. A sharp rise from the total of 33,488 (29th September) (a significant rise of 3.4% in 11 days). These numbers are rising far faster than previous predictions (admittedly by me) of 35,000 unsold houses by mid November and 36,000 by Christmas. It is possible that we could see 35,000 before the end of this week?

Auckland's unsold listings now stand at 13,054. (the pace having slowed a touch as the FBB deadline gets closer) but still on an upward trajectory.

NB. These figures don't account for withdrawals which (B&T figures currently running at around 33% since February).

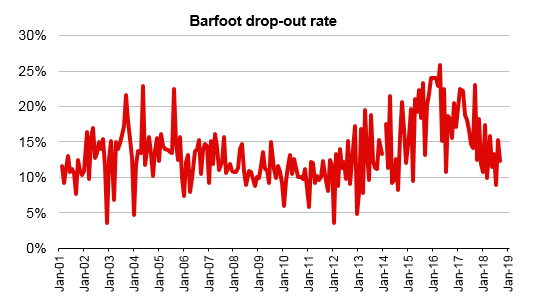

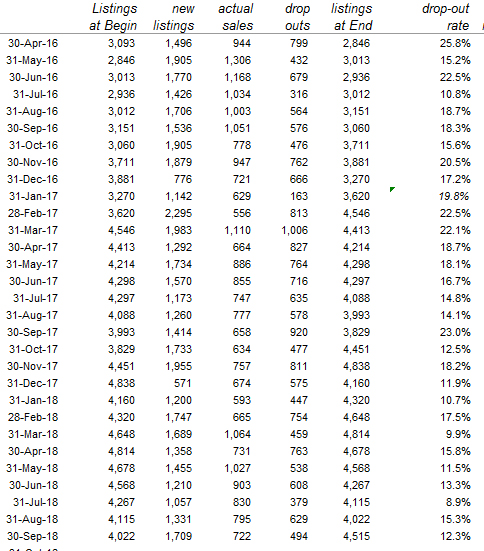

B&T's drop out rate is not running anywhere near 33%. Here it is tracked monthly over the past 17 years. In September 2018 it was 12.3%.

{kind=link}

https://www.interest.co.nz/images/barfoot-dropout-rate.jpg

The drop-out rate reconciles the formula: starting listings, + new listings, less sales, less ending listings = drop-out rate.

Sorry but that's completely incorrect David. Here are their numbers since 28th February 2018. New Listings, Total Sales and the total balance of their register as at 28th February and 30th September. I posted this on 2nd October, it's from their own published figures. The formula you currently have are incorrect.

'And a little look at the numbers shows a failure rate of 33% of all listings.

Barfoot & Thompson Figures.

March 1689 new listings, 1064 sales

April 1358 new listings, 731 sales

May 1455 new listings, 1027 sales

June 1210 new listings, 903 sales

July 1057 new listings, 830 sales

August 1331 new listings, 795 sales.

September 1709 listings, 722 sales

So 9809 New Listings since March 1st and Sales of 6072

Total stock at end of Feb = 4648 Total Stock at end of September = 4515.

So stock that's been available since March 1st = 9809 + 133 (difference between total stock at end of Feb to today) = 9942 Total Listings

6702 Sales / 9942 Total available stock = 67.4% sales ratio. Or 1/3 of the market is failing to sell and being withdrawn from sale. That's an expensive marketing adventure for all the failures!'

Are you taking the number of new listings minus the number of sales and assuming everything else is dropping out?

Read the full comment and think about it a bit, but don't expire too many cells you've got the whole day ahead of you. If you list more than you sell and the total stock levels decline then the rest of them do what?

Did you see what happenend to the FAANG stocks over night... A wonderful lesson in the dangers of leveraged trading is unfolding before our eyes. Sears below is another good example of how leverage can get people in trouble as well.

David has provided the numbers above, and you still haven't accounted for multiple listed properties. You might want to pick another battlefield.

And loving the US market meltdown.. all my hedges are rocketing up. The puts in QQQ I bought on Thursday have already doubled in value. Just wish I had got more.

Sorry Pragmatist but David has provided no numbers whatsoever - just a graph and no detail. I have provided detail and numbers, As for multi agent listings they are a negligible influence on the numbers I've given as very few sellers (possibly 1-2%) will spend the cash to list twice.

Glad you're doing well on the meltdown though, it was a good night last night, it does look like the leveraged trading into the FANG's is now starting to unwind.

Oh well.. we tried.

Pragmatist, from Davids graph, how does one explain the higher dropout rate occurring during boom years? There's some skewed analytics going on here. This dropout rate only looks good for Barfoots during the quieter times as a proportion of total (and growing) listings.

You'll have to ask him, not something I've looked into. But given a choice between trusting David or Nic, I'll take David's numbers any day.

Because the calculations are wrong.

Here is a snip of part of our data:

https://www.interest.co.nz/images/barfoot-dropout-rate-data.jpg

{kind=link}

with all data items from Barfoot releases.

Hi David

Thanks very much for sharing the numbers, which are all the same numbers as I have used.

I can see that you have been calculating the 'drop out rate' as a percentage against the total listings at the start of the month. It's the wrong calculation which is why your 'drop out' rate is high when then market seems buoyant and low when the market is poor. It's probably been wrong for years.

What you should be doing is comparing the volume of sales to the volume of withdrawals (drop out) to get a picture of the rate of withdrawal against actual sales. Happy to discuss if you want to give me a call.

In essence we have been arguing different things, but my calculations will provide a more accurate depiction of reality about how many vendors are failing.

Those numbers will keep climbing:

- FBB

- FHBs holding out for KB

- investor interest waning (poor yields, tenancy law changes)

To what extent will listings halt their rise in response to this waning demand? And to what extent will seller expectations shift lower?

Trademe Rentals for Auckland are also on the rise.

5th October there were 4013 homes listed to rent

10th October there are now 4110 homes listed to rent

A rise of 2.4% in available rental stock in 5 days!

Could the derivatives market be the next subprime? £41 Trillion is up for negotiation under Brexit negotiations, with 90% of large European firms 'hedges' going through London. EU GDP is predicted to be around $18.8 Trillion dollars this year, so 'swaps' represent more than double the GDP for the whole of Europe.

https://www.telegraph.co.uk/business/2018/10/09/bank-england-fires-warn…

'The European Union is the second largest economy in the world in nominal terms and according to purchasing power parity (PPP). The European Union's GDP was estimated to be $18.8 trillion (nominal) in 2018, representing ~22% of global economy (Nominal global GDP).'

Look at NZ's horrid cost of fuel:

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

Much much lower in other 'new world' western democracies. Similar to the UK but their salaries are higher and public transport much better

Sears has been "lost" for years.

If you're ever in the US and enter one of their stores you'll see why.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.