So how bad is it at Fonterra?

We were hoping to find out at least in part on Thursday of this week, with the release of the embattled dairy giant's financial accounts for the year to July 31.

Now, after a delay, we are left waiting for an extended period. All we know is the result will be out by the end of this month.

What I would say from experience is that delays of this nature involving the auditors are never good news.

And what I would further say, although I am only speculating, is that such delays generally occur when the auditors are in disagreement with the company over asset valuations: IE the auditors want bigger write-downs.

Fonterra's already indicated about $860 million of write-downs. If there have to be bigger write-downs than that, well, where does this start to take us?

And the other point is, regardless of what the final wash-up is for the financial year ended July 31, what happens in the new financial year that's recently begun?

Are the write-downs that Fonterra's going to take for the past financial year going to be sufficient moving through this new year? Or are we actually at the start of a cycle that will see more of these write-downs occurring. And what will that do to Fonterra and its farmer shareholders?

ANZ agriculture economist Susan Kilsby has already articulated a view that more write-downs will be required.

So, there may be more write-downs to come in future.

But, as well, will more write-downs than Fonterra has previously signalled now be required to be made for the financial year that recently finished?

There's a lot of interesting dynamics coming into play on this one.

Auditors PwC are having their last go-around with the Fonterra accounts. They are due to be replaced for the 2020 financial year by KPMG.

It's fair to say that PwC will not want to leave any stone unturned in their last time around with the Fonterra accounts. Nor will they want to be open to any criticism that sufficient write-down action may not have been taken.

This would be I dare say particularly the case with the Financial Markets Authority now taking an interest in Fonterra and its write-downs.

The FMA as ever is not saying much about it, but this is the official word from it:

“The FMA has received a complaint from a Fonterra shareholder. The FMA has engaged with Fonterra’s management and asked for information regarding concerns about Fonterra’s recent announcement and its pending financial statements for the last period. As part of its monitoring of financial reporting, the FMA had already contacted Fonterra to discuss it’s 2019 year end statements, just prior to its recent NZX announcement (write downs reported in media on Aug 12). The FMA has been in ongoing dialogue with Fonterra around its financial reporting, and Fonterra has been cooperative with the FMA. We are now considering what further information may be required to assist our enquiries.

It is not unusual for the FMA to engage with FMC-Act reporting entities when their financial statements have unusual features, such as large asset write-downs.

The FMA has also relayed the complainant’s concerns about Fonterra’s financial statements over the past four years to CAANZ (Chartered Accountants Australia New Zealand/NZICA), which is the frontline regulator of licensed audit firms. We will engage with NZICA over this matter and provide support where needed.”

So, that's another interesting bit of backdrop to this developing saga.

Fonterra in its statement last week announcing the delay of the financial result stressed that the change in reporting date was "unrelated to any discussions with the Financial Markets Authority, recent speculation about further material asset impairments, or other announcements".

But it all adds colour to a very colourful picture.

In the financial year recently completed Fonterra was under pressure to reduce debt. It had a target of $800 million of debt reduction by the end of the financial year.

It has confirmed it did not meet that target. But it hasn't said to this point how much it missed by.

I would stick my finger in the air pointing in the general direction of the wind and suggest it might have fallen something like $200 million short.

Such a figure would roughly equate to Fonterra's failure to find a buyer for its hugely problematic 18.8% stake in Beingmate.

Remarkably, Fonterra's now trying to sell the Beingmate shares on-market, something that would take a very long time to achieve. This course of action tells you two things: 1. This was a truly awful investment. 2. Fonterra needs the money, however it may get it.

In terms of Fonterra's debt, here from the horse's mouth (taken from the 2018 annual report), is what Fonterra targets:

The Board closely monitors the Group’s leverage ratios. The primary ratios monitored by the Board are:

–– Debt payback. The debt payback ratios are adjusted for the impact of operating leases. They are calculated as 1. Funds from operations divided by economic net interest-bearing debt, and 2. Economic net interest-bearing debt divided by earnings before interest, tax, depreciation and amortisation (EBITDA).

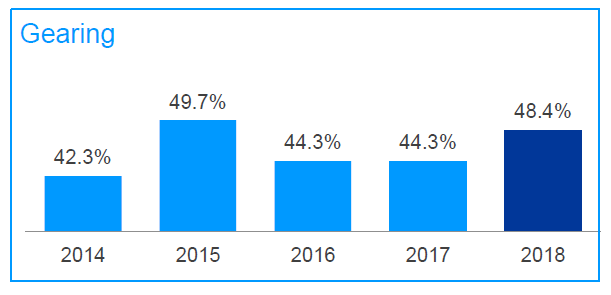

–– Gearing. The gearing ratio is calculated as economic net interest-bearing debt, divided by equity plus economic net interest-bearing debt. Equity is as presented in the statement of financial position, excluding hedge reserves. The gearing ratio as at 31 July 2018 was 48.4% (31 July 2017: 44.3%). The Group is not subject to externally imposed capital requirements.

Fonterra aims to be within 40% to 45% in terms of its targeted gearing. So, it has fallen fairly well outside of that. The below graph, from Fonterra presentation materials, shows how it has gone against the target in the past five years:

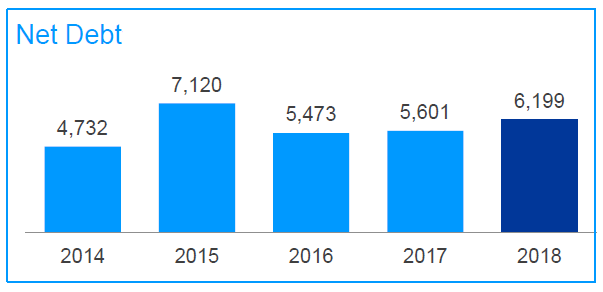

And if that all looks a bit abstract, there's the below graph that gives everything a slightly more temple-pounding feeling, with some dollars and big numbers.

In Fonterra's accounts you will find a bit of a range of figures for 'borrowing'.

The gearing ratio that Fonterra goes by is based on its preferred measure of debt, which it styles as "Economic Net Interest Bearing Debt".

Fonterra's explanation of this is that it "reflects total borrowings, less cash and cash equivalents and non-current interest-bearing advances, adjusted for derivatives used to manage changes in hedged risks". Slightly confusing, but here's the numbers, and yes, those are shown in millions of dollars, so the net debt as a July 31 last year was a touch under $6.2 billion:

It might not be helpful to digestive patterns to know that as at the half-year point in the 2019 financial year the Fonterra net debt stood at $7.4 billion, with a gearing of 52.5%. It needs to be stressed, however, that given the seasonal nature of the dairy industry, the debt figures DO blow out during the course of the first half of the year. But still...

Fonterra said this about the debt position at the half-year point:

This [52.5% gearing figure] is up 0.9% on the same period last year and is due to the higher debt at the start of the year as opposed to us needing greater levels of debt during the first half.

So, how bad is it going to be, when we do get the result announced, and what's going to happen?

To go back to the write-downs as they were originally announced, I have to say, I nearly fell off my chair when I saw that $200 million had been earmarked as write-downs on the New Zealand consumer businesses. The point to note here was that Fonterra had netted off the $100 million gain (excellent sale result) on the sale of the Tip Top ice cream business. So, if you excluded that windfall, it meant Fonterra was taking a $300 million hit on the value of domestic businesses.

Now, we all know about Fonterra's travails as being a tale of overseas misadventures. To hear that the company's now getting hit at home, elevates concerns about its future, I think, to an entirely different level.

And it is interesting in regard to this to get a bit of context from last year's Fonterra annual report. In the section on intangible assets and goodwill Fonterra had this to say (I have put some parts in bold text to give my own emphasis):

Consumer and Foodservice New Zealand

During the year, margin compression and operational challenges have negatively impacted the returns generated by the consumer and foodservice business in New Zealand.

These challenges have impacted the forecast cash flows used to support the carrying value of the consumer and foodservice New Zealand CGU.

Fonterra has identified a number of strategic and operational initiatives that will, over time, refocus the business to generate margin growth and improve productivity.

These initiatives are underway however their long-term nature means that not all the benefits are expected to be realised within the three-year business plan timeframe.

As a result, the business plan has been extended to a five-year forecast period. The cash flow forecast shows a higher rate of growth in years four and five compared to years one to three, as the benefits of the strategic and operational initiatives identified are achieved.

The margin growth and productivity improvements in years four and five are determined by assessing the expected financial impact of the initiatives identified based on past experience, the competitive landscape and market opportunities.

How do you read that? Remember, this is LAST year. What I see is a company extending out its forecast period in order to show the business turning around and therefore justifying the asset valuations the company has. Is this/was this wise?

Regardless of how much rosier Fonterra was earlier seeing the forward results for these NZ businesses, presumably a year on it is being forced to face facts that the earnings are not in fact going to match the valuations Fonterra has for these assets.

But it's interesting that this was an issue identified a year ago. And now a year later we are seeing the write-downs.

It does all go into the mixer in terms of one wondering just how much more various Fonterra assets might need writing down.

Whatever the result announced by Fonterra, whenever that is, the increasing conclusion I come to is that we are really only in the middle of a process with Fonterra.

There's more to be dug up, I'm afraid. And where does that leave Fonterra as a business at the end of it? And where does it leave the farmers?

But wait, there's more...

There is much more to be said about Fonterra and the whole situation.

I'm going to have at least one more go at this with another article before the result is announced, so, look out for that.

Businesses don't go bad overnight.

The time between when bad decisions are made and when the full ramifications of those bad decisions hit can be a surprisingly long time.

In looking back at Fonterra, I think a clear case can be made that the real 'disaster' year was 2015. And, yes, it just so happens that was the year Fonterra dived into Beingmate - but that's actually really not half of it.

I will explain in my future missive.

In the meantime we wait pensively for the Fonterra result.

These are very crucial times for Fonterra and the whole dairy industry. It is by no means clear that this story will have a happy end.

50 Comments

The other angle we need to shovel into the 'mixer' (as you so neatly characterise it) is the increasingly acrimonious and predominantly negative, yet largely low-information view being taken of Ag in general and Dairy in particular, by the Urban Hordes. This is compounded by the increasing squeeze on discretionary spend, most severely impacting the lower SES and by no coincidence, the most numerous urban demographic. Neither trend will be doing wonders for consumer spend choices for the domestic Fonterra markets and hence line-of-business valuations.

One needs to admit Fonterra is effectively an logistic company with two core tasks:

1. transport liquid milk from a farm to a plant

2. transform liquid milk to other forms in bulk

The core knowledge Fonterra holds are

1. how to build pasture based dairy farms effectively

2. how to dry milk to milk powder effectively

Fonterra is still very very young and inexperienced in areas outside of those two tasks. But, because of its status in New Zealand and the amount of cash it held in the best dairy season in 2015-16, it became very arrogant and god-like.

Now, it is paying the prices.

Cash in 15/16? I would have pointed to the lack of cash at that point. Paying a raw material price of almost half two years previous and still struggling to make a profit.

That is quite well thought out and executed post Xingmo, best I have seen from you. Trouble is I am waiting for the spin, like China could do it better?

Do they need some more OCR cuts to keep that debt managable....

We all need an ever-lowering OCR (and therefore interest rates).

Our main business in NZ, housing, demands it.

Don't keep all your eggs in one basket.

All good tourism will prop us up....

Until the Green Mobs, with renewably-fuelled torches and hand-wrought wooden pitchforks, come for Long-Haul Air Travel. Because reasons.....

Joe Blogs sitting elsewhere in the world looking at the world issues.. Spend $X on a holiday to NZ or batton down the hatches???

0% tourist number increase expected this year. That is a very optomistic view.

A deal popped up this morning 'Half price Thailand for 2 adults / two kids $680' That's cheap and it'll attract a lot of people over NZ prices.

The ol' New Zealand Cargo Cult Get-Rich-Quick mentality strikes again. No doubt we'll find some other commodity to turn into a damaging bubble destroying everything it touches. I keep hearing whispers about some country buying all the sheep milk we can produce for the infinite future. Can't lose.

yet we celebrate Foreign Banks trading in NZ making $5 Billion surplus per annum.

That would take Fonterra a decade to earn.

A bit of balanced discussion would help, maybe our NZ owned companies are being bled dry by Foreign Bank profits and super profits in the supply chain, not to mention having to compete in the international market.

Why have Foreign Banks for 1 example been given such a free ride in the NZ economy, to earn more profit than the entire NZ Trade Surplus (Deficit usually)each year.

The International globalists a not far away from killing all the geese that are laying their golden eggs.

We know how that story ended.

Yes we are told by Guy Trafford that we need dairy regardless of all the downside as it brings in $14 billion a year which although very little tax is paid by dairy keeps our dollar strong(ish). If this is all negated by outflows of up to $20 billion by foreign owned companies as reported last week then surely the banks taking out $5bill is something that needs correcting ASAP.

What is the share of the blame to be laid on the banks that have financed Fonterra for missing all the troubling signals all along ? What is the supervision/regulatory steps that were omitted in managing the Fonterra account in the banks ? What about RBNZ, which had allowed self certification by banks ? May be Orr has some inside information which prompted him to start the talk about increasing capital of the banks ? Meantime, will there be claw back of profits repatriated overseas, if required ?

Hmm, unlikely to be like Ross Asset Management, but you never know what auditors have missed that might come out on a closer FMA review on banks.

I know banks were given access to solid energy to allow the gnats a cash dividend flow to balance their losses.

Eventually put solid energy into bankruptcy.

Minister at time now left National soon after and works for a foreign bank which is weird.

Could this have happened to Fonterra, with kick backs a known motivation eg comisdions from lending targets shared through a back door.

Asset Sales to foreigners could be driven by same motivation, as doesn’t make economic sense what has happened to N Z last 30 years since R Douglas and Co got involved.

And continued thereafter.

Asset sales to foreigners is the same as borrowing from foreign banks, they own you both ways.

Any predictions where NZD will head with the release of this annual report?

I'm thinking down. But then, everyone expects it to be awful, so the only question is how awful..

A bad outcome is priced in, you can see this in the recent A$/NZ$ move (1.045 to 1.067). It will take something pretty sinister to see it sell further, Kiwi may even rally on an $800m write-down with no other bad news.

Looking at Fonterra's 2018 balance sheet I see d/d+e at 53.5%, moving up to 57% after an $860m impairment, so moving well outside their target. Also, unless I'm mistaken, their EBIT to EV multiple is 30x which is more than double the highest industry average of 14x (mostly around 10). This would indicate they haven't been generating a commercial return (paying too high for milk?)

Building to bail out, for sure.

SCF repeat, any one ?

This gonna drag on till next election and then the fun will really begin..

I dont have a good feeling about this .

As I said on this forum last week when the story broke , its not likely to be good news , but lets be optimistic .

Fonterra is to NZ what BHP is to Australia, we should all take an interest in its wellbeing , and they need to do what is right .

Writedowns are not , in themsleves, a train smash, but they do need to be managed and creditors need to be consulted ( esp Banks and Bondholders ) and the co-op should recognize "losses" called impairments in accounting parlance, as soon as possible.

Its no good to plaster over them or try and " trade out " when there are big debt issues or writedowns that can affect Banking covenants or the ability of the co-op to run as a going concern

Fully agree that "we should all take an interest in its wellbeing". It's not just the company, but the immense chain of rural businesses, small towns and provincial cities, that will surely be affected if it goes south bigly. And no-one should be cheerleading for those dominoes to get tumbling. If only for the simple economic reason that one of the first effects would be an increase in welfare rolls, paid for by general taxation, which is either funded by the person able to be spotted in a mirror, or by borrowing yet more from - well - anyone silly enough to put their hand in their pocket.

The Dairy industry pays little or no tax..we should survive. If its broken we have to let it fail - too much hand wringing by the milk shake brigade - to big to fail.

David : when Fonterrible first came into being , mate ... the prime minister Helen Clark agreed to them forming as a co-op representing NZ dairy to the world as a monopoly ... but she placed a millstone around their neck , the requirement to accept and process milk from any producer who approaches them ..

. . perhaps someone would interview Ms Clark , and ask the hard questions of her ...

While it did cost, it was miniscule. A red herring . A side show distraction.

Do you mind expanding Redcows. It would seem Fonterra was designed to fail from the start, albeit the dira dog was successfully sold to and accepted by us dairy farmers.

The net debt position of the co-op is not a problem if the debt is reflected in growth of income -producing assets .

Regrettably , the minority investments in dairy businesses in China ( where ripping off western businesses is well known ) or Sri Lanka or South Africa where culture , business ethics and corruption is endemic or direct investments in South America (a massive continent reliant on rain fed agriculture patterns far different ours) with unstable politics , currencies and economies with which we are unfamiliar , is foolhardy .

The business should focus local and trade global , and forget about trying to 'show off ' elsewhere

But their net debt is a problem. Greater leverage makes them riskier, will force up their risk premium and they will pay higher funding spreads (vicious cycle). EBIT has been falling as well, so higher debt hasn't been generating net income. With kiwi and interest rates lower their derivative liabilities and cashflow revaluation reserves will be higher as well - so another net tangible equity negative.

Consumer is greatest contributor to GDP.

Not farming, not dairy and not tourism.

People seem to forget this.

Difference between GDP and exports

I note yesterday that NZ "industrial" production down on Q2 compared to 2018 Q2.

Have to keep people borrowing and this is slowing (rate of growth)

It is this that makes economy stumble

But obviously the company has been doing well given it paid its CEO $40 million in the years that he was there? Great leadership, management and vision.....left the company in a great position...

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

Or do you just throw that amount of money around companies these days because we've all gone completely mad?

Cockies just got bamboozled by a smooth talking cloggy, the same accent that can be found anywhere in De Wallen. The directors need to be named and shamed but I cant get over Farelly thinking it was win win to send prime dairy cows to China.

That's just incredible. If they hire a CEO, pay him $43m in the 8 years 2011 til now ($5.3m per year??!) and he sinks the company in his time there, when all they had to do was sell milk, it's no wonder the company is stuffed, great decisions all round. Totally ridiculous. Karma might make a real mess of that Dutchman. If not then a farmer may do it instead, bet there would be a big queue for that.

He is really the Flying Dutchman, aye. Flew away with the loot.

Fonterra has a fundamentally flawed business model. Needing to take all milk from and pay the same to the farmer at the top of the Coromandel as the farmer down the road from the processor means they are uncompetitive compared to processors who can pick and choose - we'll see more and more of those picking off their low cost farmers, leaving them with the high cost ones. But hey, at least they have a nice shiny new building in downtown Auckland.

Affordable Housing that ? Is the New Minister for Housing interested ?

Theo Spierings has arguably done a great job...for the Netherlands' dairy industry, as it turns out.

Don't under estimate the role of an astute Finance Director.

The Board are responsible for 95% of the issues here, they employ the CEO, approve strategy and operate in the shareholders best interests (in theory)

You will find that most of the Boards in Aotearoa are sleeping, including the Bank boards. In most cases, it is one man or one woman show, orchestrated by the Aussie overlords. We are not seeing anything contrary to impress us. We are paying the price and will continue to do so, while the pollies and the execs make hay while the rot sets in.

TK- Or a CFO who knows what's going on.

Misdirection much?

https://www.google.com/amp/s/amp.rnz.co.nz/article/078f8d0a-2ea1-4530-9…

".....no explanation for the fall....the fundamentals of our business are strong..."

6 July 2019

A month later (12th Aug) Interest reported that FSF was looking at a loss somewhere between $595mill and a lot more.

What a team.

These asset write downs are just standard practice for a new CEO.

Make out the last lot screwed up and then as time goes on, the asset are revalued up and the the new CEO gets the performance bonuses.

It is almost as if Fonterra is getting as much bad news out there as possible, so as to drive their tradeable share price down. Then one of the usual suspects can pick them up cheap. A la Bonitas "Research Company".

One must remember that Fonterra still processes a lot of milk very efficiently, and sells it's products at a good profit. It's big problem has been that the top executives have usually been suspiciously naive and downright stupid when dealing with cunning dishonest foreigners.

The first chapter of the next volume of the Fonterra story began upon the leaving of the $43million man. They will shrink a bit, tighten things up, focus on production in NZ, and selling to foreigners who do the rest. In a few years, all will be forgotten again, and some visionary CEO will be found, who will invest with the same dodgy foreigners etc, etc. Great spectator sport.

"In looking back at Fonterra, I think a clear case can be made that the real 'disaster' year was 2015".

The scene was set well before 2015. It could be argued it was set up to fail from the start, through the design and promotion of dira by international experts, and naive industry leaders and politicians, followed by the subsequent scuttling of cooperative structure in favor of corporate greed.

But it's still a co-op, they all repeat it often enough it must be true.

Ok so I've never believed that either. And yes, well before 2015, the indicators of how badly they were doing were already apparent, but no one wanted to hear.

What is it about the management of New Zealand companies that try to expand overseas.

Its a never ending list of failures.

Air NZ & Ansett, Fonterra, etc etc

Strongly suggests too much not enough risk management & analysis and too much ego.

The big question here is who has PWC actually been working for, because clearly it hasnt been the Fonterra shareholders.

They have been less than transparent, and can't be trusted. Let's hope Colin Armers complaint to the FMA about PWC contempt behvaiour sees justice being served. Does anyone know PWC partner in charge of the Fonterra, and has he been knighted too?

As for ANZ economists, like fair weather sailors, they are just circling like vultures for another overseas client of theirs.

While Fonterra is clearly not in good shape, they'll be able to repair their balance sheet has the big capital spend is over. Hopefully this means delivering better value to the shareholder, NZ inc.

A good start would be shifting Head Office back to the regions, which should significantly reduce rents and staff salaries.

I have a suspicion that PWC (and other big auditing firms) earns more revenue handling bankruptcy procedures, than from regular audit work. Go figure..

'Standard & Poor's slates Fonterra over governance as another restructure looms'..NZ Herald Headline.

As usual the Rating Agencies are waking up late...Poor Banks which depend on these agencies to lend money to Corporates. And poor us, who will be bailing out the companies and the banks.

'Standard & Poor's slates Fonterra over governance as another restructure looms'..NZ Herald Headline.

And the story starts like this..'Fonterra had "lost its way" over the past seven years and governance factors had contributed to a "widespread misallocation of capital", ratings agency S&P Global says'.

As usual the Rating Agencies are waking up late...Poor Banks which depend on these agencies to lend money to Corporates. And poor us, who will be bailing out the companies and the banks.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.