Wow, what a year!

They should have bottled 2014.

On the back of sky-high global dairy prices the farmers were fair wheeling the money to the bank.

The records show that Fonterra farmers got a milk price payout of $8.40 per kilogram that year.

Hmmm. But good news for some can be bad news for others.

What was less prominently featured in Fonterra's annual report that year (the chairman's report didn't mention it at all) was Fonterra's profit figure. It was DOWN 76% at $179 million.

Amid the high prices and bumper production that year, Fonterra struggled with capacity constraints and its margins were squeezed by the prices. In some instances Fonterra was selling products at prices below the cost of milk.

Fonterra actually retained 53c of the milk price (yes, it should have been $8.93) in order to avoid it having to borrow money to pay the farmers!

So, to 2015 and Fonterra was off and running with a massive spend to increase its capacity.

Showing everyone the borrowed money

But it was paid for with borrowed money.

As I referred to in my earlier opine on this subject this week, Fonterra's preferred debt measure is "Economic Net Interest Bearing Debt", which Fonterra says "reflects total borrowings, less cash and cash equivalents and non-current interest-bearing advances, adjusted for derivatives used to manage changes in hedged risks".

In 2014 that figure stood at $4.732 billion. By July 31, 2015 the figure had incredibly blown out to $7.12 billion.

And if you are immediately thinking a fair bit of that money was splurged offshore, well, you are not wrong. But a perhaps surprisingly large amount was spent right here in New Zealand too.

Local investment during the 2015 year amounted to $900 million.

Spend, spend, spend

Big ticket items within this included $167 million for the Pahiatua dryer and distribution centre, $132 million for anhydrous milk fat, milk protein concentrate and reverse osmosis plants at Edendale and $122 million for a dryer at Lichfield.

And then yes, there was over $750 million to buy in Beingmate and $364 million for farm development and livestock purchases in China.

Fonterra's gearing ratio, which it targets at keeping between 40% to 45%, blew out to just under 50%.

The Fonterra annual accounts for 2015 show that the co-operative borrowed an eye watering $7.47 billion that year, while repaying $5.44 billion. Its cashflow sheet for the same year showed a net investment outflow of $2.04 billion.

How many businesses do you know that would virtually entirely fund such a massive acquisition of assets, all with debt?

The only way I think such a strategy could be even remotely justified would be if you had a guaranteed return on the investment, such as for example a power company commissioning a new plant for which it has a long-term supply agreement for all of the electricity produced. Even then there's risk.

For Fonterra, unless it could start getting immediate strong returns on these new assets, how was it proposing to get debt levels down, given that it was constrained from raising new funds by its farmer-only shareholder rules?

Milk tanked

And this is where the story all gets a bit ironic - but also very serendipitous for Fonterra.

Because of course, as we know, global dairy prices tanked in 2015 and then went even lower in 2016.

Now I said earlier that good news for some can be bad for others. Well, it works in reverse too, you see.

The reality is, I think those plunging global dairy prices stopped Fonterra from getting into the financial cactus, well, pretty much as early as 2015.

Yes, that's right, the tanking milk price, bad as it was for farmers, was a saviour for a horrifically overspent and overborrowed Fonterra.

Consider this: In 2014 Fonterra's cost of goods sold was $19.813 billion, reflecting the high cost of its milk. In 2015 that figure dropped to $15.567 billion and in 2016 it dropped again, to $13.567 billion.

So, that's right, Fonterra's cost of goods across that two year period dropped by 31.5%, by a whopping $6.246 billion.

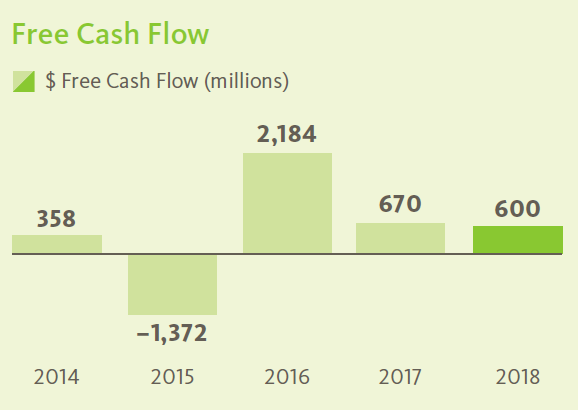

And boy, did that make a difference to the balance sheet. This five-year graph from the 2018 annual report tells the story rather well.

So, even though Fonterra's costs had fallen strikingly in 2015 it was still emptying cash because of the spending splurge. But by the following year, 2016, it was well into cash recovery mode. And of course this surge of cash enabled Fonterra to pay down debt.

It is worth suggesting though, if Fonterra had not blown out its debt so badly, it just might have been able to pay bigger dividends to the farmers in 2015 and 2016. Yes, Fonterra did help out the farmers through that difficult period - but if its balance sheet had been in better condition I would argue it could have helped out more.

But anyway, by July 31, 2016, Fonterra's Economic Net Interest Bearing Debt had been reduced to $5.473 billion and the gearing ratio was within targets, although not by a lot, at 44.3%.

The real test then for Fonterra in future years after 2016 would be what happened after dairy prices improved again.

This would then be the test of whether those assets it had splurged all that money on would be able to pay their way.

Assets that needed to perform did not

Well, I think we now know the answer. Those investments needed to be adding positively to Fonterra's performance so that it could maintain profitability as its costs of goods rose again. Clearly they did not.

And while investments such as Beingmate have turned into the disaster that many feared, the bigger question mark I think is how over valued some of the NZ assets might be. Because as Fonterra looks to strip itself back, it will be those assets that are the foundation point for the business.

We know that already Fonterra has earmarked NZ businesses for $300 million of write-downs (and it has netted off $100 million of gains on the sale of Tip Top ice cream to give a $200 million total figure).

How much more might be necessary?

I've talked further up about the $900 million spent by Fonterra in New Zealand in 2015. Well, that was actually part of $2.1 billion spent across three years.

Any borrow and spend philosophy doesn't normally have a happy ending. And this one doesn't look as though it will, even though Fonterra appears to have got very lucky for a while there.

As I said in my opine earlier this week, the time between bad decisions and the ramifications of those decisions can be quite a long time.

Now we wait to see how much stripping back will be required at Fonterra.

Who pays?

The latest talk of course is around job cuts.

For the record the 2018 Fonterra annual report showed the company had 18,200 staff of which 11,400 were based in New Zealand and 6,800 were overseas.

Among the NZ-based staff, 4,035 of them (over 35%) received salary and benefits of $100,000 or more for the financial year to July 31, 2018.

Among the overseas-based staff 1,729 (over 25%) received salary and benefits of $100,000 or more.

In New Zealand, 14 of the Fonterra staff received salary and benefits of $1 million and more, while among the overseas staff, there were nine employees receiving salary and benefits of $1 million or more.

Based on those figures, cutting some staff would certainly appear to be one way for Fonterra to save a substantial amount of money.

As I said earlier, I think we are now really only in the middle of a process for Fonterra.

The figures dating back to 2015 tell you this process is way overdue. But here's hoping for the sake of the economy that all goes well.

18 Comments

Very impressed with this and the previous article, David. Please accept my congratulations on this.

The question is why was this not noticed by the Banks which were financing the company continuously, how did they assess the company's performance and continued eligibility for the huge financing, what was the respective Boards in the company and the Banks doing to properly monitor the funds borrowed/lent and take corrective steps at the right time.

There seems to be many omissions and commissions in this sad saga.

RBNZ is also to be questioned for the self certification regime it had granted to the Banks.

What about the Auditors, PWC or whoever that is/was ? What is their share of blame in failing to protect the shareholders' interests ? What is their accountability and punishment if they are found to be deficient in their professional responsibilities.

So wrong at many levels..

I am sure Harvard will one day make out an interesting Case Study on Fonterra, if they are not already doing it.

You do realise that banks only finance c. $850m of $6.3b borrowing (2018)? So about 12%. The bulk is via their Euro MTN program.

Not a small amount even for these billion dollar banks here in NZ.. Even the MTN notes must have been subscribed to by many banks, right ? What about the lead bank, or trustee or whoever is charged with protecting those investors ? They are happy to be sleeping and let the investment go bad to worse to loss ?

How do you know the bank lenders are all NZ based? Fonterra probably have NZ's pre-eminent Treasury/Capital Markets operation and have a global panel of syndicate banks, their MTN's are held by Funds around the globe. Fonterra's problems stem largely from it's CEO/Board/poor governance.

Whether it is NZ owned/operating or overseas banks or investors of funds, whoever it is that has given the money to Fonterra, why have they not bothered to monitor the safety of their investment, is the question.

Great article as a follow-up. The key aspect for me is the apparent lack of a sensible business case for the capex, in terms of ROI, payback period, WACC assumptions and so on. Not that F is gonna show this publicly, but surely shareholders have some rights to demand it even if they have to sign NDA's for some aspects.

A few things that fonterra should done - stuck to their knitting, not tried to get too big for their boots and not trusted China, who are likely waiting in the wings to swoop now.

thanks David, please keep up the accuracy of your reports, a great reference point and benchmark when to gauge answers to forthcoming questions.

Cash Flow is still ok, with Capex reducing, it will free up $500 million p.a. represented as Depreciation in the reported net profit, or 1/2 of it at least.

The world will need more and more dairy as the population grows.

My concern would be did the Banks have a conflict of interest in terms of a big commission and interest earn by loaning Fonterra money, which overrode strategic advice that may have resulted in other options being considered, if push came to shove.

Banks have a very good eye for making a profit, which the quid pro quo is they neglect to give the right advice to the customer, especially when the customer has equity to conceal the banks agenda, which Fonterra does have.

Can you show me that growth? because I can show that milk alternatives like Soy now have %17 of US milk market and are the fastest growing segment.

Fonterra's recent alliance with A2 suggests they understand the need to diversify their product range to satisfy the milk market.

Fonterra has the plant to facilitate this, and while they may need to repurpose part of it to accommodate goat, sheep, plant or whatever milk, their additional capital outlay will be significantly less than competitors. Let kiwifruit, they just have to focus on quality and the markets will come. That means cleaning up our waterways to protect the image.

As for Fonterra's missed opportunity with A2, that's another story which only the board and management of the time can tell.

It’s interesting that Synlait appear to have difficulty achieving retail sales targets in China, tho they are 39% Chinese owned.

This is reported in stuff as a reason for their disappointing financial performance.

Perhaps the sales projections for dairy in China are overstated, blue skies.

Much of the NZ based investment was effectively legally required as Fonterra has to collect, with very few exceptions, every litre of milk farmers wish to send to it. Result is Fonterra has to overinvest in stainless steel to cope with unexpected milk flows. As for the banks they know that in the end the money paid to the farmers for their milk can be withheld if Fonterra needs it to pay down debt. The alternate milk processors can't take farmers leaving Fonterra en masse and they don't have to accept farmers so essentially the farmer's milk cheque is Fonterra's lender of last resort and the banks security blanket. This particularly applies to offshore lenders to Fonterra who are not also funding the farmers directly. The local NZ banks are more exposed to the farmers than they are to Fonterra as if Fonterra holds back cash from the farmers they won't have anything to pay the banks with and, in the short term at least, have little choice what to do with their farm. Synlait etc won't ride to the rescue although they may cherry pick the farms they want close to their plants. The majority of farmers can either supply milk to Fonterra or change what they farm.

Catch 22. DIRA is a travesty. Speaks volumes of the industry leaders who advocated for it. David’s analysis and opine is illuminating , but the train wreck was set up well before 2014.

Have they caught up?

Could this scenario ever happen again?

https://www.stuff.co.nz/business/farming/dairy/70762256/

Just curious, but you say this"Fonterra's preferred debt measure is "Economic Net Interest Bearing Debt", which Fonterra says "reflects total borrowings, less cash and cash equivalents and non-current interest-bearing advances, adjusted for derivatives used to manage changes in hedged risks"." Does anyone know the raw total of Fonterra's borrowing, at any time? If not why not, because the terminology used smells big time to me? If the figures given are eye-watering, just how bad are the raw figures?

We wait with interest on FMA investigation into PwC previous auditing practises, which probably enriched both sides of the equation for those managing the process.

With NZ business such a small circle, we may have ditched the Privy Council too soon. Thought is was right to ditch the Knight and Dame, which was milked by the politicians, but vested interests brought it back (without regard to public opinion) and are reverting to their dubious practises of handing get out of jail free cards.

Anyone know if there's a time for today's release?

... Synlait have released their figures : revenue topped a $ billion ... but analysts were disappointed that net profit for the year ended 30/6/19 only rose 10 % to $ 82 million.. not 19 % up , as forecast ...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.