By Michael Reddell*

A month or so ago there was a great flurry of media coverage when the US interest rate yield curve “inverted”. In this case, long-term government security interest rates (10-year government bond yield) moved below short-term government security interest rates (three month Treasury bill yield).

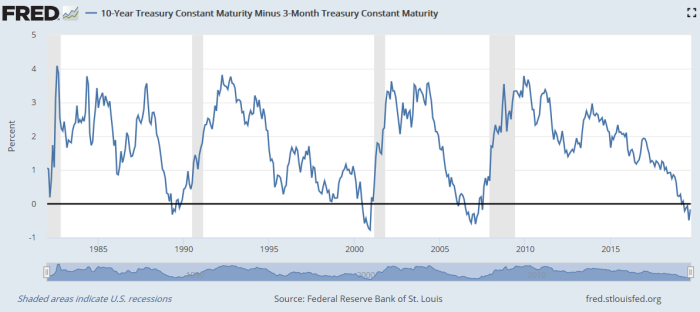

This was the sort of chart that sparked all the interest.

The grey bars are US recessions, and each time the long rate has been less than the short-term rate a recession has followed. This chart only goes back to 1982 but it works back to at least the end of the 1960s. There haven’t been any recessions not foreshadowed by this indicator, and there haven’t been times when the yield curve inverted and a recession did not come along subsequently (sometimes 12-18 months later). Who knows what will happen this time. It is, after all, a small sample (seven recessions, seven inversions since the late 1960s), and there is nothing sacrosanct (or theoretically-grounded) in using a 10 year bond rate. Use the US 20 or 30 year government bond yields and right now the curve wouldn’t even be (quite) inverted.

But there are good reasons why changes in the slope of the yield curve might offer some information. A long-term bond rate isn’t (usually) controlled by the central bank or government and might have a fair amount of information about what normal or neutral interest rates are in the economy in question. By contrast, short-term rates are either set directly or very heavily influenced by the authorities. When the short-term rate is unusually far away from the long-term rate one might expect things to be happening to the economy, whether by accident or design.

Back in the day, when we were trying to get inflation down in New Zealand (late 80s, early 90s), the slope of the yield curve was for several years, off and on, a fairly important indicator for the Reserve Bank. At times we even set internal indicative ranges for the slope of the yield curve (at the time, the relationship between 90 day commercial bill yields and five year government bond yields), and for a while even rashly set a line in the sand of not allowing the short-term rate to fall below the long-term rate.

We used this indicator because neither we nor anyone else had any idea what a neutral rate (nominal or real) would prove to be for New Zealand, newly liberalised and then post-crash, money supply and credit indicators didn’t seem to have much content, and we didn’t want to take a view on the level of the exchange rate either. But whatever the longer-term interest rate was, if we ensured that short-term rates stayed well above that long-term rate, we seemed likely to be heading in the right direction – exerting downward pressure on inflation and, over time, lowering future short-term rates as well.

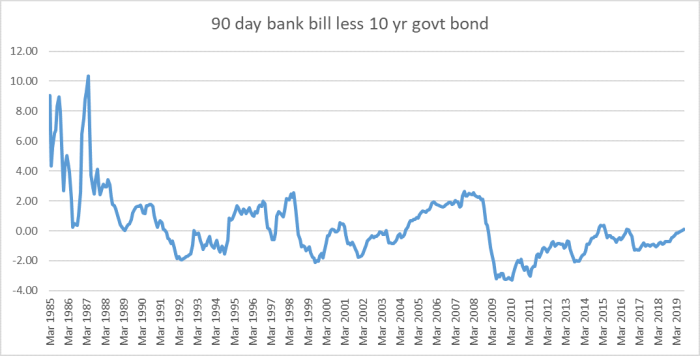

But what about the New Zealand yield curve slope now? Here is the closest New Zealand approximation to the US chart above, using 90 day bank bill yields and the 10 year (nominal) government bond yield. I’ve shown it the other way around – 90 days less 10 years – because that is the way we did it here (partly because of the long period, until 2008/09, when short-term interest rates were normally higher than long-term ones, rather different to the US situation).

I can’t easily mark NZ recessions on the chart, but there were recessions beginning in 1987, 1991, 1998, and 2009, and each of them was preceded by this measure of the yield curve slope being positive. But, for example, the slope was positive for four years in the 00s before there was a recession. Against this backdrop, there isn’t really much to say about where we are right now (just slightly positive). And take out whatever credit risk margin there is a bank bill yield (20 basis points perhaps?) and the slope of the curve would be dead flat.

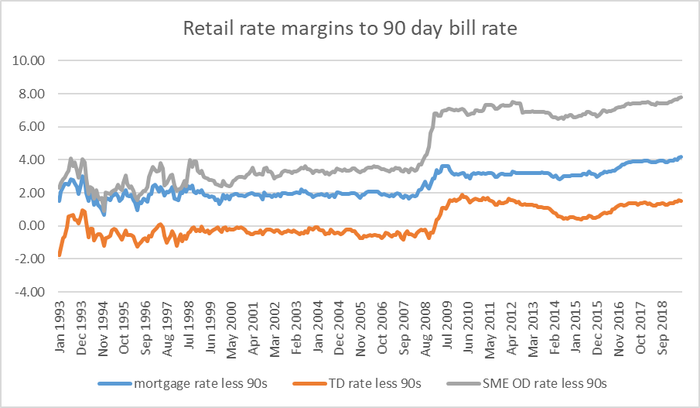

But what about a couple of other possibilities. Unlike the 90 day bill rate, term deposit rates and bank lending rates directly affect economic agents in the wider economy, and as I’ve shown previously the relationship between the 90 day bill rate and term deposit (and floating mortgage) rates has changed a lot since 2008/09.

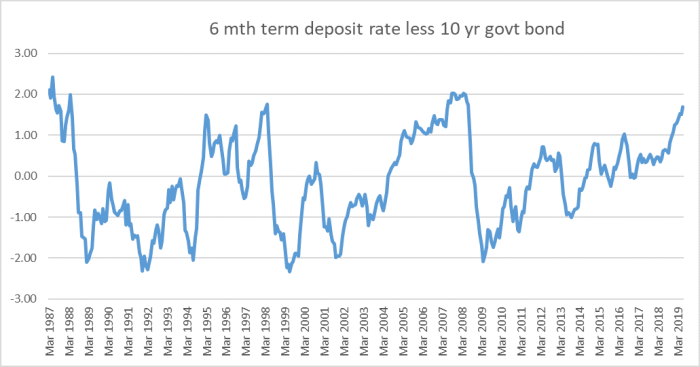

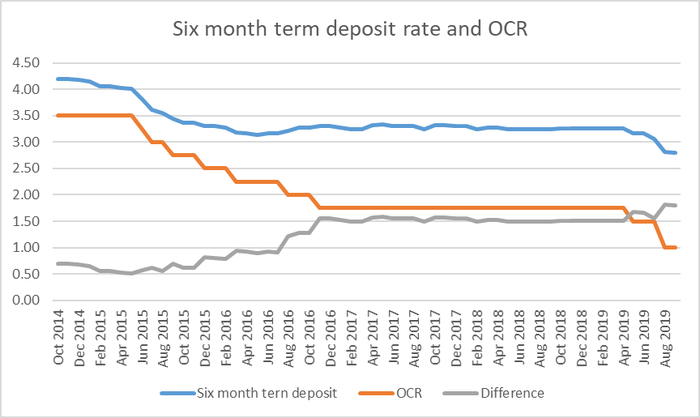

In this chart (constrained by data availability to start in 1987), I’ve taken the six month term deposit rate (from the RB website) and subtracted the 10 year government bond yield).

That starts looking a bit more interesting. The level of this variable – even after the recent Reserve Bank OCR cuts – is close to a level which has always been followed by a recession. (It is a small sample of course; even smaller than in the original US chart).

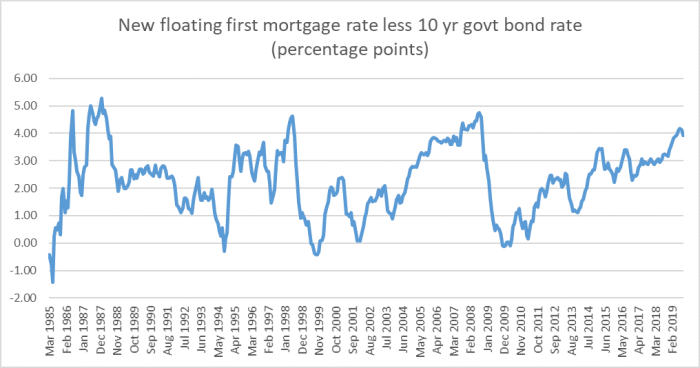

What about the relationship between the floating residential first mortgage interest rate and the 10 year bond rate? Here is the chart.

The only times this indicator has been higher than the current level – even after the recent OCR cuts are factored in, as they are in the last observation on the chart – have been followed by pretty unwelcome economic events (the 1991 recession wasn’t strongly foreshadowed by either this indicator or the previous one).

It is a small sample, of course, and there are no foolproof advance indicators. But if I were in the Reserve Bank’s shoes right now, I would take these charts as yet further warning indicators.

On which count, it is perhaps worth keeping a chart like this in mind.

We’ve had 75 basis points of OCR cuts this year but only about 45 basis points of cuts in the indicative term deposit rate (latest observations from interest.co.nz). It is not as if these retail interest rates are at some irreducible floor – retail deposit rates in countries with much lower policy rates are also much lower than those now in New Zealand. It is a reminder that, against a backdrop of a very sharp fall in New Zealand long-term interest rates (real and nominal) – even after the recent rebound the current 10 year rate is still more than 100 basis points lower than it was in December – monetary policy adjustments have been lagging behind. Long-term risk-free rates have fallen, say, 110 basis points (almost all real), and short-term rates facing actual firms and households are down perhaps 40-60 points (floating mortgage rates nearer 60).

The Reserve Bank cannot (especially after a decade of persistent forecast errors) have any great confidence in any particular view of neutral interest rates for New Zealand. With inflation still persistently below target and (as the Governor and Assistant Governor have recently highlighted) falling survey measures of inflation expectations, there isn’t a compelling case for the Bank to have lagged so far behind the market, allowing short-term rates to rise further relative to long-term rates. The Governor has appeared to suggest that the Bank will only seriously look again at further OCR cuts at the next Monetary Policy Statement in November. I reckon there is a much stronger case than is perhaps generally recognised for a cut at the next OCR review next week.

* Michael Reddell is a Wellington-based independent economist and commentator on economic and financial affairs, blogging at www.croakingcassandra.com. He previously worked at the Reserve Bank where he had held various economics and management positions over many years, including Head of Financial Markets and manager responsible for economic forecasting. This article was first published on Croaking Cassandra and is used here with permission.

24 Comments

If i could sum up the logic of this article (and most commentators):

- historically recessions have been associated with flat or inverted yield curves as monetary authorities over-tighten and the economy stalls

- Therefore monetary authorities should pre-emptively ease policy every time the bond markets sniff out a slowdown

- bingo, no more recessions ever again!!

I think the complete failure to acheive their stated objectives of central banks worldwide for over a decade makes a very strong case for getting rid of central banks entirely.

If it was just the failure to achieve the goals, you could indeed make a case for getting rid of them. But...

They aren't just failing their goals, what little they are doing is either completely ignored, or sees an inverse outcome to that which they intended.

The real question is why haven't we already disposed of them?

Because we have a tendency to believe anyone who says fancy words, earns six figures and wears a flash suit - bankers and politicians alike

Giving the Boomers a break this week?

As long as they quit moaning about easy we have it today :)

I dont understand this one bit ................ Why are we using our ammunition now , and not use it when we really need it ?

Why does the Governor not just get wheeled out and tell us exactly WTF is going on ?

CPI is less than 2%, RBNZ drops OCR until CPI 2% or more, easy to understand.

Do you have money in Term Deposits Boatman? If so your "confusion" may be more about lack of returns rather than real confusion.

So cutting the major constituent price of the very thing that underlies our economy ( and so the CPI) - the price of credit/debt - will spur 'inflation'?

That's like a retailer having a Sale! and hoping that prices rise as a result....

At what stage do 'we' see that increasing the input constituents of goods and services pushes up prices, not lowering them, and so interest rates should rise?

Never, is the short answer! Because we've gone so far in the wrong monetary policy direction that we'd all be dead if we tried to reverse course. Only 'onward into the unknown' is available to us now; hoping that a miracle happens to validate all this erroneous policymaking. And guess what? A miracle ain't comin'....

You are confusing the price of goods and services with the price of debt. They are not the same.

Do you have money in TDs? It may explain your confusion.

Because it would freak everyone out and everything would crash. What they are trying to do is to get everyone to spend up at the low interest rates. People aren't taking the bait in mass.

I think the RBNZ boys & gals might come in handy shortly by printing more NZ notes. Yeah? Anyhow....

The way things are going (and for me they seem to be going in all directions at the same time - a bit like an explosive device) no one's really got a read on what's about to happen, even when they tell you they do. There is days & days of information out there to inform you about what's going to happen tomorrow, or next month or next year - all with the invisible tagline that they really haven't got a clue, and that's exactly as it should be. They may have different triggers & come to be known by different names within history, but essentially it is all underwritten by greed. Greed is the base ingredient that tips the possible into the impossible, the big into too big & the hope into hopeless. It usually appears towards the end of the good times, which as we all know, are periodical in nature. The article's mentioned history is interesting in that it maps the last 50 years or so of our time, but we need to factor in the other 50 years (which looking back) were pretty horrible in places, if we are to consider what I would term a lifetime cycle.

Selective history is one thing, reality is another.

When it comes to high quality independent macro/political research, Mike Reddell is in a league of his own. I rate his research very highly, way higher than anything from a commercial bank or RBNZ and I would know.

Independent. It may make a difference.

The Reserve Bank cannot (especially after a decade of persistent forecast errors) have any great confidence in any particular view of neutral interest rates for New Zealand. With inflation still persistently below target and (as the Governor and Assistant Governor have recently highlighted) falling survey measures of inflation expectations, there isn’t a compelling case for the Bank to have lagged so far behind the market, allowing short-term rates to rise further relative to long-term rates.

Curves Need No R-star; Economists Need R* To Decode Curves

From the point of view of orthodox policy, it has been the needs of monetary policy that drove everything lower and by extension upside down. The yield curve has only steepened in the 21st century, and yet the economy of this period has been slower and weaker (in sustained fashion) than at any point since the 1930’s. It sets up an inversion to where the yield curve gets steeper the more the economy slows, which by mainstream definitions can’t be the case.

To solve the “equation” we merely have to frame all references to the nominal. Thus, the steepness of the yield curve itself is a byproduct of monetary policy effects on the shorter rates. For policymakers that has meant R*, the assumed natural rate of interest.

We have to keep in mind that R*, or R-star as it is sometimes notated, is not something that can be observed directly, but despite that limitation is immensely important to monetary policy. It is supposed to define the balance between inflation and deflation; if monetary policy can get “real” rates below R* it is thought of as stimulative. Conversely, if the “real” policy rate is above R* monetary policy is believed functionally restrictive.

Given that framework, if R* is falling then each time the Federal Reserve or any other central bank wishes to “stimulate” it must do so with lower and lower short-term rates in order to get the policy rate underneath where it assumed the natural rate has fallen. Once at the Zero Lower Bound (ZLB), policy is constrained in nominal terms leaving authorities to undertake unconventional policies so as to push “real” rates down where they are calculated to be stimulative.

According to calculations performed by the San Francisco branch of the Fed, R* is indeed falling and has been doing so for decades. As a result, each time the US economy is confronted with cyclical economic weakness such as the Asian flu (which resulted only a near-recession) or the dot-com recession, the “required” monetary policy response has been that much more so. The result is what we see of the yield curve, where it steepens due to the weight of policy on the front end essentially pulling it downward.

But is this really true? There isn’t a whole lot of sense in this formulation. You can see at times that it amounts to reverse engineering rather than defining an internally consistent and logical explanation of the last thirty years, starting with the fact that economists have no idea what might have caused R* to decline in the first place. Further, the bond market just doesn’t work that way, as again interest rates define opportunity rather than being anchored almost exclusively to monetary policy.

A more common sense explanation would be the opposite direction for the chain of causation: the economy slows in structural terms causing the bond market to reduce in its overall nominal framing, where cyclical weakness is therefore more pronounced over time leaving the Fed not to “stimulate” with lower and lower policy rates but to announce in review what has already happened. In short, they are calculating a lower R* as a result of being unable to square reality with the orthodox parameters of how orthodox theory posits reality is supposed to be.

R* is just the plugline or balancing factor that attempts to make sense of why neither ultra-low interest rates after the dot-com recession nor QE in the aftermath of the Great “Recession” failed to work as they “should” have. For policymakers, policy rates went low and lower but since no great recovery resulted, especially from the QE’s, it is merely asserted that R* must have been that much lower still. From this view, QE was surely powerful “stimulus” but it didn’t appear to have worked, therefore R* was just that much lower than QE got the policy rate to. If “real” policy rates had been pushed down to -10%, the still lack of recovery would have left Fed officials claiming R* surely was -10.01%.

This reverse engineering is actually quite common and necessary for a philosophy that is so often backward. What comes first is the lack of growth, leaving economists to calculate an R* based on wherever interest rates happen to be due to their reactionary efforts trying (and inevitably failing) to do something about it. We can observe this relationship in any number of important ways:...

Ha, yes, my way of thinking about this is that it is easy to get the direction of causation wrong in a cyclical process. Does decreasing A cause decreasing B which then causes a further decrease in A, or is it the other way around, and decreasing B drives a decrease in A which then drives a further decrease in B?

To me it seems more likely that a slowing economy causes falling interest rates, ie the speeding up or slowing down of the economy is the cause and interest rates the effect. So, manipulating interest rates can certainly bugger things up, but not really help that much.

Good point...in summary, all economists and central banks analyse with 2-dimensional models, which is why they are wrong most of the time. It’s never just A+B=C

Indeed:

What Current Interest Rates Really Mean

It is rote mainstream recitation that low interest rates equal stimulus while high interest rates demonstrate the opposite to some degree of “tightness.” As Friedman pointed out, this is entirely backward as demonstrated conclusively by economic history:

Initially, higher monetary growth would reduce short-term interest rates even further. As the economy revives, however, interest rates would start to rise. That is the standard pattern and explains why it is so misleading to judge monetary policy by interest rates. Low interest rates are generally a sign that money has been tight, as in Japan; high interest rates, that money has been easy.

In the US during the Great Collapse of the early 1930’s, money supply fell by one-third but the Fed believed monetary conditions were accommodative, “point[ing] to low interest rates as evidence that it was following an easy money policy and never mentioned the quantity of money.” At the opposite end, during the Great Inflation interest rates only shifted higher and higher.

But that is only part of the missing economic equation. Not only are there dire misconceptions about interest rates as they relate to monetary conditions, there is an even bigger misread of money itself. In his 1998 article, Friedman chastised the Bank of Japan for not expanding the monetary base, relying too much instead on interest rate policy alone (just as the Fed would repeat throughout the first phase of the financial crisis).

The answer is straightforward: The Bank of Japan can buy government bonds on the open market, paying for them with either currency or deposits at the Bank of Japan, what economists call high-powered money. Most of the proceeds will end up in commercial banks, adding to their reserves and enabling them to expand their liabilities by loans and open market purchases. But whether they do so or not, the money supply will increase.

There is no limit to the extent to which the Bank of Japan can increase the money supply if it wishes to do so. Higher monetary growth will have the same effect as always.

This is, of course, quantitative easing. Friedman argued that intentionally expanding the level of bank reserves, or high-powered money, would offset the “tightness” exhibited via low interest rates in Japan. The Bank of Japan followed that advice only three years later, as has the United States and Europe less than a decade after that. None of it has worked, as instead interest rates and bond yields continue to decline sharply all over the world.

So if we view Friedman as correct about the interest rate fallacy, as surely he was, then he must have been mistaken about what constitutes “high-powered money.” In the global, wholesale banking system of a credit-based reserve currency it is not difficult to figure the flaw. Bank reserves are not money nor can they ever be; they require a subsequent step to be useful in any economic fashion. That step is bank activity, whether in interbank liquidity or raw lending, it was always inaccurate to simply assume that banks respond favorably and without question to the level of bank reserves. Orthodox theory posits banking as something like a rubber stamp, just passing along whatever the central bank does without question or comment, when it actually functions of its own accords and factors – making those protocols the actual, functional money supply.

Yes, indeed. And what is primary mechanism for increasing monetary base?

The creation of debt for mortgages at ever higher valuations.

This creates NEW money person has not earned which they can then spend.

In reverse, if prices do not rise, mortgage advancement to buy house does not have to go up each year.

BIG problem. Velocity of money drops. Virtuous circle is turned to vicious.

THAT is why they cut interest rates. But they have run out of rope

There is no doubt lower interest costs stimulate businesses and consumers to spend. They gain surplus cash and some is spend, some saved or used in debt reduction. Lower rates mean the threshold return for an investment to show a positive return decline, so borrowing increases. What part of that is confusing? Sorry but slippage between ocr and retail interest rates mean rates need to move further.

A lot of old timers on this site have money in term deposits so they want the OCR and TD rates to be around 100%. If the RBNZ does not give them that rate they whine and make up BS arguments why increasing OCR would create a Utopia. Sad really.

If that's the case there isn't a level low enough to satisfy central banks. The RBNZ has nearly cut the OCR in half twice since April 2015 and the market is forecasting more. So called "stimulus" which fails it's task cannot not be working, if repeated official interest rate cuts give cause for perpetual cuts.

Furthermore, the net present value of term government and personal liabilities double every time rates are cut in half. This is so for outstanding debt and pension claims. Even workers see that the present value of their future stream of wages rises without compensation today.

People will persist in believing RBNZ and central banks drivel about inflation targeting.

Cuts in interest rates are to increase credit - ie debt being taken on. That is it.

RATHER than giving money (not debt) to people who will spend it in real economy, rather than making asset prices go up which primarily benefits the top 30% of wealth holders in an economy.

The priesthood of course, will not allow that, so on we go with the policies that have failed for 44 years.

2% GDP growth today? And 2.7% next year - which , you will note, is always going to be better than this year according to economists who get paid to be talk nonsense and unreality. WHY is it going to be better next year?? We are never told. While they are at it, they could get the Treasury embarrassing forecast out from 2017 in which it saw blue skies for 4 years and 3.5% GDP growth for 4 years. Ha. What world has is a shortage of effective demand. Why? Because wages do not grow enough to buy all extra stuff produced.

Cutting interest rates from low levels to silly levels is not going to cut it I am afraid. New policies required.

Simple, get rid of central banks. Keep an independent regulatory body for the financial sector, but delete the entire notion of monetary policy.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.