Today's Top 5 is a guest post from the team at Massey University's GDP Live.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

1. Nothing to fear except fear itself.

Photo by Alexandra Gorn on Unsplash

Government imposed lockdowns have proven to be an effective way of controlling coronavirus where the number of cases in the community are beyond a manageable limit. But is the economic toll worth it?

Recent research suggests that despite what we have been told, lockdowns only account for a small portion of the economic cost of COVID-19. By far the biggest economic effect – around 60% – is attributable to people voluntarily self-isolating because of fear of infection if they leave their homes.

This suggests that the best strategy for governments to limit the economic shock is to reduce people’s anxiety around going about their normal business by providing evidence-based reassurance that the risks of catching the virus are low as long as they take sensible precautions: social distancing, wearing a mask and washing hands.

The research by University of Chicago economists Austan Goolsbee and Chad Syverson used cellphone records to track customer’s visits to individual businesses across 110 different industries and comparing this to adjoining states that did not lock down.

“While overall consumer traffic fell by 60 percentage points, legal restrictions explain only 7 percentage points of this. Individual choices were far more important and seem tied to fears of infection. Traffic started dropping before the legal orders were in place; was highly influenced by the number of COVID deaths reported in the county; and showed a clear shift by consumers away from busier, more crowded stores toward smaller, less busy stores in the same industry. States that repealed their shutdown orders saw symmetric, modest recoveries in activity, further supporting the small estimated effect of policy. Although the shutdown orders had little aggregate impact, they did have a significant effect in reallocating consumer activity away from “nonessential” to “essential” businesses and from restaurants and bars toward groceries and other food sellers.”

2. Are we there yet? Superforecasters optimistic of a vaccine by October.

Photo by CDC on Unsplash

As the world continues to cope with the disruptive effects of the pandemic, ultimately our only hope for a return to near-normality is an effective, widespread vaccine.

According to Forbes magazine, superforecasters are more optimistic than they were that a vaccine (at least enough to inoculate 8% of the US population) could be available by the end of the year.

The downside is it would still take many more months for the vaccine to be widely available in the US and it is looking increasingly likely that regular top-ups will be required to maintain immunity.

While New Zealand is pursuing its own vaccine strategy we shouldn’t hold our breath we will have access to a widespread vaccine any time soon. Our best hope is to double-down on our elimination plan.

“The superforecasting group were asked, “When will enough doses of FDA-approved COVID-19 vaccine(s) to inoculate 25 million people be distributed in the United States?” Their answer (as August 12, 2020) is

Before 1 October 2020: 1%

Between 1 October 2020 and 31 March 2021: 44%

Between 1 April 2021 and 30 September 2021: 37%

Between 1 October 2021 and 31 March 2022: 11%

Not before 1 April 2022: 7%

The pessimistic extreme, not before April 2022, was the most common answer when the forecast begin back in April. Over time, however, members of the group have adjusted their predictions to more optimistic ranges. The current favourite, between October 2020 and March 2021, was the least favourite choice through June. This illustrates that superforecasters do not lock in to one opinion. Ego often leads people to defend their past statements even when evidence has changed. Superforecasters avoid this bias.”

3. Antitrust enforcement in the Internet era.

Photo by BP Miller on Unsplash

There is increasing disquiet globally about the distortionary strength wielded by the big tech titans.

Contrary to United States’ robust “trust-busting” history where monopolistic companies were broken up to ensure competition in the market, US regulators are facing criticism for allowing big tech companies to freely amass market share on the narrow interpretation that “consumer welfare” is not being harmed.

Online giants like Google, Amazon and Facebook have shown that once online platforms reach critical mass it’s “winner takes all”. Even so, it’s hard to show that consumers are losing out. Users on the whole have enthusiastically embraced platforms which allow them to access stuff at no, or very low, cost.

The real concern is that these firms effectively squash competition by raising the barriers to entry for new entrants and then buying out any start-ups that look like they may offer real competition. While prices for consumers may stay low, their size and disproportionate control of labour means they are having an even more worrying effect of depressing wages and increasing the levels of inequality.

The Economist reviews the increasingly partisan agendas playing out through the anti-trust debate in the US – Republicans tend to be against and Democrats for:

“Research by the OECD, a club of mostly rich countries, finds that between 2000 and 2014 the share of sales accounted for by the top eight firms in a given industry rose by four percentage points in Europe and eight percentage points in North America.

Many antitrust experts are unconcerned: industrial concentration, they argue, does not tell you how competitive the market for a particular good is. But some economists have blamed falling levels of competition for far-reaching economic ills, such as stagnant labour markets and growing inequality. In a paper published in 2019 the late Emmanuel Farhi of Harvard and François Gourio of the Federal Reserve Bank of Chicago argued that the rising market power of big companies was linked to low interest rates and weak investment, factors shaping the whole economy.”

4. Why fiscal stimulus won’t cause a surge in inflation.

Central banks and governments around the world have pumped eye-watering amounts of money into their economies in an attempt to cushion the recessionary effects of the pandemic. This is leading people to worry that, as in the 1970s, high inflation is just around the corner.

However, despite all of the trillions of dollars of stimulus, demand remains weak globally as social distancing and consumer caution over future job prospects leads to money being saved rather than spent.

And it seems New Zealand businesses don’t believe there will be inflation anytime soon. According to the RBNZ, businesses expect the rate of inflation to decline over the next 1-2 years:

Source: RBNZ Survey of Expectations

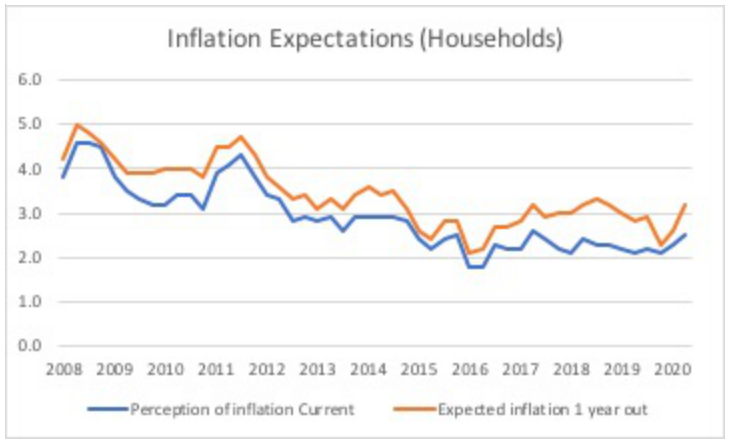

And while households expect inflation to increase in the next year, it is still in line with expectations of previous few years:

Source: RBNZ Household Inflation Expectations

In addition, an article from CNBC argues that the link between money creation and consumer prices has weakened over recent years. It’s because of this that the anticipated inflation never arrived following the 2008 recession despite massive fiscal stimulus. Asset prices went up, but that’s about it:

“Banks have kept much of the cash created by the Fed’s recent purchases “on account” in the form of excess reserves, instead of lending it out into the economy.

“The experience of the last decade is that central bank balance-sheet expansion certainly need not generate a period of excess inflation, and, in fact, even with a big balance sheet, it might still be hard to get the inflation that you want,” Guha said.

While recent stimulus measures might not directly boost prices for consumers, some say it is causing inflation in other places like the stock market or housing market.

“I think we’re looking at very significant increases in asset price inflation,” Citi’s Mann said.”

5. Will Covid-reset herald a new era of creative destruction?

Photo by BP Miller on Unsplash

While the economic destruction caused by the pandemic will be incredibly painful for many, there is a school of thought that suggests it will also open the way for new innovative firms to emerge.

“Creative destruction”, the term first coined by Austrian economist Joseph Schumpeter, is the process dismantling long-held business practices in order to make way for more efficient ways of using resources.

Derided by some as minimising the human impact of economic destruction there is no doubt that economic crises can force much needed structural change which otherwise is often blocked by the beneficiaries of the status quo. Without creative destruction many “sunset industries” from bricks and mortar retail, fossil fuel production to mass tourism would continue despite their environmental or productivity drag on society.

CBC reports:

[According] to the theory of creative destruction derived by Austrian economist Joseph Schumpeter in 1942 from ideas proposed by Karl Marx, economic and technological progress demands that businesses must die and industries and paradigms must be swept away to make room for new ones.

Canadian economist Peter Howitt, recent winner of the Frontiers of Knowledge Award for his work proving Schumpeter's principles in the real world, said that while the creative destruction process is happening all the time, economic crises speed the process along.

"When old firms or technology or skills or whatever are hanging on, they can last a long time until things get really bad," said Howitt. "It's typically during a recession that a lot of the destruction takes place."

The implication is that while those in retail or the oil business or the real estate industry may insist that the COVID-19 lockdown has been the cause of their failure, the economic crisis may instead be a trigger, a catalyst for a process already underway.

19 Comments

GDP? Old fashioned not very useful measure. How about you guys switch to GNH (Gross National Happiness)?

Exactly. It's a lazy indicator to make politicians and economists feel good about themselves. On the GDP Live website it states 'GDP is used as a measure for comparing how well, or poorly, a country is faring compared to other countries.' Really? What kind of goal to work towards as a country is merely comparing ourselves to others?

GPI (Genuine Progress Indicator) is another far more useful metric in addition to GNH. Measuring things like:

- environmental degradation

- income distribution and inequality

- volunteerism rates

- crime

- solid waste per capita

- unemployment rates

- housing cost to income ratios

- small business success rates

- etc.

But no, we keep banging on about GDP and productivity, despite all the evidence pointing towards environmental and social limits to both.

Rant over.

That's rubbish sorry. GDP per capita and productivity are very highly correlated to a country's wealth, infrastructure, health care, life expectancy etc etc. and many of the factors you identify will be captured by GDP per capita over the medium term anyway. If you want to introduce some measure of qualitative variables not captured by GDP, then find another one.

Easy. Rate of resource depletion, overlaid with rate of population increase.

Which makes your comment rubbish.

GDP measures upper-deck activity, while failing to measure the coal left in the bunkers, or the diminishing freeboard. In other words, it's at best fooling ourselves, at worst a lie.

Wrong. By all means feel free to weight GDP by any metric you feel important (resource use, carbon) - it is still the sum of our endeavors per head.

No it isn't. The Cant'y 'rebuild' was good for GDP - indeed if we all went out and trashed each other's everything, GDP would go through the roof.

Do you think that is/would be a valid measure

Mantra-chanting, no more, no less

You're not thinking it through. We do get a GDP boost from additional Govt spending, but that is finite as at some point investors will stop lending to us (don't bring Covid into it, we are only getting away with that because everyone is doing it). GDP is what it is, you can choose to ignore it if you want, but that's like pretending you know better than your doctor.

If you were replying to mine above, you need some basic comprehension skills. I never mentioned the virus, nor Govt 'spending'.

Please read my post, without your obvious assumptiveness.

GDP as a measurement tool certainly has it's limits, however it is much less subjective than GPI or GNH. Personally I think it's almost a crime that Govts focus almost solely on total GDP rather than GDP per capita or GDP per hours worked (i.e. Productivity). I think if we focused on GDP per capita and productivity the indicators mentioned in your GPI would likely follow. The problem with focusing on total GDP growth - as our Govts do - is that if we pump up population, consumption, environmental destruction etc we can grow total GDP quite fast while making us all poorer at the same time.

Everything has limits! And some people like to pull magical ideas out of their arses and call it fairy dust.

Neither of which implies that that GDP as an economic measure, isn't useful. It's not the only measure. There is no measure that can encompass the complexity of human economy and productivity.

Agreed, except productivity now is fossil energy, not human labour.

Economists are still back about the time of Great Expectations.....

Agree. GDP becomes a fudging of the numbers when productivity isn't increasing.

As Michael Reddell said it, "when it comes to living standards, productivity isn't everything...but it's almost everything". (loosely quoted)

We already started to collect a range of wellbeing indicators:

https://wellbeingindicators.stats.govt.nz/

Try any parameters .....uncertainity, printing of money, no control on panademic, inequality, asset class moving higher and economy moving lower...... it will get worse before getting better.

Wait and Watch. Meanwhile take opportunity of heated asset class be it stock or housing and make money while it last.

1. This is what I said on here back in March (to much derision I might add) ie that the psychology of fear would cause more self-imposed isolation and withdrawal from economic activity than lockdown long term (if the lockdown was successful). And that faith in the authorities ability to safeguard and prioritise citizens health would lead to a faster economic recovery or at the very least, less economic harm. Obviously, our government isn't perfect and mistakes have been made, as you would expect. However, when you look at the countries whose leaders have demonstrated poor communication and inconsistent health policy, they have both higher rates of infections (with the knock on health costs on that later no doubt) *AND* they have failed to save their economies.

4. I also agree that inflation is unlikely in the near term.

#3 : Anti-Trust Action in US

United States v. Microsoft Corp - 2001

Worth the Read

https://en.wikipedia.org/wiki/United_States_v._Microsoft_Corp..

Market Cap of Microsoft 23 March 2020 = USD $1.1 trillion

Market Cap of Microsoft 20 August 2020 = USD $1.65 trillion

The Anti-Trust case against Microsoft was concerned with Microsoft's bundling of Internet Explorer within its Windows System. History tells us that Internet Explorer died and others have moved in to occupy that space

Lets hope that the current crisis does speed creative destruction in our economy. I am concerned that current govt policies - wage subs, cheap business loans etc will only serve to prop up low productivity businesses at the expense of innovative and productive businesses and thus minimise any potential increase in creative destruction and its consequent long term benefits.

Not quite. All our existing infrastructure represents energy-expended and resources-committed. Therefore, re-purposing and triage will be worth considering before destruction. In physical terms, that is. And all else ultimately depends on things physical

Inflation is dead, except in stock markets and people's expectations.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.